Bonds & Interest Rates

Ah, someone appears to have done the arithmetic….

“Federal Reserve Chairman Ben S. Bernanke’s efforts to rescue the economy could result in more than a half trillion dollars of paper losses on the central bank’s books if interest rates rise abruptly from recent levels.

“Federal Reserve Chairman Ben S. Bernanke’s efforts to rescue the economy could result in more than a half trillion dollars of paper losses on the central bank’s books if interest rates rise abruptly from recent levels.

That sum is the difference between the value of securities in the Fed’s portfolio on Dec. 31 and what they may fetch in three years, according to data compiled by MSCI Inc. of New York for Bloomberg News. MSCI applied scenarios devised by the Fed itself for stress-testing the nation’s 19 largest banks.

MSCI sees the market value of Fed holdings shrinking by $547 billion over three years under an adverse scenario that includes an economic contraction and rising inflation. MSCI puts the Fed’s mark-to-market loss at less than half that, or $216 billion, if the economy performs in line with consensus forecasts of gradually rising growth, inflation and interest rates.”

…..more on Interest Rates HERE

Each of the three great experiments in authoritarian government in the senior economy included some promotional inspiration. As Rome was corrupted from a republic to a police state the “Genius of the Emperor” provided compelling guidance. In the Sixteenth Century “Papal Infallibility” provided the front for a venal and corrupt bureaucracy. The current financial experiment started around 1900 and essential dogma has included the omniscience and omnipotence of central bankers.

The wonders of extremely intrusive government under the label of Communism was rejected by an always dissatisfied and, in 1989, suddenly critical public. The fall of the Berlin Wall was the symbol.

Just as suddenly, full-on socialism could not be sold to the public by control freaks. “The Freeman” in the early 1990s had an article that named the names that turned to environmentalism as a possibly more successful way to impose control. The most successful and at the same time the most dangerous within this political movement has been “Anthropogenic Global Warming” (AGW). Then, the promoters discovered that the climate has been warming for some 12,000 years and the pitch was morphed to “Climate Change”. The labels also included “Greenhouse Effect” and no matter what the weather event the “cause” has been the evils of free-market economies.

Research behind the effort was quite limited – the assumption has been that there has been only one influence upon the climate and that is atmospheric carbon dioxide. This was an IPCC selection from all of the influences upon climate. The main ones are solar energy, which is variable, and the amount received at the Earth’s surface, which also varies. Both variations are periodic – as are consequent warming phases and cooling phases.

On the nearer-term, Solar Cycle 23-24 has been the weakest since 1913. Solar physicists, Livingston and Penn, have been working on the possibility of diminishing solar output since the mid-1990s. A link to the 2008 review of their updated paper follows.

Subject: Livingston and Penn paper: “Sunspots may vanish by 2015′′. | Watts Up With That?

In early January, the UK Met Office quietly released their study that temperatures have not increased since 1998.

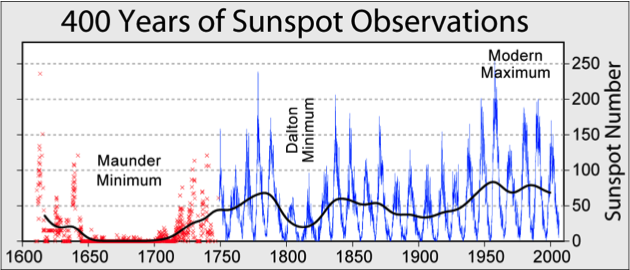

The chart below clearly shows the “Maunder Minimum” and the “Modern Maximum”, which is the period of unusually high output that prevailed from the 1940s to the 1990s. Prof. Solanki at the Federal Institute of Technology in Zurich states that this is the sun’s brightest period in a thousand years. Temperatures have been at the highest in a thousand years, but not as high as with the Medieval Maximum.

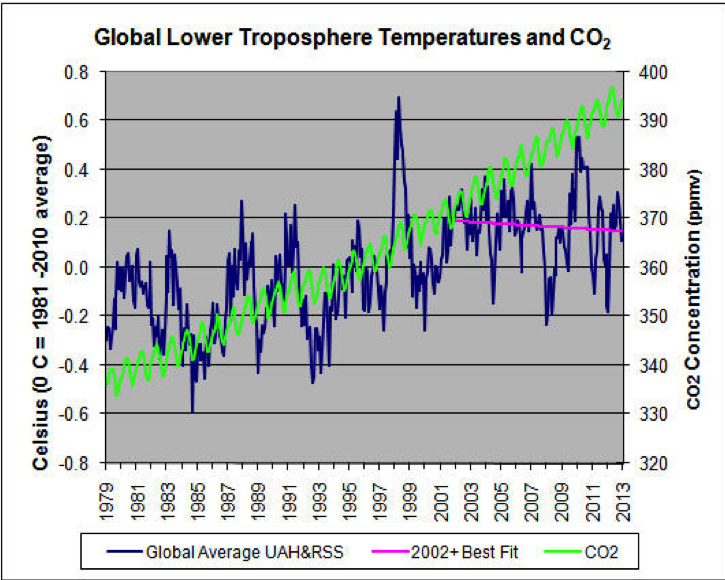

The latest warming trend seems to have stalled out, naturally, almost 15 years ago. The following chart (1979 to date) plots temperature history (blue line) trending sideways. CO2 (green line) is still going up. If the Left’s theories about CO2 were valid the rise in global temperature would be getting steeper. It isn’t. As in “paper covers rock”, solar energy trumps CO2.

Note CO2’s remarkably regular seasonal variation. This is explained as due to seasonal variation from plant life (land and sea) changing from emitting CO2, to absorbing CO2. Global commercial and industrial activity does not show the equivalent variation.

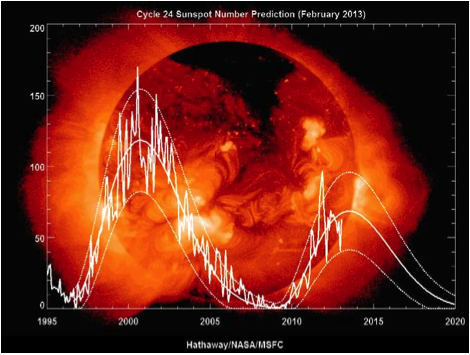

Beginning with the 1990s low, the next chart covers Cycles 23-24 when the high count was 170 sunspots with the peak in 2000. So far the high has been slightly less than 100 in 2011. This compares to the high of 254 in 1957.

Solar activity has been diminishing since and recently solar physicists have provided the research that explained and anticipated the decline to the lowest minimum since 1913. The current cycle has been scheduled to reach its best this year (one review expects this leg up to peak at 84 in August) and then turn down.

Livingston and Penn called for a significant decline in solar activity and the numbers are confirming it. Within a couple of years it could be concluded that the Modern Maximum is over. That the trend could continue to another minimum that would be as severe as the Maunder Minimum is uncertain.

The main thing is that IPCC was run by a political caste that selected theories about climate disaster and when necessary data were cooked to “prove” otherwise unsupportable notions. The goal was to create hysteria that could only be remedied through massive increases in taxation and intrusion upon private life.

The advance of science has always depended upon skepticism, sound data and logic. This authoritarian age has created some interesting departures. Throughout mankind’s history we have thrived during climate warming and suffered during extensive cooling. The IPCC insists that for the first time in history warming is harmful. Oh well, it goes with the ideology – the Berlin Wall was the first wall ever built to keep the people in rather than the bad guys out.

The last time the authoritarians made it dangerous to hold scientific theories that denied the politically correct ones was at the end of the last great experiment in intrusion. In the early 1600s Galileo was condemned for denying that the solar system rotated around the Earth.

A couple of pieces we published in 2009 concluded that the mania about “AGW”, or “Climate Change” was peaking. These are attached.

*****

Other Superstitions

Ambitious authoritarians promoted that only one thing was influencing climate change and that is the amount of CO2 in the atmosphere. That it makes up only 0.038% of the gases surrounding our planet does not matter. Nor does the long history whereby the amount of CO2 lags temperature change by some 400 to 800 years.

Of course, ambitious governments using one focus for control have not been limited to climate hysteria. Beginning in the early 1900s financial adventurers touted that a US central bank would end financial panics and disguised as the Federal Reserve System it was imposed. Original and subsequent promoters seem to have overlooked that the tout behind the formation of the Bank of England in 1694 was that it would “infallibly” lower interest rates. Naturally, to prevent financial disasters. There have been many since – usually two or three big ones per century. Sometimes severe enough for the establishment to distress itself about the inadequacies of the prevailing banking system. The other part of the pattern is that the same establishment during a financial mania boasts the current government financial agency will prevent things from going wrong.

In the 1873 Bubble enthusiasms were assured because the US did not have a central bank and the Treasury System was proof against contraction. At the crest of the 1929 Bubble enthusiasms were supported by the tout that the old and dreadful Treasury System was gone and replaced by a “scientific” Federal Reserve System.

The Fed was the first of over-rated concepts that were selected to serve authoritarian ambition.. The next was the grand idea that a central agency can and should “manage” a “national” economy. Keynesian theories were selected because they enabled a massive expansion of government, which extended its power through mainly one thing – the amount of money in circulation. Warm-mongers have been obsessed about atmospheric CO2 and policymakers have been obsessed about M1, M2, etc.

Financial history has a long record of dynamic economic expansions turning into eras of magnificent asset inflations – including financial assets. After the huge expansion of credit a long post-bubble contraction has followed. The feature of which has been severe recessions and weak recoveries.

Essentially on a global scale, when policymakers have discovered that there is no such thing as a “national” economy.

The financial mania that climaxed in 2007 virtually replicated all of the great bubbles since the first one in 1720. Ours was number six and 1929 was number five. And the record is that the senior central bank has never been able to keep a bubble going and has never prevented the lengthy post-bubble contractions.

Wrap

The next few years are going to be very interesting. Solar activity and its influence upon the warming trend that began out of the exceptionally cold winters of the late 1600s is ending. The Maunder Minimum became the Modern Maximum and the latter is ending. This would be supported by the sunspot count resuming its downtrend in the fall.

The establishment has been boasting that by manipulation of only one gas society can be saved from a self-inflicted climate disaster.

In 2007 the establishment boasted that through manipulation of interest rates a financial calamity was impossible. They had a “Dream Team” of economists. Then the same establishment admitted that it was the worst recession since the last Great Depression. Then they boasted that without their “stimulus” the 2008 Panic would not have ended. Now they admit that this has been the weakest recovery since the 1930s. This is the basic pattern of a post-bubble contraction.

The first business expansion out of the Crash is becoming mature and any weakening will be dangerous to an economy still over loaded with debt.

It should be understood that great financial manias and their consequent contractions have been regular events, as has been an unusually active sun and its recent decline. Mother Nature will continue to prevail. Implacable market forces will insist that debt be contracted and solar physics has arranged for a significant decrease in solar output.

*****

Fads in “Science”

“During the last 20 to 30 years, world temperatures have fallen, irregularly at first but more sharply over the past decade. Judging from the record of past interglacial ages, the present time of higher temperatures should be drawing to an end…leading into the next ice age.”

– National Academy of Science (NAS), 1974 – as quoted in Forbes, December 5, 2009

“The overwhelming majority of climate scientists agree that human activities, especially the burning of fossil fuels (coal, oil, and gas), are responsible for most of the climate change currently being observed.”

– National Academy of Science, Website, February 2012

Welcome to the Rational Fringe – FREE TRIAL SUBSCRIPTION

by BOB HOYE,

INSTITUTIONAL ADVISORS

WEBSITE: www.institutionaladvisors.com

James Grant thinks so…

BROKEN CLOCKS get a bad rap…at least they are right twice a day, quips Eric Fry in the Daily Reckoning.

Many are the objects, individuals and/or institutions who are lucky to be right once a day… or even once a year. Consider, for example, those poor souls who continuously predict rising interest rates. These “bond bears” have not been right once in the last 30 years.

Many are the objects, individuals and/or institutions who are lucky to be right once a day… or even once a year. Consider, for example, those poor souls who continuously predict rising interest rates. These “bond bears” have not been right once in the last 30 years.

The lesson is clear: Better to be a broken clock than a bond bear.

But even if bond bears are not right even once-a-three-decades, perhaps they will prove to be right once-a-generation… and perhaps that moment is now, or almost now.

So says James Grant, editor of Grant’s Interest Rate Observer. In a recent issue of his esteemed newsletter, Grant observed, “Today’s stunted interest rates, though not exactly unprecedented, are rare and remarkable. The world over, creditors are living on the equivalent of birdseed. Investors who once disdained sky-high yields today settle for crumbs…What are they thinking today?”

Grant answers his own question. Today’s bond buyers believe that “in an overleveraged economy, inflation is unachievable. So is growth, they have lately begun to insist. As for us, we hold a candle for both growth and inflation — and, in consequence, for our long anticipated, long overdue bond bear market.”

Grant hangs most of his prediction on fifth-grade arithmetic…or maybe advanced fourth grade: Debts are rising a lot. Revenues, not so much.

“Like a well fed teenager,” says Grant, “the national debt keeps growing and growing. On December 31, it bumped its head against the statutory ceiling that never seems to contain it. That would be $16.394 trillion, or the cash equivalent of 360.7 million pounds of $100 bills.”

Meanwhile, as the national debt continuously inflates by millions of pounds of hundred dollar bills, the national tax receipts struggle to keep pace.

“In the past 10 years to fiscal 2012,” Grant observes, “the compound annual growth in federal receipts worked out to 2.8%, that of federal outlays, 5.8%. In as much as the growth in receipts was much below the historical median (which, since 1967, had been 6.75% a year), one might — just for argument’s sake — say that the country had an income problem.”

Rapidly growing debt, coupled with slowly growing revenue, often creates a toxic environment for bonds. Bottom line: Grant is bearish on long-dated US Treasurys.

Eric Fry

for The Daily Reckoning

- January 31, 2013 — On Borrowed Time

- February 6, 2013 — S&P On the Kill List

- January 28, 2013 — US-China Relations: War in 2013?

- February 5, 2013 — The Charm of “Charm City”

- January 24, 2013 — Platinum’s Neglected Cousin

ART CASHIN: “A Dormant US Inflation Indicator Just Spiked, And It’s Got Me Thinking Of Weimar And Zimbabwe”

In an interview with King World News Veteran trader Art Cashin makes it clear he has been more concerned about the threat of inflation in the U.S. than most analysts. From that interview King World News:

“That having been said, the Federal Reserve Bank of St. Louis puts out what is called the ‘Monetary Stock.’ It is the ‘raw material’ of the money supply, and it has been dormant throughout the year.

The report for the first part of this year suddenly spiked higher, and it’s something that I’m going to keep a very close look at. It may be, and there is some seasonality, but I think people need to begin watching the money supply, particularly the M2, and see if that starts to accelerate…

If the velocity of money begins to accelerate and M2 begins to move up, then you will begin to hear people talking about or at least worrying about inflation again…”

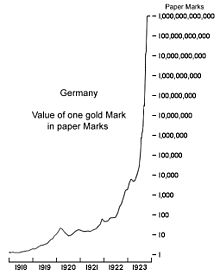

Cashin notes that this isn’t just theory, as we’ve not only seen it before in history, most people know of the most recent notorious experiences: Weimar Germany and Zimbabwe.

“Somebody once asked a famous literary character (who lived through the Weimar hyperinflation) how did he go broke? He said, ‘Slowly and then suddenly.’ The Weimar Republic saw inflation develop very slowly, and then suddenly. Once it developed it was almost like Zimbabwe except it was in a major nation, and destroyed the moral values of a whole civilization and basically led to the underpinnings of World War II.”

“Somebody once asked a famous literary character (who lived through the Weimar hyperinflation) how did he go broke? He said, ‘Slowly and then suddenly.’ The Weimar Republic saw inflation develop very slowly, and then suddenly. Once it developed it was almost like Zimbabwe except it was in a major nation, and destroyed the moral values of a whole civilization and basically led to the underpinnings of World War II.”

….read more at KingWorldNews HERE

A Must, Must, Must, Read…..says Peter Grandich

This is the way the world ends…

Not with a bang but a whimper.

T.S. Eliot

Investment Strategy

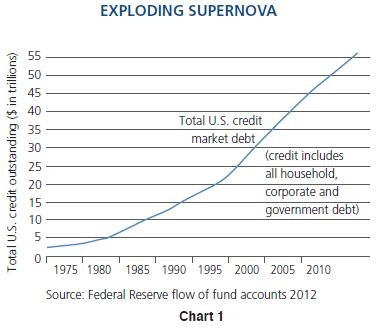

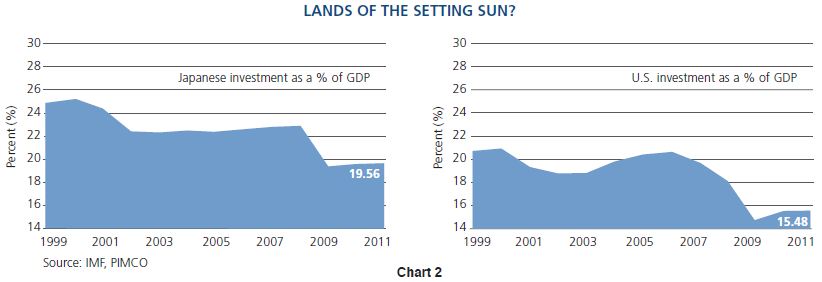

a) As it expands at a rate of trillions per year, real growth in the economy has failed to respond. More credit goes to pay interest than future investment.b) Zero-based interest rates, which are the result of QE and credit creation, have negative as well as positive effects. Historic business models may be negatively affected and investment spending may be dampened.c) Look to the Japanese historical example.

a) Seek inflation protection in credit market assets/ shorten durations.b) Increase real assets/commodities/stable cash flow equities at the margin.c) Accept lower future returns in portfolio planning.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Sovereign securitiesare generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government; portfolios that invest in such securities are not guaranteed and will fluctuate in value.Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government.Commodities contain heightened risk including market, political, regulatory and natural conditions, and may not be suitable for all investors.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair