Bonds & Interest Rates

In the years following the global financial crisis, economists and investors have gotten very comfortable with very high, and seemingly persistent, government debt. The nonchalance may be underpinned by the assumption that globally significant countries that can print their own currencies can’t get trapped in a sovereign debt crisis. However, it now appears that Japan is preparing to put this confidence to the ultimate stress test.

In the years following the global financial crisis, economists and investors have gotten very comfortable with very high, and seemingly persistent, government debt. The nonchalance may be underpinned by the assumption that globally significant countries that can print their own currencies can’t get trapped in a sovereign debt crisis. However, it now appears that Japan is preparing to put this confidence to the ultimate stress test.

For the better part of 20 years, successive Japanese governments and central bankers have been trying, unsuccessfully, to use quantitative easing strategies to pump up a deflated asset bubble. The economy has by and large not responded. The sustained and impressive growth that Japan delivered during the 45 years following the Second World War (which had made the country one of the most successful economic stories in world history), has never returned. For the last 20 years Japan has offered a “zombie” economy characterized by low growth, stagnation, and exploding government debt. The Japanese government now owes approximately $12 trillion, a figure representing more than 200% of GDP. The IMF expects that this figure will reach 245% by the end of this year. This gives Japan the unenviable title of having the world’s highest government debt-to-GDP ratio. But Shinzo Abe, the newly elected Prime Minister of Japan, and Haruhiko Kuroda, his newly-appointed Governor of the Bank of Japan, feel much, much more debt needs to be issued to turn the economy around.

The hope that Abe would be a new kind of prime minister with a bold economic formula helped revive the long dead Japanese stock market. Between May and November of 2012, the Nikkei traded within a range of 8200-9400. As Abe’s victory began to be expected, the Nikkei started moving up, reaching 10,000 by the time he was sworn in on December 26 of last year. The euphoria continued throughout the spring and by April 2 the Nikkei stood at 12,003 points. Then on April 4, BOJ Governor Kuroda made good on Abe’s dovish rhetoric and announced a plan to end years of mildly declining prices by doing whatever necessary to create 2% inflation (in reality these price declines have been one of the few consolations to Japanese consumers). To achieve its goals, the government is prepared to double the amount of Yen in circulation. Stocks immediately rallied, and in less than a week the Nikkei had breached 13,000 points, taking the index to a 4 1/2-year high. It is rare that any major stock market can achieve a 50% rally in less than a year. But the rally will be costly.

The Japanese government already spends 25% of tax revenue to service outstanding debt (compared to 6% in the US). These costs become even more astonishing when one considers the extremely low rates Japan pays. Ten-year Japanese government bonds now pay less than 0.6%, and five-year yields are now a little more than 0.20%. How much will debt service costs increase if Abe succeeds in pushing inflation to 2.0%? Two percent rates would triple long term borrowing costs. Given the size of its debts, increases of such magnitude could hit Japan with the force of 10 Godzillas.

Japan has an aging demographic and as more time goes by, the pool of potential bond buyers continues to shrink. Unlike the United States, where individual savers are mostly irrelevant in the sovereign debt market, Japanese investors have largely set the market in their own country. There is evidence to suggest that Japanese savers are increasingly considering overseas sources of yield for protection from the inflation that Abe is so determined to create.

As the Nikkei has moved upward, the Japanese Yen has taken the opposite trajectory, falling more than 20% against the U.S. Dollar since the beginning of 2012, and nearly 12% since the beginning of this year (the decline has been even greater in terms of several other currencies). This steep drop, which has taken a huge bite out of the nominal gains in Japanese stocks is unusual in the foreign exchange markets, and has threatened to destabilize an already weak global financial system.

Earlier this year the falling yen issue sparked a full-fledged headline war. On February 16th, participating members of the G20 issued a statement, clearly aimed at Japan, warning against competitive devaluations and currency wars. A day later, Japan’s Finance Minister stated flatly that Japan was not attempting to manipulate its currency. After some hesitation, the G20 seemed to accept this statement. For now it seems the international powers have fallen in behind Japan. Both IMF Chief Christine Lagarde and Ben Bernanke have praised Abe’s policies. The prevailing opinion seems to be that weakening a currency should not be considered manipulation as long as it’s done to revive a domestic economy, not specifically to harm competitors. Such an opinion qualifies as a great moment in rhetorical shamelessness.

In addition to his plans for inflationary monetary policy, Abe is also attempting to wage war from the fiscal side as well. His Liberal Democratic Party has called for over $2.4 trillion USD worth of public works stimulus over the next 10 years. This spending represents approximately 40% of Japan’s current GDP and, adjusted for population, would be the equivalent of nearly $600 billion USD annually in the United States.

It should be obvious to anyone with even half a brain that Japan’s prior experiments with ever larger doses of quantitative easing have failed. Leaders in both Japan and the United States, however, are following this path with reckless abandon. According to Abe, the entirety of Japan’s economic problems can be blamed on the fact that consumer prices have been declining by one tenth of one percent per year. If only Japanese consumers were forced to pay two percent more per year for the things they need or desire, all would be well.

Abe’s wish may already be coming true. McDonald’s announced this morning that, for the first time in 5 years, the price of hamburgers and cheeseburgers in Japan will be rising by 20% and 25% respectively. This is much needed relief for bored Japanese consumers who have likely grown tired of paying the same low prices year after year. No doubt they will be so excited by this development that they’ll will rush to the stores to buy more burgers before prices go up again. Of course there is no official concern that low-income Japanese will now have to pay more for low cost food.

The idea that informs Abe’s plan, that rising prices entice consumers to buy before the prices go up, is clearly suspect as economic law dictates that demand increases when prices fall. Any store owner will tell you that cutting prices is the best way to move merchandise. Apart from this problem, how does Abe expect consumers to buy more when their currency is losing purchasing power and more of their incomes will be needed to pay interest on the national debt?

The boldness of Abe’s plans should provide the rest of the world with a crash course in the ability of debt accumulation to jumpstart an economy. The good news is that the effects should not take too long to be seen. I believe that we will be treated with a stark lesson on the limitations of inflation as an economic panacea.

Hopefully, failure of this latest Japanese experiment will help convince leaders in the U.S. and Japan that the only true path to prosperity is free market capitalism. Rather than trying to reflate busted bubbles and micro-manage Keynesian style recoveries, politicians and central bankers should recognize their respective roles in creating the problems and get out of the way.

To order your copy of Peter Schiff’s latest book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

“We have never had every government debasing their currency at the same time. . . . This is the first time in recorded history where you have most of them doing it all together. These are perilous times . . . one way or another, this is going to end badly.”

Rogers, who owns Gold, on last week’s gold sell off – “This is normal. This is not unusual. I welcome it. I expect gold to go much, much, much higher over the next decade, but it will not and cannot until it starts having normal corrections.”

“If the U.S dollar becomes confetti, any number you want to make up. They’re printing U.S. dollars fast enough to turn them into confetti. Who knows how high gold will go as long as we have a mad man running the central bank.”

“If I had to bet on one thing in economics, my bet would be that the American Standard of Living is heading down and it is accelerating to the downside.” – Richard Russell April 12th/2013

“If I had to bet on one thing in economics, my bet would be that the American Standard of Living is heading down and it is accelerating to the downside.” – Richard Russell April 12th/2013

…..read it all HERE

We ended almost every one of nearly 100 webinars in 2011 with “Don’t Worry, They’ll Print the Money”. This is how confident my Co-Host, Ty Andros and I were that the global central banks had no other recourse but monetization.

We ended almost every one of nearly 100 webinars in 2011 with “Don’t Worry, They’ll Print the Money”. This is how confident my Co-Host, Ty Andros and I were that the global central banks had no other recourse but monetization.

We felt strongly that the western economies had passed the ‘event horizon’ and that the economic spiral was now inescapable.

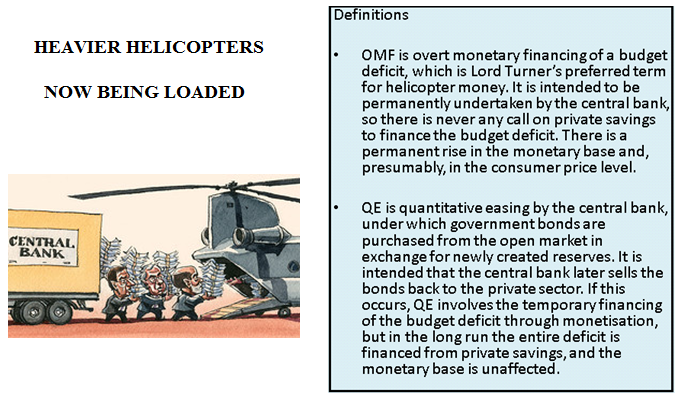

Outright Monetary Financing or OMF is what presently lies in front of us as QE¥ ends and it has profound implications for precious metals.

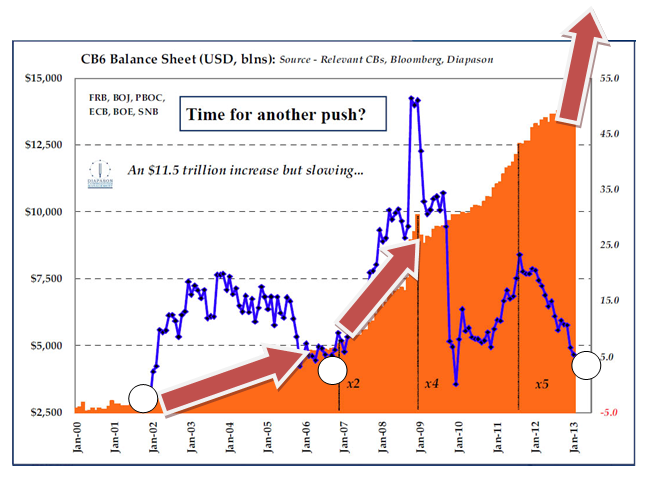

The charts as we will show are signaling that the smart money sees this and are already quietly laying down their bets. These players include the central banks not presently part of the Currency Cartel. The path however is going to be tricky and the charts also show why.

The global central bankers are feverishly loading the helicopters, but these are helicopters like we have never seen before.

We have been carefully observing that the global central bank balance sheet expansions have exhibited the following:

- Each new increase has been significantly larger,

- Each new increase has come with diminishing intervals,

- Each increase has been more coordinated between central banks,

- Each central bank balance sheet appears to keep the total expansion within a well defined boundary condition,

- Each time the TOTALRATE OF INCREASE approaches zero (see blue line below) it soon triggers the next increase.

…..read more HERE

This week, while economists should have been closely considering the implications of the actual bankruptcy of Stockton, California, they instead heaped scorn on the perceived ideological bankruptcy of David Stockman. In other words, Stockman trumped Stockton.

Ronald Reagan’s former Budget Director contributed “Sundown in America” a multi-page opinion piece to the Sunday New York Times which loudly and eloquently described the illusions of our current economic system. While I don’t agree with everything Stockman believes, I think he is showing great wisdom and courage in making dire predictions and calling for extreme changes in our policy and politics.

Ronald Reagan’s former Budget Director contributed “Sundown in America” a multi-page opinion piece to the Sunday New York Times which loudly and eloquently described the illusions of our current economic system. While I don’t agree with everything Stockman believes, I think he is showing great wisdom and courage in making dire predictions and calling for extreme changes in our policy and politics.

What was perhaps more surprising than the Times’ uncharacteristic decision to run the piece in the first place was the vitriolic and largely ad hominem backlash against Stockman that quickly emerged from across the political spectrum. The attacks have focused primarily on his history and personality, and not on his arguments. One would be hard pressed to find any journalistic reaction that did not use the words “screed” “rant” or “unhinged.” I believe these responses reveal an acute sensitivity from mainstream economists that arises from defending contorted Keynesian logic.

It can’t be easy to take the position that debt doesn’t matter and that spending creates economic growth. To do so with any hope of success requires team unity, and Stockman has never really been a team player. His reputation as an apostate and a naysayer has made him an easy target.

Famously, Stockman left the Reagan White House in protest over the Gipper’s half-finished mandate. Yes, Reagan had cut taxes, but he never really cut spending. Stockman never bought into the easy idea, championed by Jack Kemp and Dick Cheney, that deficits don’t matter and that tax cuts pay for themselves. And although the Reagan revolution did clear the way for a return to better growth in the 80’s and 90’s, Stockman knew that the piper would call someday to collect the debt. Despite his foresight on that topic, his criticism of the Reagan legacy has earned him the derision of the Republican establishment for whom that particular hero worship is sacred.

This may have informed the attack issued by neo-conservative apologist and Iraq war cheerleader, David Frum, who offered a solely psychological assessment: “Stockman provides an insight into the gloomy mindset that overtakes us in older age, it’s a valuable warning to those of still middle-aged that once we lose our faith in the future, it’s time to stop talking about politics in public.” So much for respecting our elders.

Bloomberg’s Jeff Kearns, whose support of Fed policy has earned him regular taps at Ben Bernanke’s televised press conferences, provided the most common mainstream dismissal of Stockman: “His warning that the Federal Reserve’s quantitative easing is steering the world’s largest economy toward a crash is at odds with nine quarters of job growth, record stock prices and unprecedented corporate earnings.” This “he must be wrong because things look good now” position supposes that economics can’t be understood or predicted, only observed. I received very similar treatment back in 2006 and 2007 when I tried to tell the mainstream that the real estate market was a house of cards. How could it be bad, they said, if it goes up every year?

Despite his misalignment with the Republican hierarchy, the Left has an even greater revulsion for Stockman. Since the crisis, he has become perhaps the most respected figure (with the possible exception of Alan Meltzer) to take the position that a system based on fiat currency is doomed. Those who most visibly argue these points, like Ron and Rand Paul, and myself, come from the libertarian movement. As a result, we can be easily dismissed as cranks. However, Stockman was once a card-carrying member of the power elite. His embrace of these principles is taken more seriously and is thus ripe for instant attack from liberal economists.

While the usual suspects of Jared Bernstein and Joe Wiesenthal weighed in with heaps of invective, the loudest heckles have come from, whom else, Paul Krugman. He began his multi-post campaign by questioning the “mystery” of why the New York Times would sully Krugman’s own gravitas by forcing him to share column inches with someone as “non serious” as Stockman. He then offers the back of his hand:

“I thought Stockman would offer some kind of real argument, some presentation, however tendentious, of evidence. Instead it’s just a series of gee-whiz, context- and model-free numbers embedded in a rant — and not even an interesting rant. It’s cranky old man stuff.” For the record, Stockman is only 66.

In actuality, Stockman’s NYT piece offers a litany of objectively dismal facts and cogent explanations of how we got here. While most are celebrating the nominal high of U.S. stocks (see my recent analysis of the current rally), he points out that in the five and half years it has taken for the S&P 500 to set a new high, “Real median family income growth has dropped 8 percent, and the number of full-time middle class jobs, 6 percent. The real net worth of the ‘bottom’ 90 percent has dropped by one-fourth. The number of food stamp and disability aid recipients has more than doubled to 59 million, about one in five Americans.” But Krugman fails to find the currency of his stock and trade, the macro-economic statistical models that attempt to describe how an economy works. In truth, those academic ordeals only matter in getting tenure and impressing the global elite. The real economy is much easier to understand.

Case in point: Stockton, California, which on Monday became the largest U.S. city to file for bankruptcy protection. Stockton, a city of 300,000 and two hours from San Francisco, is following the path blazed by many smaller California municipalities that have been unable to support lavish spending, salary and pension guarantees. And although Stockton has tightened its belt over the last few years (unlike similarly bankrupt San Bernadino, which is not even trying), it lacks the capacity to close the gap. Despite its enormous advantages in geography, infrastructure and location, the city is too bloated with government and clogged with taxes and regulation to allow for robust growth. As a result, Stockton is looking to pin the losses on its creditors.

As Stockman makes clear, the United States has been plagued by the same problems that doomed Stockton. His critics argue that the Federal Reserve’s printing press provides a foolproof immunity to such pedestrian problems. But in the end, these paper protections will only exist on paper. We’re all Stocktonians now.

To order your copy of Peter Schiff’s latest book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair