Bonds & Interest Rates

“Once we realize that imperfect understanding is the human condition, there is no shame in being wrong, only in failing to correct our mistakes. – George Soros

Are we there yet?

Are we at the point where people might ignore the central banks?

Thankfully, maybe.

George Soros made a valid point to a CNBC interviewer recently. He noted the Bank of Japan made a dramatic move with monetary policy stimulus so that it wouldn’t be overlooked.

I think that idea was obvious. But Soros lends a lot of credibility to an idea based on his investment track record.

But he also may signal something more.

Being longer in his years, and evermore notorious as a left-wing political beacon, it seems Mr. Soros strains to toe the line laid down during media training.

In other words: he wants to say what’s on his mind but must choose his words carefully.

What I believe Soros would say if he were not in front of a camera is this:

“The influence of central bank stimulus policy is at risk of wearing off. While some may admit central banks did help to boost sentiment and loosen up credit markets, the measly pace of stop-and-go recovery is threatening to reveal that the effectiveness of central bankers’ tools is limited. The real risk now is that people aren’t encouraged to play along and money truly never makes it into the real economy as promised.”

Ok, that’s enough of pretending to be George Soros for one day.

The ongoing deliberations among Eurozone leaders and Troika officials tell us that austerity isn’t so popular and neither is dumping bailout liability onto taxpayers. Achieving the proposed resolution of a banking union will be difficult and should keep the European Central Bank very-much hogtied.

The measures undertaken by the Bank of Japan this week to target the monetary base have been tried before, to a degree. The measures didn’t work then. Now it seems the Japanese government is desperate and hopes the measures will succeed this time. Their overly-confident rhetoric also reeks of desperation.

The Federal Reserve is fully committed, but they can only do so much while they hold their breath and hope the unemployment situation improves sufficiently. They’ve got to be thinking the deflationary forces must be strong for their policies to have not turned up any inflation worth speaking of.

Earlier this morning the March US Nonfarm Payrolls were reported. It was a disappointment.

Instead of adding anywhere near the anticipated 200,000 new jobs, the economy only added 88,000. There were, however, upward revisions to January and February numbers.

The market is acting poorly, as one might have predicted.

I went into it thinking today’s report represented a bigger downside risk for markets than it has in a long time.

Why?

Because market mood has deteriorated this week. And markets seemed very vulnerable to a potential disappointing jobs number. Though we’ve seen widely-accepted “improvement” in the labor market, even the hiccups have been met with optimism; we’ve come to assume even a bad number is good because it means the Fed will keep on keeping on.

While no one expects the Fed to be planning its exit, the “Fed to the rescue” mentality may be overdone insofar as it influences short-term reaction to data and reports.

The expectations for US economic outperformance, relative to its peers, seems to have been the only crutch keeping the US market from giving way to Cyprus uncertainty and underwhelming price action in other asset classes.

So it’s not hard to see why today’s jobs number is pressuring US stocks (and even the US dollar at the same time.)

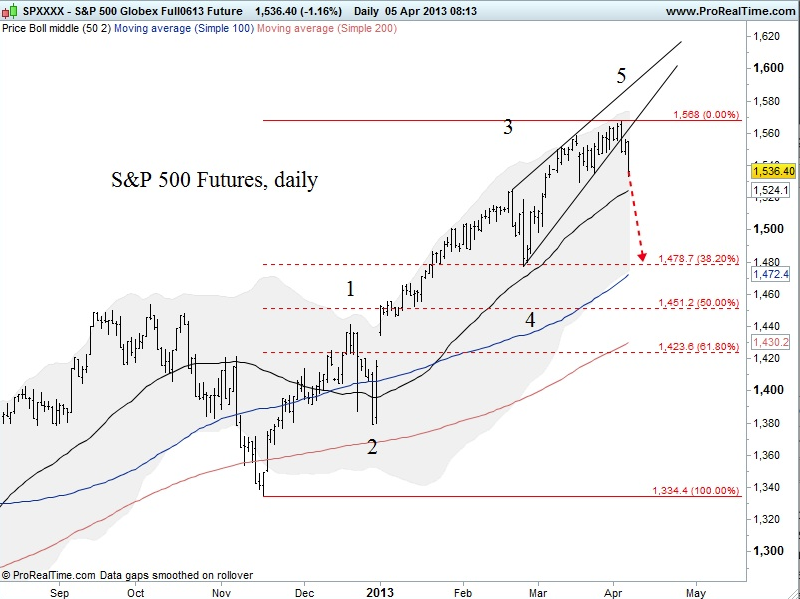

Besides, the market is certainly ripe for a correction and the technicals looked poised to drive the market lower (regardless of the jobs number). Below is a daily chart of the S&P 500 futures showing a fifth-wave extension/rising wedge set-up that suggests a significant reversal; first level of Fibonacci support comes in at 1,478:

It very much looks like the much-anticipated correction has begun.

I think that’s the way we have to play it right now, remaining open to more downside than generally expected.

But going forward, I suppose the question is this:

Do central banks have anything left in the toolbox the people can’t ignore?

I certainly don’t want to underestimate the potential central banks will concoct some sort of new and unprecedented strategy. Like I said of the BOJ above – I think policymakers (and politicians) have become desperate.

Of course, if the influence of central banks has truly run its course, then the market may have the opportunity to take over.

It’s just a correction for now. Play it. And reevaluate later.

-JR Crooks

Contents:

Three Days that Saved the World Financial System

Does a Yes to the Swiss Gold Referendum Imply an End of the CHF Cap?

Texas Wants its Gold Back! Wait, What?

Cyprus and the Unraveling of Fractional-Reserve Banking

Slovenia Faces Contagion from Cyprus as Banking Crisis Deepens

Luxembourg Warns of Investor Flight from Europe

The German Professor Who Wants to Get Rid of the Euro in Order to Save Europe

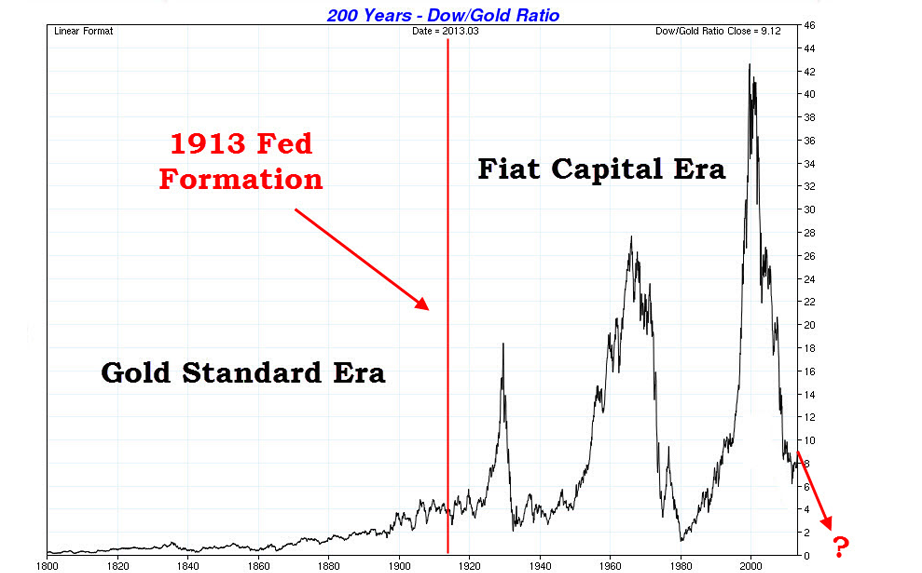

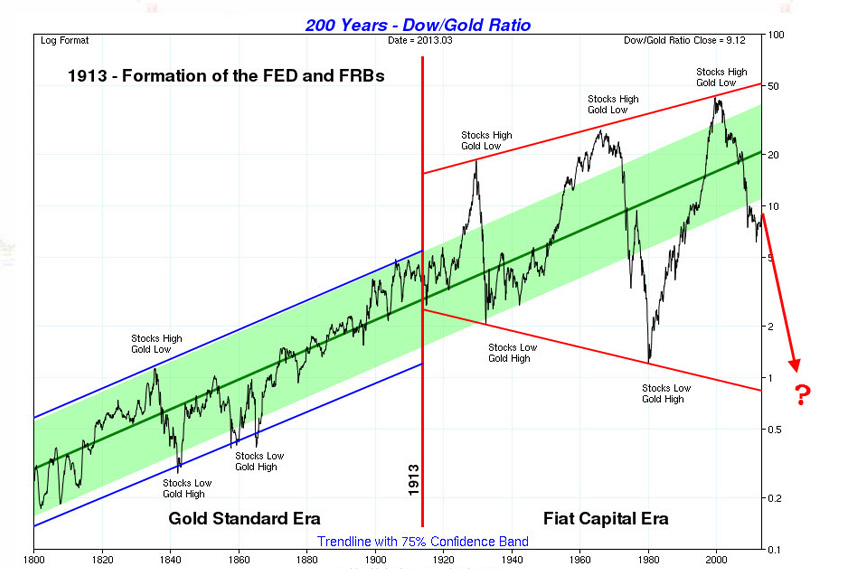

One of the more fascinating reminders of what may be to come for the remainder of this gold bull market, is the charted history of the dow/gold ratio. Below are two charts illustrating the upward potential in gold which remains for the duration of this market.

The first chart is a normal 200-year look at the dow/gold ratio. What’s particularly shocking here is the staggering levels of volatility injected into the economy and financial system following the US Federal Reserve’s formation in 1913…. [This] volatility has wreaked havoc on many, while creating excellent one-way bets for long term speculators…. [T]he second and more alarming ratio chart is illustrated with a “confidence trend band”:

.…….read it all HERE (Delay Of Game. Five (point eight) Yards)

We continue to believe that the world is still in need of major rebalancing.

Global policymakers have faced an onslaught of crises or crisis potential. As such, despite what seems to be happening (a slow market-led rebalancing), they continue to revert to policies that have driven growth (and imbalances) in the past.

A true rebalancing will bring economic pain, for sure. But the ongoing resistance we’re seeing will only mean the pain is deeper and lasts longer whenever it comes.

Of course, China is a big part of the rebalancing puzzle. And they’ve acknowledged their need to rebalance their economy. They’ve even taken concrete steps to insure they pull back from the growth path that leads to an overheated economy and an inevitable collapse.

Measures to increase the number of transactions in their own currency, the yuan, are encouraging. The greater the use of the yuan in global trade the more open it must become and the better the market can dictate its value.

We consider currencies to be the pressure valves of economies that serve to rebalance respective economies as needed. A system with an explicitly managed currency (e.g. China) or implicitly managed currency (e.g. US) cannot be good in the long-run.

But certainly there are risks to China even as it embraces some pieces of rebalancing.

But certainly there are risks to China even as it embraces some pieces of rebalancing.

Many analysts and researchers note the demographic hurdle. As much as China is urging its population, directly and indirectly, to become more urban, the needed and expected shift cannot be forced. Consider the real estate market, for example …

The inventory of housing is in place now, but most of China’s rural class and commuting class cannot afford to live there. A significant drop in price is needed to help this along. But with a significant drop in price comes a drop in wealth for those investors who’ve bought into the housing developments and the real estate market in general.

When you see a system-wide erosion in wealth you often see contagion in credit markets. China’s shadow-banking system (i.e. unconventional loans and wealth management products) has expanded amidst the last couple years of stop-and-go lending policies passed down by the government and the PBoC in response to inflationary pressures. When the value of assets drops and borrowers begin to default, the rest of the dominoes become more vulnerable.

In China’s commie-capitalist economy, the leaders maintain their grip on the economic reins. But not only do they claim credit for the good, they must also deal with the bad and the ugly.

Rebalancing will require reforms that hand over greater control to Chinese households and consumers. This means the policies that brought years of double-digit growth must be sacrificed to some extent. This is why the task of rebalancing China is oh so delicate — necessary reforms equal lower growth, but lower growth equals socio-economic tensions. Unfortunately, the tension will come a lot more quickly than the benefits of reform.

There is a reason I dug into this today — I came across two articles this morning …

The first simply notes some recent improvement in Chinese consumer demand and factory orders. Here is Reuters’ takeaway from the numbers that were reported:

Stronger domestic demand helped China’s factory activity to rebound in March, with… new orders up sharply in a sign that the underlying economic recovery is strong enough to weather any risks from patchy export performance .

This is certainly a welcomed development amid ongoing Eurozone woes that have kept China’s best export customers at bay. But is it enough to keep the economy going if Europe triggers a quake in financial markets?

The second article I came across this morning represents a bigger story that attempts to look further into the future of China’s factories. More specifically, the US shale gas revolution is likely to facilitate some rebalancing in China as it reduces the costs of producing goods in the US. This is certainly a long-term data point, but it gives merit to that arguement that “Made in the USA” will make a comeback.

Here is a key piece of the Reuters’ column titled, “Will shale gas decimate China’s toy makers?“:

The advent of cheap natural gas in the U.S. is threatening to displace expensive naphtha in the production of petrochemicals, the key building blocks for plastics, synthetic fibres and solvents and cleaners.

There was a story in The Atlantic earlier this year that talked about GE bringing factories back to the US. The simple reason is that it makes more sense to have a better grip on all stages of production and supply chain management. Consider also the fact that Chinese wages and transportation costs have risen.

And then recently I saw comments from the CEO of a major US company who said the cost of labor is not the primary reason for taking a company offshore; the regulatory and tax environment are the main reasons. If the US government finds ways of lessening this burden, and the shale gas revolution lives up to the hype, America could quickly see a manufacturing renaissance that changes global trade dynamics quite drastically.

-JR Crooks

“Please, you better hurry. I’m doing it anyway” Rogers tells CNBC.

“Please, you better hurry. I’m doing it anyway” Rogers tells CNBC.

“I want to make sure that I don’t get trapped.”

“What more do you need to know?”

Cyprus was “a warning shot to bank to depositors around the world.”

Rogers’ idea is that the risk of a confiscation of bank deposits now exists anyplace on the globe.

“Think of all the poor souls that just thought they had a simple bank account. Now they find out that they are making a ‘contribution’ to the stability of Cyprus. The gall of these politicians.”

“The losses imposed on Cyprus bank depositors by the European Union, European Central Bank (ECB) and International Monetary Fund (IMF) bailout should be a warning shot to bank depositors around the world,” says investment legend Jim Rogers, chairman of Rogers Holdings.

…..read more of what Rogers is doing HERE

MFGlobal – Customer assets were supposedly insured, segregated, and protected by the exchange. Apparently not! Jon Corzine “has no idea” where the assets went. Most clients had believed their accounts were safe, and they were wrong.

MFGlobal – Customer assets were supposedly insured, segregated, and protected by the exchange. Apparently not! Jon Corzine “has no idea” where the assets went. Most clients had believed their accounts were safe, and they were wrong.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair