In any contest there can only be one victor. For investors – that contest is between the markets and the economy. Only one can be ultimately be right. Historically, the stock market has led the economy by reflecting investors’ expectations of a deteriorating or expanding economy. We no longer live in normal historical times.

There is little doubt that the ongoing interventions of the Federal Reserve is having an artificial effect on asset prices. Since the end of the financial crisis there has been a 85% correlation between the rise of the Fed’s balance sheet and the rise of asset prices. However, the economy has only grown by roughly 1.5% during that same period of time and employment growth has failed to keep pace with population growth.

The ongoing disconnect between the market and the real economy has become glaringly obvious in recent months. This week will take a look at the latest GDP report – was the bump to 2.5% due to the temporary effects of Hurricane Sandy or were there signs of organic growth. The outcome of this analysis will be very important to the future of the stock market participants.

Despite the Central Bank interventions, which are distorting asset prices, eventually economic reality will collide with market fantasy. It is then that the greatest damage is incurred by investors who have been lured into complacency.

The Great Debate: Economy Or Markets

In any contest there can only be one victor. For investors – that contest is between the markets and the economy. Only one can be ultimately be right. Historically, the stock market has led the economy by reflecting investors’ expectations of a deteriorating or expanding economy. We no longer live in normal historical times.

There is little doubt that the ongoing interventions of the Federal Reserve is having an artificial effect on asset prices. Since the end of the financial crisis there has been a 85% correlation between the rise of the Fed’s balance sheet and the rise of asset prices. However, the economy has only grown by roughly 1.5% during that same period of time and employment growth has failed to keep pace with population growth.

The ongoing disconnect between the market and the real economy has become glaringly obvious in recent months. This week will take a look at the latest GDP report – was the bump to 2.5% due to the temporary effects of Hurricane Sandy or were there signs of organic growth. The outcome of this analysis will be very important to the future of the stock market participants.

Despite the Central Bank interventions, which are distorting asset prices, eventually economic reality will collide with market fantasy. It is then that the greatest damage is incurred by investors who have been lured into complacency.

NOTE: Next week I will be in California for the annual investor conference. Please join me on our daily blog on Thursday and Friday of next week for transcripts of my favorite speakers on the markets and the economy

There will be no newsletter next weekend due to travel. But I willv update analysis on our blog if anything important occurs.

GDP – A Disappointing Miss

For the last several months I have been consistently writing that the economy was much weaker than headlines, particularly the media, suggested. This really begin to show up in the 4th quarter of 2012 has the economy churned out a growth rate, if you can call it that, of just 0.1%.

We stated several times during that period that Hurricane Sandy would give a slight bump to GDP due to inventory draw downs and rebuilding, post- hurricane construction and development, and automobile replacement. It is the old theory of the “broken window” which states that if a window is broken it creates economic activity because the window has to be replaced.

The problem with that theory is that you are replacing things that had already been built or bought. Therefore, the dollars spent replacing items are detached from future purchases to boost further economic growth. This “drag forward” of activity ultimately leaves a “hole” in the future.

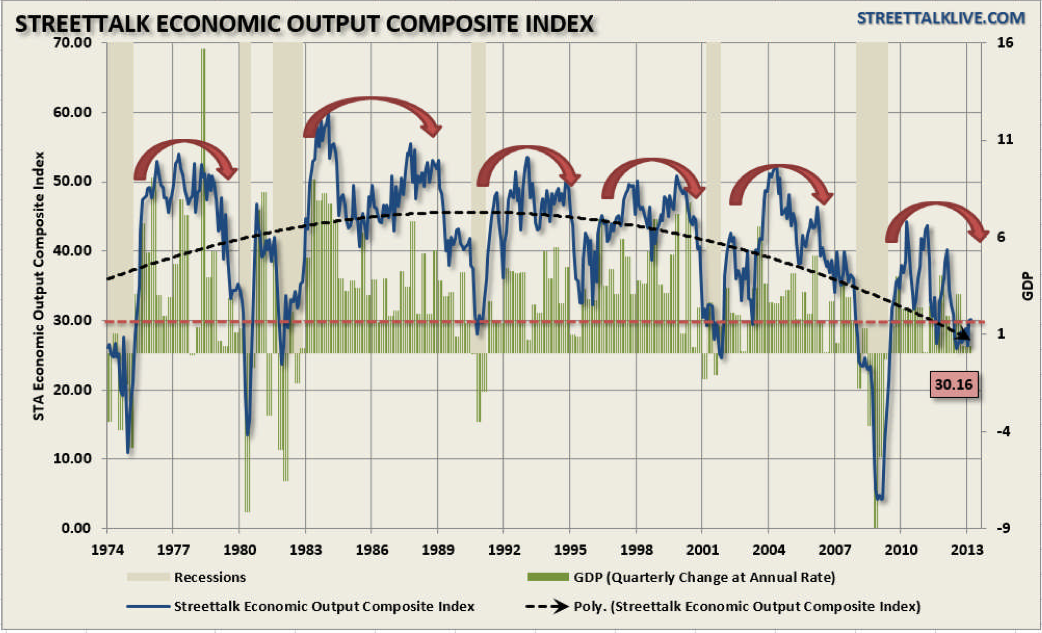

The chart below shows our economic composite indicator which we discussed in detail recently stating:

“The EOCI is a composite index consisting of the CFNAI, the Chicago PMI, the ISM Composite Index (an average of the Manufacturing and Non- Manufacturing Surveys), several Federal Reserve manufacturing surveys, the NFIB Small Business Survey and the Leading Economic Indicators. This index is meant to cover a broad measure of economic inputs to provide a clearer understanding of what is occurring in the overall economy.”

For March the index ticked up to 30.16 from 29.96 in February. The bounce in the data can be primarily attributed to a surge in economic activity in the later part of 2012 and early 2013 due to Hurricane Sandy. However, recent data readings suggest that much of that activity has occurred and weakness in the underlying data is likely to return over the next few months at least. Importantly, readings below 30 have historically been associated with the onset of recessions.