Asset protection

See “The Real Danger” below – Ed Money Talks

I started Pento Portfolio Strategies three years ago with the knowledge that the unprecedented level of fiat credit creation had rendered the globe debt disabled and would result in mass global sovereign default. As a consequence, there would be wild swings between inflation and deflation dependent upon the government provisions of fiscal stimulus, Quantitative Easing and Zero Interest Rate Policies…

I started Pento Portfolio Strategies three years ago with the knowledge that the unprecedented level of fiat credit creation had rendered the globe debt disabled and would result in mass global sovereign default. As a consequence, there would be wild swings between inflation and deflation dependent upon the government provisions of fiscal stimulus, Quantitative Easing and Zero Interest Rate Policies…

For much of the third quarter the US Federal Reserve has avowed to raise rates. This in turn caused a sharp stock market correction on a worldwide basis. The flattening of the Treasury yield curve and the strengthening of the US dollar were the primary culprits. But then the September Non-Farm Payroll Report came in with a net increase of just 142k jobs, which was well below Wall Street’s expectation. The unemployment rate held steady at 5.1% but the labor force participation rate dropped to the October 1977 low of 62.4%. Average hourly earnings fell 0.04% and the workweek slipped to 34.5 hours. There were also significant downward revisions of 22k and 37k jobs for the July and August reports respectively.

The jobs data had previously been heralded by the Fed and Wall Street as the one bright spot in an otherwise dull economic picture; and gave the Fed extra incentive to move off of zero — as if offering free money to banks for seven years wasn’t compelling enough. But at least for now the weak data has caused the Fed to step back from jumping of the cliff on raising rates, which has caused a swift move lower in the value of the dollar and boosted the prospects for multi-national corporate earnings.

The reasons why Wall Street is so enamored with ZIRP and QE are clear. Here is a partial list of what will start to occur once the Fed moves away from the zero-bound range:

- Debt service payments will begin to rise on the soaring outstanding $44 trillion in total non-financial US debt — $12 trillion of which was accumulated in the last decade. This will render the already debt-disabled consumer increasingly unable to borrow and spend.

-

The value of US high-yield (junk) debt outstanding has doubled since 2009. Many companies have survived by rolling over this debt at record-low and perpetually falling yields. Default rates will spike as Junk-bond prices begin to fall and yields start to rise.

-

Rising rates will decrease the home ownership rate of 63.4%, which is already at its lowest level since 1967. A rate rise will also cause home prices to fall back toward the historic home price to income ratio of 2.6; it is now 4.4.

-

The Mean reversion of interest rates on the $13.2 trillion of US publicly traded debt would then take about 30% of all the Federal tax revenue. Rising rates would also cause annual deficits to jump back to $1.5 trillion as they did in the great recession, causing outstanding debt levels to rise inexorably, thus eating up a much greater portion of tax revenue.

-

There is $9.6 trillion of US dollar denominated debt owned by non-US borrowers. As the US dollar rises debt payments become more challenging to manage and would cause rising defaults on marginal foreign corporate holders.

-

It will sharply attenuate the amount of stock buy backs, which were done mostly by taking on new debt ($2.9 trillion worth since March of 2009) for the purpose of artificially boosting EPS. This would cause EPS and PE multiple contraction, sending the stock market into freefall.

-

The impaired credit of hundreds of trillions’ worth of interest rate derivatives, such as credit default swaps and interest rate swaps, which will need an unprecedented bailout from the government once the counterparties become insolvent.

-

Finally, pension plans will become bankrupt once the Fed succeeds in flattening the yield curve and completely crashing the stock market and the economy. Pension plans need 9% annual returns to fulfill their obligations. But the stock market has gone nowhere in the past 14 months even though the Fed has assured the country that there would be no competition for stocks from the fixed income sector for the past 7 years. Rising rates would most likely cause the stock market to lose half its value for the third time in the last 15 years.

Those are the reasons why the Fed is so afraid to start hiking interest rates.

The highly accurate Atlanta Fed’s GDP model is predicting Q3 growth of just 1.1%. As a consequence, the Fed Funds Futures Market now is predicting that ZIRP will be in place until March of 2016. Will five more months of ZIRP be enough to levitate stocks? The answer to that question is probably yes in the short term; but it will lead to a catastrophe in the long term.

The simple truth is QE and ZIRP blow up asset prices to an unsustainable level, but do nothing in the way of supporting viable economic growth. The proof of this can best be found in Japan, where the Bank of Japan is printing 80 trillion yen ($665 billion dollars) per annum but has rendered the nation in a perpetual recession. Indeed, after three years of Abenomics the nation will probably suffer through its third recession in as many years — Q2 GDP came in at an annualized minus 1.6%.

Further evidence of the ineffectiveness of central planning can be found in the United States, where we have experienced sub-par 2% growth for the last 5 years despite unprecedented monetary easing. And 2015 is now on track to underperform that low five-year bar.

The IMF recently lowered its global growth projection by 0.2 percentage points to 3.1%. This includes an overly optimistic 6.8% read on China growth.

The Real Danger

The real danger is that the higher asset prices get pushed by central banks and governments with fiscal and monetary stimuli, the more precariously they become perched high on top of a hollow economic foundation.

With ZIRP in place for another five months, this ominous condition should only worsen. However, it also means that whenever the Fed resumes its bluster about raising rates, the markets will careen lower from an even higher level. In addition, central banks’ inability to engender the promised prosperity is rapidly eroding confidence in these institutions. Therefore, there is a growing risk that the markets will collapse despite perpetually free money — especially in real terms. Such will be the unfortunate but inevitable consequences of obliterating honest money and free markets.

Just eight or nine years ago, currencies were the hot-ticket item in the investment world. That was when central bank easy-money policies helped investors realize (and exploit) the interconnectedness of global economies and financial markets.

Just eight or nine years ago, currencies were the hot-ticket item in the investment world. That was when central bank easy-money policies helped investors realize (and exploit) the interconnectedness of global economies and financial markets.

It was also pretty easy to bet against the U.S. dollar, too.

But then the financial crisis hit.

Then the greenback became the recipient of safe-haven capital flows. At the same time, emerging-market currencies, commodity dollars and the more-popular-than-ever euro were hung out to dry.

Just like that, the currency game got real.

Investors Cash out of the Currency Game

Newbies hadn’t realized the intricacies of the foreign exchange market. Their orientation was made painful by the financial crisis, and investors quickly lost their appetite for currency investments.

Currencies are back in the headlines this year, but not because investors are excited about them.

Rather, because China is battling renminbi valuation. On top of that, emerging markets’ dollar-denominated debt has become costlier because their currencies have lost so much value so quickly.

Regardless of whether currencies are hot or cold with investors and traders, the foreign exchange market still trades and currencies offer returns … if you choose pay attention.

That’s why today I’m giving you my view on the U.S. dollar, Aussie dollar, euro and Japanese yen.

Greenback: Going Higher

Starting off with the U.S. dollar, I think it has greater upside potential in the coming months and even years.

How can the dollar climb higher after rising about 20% since June 2014? Because the U.S. is a relatively attractive destination for investment capital.

Barring a financial crisis that will shake the entire globe, the U.S. economy is more stable than most emerging markets, China and even many developed European nations. That will draw more foreign money to U.S. shores.

When this money makes its way to the U.S., those euros, pounds, yen and rubles are exchanged for dollars.

Interestingly, the U.S. dollar hasn’t been behaving like a safe-haven currency of late.

It’s not being borrowed and sold — as a carry trade currency — to fund investments elsewhere. Instead, it’s showing some correlation to risk assets such as U.S. stocks.

This suggests the dollar is being targeted for its potential to hold value or even generate speculative gains.

All said, this underpins my longer-term bullishness for the U.S. dollar.

In the interim, however, I think the buck might soften up before heading higher.

There is some concern about the influence a strong U.S. dollar is having on U.S. exports and, thus, the trade deficit. But changing expectations for a Federal Reserve interest rate hike is probably the primary driver.

Ever since the September U.S. jobs report disappointed, investors have been pushing back the likelihood of the inevitable hike.

If rates in the U.S. are not rising, then the greenback is not gaining an advantage (or erasing its disadvantage) relative to the interest rates on competing currencies.

For example, based on respective central bank benchmark rates, the Australian dollar currently boasts a 2% yield while the yield on the U.S. dollar is essentially still zero.

All things being equal, if you were choosing to park your money on one currency or the other, would you choose the one yielding 2% or 0%?

Thought so.

This is why I think the U.S. dollar bull scenario might undergo a bit of a rethink in the near-term.

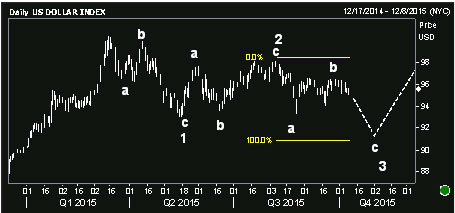

To finish a three-wave consolidation pattern, the U.S. dollar index would likely need to drop to the 91 range. From there it could begin another sustained move higher.

That, of course, is the U.S. Dollar Index, which is an uneven basket made up of six foreign currencies.

Euro (EUR), 57.6% weight

There are certainly ways to trade the U.S. Dollar Index, but you can also bet on how the dollar will fare against any one currency.

***

The euro, interestingly, has assumed a sort of carry trade role at times. It’s the role to which the U.S. dollar laid claim until last year. Before that, the Japanese yen was the notorious carry trade currency.

The euro is more than that, though.

Since emerging from the latest Greek charade, Europe has mostly stabilized and investor confidence in the euro area has improved.

Importantly, the European Central Bank has committed to a policy of ongoing monetary accommodation to ensure the economic recovery is not smothered.

In one sense, the ECB’s policy is bullish for the euro zone and thereby supportive of the euro. But in another sense, it undermines the euro’s yield relative to the U.S. dollar since the Federal Reserve is expected to hike rates soon.

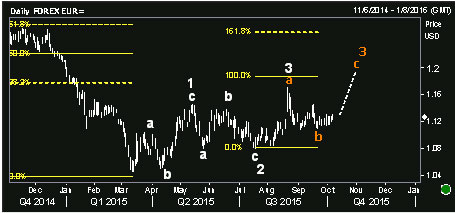

All things considered, I think the euro is in a position to extend higher.

The orange is an alternate wave count, off of which I’m basing my bets. This suggests the euro should continue higher before this move is done and it weakens vs. the U.S. dollar.

***

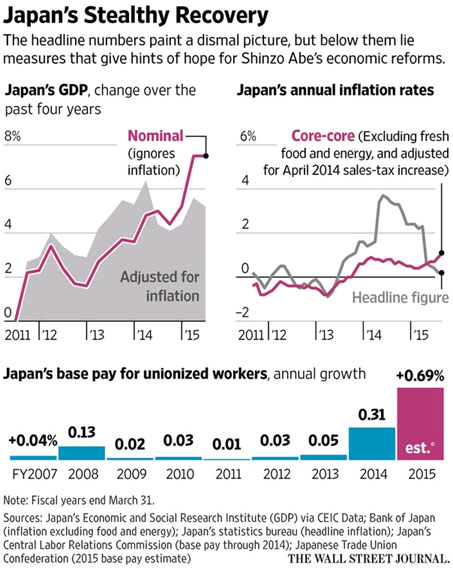

With Greece, China, emerging markets and Middle East war dominating the news, there’s little room left for Japan.

And with the absence of inflation across the developed world, notably in stagnant U.S. wages and falling commodity prices, one might just assume Japan is continuing with where its lost decade left off.

And one might be right.

But check out this chart from the Wall Street Journal.

There’s a lot to be desired, sure. But that chart medley suggests Japan isn’t in too bad a spot right now — especially compared to the uncertainty plaguing so many other economies.

What might this mean for the Japanese yen?

Maybe economic optimism draws capital toward Japan.

Maybe.

But the Bank of Japan is very much in the same position as the European Central Bank — the same position from which the U.S. Federal Reserve has been hoping to depart — providing monetary accommodation to its economy.

Ultimately, this yield differential dynamic will power the yen lower vs. the U.S. dollar.

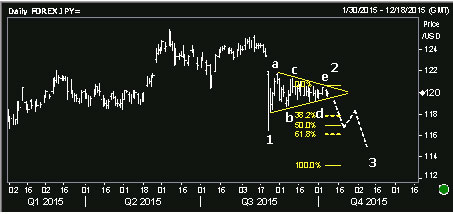

In the meantime, though, it looks like the yen has technical room to strengthen.

The chart above shows the USD/JPY exchange rate. Falling prices indicate U.S. dollar weakness, and Japanese yen strength.

***

Commodities have been pummeled. And China is now feeling the effects.

The pain in these investments has been well-documented.

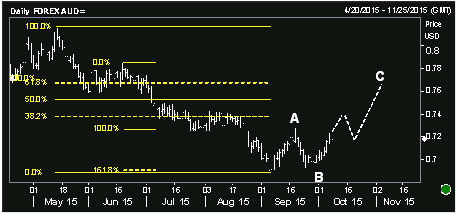

Less documented, but entirely relevant, has been the assault on the Australian dollar.

The Aussie is considered a commodity dollar because Australia is blessed with natural resources. Its economy is very much contingent upon the trade of its commodities and natural resources.

So, the value of its currency has fallen in kind.

Inherent in that performance has been central bank expectations. The Reserve Bank of Australia has been cutting or keeping rates low to alleviate commodity price pressures on its economy.

The Australian dollar lost 32% of its value since the first half of 2013.

In the latest meeting, however, the Reserve Bank of Australia did not cut rates — they remain at 2%. And the Federal Reserve is expected to keep delaying the start of its rate hike cycle.

Combine rate expectations with the technical chart setup and bearish sentiment extremes for commodities and China (a huge customer for Australia) … and you’ve got the makings of an Australian dollar rally.

***

Want to play these currencies?

You can trade the U.S. Dollar Index with the PowerShares DB U.S. Dollar Bullish ETF (UUP).

For the euro, yen and Australian dollar, you can use the CurrencyShares exchange-traded products: the euro ETF (FXE), Japanese yen ETF (FXY) and Australian dollar ETF (FXA).

These ETFs do kick off a dividend based on the underlying country’s benchmark rates. But as you might suspect from central banks’ race to zero, their yields are nothing to write home about.

Also, currencies tend to move slowly relatively to other investments, so these ETFs aren’t likely to generate outsized returns unless you catch a good trend.

Shorter-term investors may consider using options on the ETFs I mentioned to capture sizeable returns in a short amount of time.

In fact, I just recommended such a trade to my Natural Resource Options Alerts guys on one of these currencies, and it’s already up more than 17% in just a couple of days. And my “E3” system tells me there is more upside ahead.

Do right,

JR Crooks

About John Ross Crooks

According to Brad Hoppmann “JR Crooks is on fire! Last week he closed his latest gold play for a potential 90% gain, his latest oil recommendation popped over 55% in one week and his new commodity play is up close to 20% in just 2 days! Click on Natural Resources Options Alerts to watch a trading video about the “E3” system that JR Crooks is behind (advertisement – Ed)

“JR” specializes in trading commodities, currencies and options. He has spent nearly 10 years analyzing financial markets and writing about global economics. JR honed his trading techniques and global-macro worldview alongside his father, Jack Crooks, at Black Swan Capital. JR also …read more HERE

While other commodities are floundering or completely collapsing in this market, lithium—the critical mineral in the emerging battery gigafactory war—is poised to explode, and going forward Nevada is emerging as the front line in this pending American lithium boom.

While other commodities are floundering or completely collapsing in this market, lithium—the critical mineral in the emerging battery gigafactory war—is poised to explode, and going forward Nevada is emerging as the front line in this pending American lithium boom.

Most of the world’s lithium comes from Argentina, Chile, Bolivia, Australia and China, but American resources being developed by new entrants into this market have set up the state of Nevada to become the key venue and proving ground for game-changing trade in this everyday mineral. Nevada is about to get a boost first from Tesla’s upcoming battery gigafactory, and then from all of its rivals.

For several years, experts have been predicting a lithium revolution, and while investors were being coy at first, the reality of the battery gigafactories is now clear, and nothing has hit this home more poignantly than Tesla’s recent supply agreements with lithium providers who will be the first beneficiaries of this boom, followed by a second round of lithium brine developers that are climbing quickly to the forefront.

As Jeb Handwerger—founder of Gold Stock Trades—recently told the Resource Investor....continue reading HERE

Clear Signs That The Great Derivatives Crisis Has Begun

Clear Signs That The Great Derivatives Crisis Has Begun

by Michael Snyder

While things may seem somewhat calm on Wall Street at the moment, the truth is that a great deal of trouble is bubbling just under the surface.

Jim Rogers: I Would Not Be Buying U.S. Real Estate

The Chinese rush to buy U.S. Real Estate is probably a sign of a top in that market.

…..listen to Jim’s podcast HERE

also from Rogers:

China Will Not Save Us Like They Did In 2008-09

Holy Hell About to Break Loose …

by Larry Edelson

Global equity markets are teetering on the edge of a cliff. For some, like Europe’s markets, it will be the beginning of a long, drawn out bear market.

Historic. Landmark. Groundbreaking. Revolutionary.

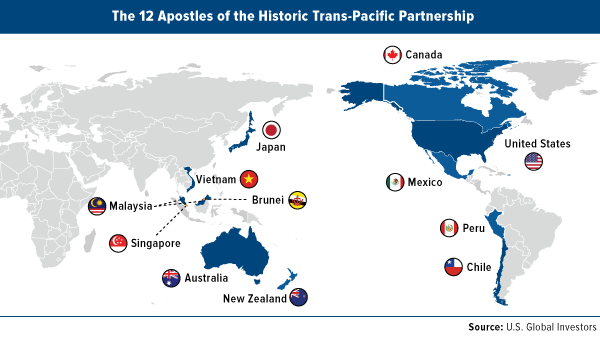

These are among many of the words that have been used lately to describe the Trans-Pacific Partnership (TPP) trade pact, which was finally signed in Atlanta this Monday by 12 participating Pacific Rim nations.

The current members include Canada, the United States, Mexico, Peru, Chile, Japan, Vietnam, Malaysia, Brunei, Singapore, Australia and New Zealand.

After nearly seven years of negotiations, the TPP promises to deliver unprecedented free and fair global trade among the 12 participant nations.

Once ratified by each country’s congress or parliament—which is likely to happen in early 2016—the accord will become the most significant, most economically-impactful trade deal in history. As many as 18,000 tariffs are expected to be eliminated. It will remove barriers to foreign investment, streamline customs procedures and create an international investor-state dispute settlement (ISDS) system, among much more.

The Peterson Institute for International Economics, a Washington, D.C.-based think tank, predicts that the resultant savings could boost the world economy by an incredible $223 billion by 2025.

….read much more on TPP as well as SWOT analysis of Stocks, Bonds, Gold and Energy HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair