Stocks & Equities

The 3 Most Telling Economic Charts in the World

With the wounds of the Great Recession still raw for every American, it’s all too easy to fall into the fear trap.

Specifically, fearing that our country is just one financial and/or political misstep away from falling back into a deep, dark period of economic contraction and despair.

Don’t believe the lies!

While the mainstream media tirelessly tries to paint a picture of economic fragility, we’ve come a long way.

Of course, such progress isn’t obvious if all we do is focus on the media headlines of the day.

However, it is obvious if we step back and get a little perspective on the situation.

Don’t believe me? You will once you get a load of these charts…

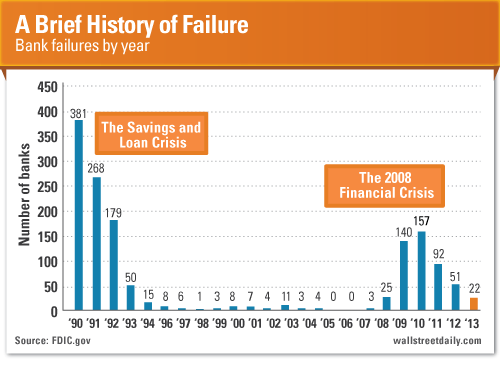

Bank on Fewer Failures

Driven by their insatiable greed, banks stood at the epicenter of the financial crisis. Hundreds of them went belly-up, including some of America’s most storied firms.

Despite considerable regulatory reforms, most Americans still distrust banks. Moreover, they believe the banking sector is so weak, it leaves the U.S. economy vulnerable to another crisis.

Not true.

As you can see, the number of bank failures continues to plummet, dropping by about 50% each year since 2010.

….see the other 2 Charts HERE

The VIX index, also known as the “fear index” has broken above 20% today. The political deadlock in Washington is continuing to take its toll on the market. The VIX has only seen 3 other days this year where it has broken above 20%.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

Back pay authorized,

Back pay authorized,

but still no government

-

- Some return to work in Arlington, Va. …

- Social TV …

- Ford’s Mulally joining Microsoft? …

- 2 reader experiences with Obamacare

The Wall Street insiders still say a U.S. default is unthinkable, but they can’t stop thinking about it. Today’s Bloomberg feature is a good example.

“A U.S. Default Seen as Catastrophe Dwarfing Lehman’s Fall,” said the Street’s go-to news source. The article then describes in vivid detail the horrifying consequences of default (“An economic calamity like none the world has ever seen”), before finally admitting:

“While none of the people interviewed for this story expect the world’s largest economy to default this time, either, most say the chances of it happening now are higher than in the past.”

Bloomberg’s vast global resources cannot locate a single person who actually expects default? “Most say” what we already know: The chances of default are “higher” than they were in the past.

“Higher” is purely relative. A 0.02 percent chance of default is higher than a 0.01 percent chance of default, but neither is especially “high.” Why spend so much space warning us about something no one thinks will happen?

Come on, Bloomberg. If a calamity is indeed looming, please quote someone who believes it. As we kick off another week with no resolution in sight, I’m happy to volunteer.

In our Friday edition, we reported that Wall Street isn’t worried about default. But no doubt they’re worried about how we escape it. Personally, as of today, I estimate the chance of default-related catastrophe at 60/40.

On our weekly internal analysts’ call today, each of our experts had their own ideas about how a default-related catastrophe would unfold. Even a day or two of default would result in a tailspin looking much like the TARP situation from the 2008 crisis. Similarly, it would take many months to repair the damage.

***

So, what has Congress been up to lately? Well, it passed a bill to give furloughed workers back pay after the shutdown ends. That may help reduce the economic impact.

On the other hand, it seems strange to see fiscally conservative politicians approving what amounts to indefinite paid vacations for federal workers. So, they’re spending the money (about $2 billion each week in salaries) but getting no government.

Does anyone think this makes sense?

***

Barring some kind of breakthrough, it looks like the government will stay closed for a while. But the lights are back on at the Pentagon, which called back 350,000 civilian defense workers this week.

I said on Friday that we could see a deal that raises the debt ceiling to avoid default, but still leaves the government mostly shuttered. (With the Pentagon calling back most of its workforce, that leaves about 450,000 workers still furloughed around the world.)

Wall Street is forming a consensus around similar scenarios.

This would mean we avoid the apocalyptic consequences of default, but the shutdown is still a big problem. Bank of America Merrill Lynch economists Ethan Harris and Michael Hanson lowered their U.S. growth forecasts and others are doing the same.

Harris and Hanson had previously projected Q4 Gross Domestic Product would grow at a 2.5% annualized pace. They now believe the effects of the government shutdown will push GDP growth down to 2.0%.

They also raise a good point: The muted market reaction may actually extend the shutdown. If the Dow were crashing and Treasury rates skyrocketing, the public would put pressure on elected officials to settle their differences. (In tomorrow morning’s edition, James DiGeorgia focuses on how the shutdown is shaping Virginia’s upcoming gubernatorial election.)

***

What else is the market focusing on? For starters, it’s watching the other Washington, where Seattle-based Microsoft (MSFT) needs a new CEO to replace Steve Ballmer. They are reportedly considering Alan Mulally, who is currently CEO at Ford Motor Co. (F).

Mulally isn’t the only possibility. Others named in news stories include former Nokia leader Stephen Elop,who was a top Microsoft executive before going to Nokia. Microsoft ended up acquiring Nokia, which makes some analysts think Elop was the chosen successor all along.

In fairness to Ford, Mulally will have to take himself out of consideration or let Ford start looking for a new CEO. Executives at that level can’t split their loyalty. Ford’s board of directors meets Oct. 10.

***

This week is the kick-off for quarterly earnings season. We’ll see whether publicly traded companies maintained healthy profit margins — and what they expect for the rest of the year. Here are some familiar names on deck this week:

- On Tuesday, Oct. 8, we get reports from aluminum maker (and former Dow-30 member) Alcoa (AA), as well as fast food leader YUM! Brands (YUM).

- Wednesday, Oct. 9 brings a pair of discount retailers: Costco (COST) and Family Dollar (FDO).

- For Thursday, Oct. 10, we have grocery chain Safeway (SWY).

- Friday, Oct. 11 is “too-big-to-fail” bank day. We can be sure JPMorgan Chase (JPM) and Wells Fargo (WFC) will report Q3 success. For them, failure is not an option.

The earnings pace picks up next week and the rest of October. The forecasts I’ve seen show most companies will meet or beat their Q3 targets. The bigger mystery is Q4 — and no one knows what to expect.

The Federal Reserve taper plan is likely on hold until the government agencies deliver the missing economic data points. The government shutdown’s economic consequences will grow if it drags on.

***

I haven’t said much about the Twitter IPO announced last week, although Nielsen is now measuring the impact of “social TV.”

Tony Sagami gave you his opinion about the Twitter IPO in our morning edition today. He thinks the next hot IPO will be even bigger and better than Twitter. Check it out.

***

Last week I asked for reports from anyone who made it through the technical glitches and actually applied for an Obamacare policy. Here are two responses. Both run a little long, but I think they illustrate the dilemmas many Americans face.

Reader Allan B. says: “I tried to use the online health plan contact for Washington State on October 1 and could not connect. On October 4, I successfully connected and used thewahealthplanfinder.org screens, with not a single delay. I ran several scenarios changing income amounts, because I am self-employed; deductibles; and premiums, etc.

“I found the assumptions about plan coverage amusing, calling the lower copays and lower deductibles the Gold Plans, when I particularly liked the Bronze Plans with very high deductibles.

“This year I received a cancellation notice from my health insurance company with whom I have had a high-deductible premium plan (about $4,800) for more than 10 years. The company is moving out of Washington State with no explanation.

“They referred me to another company, which will not insure me because I have a ‘pre-existing condition.’ That condition showed up two years ago with no family history of it. Last month I paid my share of the costs for treatment, a little over $15,000.

“Most of my career I have worked to help low-income and disabled people obtain federal medical benefits, both Medicare and Medicaid, so I have a personal and professional interest in the success of the ‘Patient Protection and Affordable Care Act.’ I see many interesting ideas about improving and revising the Act that Congress should consider. However, for now I am pleased I can tell people who previously could not obtain medical coverage that we have new options now. We can move and change jobs without fear of losing healthcare coverage.”

***

Reader K.W. says: “I am 53 and my husband is 57. We both cannot get insurance through our employers. His company does not offer it. I work under 30 hours due to caring for an aging parent and so I do not get it either.

“The ACA has caused insurance carriers to stop or curtail the offering of catastrophic coverage to people in their 50s. We currently pay $600 a month for both of us with very little coverage — having to add riders for cancer, heart disease and stroke — in order to cover ourselves catastrophically. PLUS we have a $12,500 deductible EACH. This kicks in after one annual physical and three doctor visits.

“We really cannot afford, nor do we have in savings, $25,000 in case something were to happen to each or both of us. When I priced the ACA plans, the Silver plan wants $1,100 a month and a $12,000 deductible. We will not pay over $13,200 a year in premiums in order to face that deductible either.

“We are not sure what we will do when the fines increase to catastrophic deductible levels.

“This is the time when we should be putting away as much as possible for retirement. We will not be able to do that with the ACA premiums, lack of benefits and high deductibles.

“A family like ours has to clear $18,000 in order to be able to fund $13,200 a year in premiums? That is over half my take-home pay.

“A LOT of money is being taken out of the economy that we can’t spend or save. We also have worked since we were in our teens, never on public assistance. Something is stinking and rotten with this whole scenario. Thank you for taking a deeper view into this debacle.”

***

Brad: “Debacle” is a good word for our healthcare system, with or without Obamacare. I think this may be why people are so angry and frustrated. They don’t believe Obamacare will help much, nor do they like the system we had before.

People like K.W. are in a particularly bad spot. They are too young for Medicare and make too much money for Medicaid, but not enough to pay high premiums and deductibles. What can they do?

***

Stocks fell today following a no-progress weekend in Washington, but Wall Street honchos still seem unconcerned about a Treasury default. Let’s see what else happened …

- U.S. Treasury yields fell today. The benchmark 10-year note ended at 2.63%.This makes no sense unless one assumes default is off the table. Did someone tell traders not to worry?

- The list of missing economic data gets longer every day. We’ve already missed August construction spending, August factory orders, and September unemployment. By Friday we’ll also be missingProducer Price Index and retail sales numbers.

- The Federal Reserve is open for business. This Wednesday they will release the minutes from the September FOMC meeting — the one where they decided to postpone tapering.

- The missing data means QE will probably go on at least a few more months.

Good luck and happy investing,

Brad Hoppmann

Publisher

Uncommon Wisdom Daily

“The current bullish uptrend remains intact which requires that we maintain exposure to the equity markets for the time being.”

Leading up to last week the threat was that if the government was shut down that the markets would tumble. I made it clear that this was unlikely to happen as the “markets” have seen this before, and with the Federal Reserve remaining fully committed to artificially inflating asset prices, there was little downside risk present.

So, for all the “fuss and turmoil” the markets really paid very little attention to the antics in Washington.

So, for all the “fuss and turmoil” the markets really paid very little attention to the antics in Washington.

While market volatility certainly increased in the past week – there was no violation of any support levels or the current bullish trend. In fact, as I stated this past week in our daily blog posting:

“As you can see the market reached its peak in July as the Federal Reserve reiterated its position that it would not be tightening its accommodative policy anytime soon. That rally from the June lows had taken the markets to an extreme overbought condition that needed a correction/consolidation process to resolve. However, it is important to notice that the May/June correction NEVER triggered a ‘sell signal.’

The significant difference is that the correction which began in August took the markets down to the longer term uptrend but triggered the issuance of a “sell signal” in the process. This change in dynamics required our models to reduce equity risk by 25%. (Portfolio models are holding 75% of target equity allocations currently.)

The subsequent market bounce, following a collision of announcements in September with Larry Summers stepping out of the race for Federal Reserve Chairman, ostensibly putting Janet Yellen in the seat, Obama stepping back from military action in Syria and the Federal Reserve not “tapering” their current bond buying program at their September meeting, seemed like the selloff was over.

However, that rally failed on two levels:

1) The markets failed to break out to a new high; and

2) The “sell signal” was not reversed.

This suggested that the corrective process was still in play, and despite the rally, kept the portfolios holding increased cash positions.

The recent government shutdown/debt ceiling debate drama is certainly providing the necessary catalyst for the continuation of the current corrective process. However, the markets, at this point, have not violated any short/intermediate/or longer term support levels that would warrant significantly reduced equity exposure. The current bullish uptrend remains intact which requires that we maintain exposure to the equity markets for the time being.”

The rally off of that short term weekly support on Friday kept the markets in play for the time being. However, the upcoming debate over the debt ceiling certainly puts the markets at risk in the short term and is something that we should remain very mindful of.

>> Read More. Download This Weeks Issue Here.

About Lance Roberts

Lance Roberts is the General Partner & CEO of STA Wealth Management, Host of the “Streettalk Live” Daily Radio Show (streamed live at www.streettalklive.com), and Chief Editor of the X-Report and the Daily X-Change Blog.

Follow me on Twitter: @streettalklive

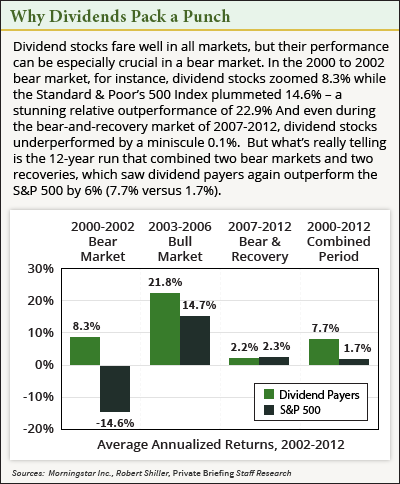

Most Dividend Payers Will Outperform.

We’ve all seen the statistics that extoll the virtues of the dividend payers – for instance, that from 1980 to 2005, Standard & Poor’s 500 Index dividend payers outperformed their non-dividend-paying counterparts by more than 2.6 percentage points a year (an outperformance that, over a long period, translates into major additional gains in a portfolio).

And there’s lots of research that underscores the fact that dividend payers gain more than the market averages in bull markets and lose a lot less in bear markets.

But a chart (see below) depicting some recent research by Morningstar Inc. really caught my eye: It very nicely illustrates that dividend stocks will deliver this “outperformance” over the course of multiple bull-and-bear markets. From 2000 to 2012, a 12-year run that combined two bear markets and two recoveries, dividend payers outperformed the S&P 500 by 6% (7.7% vs. 1.7%).

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair