Bonds & Interest Rates

Rome will have a new pope before Italy gets a new government. Good job there’s no rush…

Rome will have a new pope before Italy gets a new government. Good job there’s no rush…

ROME has now been without a government since mid-December. Italy’s politicians will only start to talk later this week about doing something about last month’s failed elections. Barely a month after Benedict XVI resigned, the Catholic world will have a new pope before Italy gets a prime minister. It’s lucky there is no rush.

Italy’s debt was downgraded on Friday by the Fitch ratings agency. Interest rates have already risen further since then. Rome goes back to the bond market to raise new finance this Wednesday. Yesterday meantime brought a cut to the GDP figure reported for end-2012, now shown shrinking by 0.9% from three months earlier.

Can Italy shake itself out of this mess? Apparently at opposite ends of the political spectrum, both Beppe Grillo and Silvio Berlusconi have catalysed discontent with European politics, very often blaming the Euro as ultimate responsible for the crisis. But what would happen if the political programme of Grillo’s 5 Star Movement came to reality, and more specifically if Italy decided through a referendum to leave the Euro?

What if the Italian debt was restructured? And if these hypotheses don’t become reality, which scenarios are likely to take place instead?

#1. Italy chooses to leave the Euro

Returning to the Lira would mean that private savings would be redenominated in the old currency (well, a new currency with an old name), and be devalued. Savers would get poorer in real terms, losing purchasing power overnight. After all, going back to the Lira would be chosen exactly because it gave monetary sovereignty back to Italy. And what tradition could be more Italian than devaluing the Lira?

But this leads to the next question: would the ‘old’ public debt be redenominated as well? It seems unlikely, as creditors would not accept such a loss in real terms. The consequences of having a public debt denominated in Euro while devaluing the Lira are easy to imagine.

#2. Restructuring the public debt

Restructuring debt is normally a consequence of a default. Letting Italy reach that stage would clearly present a hazard to all Eurozone states. But cutting interest rates on bond contracts that have already been agreed would also be a heavy blow for Italian banks, and for households too. Because 63% of the public debt is owned domestically. Consequently, Italy would have a hard time trying to finance new debt after stinging its own citizens, most especially if it had just quit the Euro and lost the support of the European Central Bank.

#3. Italy muddles through

If Italy both stays in the Eurozone and avoids the extreme measure of debt restructuring, it seems unavoidable that the austerity of the past few months would continue. Italy could still finance its debt, with a little help from the ECB if needed. But only with some strict conditions, of austerity plus growth.

We’ll leave to the reader’s discretion whether austerity and growth can be used in the same sentence. But it is certain that the pain heaped on voters by “muddle through” would leave Italy repeatedly exposed to fresh debates over leaving the Euro or restructuring the public debt. Only, with the pain growing worse, the element of “choice” could be removed – making Euro exit and creditor losses an extreme but inevitable consequence of the failure to address or resolve Italy’s deep financial problems.

#4. Italy loses its independence

We’ll divide this scenario into two subcategories, one of which may sound familiar to Italian readers at least.

First, there’s a potential loss of sovereignty. Because extreme situations require extreme measures. The chance of compulsory administration by European authorities can’t be ruled out. In fact, and for good or for bad, the appointment of Mario Monti as prime minister to rescue Italy from the brink in autumn 2011 was a loss of national sovereignty.

This is a consequence of community life: many indignities will be permitted to avoid contagion. It seems fair to believe that the recent electoral result exposes Italy to this happening again, with Rome’s 16 Eurozone partners imposing their own victor.

Another possibility, and again with loss of sovereignty for Rome, would however be at the extreme opposite of the spectrum. Because it would see the expansion of European monetary and economic unity to include political and fiscal unity as well. This is probably very unlikely to happen in the short term. We know that the punctual German taxpayer is not particularly flattered by the idea. Yet the European Union’s own leaders believe it is a possible scenario, and the best. And they after all are in charge for the time being.

With so many politicians trying to take control, is there a way for a private citizen to protect his or her own financial independence and freedom? What we know for sure is that in the last few weeks the Italian phonelines here at BullionVault have started to ring more frequently.

“I’m sure I’m not the only Italian contacting you to buy gold in this situation,” says G.F. from Naples, explaining he has decided to invest in some gold to protect his savings in case the Euro collapses or Italy goes back to the Lira. And if the debt crisis worsens and turns unmanageable, who will pay in the end? Not the debtors, that’s for sure: they don’t have any money. Creditors always pay, and providing the funds they accepted that risk.

Owning physical gold would certainly be a great advantage if either of the first two scenarios above became real. Gold is an international asset, it does not represent a credit, and it is not bound to national or monetary policies. It can’t be reproduced or have its value debased at command, nor through a referendum either. Traditionally and in the worst crises, gold guarantees individual sovereignty and financial independence, an autonomy of choice, movement and action.

Yet this crisis insurance has been getting cheaper for Italian savers. Over the past few weeks the gold price in Euros dropped to the same level of November 2011. It is currently around €39,000 per kilo, when just six months ago it reached a fresh record peak of €44,300. Only uncertainty seems to be inevitable in Italy. But anyone interested in taking out insurance against a Euro exit or debt write-down might find it useful to remember that physical gold is not a credit. It can’t be restructured. It does not carry default risk.

Alessandra Pilloni

BullionVault

Published novelist and former language consultant Alessandra Pilloni is European operations executive for Italy at BullionVault, the world-leading gold and silver exchange for private individuals. Alessandra’s views and comment on precious metals investment are regularly sought by both Italy’s mainstream media and specialized blogosphere, among them Il Sole 24 Ore,La Stampa and Panorama.

(c) BullionVault 2013

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

History shows this does not end well.

Jim Rogers decries the growing uncertainty and recklessness of global central planners as the world enters unchartered financial markets:

For the first time in recorded history, we have nearly every central bank printing money and trying to debase their currency. This has never happened before. How it’s going to work out, I don’t know. It just depends on which one goes down the most and first, and they take turns. When one says a currency is going down, the question is against what? because they are all trying to debase themselves. It’s a peculiar time in world history.

I own the dollar, not because I have any confidence in the dollar and not because it’s sound – it’s a terribly flawed currency – but I expect more currency turmoil, more financial turmoil. During periods like that, people, for whatever reason, flee to the U.S. dollar as a safe haven. It is not a safe haven, but it is perceived that way by some people. That’s why the dollar is going up. That’s why I own it. Will I own it in five years, ten years? I don’t know.

It makes it extremely difficult for the investor looking for acceptable risk/reward or the saver looking to protect their purchasing power; as in Rogers’ view, all options have their problems:

I own gold and silver and precious metals. I own all commodities, which is a better way to play as they debase currencies. I own more agriculture than just about anything else in real assets because…

…..read more HERE

This Excerpt is from a thirteen minute publication from March 7th where we cover seven countries … including a full-blown breakdown of the US Fed’s Beige Book, and the latest macro-data, with a specific focus on the US Treausury market …

… along with a look at German and French macro-data, and the Italian markets …

… a two-stop tour of South America …

… and a look at last night’s data from Australia.

But how do we know when irrational exuberance has unduly escalated asset values?

But how do we know when irrational exuberance has unduly escalated asset values?

Into this academic but high-staked market fog has stepped another Fed official, this time not a Chairman but a relatively new yet similarly quizzical Governor. Jeremy Stein’s February 2013 speech has not gained the attention that Chairman Greenspan’s did, but it is remarkably similar in its intent and initial question: Governor Stein asks, “What factors lead to overheating episodes in credit markets?… Why is it that sometimes, things get out of balance?” Without mimicking Chairman Greenspan’s phrase, Governor Stein renews the quest, asking nearly a decade and a half later, “How do we know when irrational exuberance has unduly escalated asset values?”

I suppose it’s fair to criticize both queries on two grounds: 1) Although asked by Chairman Greenspan, it was never really answered in the 1996 speech. 2) If the Fed’s so smart, why are some of us still poor? Why did our 401(k)s become 201(k)s in 2009 before recovering to near peak levels currently? If they’re so smart, why the roller coaster ride, the 30% decline in home prices since 2006, and our current 7.9% unemployment rate?

Well to answer for the absent Chairman and the necessarily silent Governor Stein, the Fed incorrectly assumed that as long as inflation was benign, and future productivity prospects were near historical proportions, then asset price exuberance was an indirect and much less significant influence on economic growth. The Chairman admitted as much in a public “mea culpa” several years ago. We’re not that smart, he seemed to intone. Sometimes we make mistakes. I’m with you there, Mr. Chairman. Sometimes we all do.

So let’s approach this new paper with eyes wide open and pant bottoms close to those mythical musical chairs. Governor Stein’s speech reflects importantly on the answer to the question asked by a recent Wall Street Journal headline: “Is (the) Bull Sprint Becoming a Marathon?” Is there indeed “A Boom Time” in markets as the Financial Times queried on the heels of Dell, Virgin Media, and then HJ Heinz?

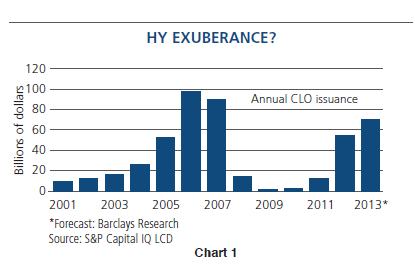

Governor Stein, as does PIMCO, suggests caution. On a scale of 1-10 measuring asset price “irrationality”, we are probably at a 6 and moving in an upward direction.Admittedly, Stein never ventures into the netherworld of stock market prices or leveraged buyouts. He appears to know better. What he does stake claim to however is a thesis for high yield spreads with the implication that other credit markets bear similar consequences. His initial starting point is that the pricing of credit is primarily an institutional as opposed to a household decision making process. Individuals may become unduly irrational when it comes to buying high yield ETFs or mutual funds, but it is the banks, insurance companies and pension funds, to name the most dominant, that influence the price of credit – high yield bonds – and by osmosis, investment grade corporates, municipals, and other non-Treasury risk credit assets. From this initial premise, he then points to recent research by Harvard’s Robin Greenwood and Samuel Hanson that suggests that while credit spreads are helpful future guides, that a non-price measure – the new issue volume (and perhaps quality) of high yield bonds – is a more trustworthy input. To quote: “When the high-yield share (of issuance) is elevated, future returns on corporate credit tend to be low.” And because of financial innovation and easier regulatory changes, institutional buyers such as banks, insurance companies and pension funds tend to match the mountains of issuance with an exuberance that eventually can be labeled irrational. Stein’s bottomline is that recent evidence suggests that we are seeing a “fairly significant pattern of reaching-for-yield behavior emerging in corporate credit.” In fact, investors bought over $100 billion of high yield and levered loan paper last year, a record level even exceeding the ominous levels in 2006 and 2007. Shown below in Chart 1 is a history of CLO issuance, admittedly a subset of high yield, but one which illustrates the supply pattern Governor Stein is leery of.

Now at this point, I suppose readers expect yours truly to jump all over the Governor’s speech/premise and to advance my own more learned thesis. Not really. With previously expressed reservations about the prescience of the Fed (or any of us!) I applaud his attempt to answer the initial 1996 question. I think Governor Stein’s speech was a little uni-dimensional, and a little too supply and model driven as opposed to behaviorally influenced, but I liked it, and PIMCO agrees with its conclusion. Corporate credit and high yield bonds are somewhat exuberantly and irrationally priced. Spreads are tight, corporate profit margins are at record peaks with room to fall, and the economy is still fragile. Still that doesn’t mean you should vacate your portfolio of them. It just implies that recent double-digit returns are unlikely to be replicated and that when today’s 5-6% high yield interest rates are adjusted for future defaults and recovery values, that 3-4% realized returns are the likely outcome. Just this past week the Financial Times reported that global corporate default rates are inching higher just as companies with fragile balance sheets sell large amounts of debt. Don’t say Governor Stein didn’t warn you.

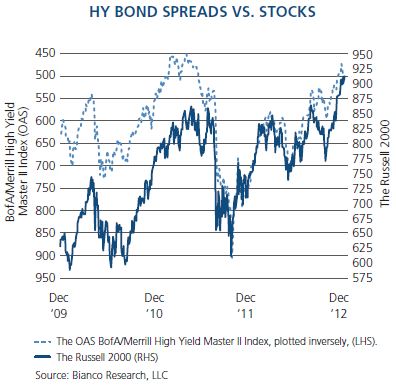

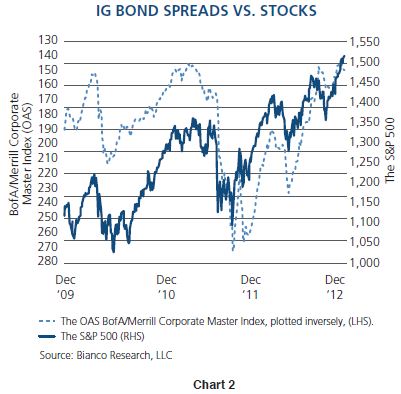

But I would step now into the forbidden territory of equity pricing by presenting additional historical correlations compiled by Jim Bianco of Bianco Research – admittedly not a thickly populated academically staffed organization like the Fed, but a well-regarded one nonetheless. He points out in a recent daily release that high yield and corporate bonds are really just low beta equivalents of stocks. It appears that they are. The following charts show a rather commonsensical negative correlation of high yield spreads (and therefore future high yield returns) to stock prices.

The conclusion would be that where high yield prices go, stock markets follow, or vice versa. Narrow yield spreads in high yield credit markets appear to be accompanied by “narrow” equity risk premiums in the market for stocks, which is another way of saying that the course of future equity returns may not resemble its recent exuberant past. 3-4% high yield returns over the next few years? Why shouldn’t that logically lead to a generalized 5-6% return forecast for stocks? Admittedly, returns for both high yield and equity markets have been unduly influenced in the past few years by Quantitative Easing, the writing of trillions of dollars of Federal Reserve checks and the exuberant migration of institutions and households alike to the grassier plains of risk assets dependent on favorable economic outcomes. It is what central banks encourage and to date it has been successful. If and when that support dissipates or if the economy remains anemic, investors should be cautious and temper their enthusiasm.

PIMCO’s and Governor Stein’s “rational temperance,” in contrast to excessive historical bouts of “irrational exuberance,” simply counsels to lower return expectations, not to abandon ship. PIMCO is a global investment manager – not one with a perpetual frown or even an ever-present half empty glass – but one which hopes to provide alpha and above market returns while still standing tall in the aftermath of future irrational bouts of exuberance. We join with Governor Stein and perhaps Alan Greenspan in encouraging not an exit but a reduced expectation. Credit spreads nor interest rates cannot be artificially compressed forever, nor can stock prices rise perpetually on their coattails. Be rational, be optimistic if so inclined, but temper it with a commonsensical conclusion that we have seen something similar to this before, and that previous outcomes seldom matched the exuberance.

IO Speed read:

1) Chairman Greenspan’s “irrational exuberance” speech in 1996 posed an excellent question, and history provided the answer.

2) Fed Governor Jeremy Stein asks the same question in 2013 with a uni-dimensional but useful model.

3) Stein’s paper, accompanied by correlations from Bianco Research, suggests caution in today’s high yield market.

4) High yield bonds, stock prices and other risk spreads move in relative tandem.

5) PIMCO cautions “rational temperance”: be bullish if you want, but lower return expectations on all asset classes.

Mr. Gross is a founder, managing director and co-CIO of PIMCO based in the Newport Beach office. He has been with PIMCO since he co-founded the firm in 1971 and oversees the management of more than $1.9 trillion of securities. He is the author of numerous articles on the bond market, as well as the book, “Everything You’ve Heard About Investing is Wrong,” published in 1997. Among the awards he has received, Morningstar named Mr. Gross and his investment team Fixed Income Manager of the Decade for 2000-2009 and Fixed Income Manager of the Year for 1998, 2000, and 2007 (the first three-time recipient). He received the Bond Market Association’s Distinguished Service Award in 2000 and became the first portfolio manager inducted into the Fixed Income Analysts Society’s hall of fame in 1996. Mr. Gross is a seven-time Barron’s Roundtable panelist (2005-2011), appearing in the annual issue featuring the industry’s top investment experts, and he received the Money Management Lifetime Achievement Award from Institutional Investor magazine in 2011. In a survey conducted by Pensions and Investments magazine in 1993, he was recognized by his peers as the most influential authority on the bond market in the U.S. He has 43 years of investment experience and holds an MBA from the Anderson School of Management at the University of California, Los Angeles. He received his undergraduate degree from Duke University.

The BofA Merrill Lynch High Yield Master II Index is an unmanaged index consisting of U.S. dollar denominated bonds that are rated BB1/BB+ or lower, but not currently in default. BofA Merrill Lynch Corporate Master Index is an unmanaged index comprised of approximately 4,256 corporate debt obligations rated BBB or better. These quality parameters are based on composites of ratings assigned by Standard and Poor’s Ratings Group and Moody’s Investors Service, Inc. Only bonds with minimum maturity of one year are included. The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. ©2013, PIMCO.

During his testimony before Congress this week, Federal Reserve Chairman Bernanke made it a priority to dampen the growing concern that the unprecedented growth of the Fed’s balance sheet presents great risks to the economy. There has been a heightened sense even among normally complacent members of Congress that the Fed could spark a precipitous decline in the economy and the financial markets if and when it seeks to “withdraw liquidity” by selling even a minor portion of its bond portfolio (which is projected to swell to $4 trillion by year end). This is a valid concern that I have been discussing for years.

During his testimony before Congress this week, Federal Reserve Chairman Bernanke made it a priority to dampen the growing concern that the unprecedented growth of the Fed’s balance sheet presents great risks to the economy. There has been a heightened sense even among normally complacent members of Congress that the Fed could spark a precipitous decline in the economy and the financial markets if and when it seeks to “withdraw liquidity” by selling even a minor portion of its bond portfolio (which is projected to swell to $4 trillion by year end). This is a valid concern that I have been discussing for years.

Gentle Ben soothed these fears by his novel assertion that the Fed doesn’t actually need to sell bonds to neutralize previously injected stimulus. Instead, the Fed could simply allow its bonds to mature, thereby achieving a more natural, and potentially less disruptive unwinding of its gargantuan portfolio. Although his explanation seemed to satisfy many of the Congressman (and the vast majority of the journalists who slavishly dote on Bernanke’s assurances), the idea is completely absurd.

As a result of its previous efforts during “Operation Twist” (which was conducted in order to push down long-term interest rates), the Fed has already swapped hundreds of billions of dollars of short-term securities for Treasury bonds with maturities of ten years or longer. Only a small portion of the Fed’s portfolio, then, becomes due at any given time. The average maturity of the entire portfolio is now over 10 years. There may well come a time when inflation or asset bubbles become so pronounced that aggressive withdrawal of stimulus is needed. Forceful action will only be possible through active selling, not simply by passive maturation.

However, either approach will be insufficient to tighten policy without a simultaneous cessation of buying of newly issued Treasury bonds. After all, to shrink the size of its balance sheet the Fed must stop adding to it…or at least add less than it is subtracting. Even if the Fed had the luxury of holding its bonds to maturity, such a stance would not prevent a collapse in the bond market. The Treasury does not have the cash needed to retire maturing bonds if the Fed stops rolling them over. As the government will have to sell the new bonds to other buyers, one way or another additional supply is going to hit the market.

The Federal government is projected to run trillion dollar deficits for years to come. To cover that gap, the Treasury will need to continuously sell new bonds. This need will persist regardless of the Fed’s policy priorities. For the last few years the Fed has been by far the biggest buyer of Treasuries, in recent times sucking up more than 60 percent of the total issuance. According to some reports, the Fed is expected to buy up to 90 percent of Treasuries in 2013. The only other significant buyers are foreign central banks (who buy for political reasons) and nimble hedge funds. Who does Bernanke expect will fill his shoes when he stops shopping?

To answer that question you must consider the economic environment that would compel the Fed to tighten in the first place. Presumably a period of accelerating economic growth, surging inflation, or rising interest rates would trigger asset sales. In such a situation, who in the world would want to buy low-yielding, long-term government paper while inflation is surging, the dollar is falling, and interest rates are rising? With the Fed on the sidelines, such an investment would be a guaranteed loser. Bernanke claims that the financial conditions will be soothed by an aggressive communications campaign that would let market participants know, in advance, precisely how the Fed intended to dispose of its assets. The cardinal rule in investing is that big players never telegraph their intentions. Fed “transparency” will simply mean that the hedge funds now making money by getting in front of the buying will be making even more money by getting in front of the selling! There will be no cavalry of new buyers riding to the rescue.

This means that any attempt to tighten, no matter how passive, will result in a significant drop in the price of U.S. Treasuries and mortgage-backed securities. Not only would this inflict massive losses to the value of the Fed’s balance sheet but it would exert enormous upward pressure on interest and mortgage rates that the Fed will be unable to control.

In addition to his absurd “let them mature” gambit, Bernanke also announced other novel policy tools that will supposedly help him orchestrate a successful exit strategy, most notably raising the rates paid on funds held at the Federal Reserve. Such a move is expected to deter banks from lending into a surging economy or to invest in risky assets by enticing them to park cash at the Fed. But how high must these rates go, and how much would it cost the Fed (in reality U.S. taxpayers) to do this effectively? Given how high I believe inflation will become, these payments could be truly staggering. The net result will be a substitution of large operating losses for large portfolio losses (which would have come from bond sales).

As I have said many times before, the Fed has no credible exit strategy. Its portfolio is far too large, and the economy, the housing market, the banks, and the government, are far too dependent on ultra-low interest rates to allow Bernanke any real options. In truth, his only exit strategy is to just talk about an exit strategy. Bernanke’s contention that the Fed need not sell any of its bonds is the closest thing yet to an official admission of this fact. Not too long ago Bernanke made the absurd claim that his intention to sell the bonds on the Fed’s balance sheet meant that he was not monetizing debt. How times have changed.

Bernanke is banking on the hope that his policies will jump start the economy which will then be able to motor along on its own. However, the current era of cheap money and fiscal stimulus will never create an economy that is capable of standing on its own legs. Instead, it is propping up a parasitic economy that is completely dependent on the very supports the Fed believes it can one day remove. But if the Fed does not remove them on its own, the markets eventually will.

Bernanke also defended himself against some members of Congress, particularly economically savvy New Jersey representative Scott Garrett, who pointed out the hypocrisy of Bernanke’s claims that Fed policies are responsible for the recent rise in home prices (while simultaneously absolving the Fed of any responsibility for rising home prices during the real estate bubble). To justify this claim, Bernanke made the self-serving distinction that while the Fed is currently purchasing mortgage-backed securities (in order to lower mortgages rates and boost home prices), no such actions existed prior to the 2008 financial crisis. As a result, he claims the Fed could not have been responsible for the bubble. On this point he is dead wrong.

Fed policy during the mid-years of the last decade had an enormous effect on mortgage rates and home prices. By holding short-term rates too low for too long, the Fed was responsible for the proliferation of Adjustable Rate Mortgages and the popularity of the ultra-low teaser rates without which the housing bubble never could have been inflated so large in the first place.

In other words, the Fed broke it then, but it sure can’t fix it now.

Much more at Euro Pacific’s Homepage HERE

About Peter Schiff

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair