Stocks & Equities

Investors locked in some of the recent gains by world stocks and bonds on Wednesday as they waited to see what the mood was at the most recent meetings of the U.S. Federal Reserve and the Bank of England.

European shares fell for a second straight day, then stabilized. Overnight losses on Wall Street and in Asia, along with concerns about company earnings, kept investors cautious.

Focus was largely on events later in the day. The Bank of England will publish minutes of its recent meeting at 0930 GMT (4:30 EDT). Then come U.S. retail sales data and eagerly awaited October minutes from the Fed.

Fed Chairman Ben Bernanke set the tone on Tuesday when he said the U.S. central bank will keep monetary policy ultra-easy as long as needed.

The dollar .DXY sagged after the comments but began firming up as European trading gained pace. The euro still hovered near a three-week high.

“It confirms our view that the Fed will be extremely careful in taking away accommodative monetary policy and that tapering will begin by March at the earliest,” said Elwin de Groot, an economist and strategist at Rabobank.

“Even though it feels like things may not go further, this policy will simply sustain it. And it is difficult to fight against it, so we could see a further narrowing of spreads and riskier asset prices going higher.”

…..market action in Britain China HERE

Yes Mrs. Yellen, QE Is Creating An Asset Bubble

Much to the consternation of those who continue to insist that we are not in a bubble it is my opinion that we are in a bubble at the moment and one that is being blown ever larger by investors who want to believe that the money machine will continue to spew forth profits and the risk of malfunction is extremely low. There can be no question that my views that QE has failed and that we are now at the upper end of a cyclical bull market within a secular bear market are not popular views. Those who believe in the efficacy of QE are very quick to point out that my views are – at this point – utterly useless as I have been wrong for the entirety of the year.

Just to set the record straight on that point here is what I said back in January:

My best case scenario for 2013 is a range basis the S&P of 1600 on the high side and 1260 – the 2012 lows – as the low side.

I missed the high by at least 12% – not a particularly good call to say the least. I of course am not alone in my views that we remain in a secular bear market nor am I alone in my call on when we will start the next cyclical bear market – both in the sense of timing and magnitude. It will of course do that – enter a new cyclical bear market that is – as it always does. Furthermore, when the market gets stretched to far in one direction it tends to overshoot in the opposite direction.

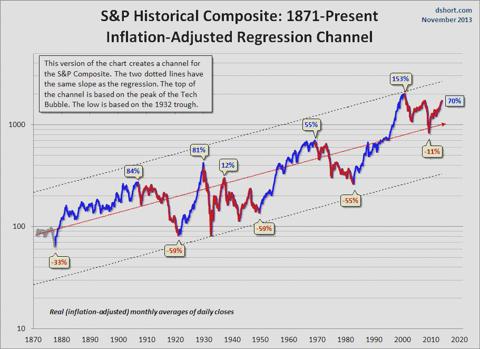

Doug Short’s chart below makes note of the fact that even though the dotcom bubble – at it’s peak – was the beginning of the current secular bear market – the market sell off in 2000 fell well short of what was seen in previous secular bear markets. In fact the 2000 market sell off didn’t even bring the market back to the regression trend line. The 2008 sell off did push the market slightly below the line – 11% to be precise – but even this sell off fell well short of all previous pull backs.

(click to enlarge & view the whole article with 13 charts)

The Dow reached 16,000 for the first time this morning.

That got me thinking about the book titled Dow 36,000: The New Strategy for Profiting from the Coming Rise in the Stock Market which was published in the year 2000. 13 years later and only 20,000 points short!

The news of “Dow 16,000” appears to be celebrated a little more than previous milestones since it coincides with the S&P 500 hitting 1,800 for the first time on the same morning.

With all the celebrating and headline frenzy, there has not been much chatter all with respect to what has driven the Dow to this new high. Almost all of the gains over the past two years have been the result of easy monetary policy. Corporate non-financial earnings have essentially been flat over this time, and financial earnings have been largely subsidized by the U.S. Federal Reserve paying interest (which it never did until a couple of years ago) on the $3 trillion of commercial bank excess reserves held on deposit at the Fed.

“Dow 16,000” should serve as a reminder to us to ask when earnings growth is coming. Will an economy that is more sluggish that the Fed and private economists expected be able to produce more earnings? Can companies cut even more costs (and employees) to squeeze out more earnings in order to justify their share prices?

At “Dow 16,000” these questions carry more weight than at “Dow 15,000” and “Dow 14,000” etc. If earnings don’t materialize, then maybe more Quantitative Easing will be required. Bulls might be happy to know that the next Fed Chairman Janet Yellen won’t have many qualms about doing this regardless of the long-term costs and ramifications.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

Lance’s thorough Stock Market Analysis – Ed

Lance’s thorough Stock Market Analysis – Ed

To start this week’s missive I want to share with you an excerpt from Randall Forsythe’s “Up and Down Wallstreet” column this weekend:

“IN A NEW STUDY, McKinsey & Co. concluded the Fed had no role in boosting stock prices and hence there is no bubble. Truth to tell, the consultancy had slipped from my consciousness since it extolled Enron as “one of the world’s most innovative companies,” instead of a criminal enterprise. Of course, since then, former McKinsey managing director Rajat Gupta was convicted of insider trading. McKinsey advised AT&T there wasn’t much future in mobile phones (which Bell Labs invented); advised General Electric, which lost $1 billion by following its advice; recommended that U.K. rail company Railtrack cut infrastructure spending, leading to fatal accidents and Railtrack’s collapse, among other great calls.

In particular, McKinsey asserts there has not been a large-scale shift to equities in search of higher returns. To be fair, the consultancy’s paper preceded the report from colleague Brendan Conway on Barrons.comthat inflows into equity mutual funds and exchange-traded funds are on track to top $450 billion in 2013 — more than the previous four years combined. Anybody can overlook nearly a half-trillion bucks in concluding there’s been no big shift to stocks.

McKinsey based its conclusions on the observation that price/earnings ratios and price-to-book ratios aren’t out of line. Yellen pointed out the equity-risk premium — the expected extra return from stocks over risk-free government bonds — adequately compensates investors. On the latter score, the equity-risk premium is flattered by the low level of Treasury yields — QE’s explicit goal. As for P/Es being moderate, that’s helped by the numerator being boosted by the reduction of interest expense — some $319 billion since 2007, according to ever-invaluable analysis from MacroMavens’ Stephanie Pomboy.

Even with this detachment from reality, and fundamentals, the markets advanced higher this week as Janet Yellen promised MORE, and potentially MUCH MORE, accommodative policy in the future.

Not coincidentally, the Wall Street Journal reports investment-grade corporate-bond issuance is running at a $1 trillion annual rate as companies take advantage of historically low rates, with which the Fed has had something to do. Moreover, the release of banks’ loan-loss reserves has added $112 billion to financial companies’ profits in the past two years, Pomboy says, which just might have something to do with higher house prices.

At the same time, an analysis by a famous hedge fund (whose name I can’t reveal or they’d kill me or I’d have to kill you) finds profits at non financial companies have been flat since 2011. Thus, the rise in their stock prices implies higher P/Es — consistent with the effects of monetary stimulation.

What is probably most disturbing though is that Janet Yellen does NOT

BELIEVE, despite mounting evidence to the contrary, that investment risk is

rising:

- Yellen Says Fed Doesn’t See Buildup Of Financial Risks

- Yellen Sees Limited Evidence Of ‘Reach For Yield’

- Yellen Says Fed Looks Out For Any Potential Asset Price Bubbles

- Yellen Doesn’t See `Misalignments’ In Asset Prices

….read more HERE

My “Peter Lynch Moment” Just Served a Huge Buy SignaL

My “Peter Lynch Moment” Just Served a Huge Buy SignaL

Mutual fund superstar Peter Lynch used to say that individual investors had a big advantage over Wall Street. If you just keep your eyes and ears open, Lynch would write, you’re bound to see big profit opportunities long before the investment-banking boys in New York.

And the biggest opportunities are often right in your own neighborhood.

Lynch knew his business.

For months now, we’ve been talking about a “ground floor” investing opportunity – a whole new business that I believe could triple or more in the next few years.

Well, just the other night, as my lovely wife and I were strolling to a village restaurant near our home, I ran right into proof that this potential $6 billion industry has already grabbed a big handful of the all-important consumer market.

This was more than just validation: It tells me this market is evolving even faster than I projected – and says I may have underestimated the overall market potential.

And that’s not all…

….read the rest HERE (Ed Note: Be sure to read the last half of “Shaking Up Silicon Valley” )

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair