Stocks & Equities

What a difference a few weeks can make.

All eyes were anxiously watching the Federal Reserve in mid-September. The key question on every investor’s mind: Would they or wouldn’t they? (Taper quantitative easing, that is.)

The S&P 500 Index had recorded its largest monthly drop in 15 months in August. But the Fed surprised investors by keeping the current pace of $85 billion in monthly bond purchases.

Today the benchmark index is at a record, having jumped 24 percent this year, the best performance since 2003. Yes, investor sentiment has shifted dramatically.

[Editor’s note: For more detail on where Mike sees potential outperformance, Click HERE for an audio extra.]

Not only is tapering no longer the worry of the day, but apparently it’s not even on the horizon. Most commentary and analysis I’m reading has pushed the start of reducing the stimulus program well into 2014.

The government shutdown and prospect for continuing budget battles early next year has a lot to do with the shift in consensus. And the jobless rate, a key indicator for the Fed, is still too high. (The government finally got around to releasing it – 7.2 percent in September compared with 7.3 percent in August.)

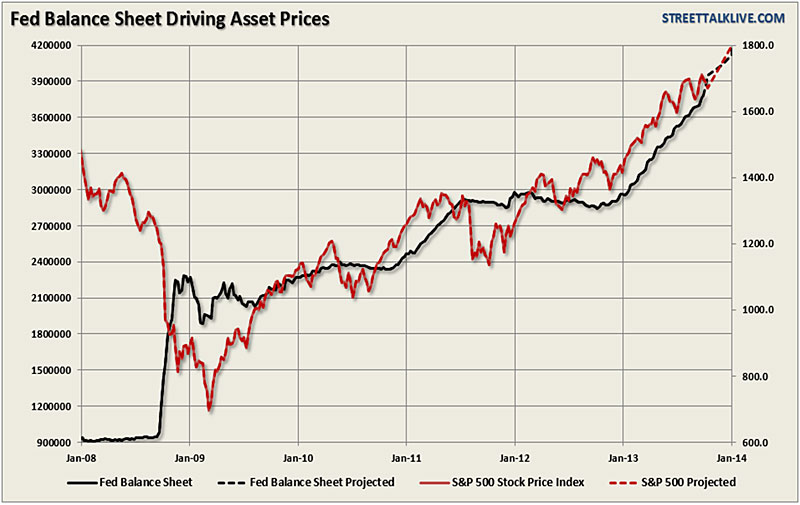

(Click image or HERE for larger view)

As the graph above shows, there’s a strong tie between the size of the Fed’s balance sheet and the stock market’s rise. Ever since the Fed’s first round of QE in 2009, and with each successive expansion, the S&P 500 has responded almost in lock-step.

Shift in Stock-Market Leadership

The no-taper relief rally has been accompanied by a shift in stock-market leadership, which I pointed out several weeks ago. Specifically, the risk-on trade is back, featuring outperformance by economically sensitive assets that are considered riskier, including:

1. Cyclical stocks and sectors, such as basic materials, technology and industrials.

The good news: You don’t have to invest in foreign stocks or international ETFs to tap into this potential. Instead, you can “go global” by investing locally by focusing on sectors or stocks that earn a substantial share of sales from abroad.

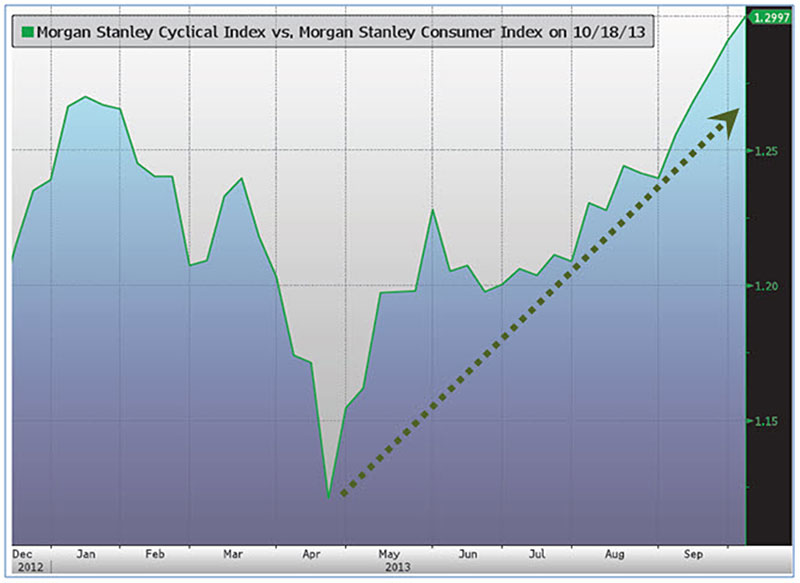

Here’s why cyclical sectors should keep outperforming. In the chart above, the dotted line plots the Morgan Stanley Cyclical Index relative to the Morgan Stanley Consumer Index.

When the line is rising from the lower left to the upper right, it means cyclical stocks (materials, energy, technology, industrials, consumer discretionary and financials) have the upper hand over defensive stocks (consumer staples, health care, telecommunications and utilities).

The reason: A downshift in global growth is stabilizing, and there are signs of improvement overseas. Over the past three months, global manufacturing expanded in 27 of the 33 largest economies. That’s a bullish sign for cyclical stocks.

The table above lists the performance by sector since the end of June. It’s no surprise that nearly all of the top-performing stocks and industries also have the highest percentage of foreign sales — they stand to benefit most as global growth re-accelerates.

– Technology, for instance, generates 40 percent of sales from overseas markets. It’s the second-best-performing sector since June, up 14 percent.

– Energy and industrials earn 20 percent and 21 percent of sales abroad. They’re beating the benchmark Russell 2000 Index too.

– Materials is trailing, yet with 30 percent of sales from overseas, the sector has been playing catch-up, with a gain of 14.7 percent since July 1.

In the third quarter, materials and technology companies have reported the biggest upside earnings surprises compared with estimates (26.8 percent and 12.3 percent, respectively), according to FactSet Research.

I’ll be keeping an eye on these trends as earnings season progresses, and you should too. The shift in market leadership toward cyclical stocks, if it’s sustainable, may have a long way to go. And there are plenty of attractive technology, energy and materials stocks to choose from today.

Make sure to go to our Money and Markets’ Facebook page for a review of two undervalued cyclical stocks I’m looking at.

Good investing,

Mike Burnick

Good morning! Here’s what you need to know.

Good morning! Here’s what you need to know.

- Markets were mostly higher. Korea’s Kospi led in Asia at 0.54%. In Europe, Germany’s DAX was up 0.45%. U.S. futures were up about 0.30%.

- China’s purchasing managers index for Octobe rprinted a seven-month high 0f 50.9, beating expectations of 50.4. “This implies that China’s growth recovery is becoming consolidated into 4Q following the bottoming out in 3Q. This momentum is likely to continue in the coming months, creating favorable conditions for speeding up structural reforms,” HSBC chief China economist Hongbin Qu said.

- Europe is still growing, but it’s slowed down a bit. The Eurozone’s composite PMI declined to 51.5 from 52.2. “Although modest, the expansion is reassuringly broad-based across the region, reflecting signs of economic recoveries becoming more entrenched in the periphery as well as ongoing expansion in Germany and stabilisation in France,” Markit’s Chris Williamson said.

- India is now expected to see its GDP decline to the lowest level in more than a decade. Reuters polled 24 economists, who now see growth slowing to 4.7% — the same figure the World Bank recently came up with. “India’s ailing economy is likely to remain under pressure from weak domestic and foreign demand for some time, while uncertainty ahead of elections next year is expected to keep investors and businesses at bay,” Reuters’ Rahul Karunakar and Ashrith Rao Doddi write

- Institutional investors accounted for 14% of all sales in September according to RealtyTrac, up from 9% of all sales last month. “The housing market continues to skew in favor of investors, particularly deep-pocketed institutional investors, and other buyers paying with cash,” Daren Blomquist, vice president at RealtyTrac said in a press release.

- This is the busiest earnings day of the year, with 358 different firms releasing their Q3 figures. Ford is already in: they beat earnings, missed sales estimates, and its shares are up 3.6% pre-market. Also before the bell we get, among others, 3M ($1.75/share expected), Altria ($0.64/share expected), Colgate ($0.73/share expected), Dunkin Donuts ($0.43/share expected), Southwest Airlines ($0.33/share expected), and Xerox ($0.25/share expected). Amazon ($-0.09/share expected) and Microsoft ($0.54/share expected) also report, after the bell.

- We also get a raft of new economic data this morning. At 8:30, weekly jobless claims print, with 335,000 expected versus 358,000 prior; and August international trade data, with a decline of -$900 million expected. Just before 9 am, October flash PMI prints, with a decline of 0.01 to 52.7 expected. Finally at 10 am, we get the Job Openings and Labor Turnover Survey (JOLTS).

- The Obama Administration appears ready to extend the open enrollment period to sign up for health insurance at least through March, Reuters’ David Morgan and Mark Felsenthal report. And pressure is now mounting from Democrats to make additional reforms to the Affordable Care Act’s centerpiece, the health insurance exchanges. “Representative James Clyburn of South Carolina, the third-ranking House Democrat, criticized the website for forcing consumers to provide private information before deciding what kind of health insurance plan they want to buy. ‘I’ve talked to too many people who tell me before they ever get around to figuring out what it is they want to buy, they’re having to answer questions that they don’t feel they should be answering,’ Clyburn said.

- The CEO of British-based WPP, the world’s largest ad firm by revenue, told the Wall Street Journal that allegations the U.S. was spying on its own allies would damage both “brand America” as well as the ad industry, since it could lead to commercial data collection becoming more restrictive. “If Germany’s Chancellor is bugged—true or not—the bare suggestion of this is bad,” Mr. Sorrell said. “Imagine [CEO of rival Publicis Groupe SA Maurice Levy ] calling me to assure me that he wasn’t tapping my phone, or the other way round…It’s pretty serious stuff.”

- Bitcoin prices briefly hit $230 overnight and remain above $200 this morning on the Mt. Gox exchange, recalling the insane surge that occurred this spring and reflecting the resiliency of the digital currency.

Few things are scarier for smart investors than buying when stock markets are at all-time record highs. With the S&P 500 (SNPINDEX: ^GSPC ) having soared to new records yesterday, sentiment among mainstream investors is unmistakably bullish. But subtler signs of nervousness have started to appear about the health of the economic recovery and the ability of the bull market to continue, raising fears that a stock market correction is imminent.

Ordinarily, investors can expect to see drops of 10% or more in the market roughly once a year, even in the context of an ongoing bull market. But the S&P 500 hasn’t suffered a 10% pullback since December 2011. With such a long period having gone by without a stock market correction, does it make sense to hold off on buying stocks in hopes of getting lower prices? Or should you go ahead and buy, risking getting mauled by a big bearish move?

Are you ready for what you’re wishing for?

Whenever there are extreme market movements in either direction, emotion starts to play a huge role in investing decisions. Extended and uninterrupted stock-market rallies, as we’ve seen throughout the past two years, leave those on the sidelines feeling increasingly worried that they’ve missed out on huge potential gains. This pushes them to invest even as higher share prices make stocks less attractive from a valuation standpoint. In that light, waiting for a correction might seem like the smarter move.

Yet, waiting creates two more challenges. First, you have to have the patience to stick with your decisions, and that can be difficult if the bull market rages higher. For instance, at the beginning of 2013, markets soared after lawmakers averted the threat of a huge tax increase on the entire American public. Those gains led some to decide to wait for a pullback before getting in. They’ve been waiting ever since, and the S&P 500 is now 20% higher.

Second, once the correction comes, you have to have the conviction to follow through with your original commitment to buy. That’s also a tough thing to do, because most stock market corrections hinge on some piece of exceptionally bad news that can make less secure investors question their entire investing plans.

Two smart moves to make now

What makes the most sense is never to stop investing entirely, even as markets keep rising, but also to keep your eyes open for better prospects if a stock market correction occurs. That way, you’ll benefit no matter which way the market moves.

When considering investments at near-record levels, it often pays to focus on areas of the market that most investors have neglected. Lately, consumer-staples stocks have gotten a huge amount of attention, with many investors turning to them for their reliable dividend income and defensive characteristics during pullbacks. Yet all the demand for dividend stocks has pushed their valuations up dramatically.

By contrast, commodity stocks, like gold miners and fertilizer producers, have gotten hammered. In the potash fertilizer space, PotashCorp (NYSE: POT ) and Mosaic (NYSE:MOS ) plunged during the summer when a key player in the global potash market backed out of a cartel agreement with its main partner, spurring speculation that potash prices would drop severely. It’s true that neither Mosaic nor PotashCorp owes its entire fortune to the potash industry, given that both also make other products that don’t rely on potash. Yet, short-term traders sold first and asked questions later, expecting the worst, and not wanting to get caught up in ongoing drama in the industry. For long-term investors who can afford to handle near-term uncertainty, the arguments favoring greater demand for crop-enhancing products like potash remain unchanged, and that should help Mosaic and PotashCorp recover eventually. That makes the two stocks worth looking at for their potential value opportunity.

At the same time, though, it also makes sense to look for stocks you’d want to buy if a stock market correction actually happens. Procter & Gamble (NYSE: PG ) has a lot of growth potential from global markets, but at 21 times trailing earnings, the shares reflect a premium for its 3% dividend yield and reputation as a defensive stock. Investors appreciate P&G’s brand success and its reliable demand from customers who see its products as essential staples. But paying too much for even the highest-quality consumer stock doesn’t make sense, especially when Procter & Gamble hasn’t yet delivered on its promise to expand its earnings power more rapidly. After a stock market correction, though, P&G shares could look a lot more attractive for the long run.

Be correct about a correction

Stock market corrections happen, and it pays to be ready for them. But you also have to be ready for them not to happen on any predictable time frame. Your best solution includes making the most of current opportunities while also setting the stage to jump on cheaper stocks when they emerge.

Start investing today!

Letting the lack of a stock market correction keep you from investing entirely would be a big mistake. Millions of Americans have done exactly that, waiting on the sidelines since the market meltdown five years ago and therefore missing the big bull market that followed. You can learn more about how to overcome your fears and invest by reading our brand-new special report, “Your Essential Guide to Start Investing Today.” Inside, The Motley Fool’s personal finance experts show you why investing is so important, and what you need to do to get started. Click here to get your copy today — it’s absolutely free.

Tune in to Fool.com for Dan’s regular columns on retirement, investing, and personal finance. You can follow him on Twitter @DanCaplinger.

About Dan Caplinger

The S&P 500 is falling in morning trading after hitting another all-time high yesterday.

The index is down 0.6%, trading at 1743. It’s closed up for five days in a row, and has risen in 9 of the last 10 trading sessions for a total gain of 5% from its government shutdown low.

The FHFA House Price Index was the only datapoint released in the U.S. this morning, and though price appreciation slowed more than expected, the release didn’t move the market.

A story about Chinese banks has been cited as a reason for worry among market participants this morning.

Brown Brothers Harriman global head of currency strategy Marc Chandler disagrees.

In a note on his blog, he writes:

After falling sharply in recent days, especially yesterday after the disappointing jobs data, the US dollar is broadly higher today, with the yen the main exception. It has strengthened by almost 1% today.

Many are attributing the price action to news that the five largest Chinese banks tripled the bad loans written off in the first half of the year to CNY22.1 bln (~$3.65 bln). Yet, tellingly and importantly, the Chinese banks had already made the provisions and thus did not, reportedly, impact the record profits (~$76 bln) in H1.

There is some speculation that this is a precursor to a wave of defaults, but in itself writing off the bad loans is a very important step in its own right. It is a step toward modernization and liberalization. Provisioning for bad loans and then drawing on those provisions is part and parcel of a modern banking system.

Precisely why one would sell, say the New Zealand dollar, the weakest major currency today, losing about 1.4% through the European morning, or the Mexican peso, which, with a 0.8% loss is the weakest among the emerging market currencies, in response to Chinese banks writing off bad loans in the first half of the year, is not immediately self-evident. Indeed, not writing off bad loans, we would argue, was part of the problem. Writing off bad loans is part of the solution. For the record, the yuan itself rose to a new 20-year high against the dollar.

The chart below shows the drop in S&P 500 futures as of 7:18 am PST:

Warren Buffett has a seemingly unassailable reputation as the world’s #1 investor.

Yet, even as Buffett has outperformed the S&P 500 over the past decade, the “Oracle of Omaha” has stressed that Berkshire Hathaway’s sheer size limits his ability to generate the eye-popping investment returns of his early days.

By managing a much smaller amount of money, Wall Street legend Carl Icahn doesn’t have that problem.

By managing a much smaller amount of money, Wall Street legend Carl Icahn doesn’t have that problem.

Thanks to big bets on Netflix and vitamin maker Herbalife, Forbes magazine listed Icahn as one of the 40 Highest-Earning hedge fund managers in February 2013.

A month later, Icahn crept into the top 20 of the Forbes 400 and today he is the wealthiest man on Wall Street with an estimated net worth of $20 billion.

That made Carl Icahn richer than hedge-fund icon George Soros.

So Who is Carl Icahn?

While Buffett plays up his “white hat” avuncular, “awe shucks” Midwestern image, Carl Icahn wears the “black hat” among U.S. investment titans.

The Queens, N.Y., native had an unlikely start, earning a degree in philosophy at Princeton University and attending medical school at New York University before dropping out after two years. Icahn began his career on Wall Street in 1961 when his uncle got him a job as an options broker. In 1968, he formed Icahn & Co., a securities firm that focused on risk arbitrage and options trading. Icahn began doing small-time buyouts of individual companies in 1978.

By the 1980s, Icahn had developed a reputation as a ruthless “corporate raider.” He made a fortune for himself by launching hostile bids for company’s ranging from TWA to Uniroyal, Texaco and RJR Nabisco.

The World’s Top Activist Investor

With their names splashed regularly across headlines, activist investors have always been among the highest-profile investors around. But no one has a higher profile than Carl Icahn, whose name has become synonymous with titanic corporate battles for as long as most Wall Street veterans can remember.

Specifically, Icahn takes minority stakes in public companies and typically pushes for new management or the restructuring of the companies. In just the last 24 months, Icahn has taken positions in and then launched campaigns against 15 companies.

Icahn has had a particularly busy 2013, losing a high-profile battle to Michael Dell in his bid to buy the PC-maker. On August 13, 2013, Icahn announced via Twitter a stake in Apple. Apple shares surged 9% in the week after his tweet. Just recently, Icahn took to Twitter again to announce his latest investment, a 61.6 million share stake in Talisman Energy. He also announced he would seek a seat on the board of the company. The stock, which had been having a lousy 2013, jumped immediately.

Icahn’s Investment Philosophy

Despite his reputation as a corporate raider, Icahn describes his investment philosophy as value-oriented, “Graham & Dodd investing with a kick.” But unlike Buffett, Icahn’s philosophy is to get in and get out for a quick buck through a big stock buyback, asset spinoffs, or ousting the CEO — to help pop the stock.

Icahn looks for companies where the value of their assets far exceeds the total value of their shares, or market cap. He focuses on “hard assets” like real estate, oil reserves and timberland that are relatively easy to value and resell. With the notable exception of Apple (AAPL), he avoids high-tech companies that have to reinvent themselves each year.

Icahn thinks of himself a contrarian to the bone. He loves to buy at the worst possible moment, when prospects are darkest and no one agrees with him. As Icahn put it, “When you conclude something is really cheap, you’ve got to be willing to load up.” He also advises not to automatically believe what the market is telling you about value. “If you know you’re right, you have to stick to your guns,” Icahn said.

Icahn has a remarkable knack for picking the right targets and generates most of the ideas in his firm by scribbling on a yellow pad. With his fearsome reputation, as soon as a company attracts Carl Icahn’s attention, investors are almost certain to make money starting the day Icahn buys the shares. After that, it’s all about squeezing management to augment the inevitable gains.

With both Icahn and corporate America awash in cash, Icahn has said: “We’re at the top our game. There’s never been a better time to do what we do.”

Icahn: ‘Showing You the Money’

Icahn has expressed frustration in the past that his investment prowess does not get the recognition that Warren Buffett does. He has a point. From 1968 through 2011, Icahn grew the initial $100,000 he invested in his Wall Street firm at a 31% annual rate. Over the same period, the book value of Buffett’s Berkshire Hathaway grew by 20%.

That superior performance, however, came at the price of greater volatility. Icahn returned an annualized 24.53% over the past ten years, according to Morningstar. Buffett’sBerkshire Hathaway (BRK-B) rose by a mere 8.68% percentage annually over the same period. But Icahn’s investors had to endure a 79% share-price decline in 2008, compared with 31.8% drop for Buffett.

I recently revealed how you invest alongside Carl Icahn in the most recent issue of my monthly investment newsletter, The Alpha Investor Letter.

Icahn is having one of his best years ever in 2013, with this recommendation up 93.56% through Oct. 21.

By way of comparison, Berkshire Hathaway (BRK-B) is up only 30.31% year to date.

The bottom line?

If you are willing to endure the greater volatility for greater returns, investing alongside Icahn could be one of the best investment decisions you ever make.

To read my e-letter from last week’s Eagle Daily Investor, please click here. I also invite you to comment about my column in the space provided below my Eagle Daily Investorcommentary.

Sincerely,

Nicholas Vardy, CFA

Editor, The Global Guru

Subscribe to my Newsletter and Trading Services.

Follow me on Twitter.

Check out my Blog.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair