Stocks & Equities

STOCK MARKET SUMMARY upated after today’s close + a Gold Comment immediately below saying…. “one of the best gold market timers around, is Mark Leibovit”

Mark Says “Time is running out for the current (stock rally), but the intermediate trend for 2012 is still bullish”

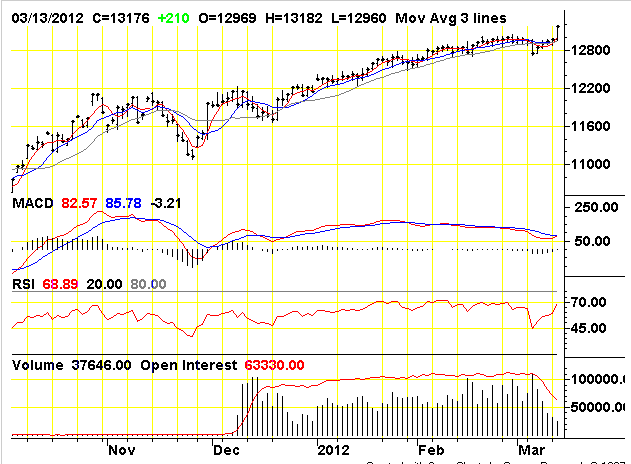

Equities exploded higher yet again today as the news seems to be all good. For the session the Dow was up 217.97 at 13,177.68, the S&P 500 was up 24.86 at 1395.95, and the Nasdaq Composite was up 56.22 at 3039.88. Volume increased over Monday and breadth was strong.

Well folks, in a normal market this would smell like a top. Markets explode higher yet again after a prolonged run – and all the news is GREAT! Retail sales strong, key banks pass stress tests (did anyone expect otherwise?), unemployment is down, 200,000 new jobs were created last nonth, Europe’s problems are on their way to being solved, etc. It seems the ‘wall of worry’ that the market has been climbing is being dismantled brick by brick.

While this latest rally looks suspect from a contrarian standpoint, we must wait for price and volume to confirm any reversals that may develop. Until then, the trend is higher.

Equities opened strong and finished stronger as news of the bank stress tests were released two days early after the Fed announced no change in interest rates with inflation not being a major threat.

Financials exploded higher as the release of the bank stress tests removed an element of uncertainty and forced shorts to cover positions. Also news that JP Morgan Chase is increasing their dividend and initiating a $15 billion stock buyback program brought in a rush of buyers late in the session. JPM closed 7.03% higher at 43.39.

Better than expected retail sales got stocks off to a solid start this morning. February retail sales rose by 1.1% vs. consensus of 1.0%. Excluding autos, retail sales were up 0.9% vs. consensus of 0.6%.

The FOMC opted to leave its fed funds target rate at 0.00% to 0.25%. The statement said that economic conditions, including low rates of resource utilization and a subdued outlook for inflation, are likely to warrant exceptionally low levels for the fed funds rate at least through late 2014.

In individual stock news, Molycorp shares gained 3.2 percent to $30.82.

Shares of Urban Outfitters Inc fell 5.3 percent to $27.95 after the company said it expects margins to continue to be pressured.

———————————————

Canadian News

Canadian equities moved higher after an upbeat FOMC statement and strong U.S. retail sales.

The S&P/TSX composite index gained 109.68 points to 12,537.69 as nine of its 10 main sectors posted gains. Materials stocks sank 0.4 percent on weak gold bullion prices.

Broad market gains were led by energy company Suncor Energy which gained 2.6 percent to C$34.04, and financial company Royal Bank of Canada which gained 2.2 percent to C$58.00.

The Fed didn’t signal any change in its plan to keep interest rates low which stoked optimism about the economy. That in turn put upward pressure on oil and copper prices, which impacted energy and base-metal mining shares.

Mining stocks were strong, led by gains in Teck Resources as its shares gained nearly 3 percent to C$36.53 while First Quantum advanced 3.3 percent to C$21.13.

The dollar was stronger despite all of the hoopla in the equity market. The U.S. Dollar Index was up .243 at 80.133.

Precious metals were lower today as gold sank on liquidation as the risk trade is firmly on at this point. Spot gold was off 27.50 at 1673.30. Silver was off .18 at 33.43, platinum was off 10 at 1684, and palladium was up 1 at 701.

Copper posted strong gains on the great news throughout the session as the May contract settled .0650 higher at 3.9025.

Crude oil settled 0.37 higher at 106.71.

Good Night.

Gold Comment from Dan Dorfman of Trim Tabs Lauding Mark Leibovit’s Timing Excellence (and current caution)

TrimTabs Money Blog

Gold Bulls Fear More Grief, Maybe a $200 Dive

By Dan Dorfman

Don’t get suckered! There are times when gold can turn into fool’s gold. This could be one of those times. In other words, gold stands out as an exciting investment for the long run, but looms as a potential dog of an investment for the short run.

Those essentially are the cautionary suggestions from a couple of outspoken and generally buoyant long-time gold bulls. More specifically, they’re saying if you’re tempted to take a flier on the precious metal in the hopes of buying it on the cheap after its wicked $130-an-ounce decline over five days that sent it skidding to around $1,660, your timing could be for the birds.

Their basic view is that the recent thunderstorms in the gold market-largely a reflection of a hint from Federal Reserve chairman Ben Bernanke that further quantitative easing might not be in the cards, Greek debt fears and a firming of the greenback-may be far from over. The inference is clear, namely gold could head down again before it heads up.

Our other wary long-term gold bull, one of the best gold market timers around, is Mark Leibovit, editor of the Arizona-based Leibovit VR Gold Letter. His view: gold shares are weakening and we need a confirmation of a bottom before jumping back in. “I would step aside till the dust settles,” he says. Another current negative, he notes, is the seasonal factor, a reference to the fact that gold often tops out in February or March, remains stagnant for about 90 to 120 days and then resumes its advance in the late summer.

For the longer term, though, Leibovit, who sees a full-scale confrontation between Israel and Iran before the end of May, says gold remains on a buy signal, but he emphasizes he would only buy the volatile metal here on weakness and cautions “it’s definitely not for the faint of heart.”

Before year end, though, he sees a gold reversal, with the metal, reflecting all the well known positive fundamentals, in particular global round-the-clock money printing, climbing to $2,000 or more. Among his favorite gold plays are Canadian Mapleleaf coins, Central Fund of Canada and a Canadian exchange-traded fund backed by the Royal Canadian Mint, an ETF that trades on the Toronto Stock Exchange under the symbol MNT and enables its investors to take delivery of their physical assets.

Marks Stock Comment before today’s opening

STOCKS – ACTION ALERT – SELL (Time is running out for the current rally, but the intermediate trend for 2012 is still bullish)

Today is both ‘Turnaround Tuesday’ and FOMC day likely triggering a rally following a down day on Monday. I have unfulfilled upside targets in the S&P 500 between 1395 and 1445, but felt a shakeout back to first 1323 and possibly 1270 were doable this Spring. We may still rally into the end of the month or early April and I could be early in my SELL signal. One of the key indexes to watch is the Russell 2000 which displayed several short-term sell signals in my work in February ahead of the early March sell-off. It is now rebounding and a breakout above 833.02 (the February 6 high) especially on volume would likely be coincident with new rally highs elsewhere. We are also watching the key Dow Transports which also topped out in early February at 5384.15, now 5144.28. New market highs, however, does not negate the chances of still seeing a sharp correction in the Spring, but this time coming from higher ground rather than current levels.

The Dow Daily below:

The Dow Daily below:

Tse Daily Chart 3/13/12

VRTRADER.COM Trial Signup:

THE RENEWAL OF YOUR SUBSCRIPTION IS AUTOMATIC. YOUR CREDIT CARD WILL CONTINUE TO BE BILLED UNLESS YOU NOTIFY VRtrader.com SEVEN DAYS PRIOR TO SUBSCRIPTION EXPIRATION EITHER VIA EMAIL POSTING THE WORD ‘UNSUBSCRIBE’ IN THE SUBJECT BOX OR TELEPHONE US AT (928) 282-1275 OF CANCELLATION. NO REFUNDS ARE AVAILABLE ON SILVER, PLATINUM OR VR FORECASTER (ANNUAL FORECAST MODEL) SUBSCRIPTIONS.

Welcome and congratulations on choosing VRTrader.com as a source for your stock market commentary, information and analysis for the U.S. Stock Market. Needless to say we are very happy that you are joining us for AT LEAST the next 30 days days and look forward to providing you rewarding and inciteful information that will help you toward your goal of succeeding in the markets.

Here is the Special Trial Offer: Use this month to kick our tires. Pay 50% for the first 30 days (No refund) and sample our Silver or Platinum service and then decide what works best for you. If you aren’t 100% ready to move forward, simply email us to cancel one week before your 30 day 50% off trial subscription ends and it will be canceled and you will not be charged ANY FURTHER, no questions asked. Just send an email to mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com or call 928-282-1275 to cancel. You will receive an emailed confirmation of your cancellation at that time.

The 30 day trial is allowed one time only. By taking this 30 day 50% trial, you agree to be charged the full cost of the monthly Silver or Platinum service (choose one only) at the end of the 30 day trial subscription period, unless you cancel first. The regular Silver monthly rate is $49.40 and the Silver quarterly rate is $133.50. The regular Platinum monthly rate is $129.95 and the Platinum quarterly rate is $350.85. The special trial 50% off trial rates are listed below. Sign up today!

There are no refunds or pro-rata refunds offered at VRTrader.com for any subscription. You are being offered a 50% discount for trying our service for the first 30 days only!

Over the years, we have discussed the various ways that companies utilize their free cash flow to generate a return for their shareholders. In our small-cap universe, we have traditionally focused on companies that reinvest their earnings back into the business to generate sustainable growth. More recently the markets have started focusing on companies that payout their cash flow to shareholders in the form of dividends or distributions. Even better are those companies that generate so much cash that they can afford to invest in growth as well as pay a dividend. But there is also a third method of allocating capital that is often misused and even more often misunderstood – share repurchases (buybacks).

The consensus is mixed on whether or not share repurchases are in fact a viable strategy for generating shareholder returns. When a company has excess cash and they believe their shares are undervalued, they will often issue a normal course issuer bid which allows them to purchase and cancel a predetermined maximum number of shares of their own company. The idea is that if you believe that your own company will provide you with the best risk-adjusted return on your capital then why would you invest your capital anywhere else.

Warren Buffet recently said in his 2012 letter to shareholders (http://www.berkshirehathaway.com/letters/2011ltr.pdf) that in addition to generating strong earnings growth he also typically hopes that the stock prices of the companies he purchases languish in the markets for several years after he buys them. Using an example of IBM, he explained that if the company were to spend $50 billion over a 5 year period to repurchase its shares that his current interest of 5.5% in the company would growth to 7% if the share price were to average $200 over the period, but only 6.5% if the share price where to average $300. Since Warren has no intention of selling his shares during that period his best case scenario would be if the cash flow remained strong but the stock price plummeted. This is a wide diversion from the mentality of many retail investors who require constant validation from the market in the form of appreciating stock prices.

The reason that share repurchases are often criticized is because they are very commonly misused. Very often companies will publicly disclose that they have received exchange approval to proceed with a share buyback but then fail to repurchase any shares. The hope is that the announcement alone will garner investor interest. The more common problem is when share repurchases are made by companies that are not undervalued. Warren Buffet said, “I favor repurchases when two conditions are met: first, a company has ample funds to take care of the operational and liquidity needs of its business; second, its stock is selling at a material discount to the company’s intrinsic business value, conservatively calculated. We have witnessed many bouts of repurchasing that failed our second test.” The CEO and Board of Directors commonly have a tendency to view their own company as undervalued, particularly if it has suffered a large decline in the share price. This bias can lead firms to repurchase stock when it is in fact overvalued, an activity which has the impact of destroying shareholder value.

The key to assessing a share repurchase strategy is to analyze the metrics of the individual situation. Does this company have the available liquidity to repurchase shares? Is the company clearly undervalued on the basis of free cash flow and will a share repurchase have the intended impact of improving performance on a per share basis? If the answer to these questions is yes then a share repurchase may be a very viable strategy for creating shareholder value long term.

What Now

The gold doomsayers have found their champion in the media’s favorite financial advisor and one of the world’s richest men. Warren Buffett, the man dubbed the “Oracle of Omaha,” has repeatedly and publicly denied that gold is an investment, and called gold buyers “speculators” and people “who fear almost all other assets.” In fact, Buffett claims that gold’s rise has the same characteristics as the housing and dot-com bubbles, and it is only a matter of time before it reverses course. He doesn’t mean that the price will decline because of austerity measures and a free-market interest rate, mind you. He just asserts that because he’s deemed it a bubble, it will inevitably burst.

The financial world by-and-large views Buffett as an objective observer, a rare investor who still considers the best interests of common man when he speaks. Each year, there is much hullabaloo over the letter Buffett writes to the shareholders of Berkshire Hathaway. When Buffett makes a claim, the financial world coos and repeats it without question.

I concede that Buffett is a talented investor and a great communicator. He clearly has had great success and has much to offer. But that shouldn’t blind anyone to the fact that Buffett is not a trusted observer. He’s a crony capitalist who bends the truth to serve his long-held ideological commitment to big government.

In the early stages of the financial crisis, when I was writing and promoting my first book Crash Proof to warn private investors about trouble ahead, Buffett was accumulating shares in companies such as Goldman Sachs, Wells Fargo, Bank of America, and General Electric. I knew these companies were insolvent, so I wouldn’t touch them with gardening gloves on. When the credit markets seized up, Buffett worked behind the scenes and in public to make sure each of his pet companies were bailed out. This was not by coincidence. Buffett actually stated in September 2008 that he would not have invested in Goldman Sachs if not for the implicit guarantee of federal assistance. As a result, he profited at the expense of taxpayers at the very time when they were losing their savings in the markets. Meanwhile, many “in the know” politicians bought Berkshire stock during the height of the crisis, making a profit from their votes, and giving them incentive to revere Buffett all the more. Buffett once said that if the government didn’t bailout failed companies, he would be “having my Thanksgiving dinner at McDonald’s instead of having a big dinner at my daughter’s.” Seems like there were two bloated turkeys at that meal.

If Buffett were a true capitalist, he would be in favor of gold. He has noted that the value of the dollar has fallen 86% since he took over Berkshire Hathaway in 1965 and even said in his latest shareholder letter that investors are “right to be fearful of paper money.” But he continues to harp on gold. It seems the only unit of account Mr. Buffett approves are shares of his own company!

The adoption of an independent measure of value like gold presents two problems to Buffett. First, it would reduce the nominal returns of his dollar-based investing strategy. Second, it would restrict Washington’s ability to goose the financial system in his favor.

In the 19th century, when gold and silver were legal tender, the outsized returns to which Buffett has become accustomed were much harder to earn. Most people kept their money in physical bullion or bank deposits – and earned a real rate of return. Now, under the fiat system, working folks are forced into the more complicated world of equity investing. This, too, can generate real returns, but it’s a tougher playing field for the inexperienced.

Also, the fiat system artificially balloons the financial services portion of the economy. In the 19th century, fortunes were made more often by business owners than simple equity investors. People were more likely to be rewarded for providing a productive service than having direct access to the Fed’s discount window.

A quick look at Berkshire’s performance verses gold since the Credit Crunch goes a long way to explaining Buffett’s antipathy toward the yellow metal:

But Mr. Buffett’s lack of credibility goes deeper than a differing monetary philosophy. He has been in the press since last August claiming that he pays less taxes than his secretary – and urging Congress to pass a “Buffett Rule” mandating a 30% minimum tax on millionaires. The natural reaction is to say, “If you want to pay more, go ahead.” But Buffett has gone on record saying that it’s not enough for him to lead by example, and demanding that all of America’s well-off bear the burden of Washington’s reckless spending binge.

The problem is that Buffett’s entire argument is constructed on deception. Buffett is rated as the third richest man in the world for managing the nearly $393 billion in assets, and he highlights that he only pays 17.4% of his income in taxes. But this is because he earns less than 1% of his annual wealth from his salary, while over 99% is earned as the largest shareholder of Berkshire Hathaway. Buffett claims that he discounts his Berkshire holdings because he plans to give it all to charity when he dies. So, it’s not that the tax rates are so low, it’s that Buffett plans to give away 99% of his wealth.

But even accounting for this clever accounting trick, Buffett is still grossly understating his personal tax burden. He owns roughly 1/3 of Berkshire’s outstanding shares, the profits from which are subject to a 29% corporate tax rate. Last year, Berkshire paid $5.6 billion in taxes – and the IRS says they owe $1 billion more! In addition to corporate taxes, Buffett is also subject to an additional 15% capital gains tax on his stock when he cashes out, not to mention any future estate tax, leaving many to conclude that his share of taxes is certainly higher than his secretary’s.

You might wonder what Buffett would hope to gain by understating his own tax rate. To answer that, you have to understand Buffett’s ideological background. His father, Howard Buffett, was a US Congressman known for his staunch libertarianism. As has been recounted by biographers, Buffett resented being uprooted from his Omaha, NE home to move to Washington, DC and felt estranged from his stoic father. That is to say, Buffett’s commitment to the nanny state runs very deep.

But also, as mentioned earlier, Buffett personally benefits from the current corrupt state of affairs. He gets prestige from nominal gains in his stock price. He gets bailout money to guarantee the insolvent companies in which he invests. Even that estate tax that will hit him when he passes currently allows him to buy out other businesses at a steep discount.

It also shouldn’t be a surprise that humble Howard was a staunch advocate of gold and silver as money – nor that wealthy Warren rejects precious metals as having “no utility.”

The media has built Warren up to be a demigod, a straight-talking Nebraska boy that can hold his own against the vipers of Wall Street. But he is just a man with a talent for making money, and his motives should not be beyond reproach. Is he advocating the use of taxpayers’ money to bailout his business interests so he can profit? Is he being honest about what money is? Does he even understand the business cycle?

Gold prices will only go down when governments change course and make significant cuts. Until then, gold is not in a bubble. It’s the only way to protect your wealth; and in the current economic condition, it’s poised to go much higher. I think it’s high time Buffett takes to heart his father’s wise words: “For if human liberty is to survive in America, we must win the battle to restore honest money.”

Peter Schiff

C.E.O. of Euro Pacific Precious Metals

email: info@europacmetals.com

website: www.europacmetals.com

Peter Schiff is CEO of Euro Pacific Precious Metals, a gold and silver dealer selling reputable, well-known bullion coins and bars at competitive prices. To learn more, please visit www.europacmetals.com or call (888) GOLD-160.

For the latest gold market news and analysis, sign up for Peter Schiff’s Gold Report, a monthly newsletter featuring original contributions from Peter Schiff, Casey Research, and other leading experts in the gold market. Click here to learn more.

“The Bank of Japan and The Bank of England are also flooding their markets with newly printed cash. And this week, in comments before Congress, Federal Reserve Chairman Ben Bernanke also signaled he has no intention of stemming the flood of easy money coming from his central bank.” – Money and Markets

US Stock Market Update

by Peter Grandich

Despite numerous bearish long-term fundamentals, I’ve stated the market’s least resistance is up. While not a card-carrying member of the “Don’t Worry, Be Happy” crowd, I’ve managed to avoid taking any bearish strategies and thus not becoming part of the perma-bear carnage that has grown since the bottom in March 2009.

Having said that, I do think it’s time to start preparing for the top in this massive countertrend rally in a secular bear market that began back in late 2007. Somewhere between here and the marginal new, all-time high I suggested the DJIA could reach, I feel selling non-metals related shares seems wise. I would like to be mostly in cash (except for mining shares) before years-end.

I know the question many now have – what about resource stocks? Selling in May and going away may just be wise this year but for now, all systems remain go.

I do believe on the first news of a large-scale military conflict with Israel and Iran, we shall likely expedite any selling still left to do.

Stay tuned!

ABOUT PETER GRANDICH

Though he never finished high school, Peter Grandich entered Wall Street in the mid-1980s with no formal education or training and within three years was appointed Vice President of Investment Strategy for a leading New York Stock Exchange member firm. He would go on to hold positions as a Market Strategist, portfolio manager for four hedgefunds and a mutual fund that bared his name.

His abilities has resulted in hundreds of media interviews including GMA, Neil Cavuto’s Your World on Fox News, The Kudlow Report on CNBC, Wall Street Journal, Barron’s, Financial Post, Globe and Mail, US News & World Report, New York Times, Business Week, MarketWatch, Business News Network and dozens more. He’s spoken at investment conferences around the globe, edited numerous investment newsletters, and is one of the more sought after commentators.

Grandich is the founder of Grandich.com and Grandich Publications, LLC, and is editor of The Grandich Letter which was first published in 1984. On his internationally-followed blog, he comments daily about the world’s economies and financial markets and posts his views on social and political topics. He also blogs about a variety of timely subjects of general interest and interweaves his unique brand of humor and every-man “Grandichism” expressions with his experience gained from more than 25 years in and around Wall Street. The result is an insightful and intuitive look at business, finances and the world, set in a vernacular that just about anyone can understand. In his first year, Grandich’s wildly-popular blog had more than one million views. Grandich also provides a variety of services to publicly-held corporations on a compensation basis.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair