Stocks & Equities

His last 645 trades, dates & performance:

….view all 645 trades HERE

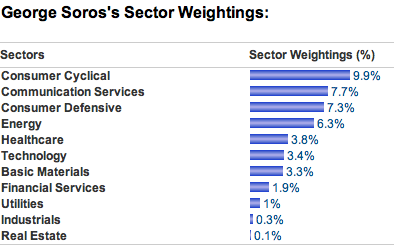

George Soros is known for the unmatched success of his Quantum Fund. A hedge fund guru, he is recognized for having the best performance record of any investment fund in the world over its 26-year history. A mere $1000 invested in 1969 when Soros established the Quantum Fund would have been worth $4 million by the year 2000. During that time he achieved a cumulative 32% annual return.

….view all 645 trades HERE

Sometimes charts, graphs, and images line up persuasively, and for U.S. stocks John makes the case that this is one of those once in the blue moon times:

A few examples:

Broadening triangle

This one is from David Chapman, manager of the Millennium Bullion Fund. As he describes it in a recent SafeHaven article:

A broadening triangle pattern is rare and if it does occur it normally is not seen over such a long period of time. This pattern saw its first peak in 2000 (A) followed by the initial bottom in 2002 (B) followed by the huge 5 year rally that topped in October 2007 (C) then the 2008 financial crisis crash (D). The current rally that got underway in March 2009 could soon make its final top (E).

A bearish broadening or expanding triangle would normally break down through the bottom of the triangle and have objectives that could in theory equal the widest point of the triangle. In this case, that would be D to E. This scenario could result in a complete collapse of the DJI. Some technical analysts such as Robert Prechter of Elliot Wave International www.elliotwave.com and Robert McHugh of McHugh’s Market Forecasting & Trading Report www.technicalindicatorindex.com have long been forecasting a potential final top to the current Grand Supercycle and that it could culminate in a huge financial collapse. This appears to fit their model.

…see more on Magazine cover hyperbole, Excessive P/E ratios, Consumer Sentiment & Margin Debt HERE

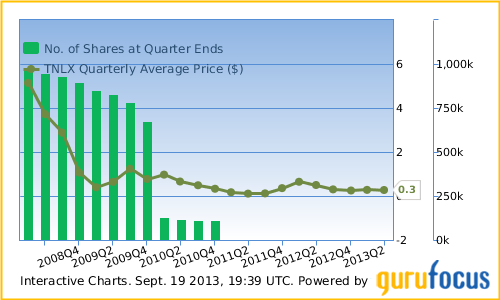

Over the past week, Mario Gabelli has made several guru real time transactions. These transactions involve one new buy and an increase in two others. These real time picks represent purchases or sales of a stock in which a guru owns greater than a 5% stake. These real time picks help to keep you more closely informed.

Trans-Lux Corp. (TNLX)

On Sept. 13 Gabelli made his first buy into Trans-Lux. The guru bought a total of 10,087,100 shares of the company’s stock. He bought these shares at an average price of $0.125 per share. Since his buy the price has increased 60% to $0.20 per share.

Gabelli previously held on to Trans-Lux but closed out his position in 2011Q1. His updated position is the largest stake he’s ever taken with the company, with 38.92% of the company’s shares outstanding.

…..view more on Trans Lux & his other 2 positions HERE

“There is a chance that this was a bull trap. If it’s down again tomorrow, then the chances of that increase.” – www.toddmarketforecast.com

Todd Market Forecast for Thursday September 19, 2013

Available Mon- Friday after 6:00 P.M. Eastern, 3:00 Pacific.

DOW – 40 on 500 net declines

NASDAQ COMP + 6 on 250 net declines

SHORT TERM TREND Bullish

INTERMEDIATE TERM TREND Bearish

STOCKS: Not much to say about today. It was a consolidation day and there was some profit taking. Some were saying that the economy remains weak, otherwise the Fed would have tapered.

There is a chance that this was a bull trap. If it’s down again tomorrow, then the chances of that increase. A bull trap is a high volume surge to new highs that marks a peak of sorts.

GOLD: Gold added a few dollars to yesterday’s explosion.

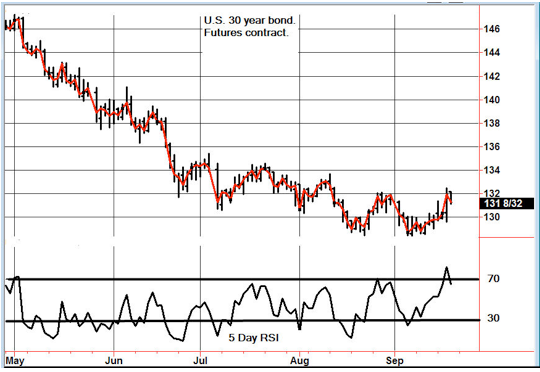

CHART: This is a very interesting chart. Bonds have been going down since May in spite of Fed buying. In other words, longer term interest rates are increasing regardless what the Fed wants. We’re going to go back on a sell for now. If bonds move to 133, it will push us back to the bullish camp.

TORONTO EXCHANGE: Toronto lost 5.

S&P\TSX Venture Comp: The Venture Comp was flat for the session.

BONDS: Bonds gave back some of yesterday’s sharp gains.

THE REST: The dollar collapsed. Silver, copper and crude oil were sharply higher.

BOTTOM LINE:

Our intermediate term systems are on a sell signal.

System 2 traders We are in cash. Stay there on Friday.

System 7 traders We are in cash. Stay there on Friday.

NEWS AND FUNDAMENTALS:

Initial claims were 309,000, less than the expected 341,000, but again, the data was not complete. The Philadelphia Fed Survey was 22.37, better than the expected 10.0. Existing home sales were 5.48 million, more than the expected 5.255 million.

———————————————————————————————————–

We’re moving back to a sell for bonds as of today September 19.

We’re on a sell for the dollar and a buy for the euro as of September 18.

We’re on a buy for gold as of September 18.

We’re on a buy on silver as of September 18.

We’re on a sell for crude oil as of August 29.

We’re on a sell for copper as of August 29.

We’re on a buy for the Toronto Stock Exchange as of August 23.

We are on a buy for the S&P\TSX Venture Comp. as of August 16.

INDICATOR PARAMETERS

INDICATOR PARAMETERS

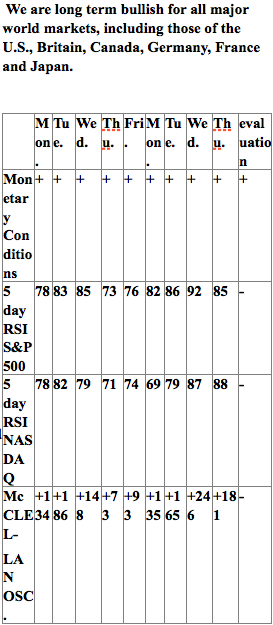

Monetary conditions (+2 means the Fed is actively dropping rates; +1 means a bias toward easing. 0 means neutral, -1 means a bias toward tightening, -2 means actively raising rates). RSI (30 or below is oversold, 80 or above is overbought). McClellan Oscillator ( minus 100 is oversold. Plus 100 is overbought). Composite Gauge (5 or below is negative, 13 or above is positive). Composite Gauge five day m.a. (8.0 or below is overbought. 13.0 or above is oversold). CBOE Put Call Ratio ( Below .80 is a negative. Above 1.00 is a positive). Volatility Index, VIX (low teens bearish, high twenties bullish), VIX % single day change. + 5 or greater bullish. -5 or less, bearish. VIX % change 5 day m.a. +3.0 or above bullish, -3.0 or below, bearish. Advances minus declines three day m.a.( +500 is bearish. – 500 is bullish). Supply Demand 5 day m.a. (.45 or below is a positive. .80 or above is a negative).

No guarantees are made. Traders can and do lose money. The publisher may take positions in recommended securities.

About The Todd Market Forecast

RANKED # 1 BY TIMER DIGEST

Timer Digest of Greenwich, CT monitors and ranks over 100 of the nation’s best known stock market advisory services.

Once per year in January, Timer Digest publishes the rankings of all services monitored for multiple time frames.

For the years 2003, 2004 and 2005, The Todd Market Forecast was rated # 1 for the preceding ten years. For the year 2006, we slipped to # 3 and in 2007, we were ranked # 5.

Our bond timing was rated # 1 for the years 1997, 2007 and 2008.

Gold timing was rated # 1 for 1997 and # 2 for 2006. Late word! We were rated # 1 for 2011.

We were # 1 in long term stock market timing for the years 1998 and 2004 and # 4 in 2010.

We provide daily commentary via e-mail for the stock market, gold, oil, bonds, currencies and stock index futures. We also publish a monthly newsletter.

Our approach is mainly technical in nature. We pay attention to chart patterns, volume, overbought – oversold indicators and market sentiment. However, consideration is also given to fundamentals such as interest rates, Fed policy, earnings and the economy.

We have two main approaches. First we seek to provide specific entry and exit points for conservative investors who utilize mutual funds and ETFs. We also give precise instructions for short term traders who utilize ETFs, Options and stock index futures.

Managed Accounts

In cooperation with Financial Growth Management, we offer a low risk bond income program. Your account would be managed through TD Ameritrade or Trust Company of America.

Your funds will be exchanged between high yield bond funds and money market funds based on a proprietary mathematical model. Our goal is to return 10-12% per year during a 3 to 5 year market cycle with very low risk.

If you would like more information, please contact Ray Hansen at 714 637 7784.

P.O. Box 4131

Crestline, CA 92325

ph: 909 338 8354

fax: 909 338 8354

toddmark

Hidden Finds from the edge of Biotech & Neurotechnology….

Four Small-Cap Growth Names with Different Value Drivers: Keay Nakae

Source: George S. Mack of The Life Sciences Report (9/19/13)

It’s important to take the emotion out of investing. Keay Nakae, senior research analyst with Ascendiant Capital Markets, looks at micro- and small-cap biotech stocks from an engineer’s perspective: It’s all about the data. In this interview with The Life Sciences Report, Nakae reports on four companies with upcoming catalysts that potentially position them for significant growth—and the ability to grab investors’ attention. More >

Hidden Finds in Regenerative and Medical Technology: Jeff Cohen

Source: Peter Byrne of The Life Sciences Report (9/12/13)

Ladenburg Thalmann & Co. Inc.’s Jeff Cohen regularly explores the frontiers of regenerative and medical technology looking for solid investment opportunities. In this interview with The Life Sciences Report, Cohen reveals promising finds in one of the world’s fastest-growing business sectors. From robotics to skin grafts, Cohen knows his science and his market. More >

Griffin Securities’ Keith Markey Gives Performance Reviews on Four Favorite Biotech Names

Source: Peter Byrne of The Life Sciences Report (9/12/13)

As science director for Griffin Securities, Keith Markey knows his way around the advanced technologies of the most promising research in biotech. In this interview withThe Life Sciences Report, Markey explains the science behind new developments in the antibiotic, diabetic and dermatological fields, highlighting ground-floor investment opportunities that investors will not want to miss. More >

Digging Below the Surface of Neurotechnology: Casey Lynch

Digging Below the Surface of Neurotechnology: Casey Lynch

Source: George S. Mack of The Life Sciences Report (9/5/13)

Neuroscience is about as complex as it gets. The central nervous system contains the brain and spinal cord, where hundreds of billions of neurons are located—and that doesn’t include the peripheral nervous system. Casey Lynch, managing director of NeuroInsights, works to make sense of both the disease processes affecting the nervous system and potential therapies that could help patients and enrich investors. In this interview with The Life Sciences Report, Lynch brings some clarity to the complexity, and speaks frankly about the wild goose that some Alzheimer’s disease investigators have been chasing. More >

Scientific Conferences Create Buzz and Move Biotech Stocks: Michael King

Source: George S. Mack of The Life Sciences Report (9/5/13)

It’s that time again. From Labor Day through the New Year, analysts jet off to conferences across the U.S. and Europe to hear data they’ve been waiting on for years. Michael King, managing director and senior biotechnology analyst at JMP Securities, has been at this game for almost two decades, and he has a firm grip on how data releases about molecules and their targets will affect the biotech stocks in his coverage. In this interview with The Life Sciences Report, King also names four growth companies making important advances in hematologic cancers. Just in time. More >

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair