Stocks & Equities

This week will be an important week for stocks. Not only because of the debt ceiling, but also because the earnings season will start again. What is to be expected?

This week will be an important week for stocks. Not only because of the debt ceiling, but also because the earnings season will start again. What is to be expected?

The next few days will be a great indication for the rest of 2013. The debt ceiling is number 1: the market assumes that there will be an agreement before October 17th, and so do we. A nasty turn of events is something you always have to be prepared for, but the signs from Washington seem to indicate that there is enough sense of reality and responsibility.

Earnings

Political turmoil aside, the focus of investors will be mainly the company results and earnings reports. There is a fear among investors that the fast climb of interest rates in the US this summer has had a negative effect on earnings. Byron Wien, vice chairman of Blackstone, already mentioned this in the middle of August.

Wien is supported in his view by David Bianco, stock strategist for Deutsche Bank. Bianco believes as well that the corporate world will report lower margins because of the higher interest rates. He also warns for the mindset of investors because of the political mess in Washington. Disappointing company results can then be the last drop for investors, who could pull out for now.

Our tip: don’t pay too much attention to the percentages of companies that have beaten estimates. That’s a fixed process and doesn’t say a lot about what is going to happen. We’ll cover that more in depth at another time.

More from Sprout Money – Here comes the Commodity Super cycle: Part 2

More Bulls than Bears

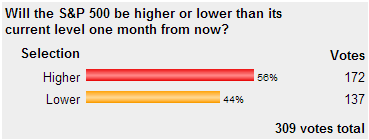

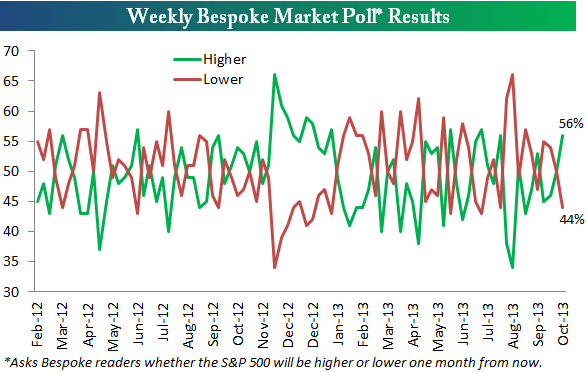

Even after a weekend in which talks broke down regarding the DC deal that the market thought it might get at the end of last week, there were more bulls than bears in our weekly Bespoke Market Poll by a margin of 56% to 44%. This was similar to the surprising reading we saw in AAII bullish sentiment last week.

HONG KONG — With just days until a crucial deadline on the U.S. debt ceiling, stock markets in Asia started the week with modest declines as investors considered the global financial devastation of a U.S. debt default.

Talks in Washington over the weekend did not produce an agreement on restoring government operations and raising the nation’s debt limit — both of which are seen as vital to allowing the government to pay its bills.

Although many analysts expect an 11th-hour resolution to the political impasse before Thursday, there is a considerable amount of nervousness among world leaders and investors that the brinksmanship in Washington could trigger a partial debt default, or that an extension of the debt-limit deadline would merely defer the underlying problems.

Canada’s main stock index was little changed on Friday with investors waited with bated breath for a resolution by U.S. lawmakers to end a federal government shutdown and overall market action muted ahead of the Canadian Thanksgiving long weekend.

Canada’s main stock index was little changed on Friday with investors waited with bated breath for a resolution by U.S. lawmakers to end a federal government shutdown and overall market action muted ahead of the Canadian Thanksgiving long weekend.

After recording its biggest jump in three months on Thursday, the Toronto Stock Exchange’s S&P/TSX composite index finished the session down 2.30 points, or 0.02%, at 12,892.11. Thursday’s gains came after U.S. House speaker John Boehner said Republicans are offering legislation that will allow for a temporary increase in the debt ceiling.

Any sign that an agreement may be in the works to head off a possible default by the U.S. government was enough to push North American markets sharply higher. U.S. President Barack Obama and congressional Republican leaders worked to end their fiscal impasse on Friday but struggled to strike a deal on the details for a short-term reopening of the government and an increase in the U.S. debt limit.

It is widely thought that failure to raise the borrowing limit would have serious repercussions for the fiscal standing of the United States, the world’s biggest economy, and for markets and economies of the United States and other nations worldwide.

But we have seen a similar situation play out recently with proclamations of dire consequences only to end in a ‘miraculous’ solution at the eleventh hour. Once again the debt ceiling issue is providing amusing political theatre as each side has their much sought after moment to climb on their soapbox and spout their special interest and/or agenda of the day.

While we have witnessed moderate volatility during this U.S. “crisis,” the markets appear to be relatively confident that a solution will once again emerge. Investors appear to be casting politicians as the boy who cried wolf and largely shrugging off the issue having seen it all before to a degree – despite the hourly ‘chicken little’ coverage from some reporters on networks like CNBC.

While the massive issue of government debt is nothing to sneeze at, the debt ceiling is not likely to be the central issue that topples North American markets. The issue will likely be resolved and appear like noise within short order.

What investors should be paying attention to is third quarter earnings season which is on the horizon and should start coming at us in earnest over the next several weeks. Ultimately it is growth or declines in cash flows in the particular stocks you own that will chart the direction of your portfolio overtime, not the three ring circus Washington continues to provide for your amusement.

Pay more attention to quarterly earnings calls from your core growth and income stocks (or let us do it for you) and less to Washington – while they may not provide the entertainment value, they truly affect your financial position and will likely allow you to keep down your lunch.

|

KeyStone’s Latest Reports Section |

Gold stocks continue to be universally despised, plagued by extreme bearishness. This has hammered their stock prices to epically-undervalued levels that are truly fundamentally absurd. This whole sector is now trading as if the gold price was less than a third of current levels! This massive disconnect has created vast opportunities for brave contrarians who have forged the mettle to buy low when few others will.

For literally thousands of years around the entire planet, gold has been an indispensable asset. It has been Tolkien’s One Ring of money, ruling over all national currencies ever created. It has been essential for wealth preservation and portfolio diversification, not to mention inflation protection and capital gains. The natural human lust for gold has dramatically reshaped world history, there is simply nothing else like it.

With gold highly-prized and valuable in all places and all times, the companies that painstakingly wrest it from the bowels of the Earth have also been highly valued. Their hard efforts recover a rare, scarce, and finite resource of great value, so investors usually flock to own these companies. Their extreme degree of out-of-favorness among investors today is far from the norm, it is actually a wildly-unprecedented anomaly.

…..much more HERE

T”he US dollar is poised right on the edge of a cliff.” said the Godfather of newsletter writers. A lot below in this powerful commentary – Ed

“The chart below shows the S&P Composite, and the red line is the VIX or volatility index. As you can see, the VIX has risen to its highest level since July. Thus, the VIX is sensing some volatility to come over the next few months. As a rule, I usually ready myself for some market volatility when the VIX climbs from a dull period to over 20. We’re not quite there yet.

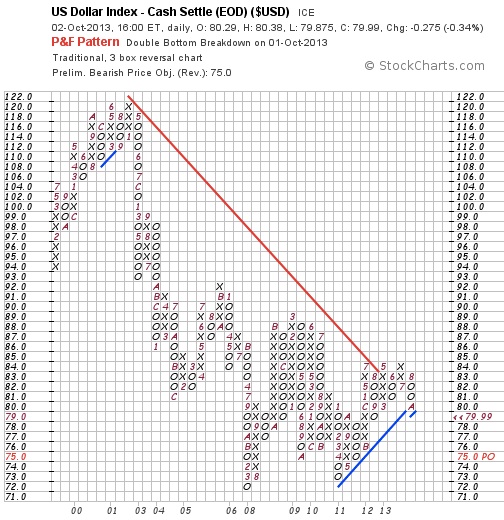

The chart below is the one that I believe is critically important — it’s the US dollar. The US dollar has acted as a safe haven for money in the US and all over the world. Thus, if we get a sell signal on the dollar it will have international implications.

Because it is so important, I am also including this P&F chart of the US dollar. The dollar appeared to be ready to break out on the upside, but a sudden reversal took the dollar down to the 80 box. The dollar is poised right on the edge of the “cliff.” A decline to 79 would look bad, and a further decline to 78 would result in a sell signal with the possibility that the dollar would then test its most recent low at (god forbid) 73.

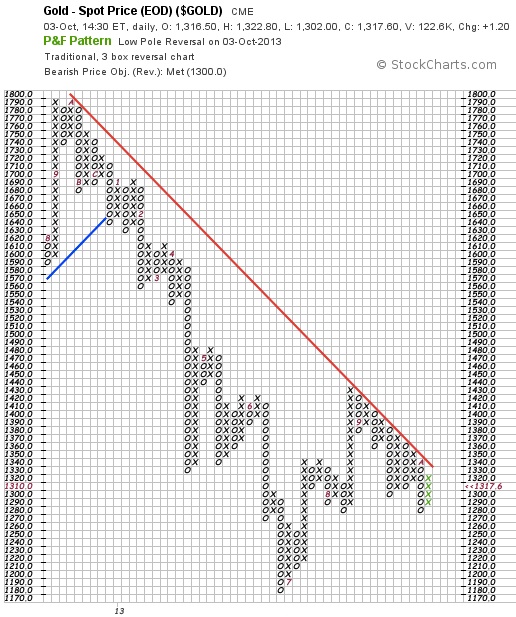

This chart of gold offers a portion of hope. We now have a four-box rally off the low of 1280. If gold can hit the 1340 box we will have what every gold-bug is praying for — a reversal to the upside, taking gold above the bearish red trendline. What are the odds that this will happen? If I knew, I’d be richer than Warren Buffett.

Below we see my inflation-or-deflation chart. Here we see the bond/gold ratio. When deflation is seen ahead, gold will tend to decline and bonds will tend to advance. The chart shows the bond/gold ratio rising. Thus, the markets are saying that deflation lies ahead.

This is very important since as I’ve noted before, Ben Bernanke will not tolerate deflation. Thus, this chart is telling us that tapering is not in the cards. As deflation becomes more visible, I expect the world’s central banks to battle against it with ever-greater portions of quantitative easing. This, of course, will set off a bull market in gold and silver.”

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE.

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair