Bonds & Interest Rates

Following the Federal Reserve’s meeting on Wednesday there was a lot of speculation about how long the Fed will continue its Quantitative Easing (QE) program. Since the Fed’s statements are cryptic, I prefer to look at its economic projections. In this article, I discuss how the Fed’s current GDP and unemployment projections compare to the projections at previous meetings. At almost every meeting since 2011, the Fed has lowered its forecasts. Before a “Fed exit” is on the table, we probably need to see GDP projections increase from meeting to meeting. That may be far off and QE Infinity looks likely to be around for a while. Despite the Fed’s efforts, US Treasury bond yields are rising and prices falling (as measured by the iShares Barclays 20+ Yr Treasury Bond ETF (TLT)), but the big move in the bond market may happen when the Fed’s GDP projections begin to change directions.

Following the Federal Reserve’s meeting on Wednesday there was a lot of speculation about how long the Fed will continue its Quantitative Easing (QE) program. Since the Fed’s statements are cryptic, I prefer to look at its economic projections. In this article, I discuss how the Fed’s current GDP and unemployment projections compare to the projections at previous meetings. At almost every meeting since 2011, the Fed has lowered its forecasts. Before a “Fed exit” is on the table, we probably need to see GDP projections increase from meeting to meeting. That may be far off and QE Infinity looks likely to be around for a while. Despite the Fed’s efforts, US Treasury bond yields are rising and prices falling (as measured by the iShares Barclays 20+ Yr Treasury Bond ETF (TLT)), but the big move in the bond market may happen when the Fed’s GDP projections begin to change directions.

The Fed’s Projections For GDP Growth & Unemployment

The following charts aggregate the projections for GDP growth and unemployment (as released after Fed meetings). The Fed releases its data in the form of a broad range of projections and a narrower “central tendency.” The figures below represent the midpoint of the central tendency for each period.

….read & view much more HERE

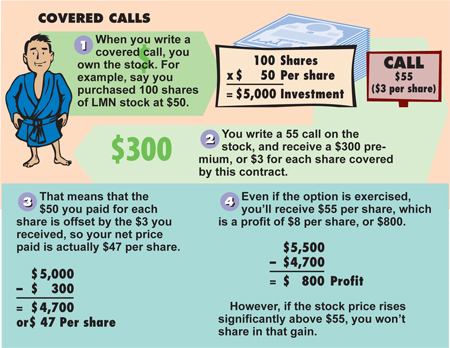

One of Michael Campbell’s favorite investment strategies is to sell options against his investments. Selling options can be an ideal way to add income to your account. There might be no guarantees in the stock market, but that doesn’t mean you can’t minimize risk, and generate income.

Here’s an example of Selling Call Options:

You have 500 shares of XYZ stock trading $20 a share and valued at $1,500.

You sell (writes) 5 call option contracts (1 option contract covers 100 shares) @ $300 x 5 and receive $1500. This premium of $1500 covers a certain amount of decrease in the price of XYZ stock (i.e. only after your initial $10,000 stock position has declined by more than $1500 at the time of the option expiry would you lose money overall).

Let’s look at the possible scenarios…

1) The Covered Call Option expires worthless. This happens if the current market price of XYZ is below the strike price ($20) of the call option on its expiration date. This is fantastic because you were paid income up front and now that the time of the option is over, you are no longer obligated to anything. You can forget all about the option and continue to hold the stock, or you can repeat and sell another covered call option.

2) The Covered Call Option is exercised. In this case, you were paid money up front and then you were obligated to sell the stock at the agreed upon price ($20) on the expiration date of the call option. This is still profitable news because you owned XYZ at $20, took in the $1,500 you were paid to sell the Call Option, your profit from the date you made the decision to sell the call option is $1,500 / $10,000 or 15%.

The point is that you are increasing your guaranteed income by being willing to trade away some of your upside profit potential.

Here’s another example in a visual form:

There are other option strategies, for example to learn how to protect yourself from losing money by buying insurance in the form of a put option, go HERE

Spending Patterns Paint Half Truth

by John Browne Euro Pacific Capital

On March 13th, the Commerce Department announced a 1.1 percent increase in food and services retail sales, doubling a prior Dow Jones survey of economists that forecast an increase of just 0.6 percent. This new data has led to a fresh wave of enthusiastic commentaries that the US economy is set for a strong recovery. Less examined were the underlying factors that supported the increase.

Through the persuasive powers of its Chairman, Ben Bernanke, the US Federal Reserve has convinced the world’s three other key central banks – the Bank of England, the ECB, and the Bank of Japan – and many others to adopt its policies of quantitative easing (QE) to spur economic growth. By lowering the cost of borrowing and lessening the rewards of saving, I believe that these policies have led to increases in spending. But to call it a success involves only looking at one side of the balance sheet. The supposed benefits come at a high cost.

Gasoline prices rose by nearly 15 percent from January to February of this year. Spending also rose in grocery stores, which are considered to be a gauge of necessity spending. On the other hand, declines in department store, restaurant, and furniture spending would seem to indicate that consumers are cutting back in areas that economists deem to be “discretionary.”

Four years of annual trillion-dollar-plus government deficits and the Fed’s creation of more than $2 trillion of synthetic money since the crisis beganhave injected almost unimaginable amounts of “stimulus” into the US economy. In addition, the Fed’s downward distortion of the rates of interest, inflation, and unemployment is cynically designed to encourage a false sense of economic growth and economic optimism.

In view of all of this, it is absolutely amazing how listless overall consumer spending has been. I see it as evidence that other forces are holding the lid down on real increases in economic growth.

But investors are loathe to ignore such a wave of buoyancy in official government figures. The result has been an impressive recovery in US equity indices of some 125 percent since the market lows of 2009.

Bernanke has indicated that the Fed will maintain both zero percent interest rates and massive QE into the foreseeable future. We must assume that such moves will continue to create dubiously impressive trends in spending and stocks.

Prudent investors are faced with a scenario where consumers may be persuaded to extend their purchasing of necessities and replacements to more discretionary items. If that happens, it could provide welcome short-term growth to the US and other economies in the world. Also, it may justify selective investment in domestic equities, particularly necessary commodities.

However, beneath the false enthusiasm of the markets will lurk threats to the US dollar, and of a potentially dramatic rise in US interest rates. These dangers demand extreme caution, especially in light of recent double-digit percentage rises in the stock market.

John Browne is a Senior Economic Consultant to Euro Pacific Capital. Opinions expressed are those of the writer, and may or may not reflect those held by Euro Pacific Capital, or its CEO, Peter Schiff.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

Order today a copy of Peter Schiff’s book The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country and save yourself 35%!

Right now, I remain bearish most commodity markets. The reason being, they simply have not fulfilled a short-term cyclical test of support. So, more downside is possible in gold, silver, oil, and an assortment of other commodities.

In fact, I expect we’ll soon see gold break down and plunge well below the $1,500 level and head even lower … silver crater through $26 and drop to below $20 … and crude oil plunge to below $70.

We’ll see food prices also get creamed. Sugar, coffee, cocoa, corn, wheat, and soybeans. Just about every commodity under the sun is soon going to sink further.

That’s because we’re not in the next phase of inflation yet. Rather, we’re in temporary deflation.

Deflation brought about largely because the only money that is moving these days is coming out of sovereign bonds and going into equities … and because taxes all over the world are headed up, threatening to send the rest of the capital that’s out there into hiding, rather than into business formation or investment.

But there’s also no doubt in my mind that …

Another Inflationary Surge

Is Coming One Day

For one thing, nearly $4 trillion of printed money is sloshing around the global banking system. Money printed by the U.S. Federal Reserve … by the European Central Bank … by the Bank of Japan … and by the Bank of England.

That money is mainly still in commercial banks’ coffers. It was designed to bail them out. And that it did.

But because loan demand is still soft, the banks aren’t lending. They soon will, and that money — $4 trillion worth — is likely to run rampant through the global economy.

I know …

The Federal Reserve and the other central banks are largely following Ben Bernanke’s lead — and they all believe that when the time comes, they can reel that excess liquidity back in, and prevent it from running rampant through the global economy. Thereby snuffing out the next inflation surge.

But in my opinion, there’s no way the central bankers are going to be able to reel that money back in, for two chief reasons:

But in my opinion, there’s no way the central bankers are going to be able to reel that money back in, for two chief reasons:

1. Once the banks start to see an increase in loan demand — instead of hoarding the money, they’re going to use it to make a slew of new loans — which is how banks make most of their profits. And …

2. Believe it or not, the central banks don’t understand interest rates. They think that they can raise rates at the appropriate time and that higher rates will quell loan demand, thereby pulling liquidity out of the system.

That might be true in a more normal economy, but in today’s economy, it’s totally backward. Why?

Because rates are so low to begin with, as rates rise, it’s likely to have the opposite impact: Investors and consumers will begin to realize that rates are going up — and they are then going to want to buy more and borrow more.

In other words, as the central banks raise rates somewhere down the road, they’re going to see precisely the opposite of what they intended …

A Surge in Credit and Loan Demand!

I’ve been waiting for the first signs that interest rates are headed back up again, because before they really take off, I want to buy a second home back in the USA and mortgage it to the hilt with cheap, borrowed money.

There are a lot more investors out there just like me. Millions of them.

And when that anticipation of a long span of rising interest rates comes, the $4 trillion the central banks printed will run like crazy through the global economy, pushing up overall price levels.

So the questions then become … “When will it start?”

“How high could inflation go?”

“What sectors will be impacted the most and what can I do to protect the value of my money?”

And “Where can I make the most profits?”

My answers …

First, while no one can accurately nail down when the next inflation surge will begin, all of my indicators tell me that we should start to see general, across-the-board price rises toward the end of this year.

Second, I do NOT believe the U.S. economy will ever see hyperinflation as we saw in Weimar Germany, in Zimbabwe, and in a host of other countries like Brazil and Argentina.

Reason: From a global perspective, core economies never experience hyperinflation. Only the peripheral economies do. Even Rome didn’t collapse from hyperinflation.

Third, the sector that will respond almost immediately will be none other than the same sector that responded the most in the earlier wave of rising inflation: Commodities, tangible assets, natural resources.

But don’t kid yourself on equity markets. They too will rise, even more rapidly than they currently are, as inflation lifts equities.

Fourth, some of the biggest profits you’ll ever see in your lifetime will come from equities in the natural resource sector. Companies that leverage the power of the underlying commodities they explore for, refine, produce, sell and distribute.

But again, we are not there yet. Real inflation is not here yet and will NOT begin for several more months. Instead, deflation is still the major near-term threat.

So, as always, stay tuned …

Best wishes,

Larry

After Cyprus Bank Bailout, Depositors Race to Withdraw Their Cash. Is the Rest of Europe, the US Next?

After Cyprus Bank Bailout, Depositors Race to Withdraw Their Cash. Is the Rest of Europe, the US Next?

A small bailout in a small state has roiled the global financial markets and triggered a political backlash as far away as Russia. Euro and shares slide over fears that Cyprus could trigger bank runs in other countries

The €10-billion Cyprus bailout breaks taboo of hitting bank depositors with losses, After all-night Friday talks, euro finance ministers agreed a €10-billion bailout for the stricken Mediterranean island and said since so much of its debt was rooted in its banks, that sector would have to bear a large part of the burden.

The hit imposed on Cypriot bank depositors by the euro zone has shocked and alarmed politicians and bankers who fear the currency bloc has set a precedent that will unnerve investors and citizens alike.

“This is an unprecedented decision for a eurozone country. It is also one whose potential consequences reach much further than an island in the eastern Mediterranean. It threatens to cause the transmission system between the economic and financial sectors on one side and the political and social on the other to seize up. Without this, the euro cannot be propelled forward. It cannot function.”

. …the latest:

…the latest:

Cyprus bailout deal rattles investors around the world

The Cyprus bailout broke ‘the cardinal rule’

Cyprus Delays Vote on Bailout Plan

Cyprus bailout crisis shakes markets

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair