Bonds & Interest Rates

Good morning. Here’s what you need to know.

- Markets in Asia were mixed in overnight trading. The Japanese Nikkei fell 0.4% while the Shanghai Composite retreated 1.0%. European markets are mostly lower except for Germany and London, which are both currently up around 0.5%. In the United States, futures point to a positive open.

- China’s official manufacturing PMI fell to 50.6 in Aprilfrom 50.9 in March, below economists’ expectations fro a drop to 50.7. Any PMI reading above 50 signals expansion, so the 50.6 reading indicates that Chinese manufacturing is still expanding, but the pace of growth is slowing.

- South Korean exports seemed to confirm the theme,posting only 0.4% year-over-year growth in Aprilversus economists’ consensus prediction for a 2.0% advance. South Korean exports are referred to as the “economic canary in the coal mine” due to the country’s close trade relationship with China.

- In the U.K., manufacturing PMI unexpectedly rose to 49.8 in April from 48.6 in March, beating estimates for a tick down to 48.5. The 49.8 reading is below 50, which means the U.K. manufacturing sector still contracted in April, but much less than it did in March.

- ADP’s monthly employment report is released at 8:15 AM ET. Economists expect the report to reveal that 150,000 private payrolls were created in the U.S. economy in April, down from 158,000 in March. The release foreshadows the bigger nonfarm payrolls report due out on Friday.

- At 8:58 AM, Markit releases its final reading of U.S. manufacturing PMI for the month of April. Economists expect the index to come in at 52.0, matching the flash estimate published earlier this month, but down from March’s 54.9 reading.

- The ISM Manufacturing index follows at 10 AM. Economists predict the index will moderate to 50.6 from last month’s 51.3 reading, showing further evidence of slowing growth in American manufacturing.

- Also out at 10 AM are data on construction spending for the month of March. The consensus expectation is that growth in construction spending slowed to 0.6% in March after expanding 1.2% in February.

- At 2 PM ET, the Federal Reserve announces its latest FOMC monetary policy decision. Observers will be watching closely for any change in the language to acknowledge the recent slowdown in economic indicators, especially those dealing with inflation, which has trended down in recent months. This likely provides impetus for continued quantitative easing.

- Throughout the day, global automakers will be reporting April sales figures. Analysts predict total vehicle sales were 15.22 million units at a seasonally adjusted annualized rate in April, unchanged from March. Follow all of the data LIVE on Business Insider >

- BONUS: Runway model Kendra Spears is set to marry Prince Rahim Aga Khan, son of the Imam of the global community of the Shia Ismaili Muslims.

Please follow Money Game on Twitter and Facebook.

The Fed meets today and tomorrow. The ECB meets on Thursday. Those will be the defining market forces for the next three trading sessions.

The Fed meets today and tomorrow. The ECB meets on Thursday. Those will be the defining market forces for the next three trading sessions.

There is little if any point in trying to trade this week (at least until Thursday). The Fed is notorious for leaking info to the well-connected. The most recent “accidental” sending of a report a day early is just the latest example.

In simple terms, the market will be even more of an insider’s game today and tomorrow than usual. No point trying to open a new position in that window.

However, against this backdrop the big picture for the markets is growing worse and worse.

The US is almost assuredly back in recessionary territory. This is coming on the back of the weakest recovery (if you can call it that) in post-WWII history.

The Feds hide this economic nightmare by simply not counting those who are unemployed (lower the denominator in the fraction and your unemployment ratio falls), and by using bogus deflators in their GDP growth numbers (the current CPI is 2.1%… but the Feds calculated the first quarter GDP growth numbers use an inflationary measure of 1.2%).

Change your measurements and BOOM you’ve got a recovery. It works if you’re a Government bean counter trying to keep your job. It doesn’t work so well for everyone else.

However, there are clear signs we’re heading back into recessionary territory. I think the first quarter 2013 GDP growth print is the best we’ll see all year. And it’s very possibly things will get ugly before the year ends.

Speaking of which…

Ben Bernanke has announced he won’t be attending this year’s Jackson Hole meeting. A Jackson Hole meeting without the Fed Chairman is like having a performance of Hamlet without Hamlet himself in it. Why would the single most important Central Banker not attend one of the biggest economic meetings of the year?

He claims it’s due to scheduling conflicts. As if he didn’t know about this meeting in advance.

The fact is Bernanke is likely going to step down at the end of this term in January 2014… which means the markets will be losing one of their biggest props, the famed Bernanke Put.

God help whoever fills the role in the future. Assuming things hold together until next year (a BIG assumption) the new Fed Chairman will be inheriting one of the worst messes in history.

Investors take note, the markets are sending multiple signals that things are not going well in the world. Companies based on the real economy are dropping hard.

I’ve been warning subscribers of my Private Wealth Advisory that we were heading for a dark period in the markets. I’ve outlined precisely how this will play out as well as which investments will profit from another bout of Deflation.

As I write this, all of them are SOARING.

Are you ready for another Collapse in the markets? Could your portfolio stomach another Crash? If not, take out a trial subscription to Private Wealth Advisory and start protecting your hard earned wealth today!

We produced 72 straight winning trades (and not a SINGLE LOSER) during the first round of the EU Crisis. We’re now preparing for more carnage in the markets… having just seen another SIX trade winning streak…

To join us…

Best Regards,

Graham Summers

Tonight, this Deal Closes Forever

The price for The Perfect Trade is about to rise to $1499 per year.

We’re up 52% this year so far… CRUSHING the market, our competitors, even the legend’s hedge funds.

And we’ve done it with one trade, made once per week.

Want in on this strategy? You’ve got just four days to move…

Don Draper, Mad Men’s master advertiser likes to say “when you don’t like what they are saying, change the conversation.” When it comes to the current economic weakness, which was confirmed again today by the release of lower than expected GDP data, Washington would love do just that. Fortunately for them, they consistently outdo the master minds of Madison Avenue when it comes to misdirection. If the government doesn’t like what people are saying, they don’t bother just to change the conversation, they change the meaning of the words.

The latest example of this was revealed earlier this week when the Bureau of Economic Analysis (BEA) announced new methods of calculating Gross Domestic Product (GDP) that will immediately make the economy “bigger’ than it used to be. The changes focus heavily on how money spent on research and development (R&D) and the production of “intangible” assets like movies, music, and television programs will be accounted for. Declaring such expenditures to be “investments” will immediately increase U.S. GDP by about three percent. Such an upgrade would immediately increase the theoretic size of the U.S economy and may well lead to the perception of faster growth. In reality these smoke and mirror alterations are no different from changes made to the inflation and unemployment yardsticks that for years have convinced Americans that the economy is better than it actually is.

Today’s data release confirms that the economic “recovery” is weaker than expected and remains heavily dependent on Federal support. Personal spending was indeed up 3.2%, the biggest jump in two years, but real earnings were down by 5.3%, the biggest fall since 2009. Not surprisingly the buying was made possible by a drop in the savings rate, which came in at just 2.6%, the lowest since the 4th quarter of 2007. No doubt, rising home prices and falling mortgage rates (made possible by Fed stimulus) allowed Americans to refinance their homes and to borrow and spend the money that they did not earn. With GDP continuing to disappoint, a statistical make-over couldn’t come at a more convenient time.

In the simplest terms, GDP is calculated by combining a nation’s private spending, government spending, and investments (while adding trade surplus or subtracting trade deficits). Business spending on R&D, a portion of which comes in the form of salaries,has traditionally been considered an expense that does not explicitly add to GDP. But now, the United States will lead the rest of the world in redefining GDP. Washington has now declared that the $400 billion spent annually by U.S. businesses on R&D will count towards GDP. This equates to about 2.7% of our nearly $16 Trillion GDP. The argument goes that, for example, the GDP generated by iPhones has far exceeded the cost spent by Apple to develop the product. Therefore, Apple’s R&D is not an expense but an investment.

The BEA also argues that the cost of producing television shows, movies, and music should count as investments that add to GDP. Supporters of the change often hold up the blockbuster television comedy Seinfeld as an example. Given that the show’s billions in earnings far exceeded its initial costs, they argue that the production expenses should be considered “investments” (like R&D) and be added into GDP.

Economists who have staked their reputations on the efficacy of Keynesian growth strategies have argued that such changes will more accurately reflect the realities of our 21st century information economy. But their analysis ignores the failures so often associated with R&D and artistic productions. For every breakthrough iPhone there are dozens of ill-conceived gizmos that never get off the drawing board. For every Seinfeld, there are countless failures and bombs that leave nothing but losses.

In essence, the new methodology is an exercise in double accounting. For instance, suppose a company employs an accountant who works in the sales department, who is then transferred to the R&D department at the same salary. He still counts beans but now his salary will be billed to the R&D budget rather than sales. In the old methodology, the accountant’s impact on GDP would come only from the personal consumption that his salary allows. Going forward, he will add to GDP in two ways: from his personal consumption and his salary’s addition to his company’s R&D budget. The same formula would apply to a trucker who switches from a freight company to a movie production company (for the same salary). If he moves refrigerators, he only adds to GDP through his personal spending, but if he hauls movie lights, his contribution to GDP is doubled. It makes no difference if the movie bombs.

These double shots are different from traditional investments, which inject savings (or idle cash) back into the marketplace. Until money from personal or corporate savings is invested, it is not adding to GDP.

Another change that will artificially boost GDP concerns how government salaries will be counted. Unlike most private sector compensation, wages, salaries, and pension contributions paid to government workers are added directly to GDP. This distinction makes sense and eliminates potentially double accounting. Profits generated by private companies add to GDP when they are ultimately spent or invested by the company. Wages reduce profits, and therefore reduce GDP. But that reduction is cancelled out by the consumption of the employee receiving the wages. Governments do not generate profits, so salaries are the only way that public spending adds back to GDP.

The new system magnifies the GDP impact of government pensions, which are a principal component of public sector compensation. Going forward, the pensions will be calculated not from actual contributions, but from what governments have promised. Under the old system, if a state had a $10,000 pension obligation but only contributed $1,000, only the $1,000 would be added to GDP. Under the new system the entire $10,000 would be counted. So now governments can magically grow the economy simply by making promises they can’t keep.

The bottom line is that now certain private sector salaries (in R&D and entertainment) will be counted twice and public pension contributions will be counted even if they aren’t made. The economy will not actually be any larger or grow any faster, but the statistics will claim otherwise. With the stroke of a pen, our debt to GDP ratio will come down. Will this soothe the fears of our creditors? Will critics of big government take comfort that spending as a share of GDP may be lower? My guess is that the government is confident that its trick will work, and that distracting attention with a statistical illusion is the sole motivation for the change.

A similar type of hocus pocus has been successfully used to make inflation appear much smaller. A few months ago I produced avideo showing how changes in methods used to calculate the Consumer Price Index (CPI) have resulted in a widening gap between increases in real prices and the CPI. The changes, that incorporate such concepts as hedonic adjustments and substation bias, were made to make the CPI more “accurate,” but have instead produced consistently lower results. Although I used a basket of 20 goods for that experiment, I gave particular attention to such things as newspaper and magazine prices and health insurance costs. But just recently I came across another data set that leads to the same conclusion.

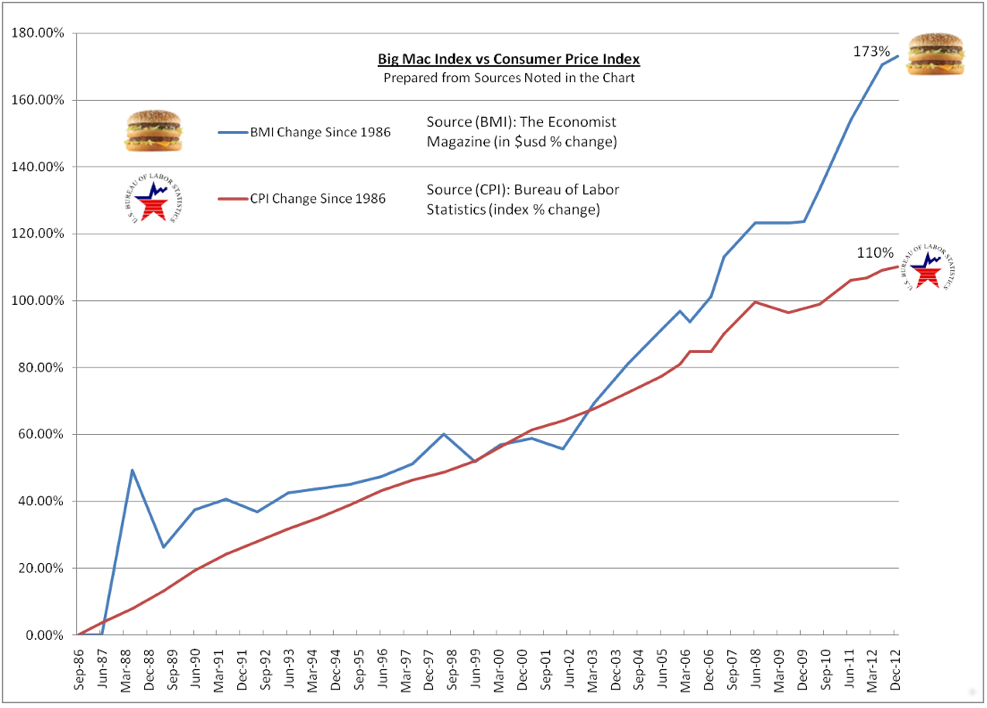

Since the late 1980’s, The Economist Magazine has compiled something called the “Big Mac Index,”(BMI) a global survey of the cost of McDonald’s signature hamburger. Although the index is primarily used as a means to compare purchasing power parity around the globe, it also can be used to track the prices of Big Macs in the U.S. over many years.

From 1986 to 2003 the U.S. BMI rose roughly in line with the CPI. Although the burger occasionally rose faster or slower, over that 17 year period both indexes increased by about 68% (or about 4% per year). But from April 2003 to January 2013 the CPI Index is up just 25% percent (from 183.8 to 230.28 or about 2.5% per year) while the BMI is up 61% (from $2.71 to $4.37 or about 6.1% per year), or more than twice the official inflation rate.

What could possibly account for the difference? Has the Big Mac gotten bigger, better, tastier, or healthier? As an iconic product, McDonald’s has been reluctant to change a proven formula. If the Big Mac hasn’t changed, is it possible that our inflation yardstick has?

It has been estimated that if the government used the same methodology to measure inflation that it used during the 1980’s, we would be currently dealing with official inflation that would be many times higher than today’s official 1.5% rate. The Big Mac appears to confirm this.

But now the government appears ready to distort the figures even further. With little resistance from the media or the public, the Obama Administration and Congressional Republicans seem ready to switch the inflation measurements used for Social Security away from the CPI in favor of the even more attenuated “Chain Weighted CPI.” This index, which is consistently lower than the CPI, looks to incorporate changes in spending patterns when consumers switch to more affordable products (in other words, it measures the cost of survival, not the cost of living). And while many admit that this is a manipulation, no one really seems to care.

Similarly clumsy tricks have been used to make our unemployment problem appear less severe. Over the years new methods have been introduced to factor out those who have “dropped out” of the labor force or to count part-time or temporary workers as employed.

All this takes us right back to Don Draper. If you can’t change the conversation, change the words. If that doesn’t work, just change the dictionaries.

To order your copy of Peter Schiff’s latest book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

“Markets can stay irrational longer than you can remain solvent.” – John Maynard Keynes

In any contest there can only be one victor. For investors – that contest is between the markets and the economy. Only one can be ultimately be right. Historically, the stock market has led the economy by reflecting investors’ expectations of a deteriorating or expanding economy. We no longer live in normal historical times.

There is little doubt that the ongoing interventions of the Federal Reserve is having an artificial effect on asset prices. Since the end of the financial crisis there has been a 85% correlation between the rise of the Fed’s balance sheet and the rise of asset prices. However, the economy has only grown by roughly 1.5% during that same period of time and employment growth has failed to keep pace with population growth.

The ongoing disconnect between the market and the real economy has become glaringly obvious in recent months. This week will take a look at the latest GDP report – was the bump to 2.5% due to the temporary effects of Hurricane Sandy or were there signs of organic growth. The outcome of this analysis will be very important to the future of the stock market participants.

Despite the Central Bank interventions, which are distorting asset prices, eventually economic reality will collide with market fantasy. It is then that the greatest damage is incurred by investors who have been lured into complacency.

The Great Debate: Economy Or Markets

In any contest there can only be one victor. For investors – that contest is between the markets and the economy. Only one can be ultimately be right. Historically, the stock market has led the economy by reflecting investors’ expectations of a deteriorating or expanding economy. We no longer live in normal historical times.

There is little doubt that the ongoing interventions of the Federal Reserve is having an artificial effect on asset prices. Since the end of the financial crisis there has been a 85% correlation between the rise of the Fed’s balance sheet and the rise of asset prices. However, the economy has only grown by roughly 1.5% during that same period of time and employment growth has failed to keep pace with population growth.

The ongoing disconnect between the market and the real economy has become glaringly obvious in recent months. This week will take a look at the latest GDP report – was the bump to 2.5% due to the temporary effects of Hurricane Sandy or were there signs of organic growth. The outcome of this analysis will be very important to the future of the stock market participants.

Despite the Central Bank interventions, which are distorting asset prices, eventually economic reality will collide with market fantasy. It is then that the greatest damage is incurred by investors who have been lured into complacency.

NOTE: Next week I will be in California for the annual investor conference. Please join me on our daily blog on Thursday and Friday of next week for transcripts of my favorite speakers on the markets and the economy

There will be no newsletter next weekend due to travel. But I willv update analysis on our blog if anything important occurs.

GDP – A Disappointing Miss

For the last several months I have been consistently writing that the economy was much weaker than headlines, particularly the media, suggested. This really begin to show up in the 4th quarter of 2012 has the economy churned out a growth rate, if you can call it that, of just 0.1%.

We stated several times during that period that Hurricane Sandy would give a slight bump to GDP due to inventory draw downs and rebuilding, post- hurricane construction and development, and automobile replacement. It is the old theory of the “broken window” which states that if a window is broken it creates economic activity because the window has to be replaced.

The problem with that theory is that you are replacing things that had already been built or bought. Therefore, the dollars spent replacing items are detached from future purchases to boost further economic growth. This “drag forward” of activity ultimately leaves a “hole” in the future.

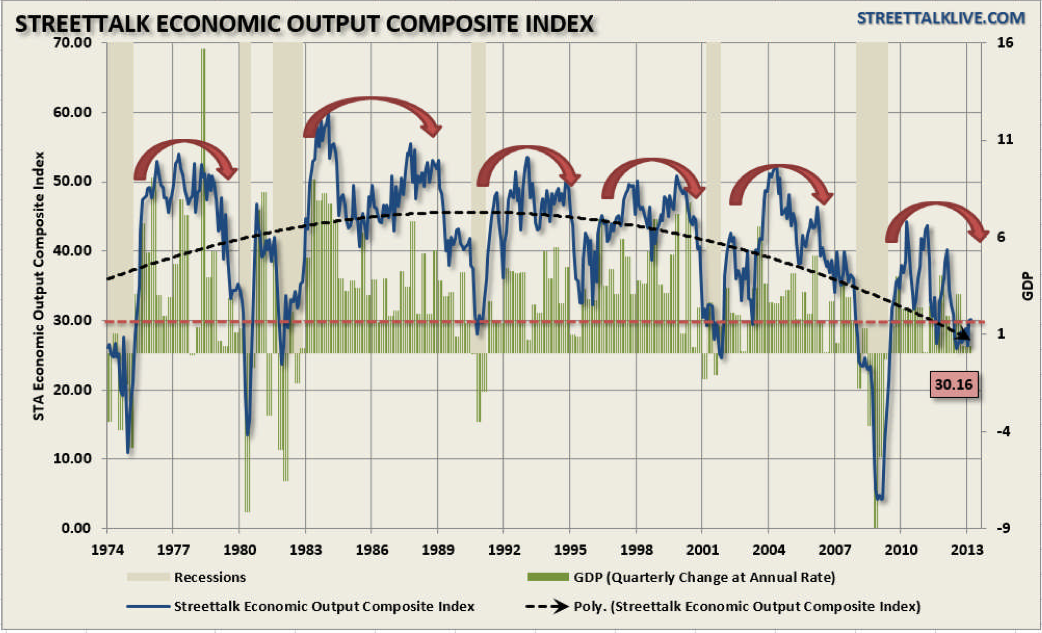

The chart below shows our economic composite indicator which we discussed in detail recently stating:

“The EOCI is a composite index consisting of the CFNAI, the Chicago PMI, the ISM Composite Index (an average of the Manufacturing and Non- Manufacturing Surveys), several Federal Reserve manufacturing surveys, the NFIB Small Business Survey and the Leading Economic Indicators. This index is meant to cover a broad measure of economic inputs to provide a clearer understanding of what is occurring in the overall economy.”

For March the index ticked up to 30.16 from 29.96 in February. The bounce in the data can be primarily attributed to a surge in economic activity in the later part of 2012 and early 2013 due to Hurricane Sandy. However, recent data readings suggest that much of that activity has occurred and weakness in the underlying data is likely to return over the next few months at least. Importantly, readings below 30 have historically been associated with the onset of recessions.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair