Stocks & Equities

Successfully time one of these dramatic moves and you’ve created a big money making opportunity for yourself. Especially if you Shortsell the much quicker, more sudden & dramatic Bust moves. Then again if you are not a Shortseller, avoiding a Bust will at least save you a lot of capital as so many found out in 2008 when Blue chip Exxon lost 58% in 5 months, Microsoft 45% & Boeing fell from $88 to $30 – Money Talks Editor

More insights into long-wave theory…

– Readers don their K-wave caps and weigh in on this long-wave business…

– Why a 60-year-long wave theory should matter to you…

– Plus, Wayne Mulligan on how you can cut Wall Street out of your investments… the promise that crowdfunding offers investors.

“I agree with Mr. Rothbard’s opinion that government interference in the markets causes the boom and bust cycles,” writes one reader.

“But I also agree with the Elliott Wave and socionomics theories that market changes result from sentiments motivated by the thinking and mood changes of the masses (often unconscious), resulting in periods of economic change, booms, busts, wars, depressions, music, clothing styles, movies, etc.”

Hrmm… good point. Each theory definitely brings something to the table. Picking out when to apply each is the tricky part.

“OK, here’s my take on the K cycles,” writes a second reader, though we’re forced to trim her message down to fit our scarce space.

“First,” she explains, “maybe humans just need to go in cycles, and maybe it just takes about 60 years (plus or minus) for us to do it. After all, stock markets, economies, currency issues and interest rates are all human-generated (apes don’t bother with these things).

“Second, I think interest rates follow the K cycles pretty closely — give or take a bit for a hellbent Fed trying to ‘control’ interest rates. The last year or so would seem to indicate the Fed really can’t control interest rates as they would like us to believe. Time will tell for sure. But if interest rates do follow the K-wave, then there is reason for concern, as rising rates will certainly trounce the stock market and economy and seriously reduce the gummit’s disposable income (if it isn’t already).

“The K cycle does seem to match with recent history, so I suspect, against Rothbard’s suggestion, that there is some merit there. As you know, however, cycles work great until they don’t.”

“There may be a grain of truth in Rothbard’s words,” writes a third reader, “that soothsayers merely adjust their predictions to fit the facts. However, as a trader, I see waves (cycles) daily.

“There may be a grain of truth in Rothbard’s words,” writes a third reader, “that soothsayers merely adjust their predictions to fit the facts. However, as a trader, I see waves (cycles) daily.

“Traders use such arcane technical analysis tools as RSI, MACD, stochastics, Elliott Waves, Bollinger Bands et al., and these are used to predict a change from positive to negative and vice versa.

“As these waves coincide, inevitably, they push the markets higher or lower in the direction of coincidence (i.e., the one-minute coincides with the five-minute, which coincides with the 15-minute — you get the idea). Whenever you get a series of coincidences, the bigger the push, the more waves coincide, the more in one direction or another the markets will move. Like the waves on the ocean, driven by the winds. However, these business waves are driven by us…”

Heh. We try to leave the “arcane” technical analysis to our friend at theRude Awakening, Greg Guenthner. As for the Kondratiev wave theory, the basic premise seems reasonable enough to us.

Over periods of time, technological advances make people more productive. Business picks up. As people become more confident… their enthusiasm grows to a point where they start to give credence to business ideas and investments that make no sense. We suspect a politician or central bank is somewhere in the mix, too.

People start to take on too much debt. They pay ridiculous prices for certain assets because they either are too wrapped up in the market to realize their true value, or they’re hoping someone else is a greater fool. Eventually, at some point, someone stops for a second and asks what the hell is going on… and the fantasy is brought to a standstill, and then is shattered altogether. Phew…

And if all of that happens in 60 years or so… well, we guess you can call it a K-wave. But really, we’d feel more comfortable calling it with the benefit of hindsight.

And if all of that happens in 60 years or so… well, we guess you can call it a K-wave. But really, we’d feel more comfortable calling it with the benefit of hindsight.

Conveniently, as we write this to you, two reader messages plopped into our mailbag.

“Just who could use a long, irregular 60-year cycle?” one of the readers asks. “Isn’t a four-year cycle tough enough for most people?”

“While I agree with the wave theory,” writes the other reader, “I have to admit I agree with the statement that ‘markets can remain irrational longer than I can remain solvent.’ Since I have only 30 years, at best, years left, what should I do to insure I can take care of myself over this period?”

Glad you asked. Just what is the whole point of this discussion? Sixty years is a lifetime for some people… if they’re fortunate. What good is the long run? That’s when we’re all dead, you might be thinking.

Well, not everyone! Your editor has big plans 60 years from now! Besides, what if we’re on the cusp of a new cycle? What new innovations could we see in the near term? How would they change the way we live? Is this just a pipe dream? Has this abstract 60-year K-wave stuff driven us completely unbalanced and stark raving mad?!

Well, we hate to do this to you…. but you’ll have to tune in next week to find out. Today is Friday. Who wants to go down a rabbit hole as the weekend stares them in the face? Nobody, that’s who.

(OK… fine. If you’re really dying to talk about K-waves, we won’t leave you out in the cold. You can reach us here: peter@dailyreckoning.com.)

In the meantime, we’ll leave you in the hands of Wayne Mulligan. In today’s episode, he explains a new investment opportunity that is going to come into its own in the coming months. We’re very excited about it.

Then, in today’s DR PRO, Ryan O’Connor cuts Twitter down to size… and explains why one play he’s recommended (already up 31% to date) is still a buy. If you haven’t upgraded yet, you’re missing out on Ryan’s market-crushing picks. Why don’t you click here to upgrade, already!

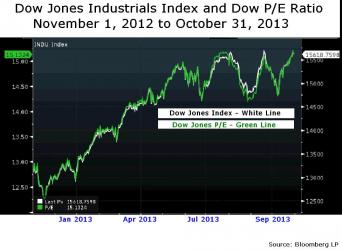

U.S. stocks rose, with benchmark gauges extending records, as investors assessed data on factory production amid speculation the Federal Reserve will maintain the pace of its monthly bond buying.

Exxon Mobil Corp. gained 1.3 percent after Warren Buffett’s Berkshire Hathaway Inc. disclosed a stake. FedEx Corp. climbed 1.4 percent after billionaire investorsGeorge Soros andJohn Paulson took positions. Fannie Mae and Freddie Mac increased at least 7.2 percent as Bill Ackman’s hedge fund disclosed stakes in the government-backed mortgage insurers. Western Union Co. dropped 5.3 percent after the company said its chief financial officer is leaving.

The Standard & Poor’s 500 Index rose 0.1 percent to 1,792.72 at 1:20 p.m. in New York. The gauge has gained 1.3 percent this week, poised for its sixth straight advance, the longest rally since February. The Dow added 48.30 points, or 0.3 percent, to 15,924.52. Trading in S&P 500shares was 8.1 percent higher than the 30-day average for this time of day.

Janet Yellen’s remarks yesterday told investors that “interest rates are going to remain low for a while, which is a positive environment for equities,” John Fox, director of research at Fenimore Asset Management in Cobleskill, New York, said by phone. Fenimore oversees about $1.8 billion. “The combination of earnings growth and expanded PE due to investors feeling better about things just continues to move the market higher.”

….read more HERE

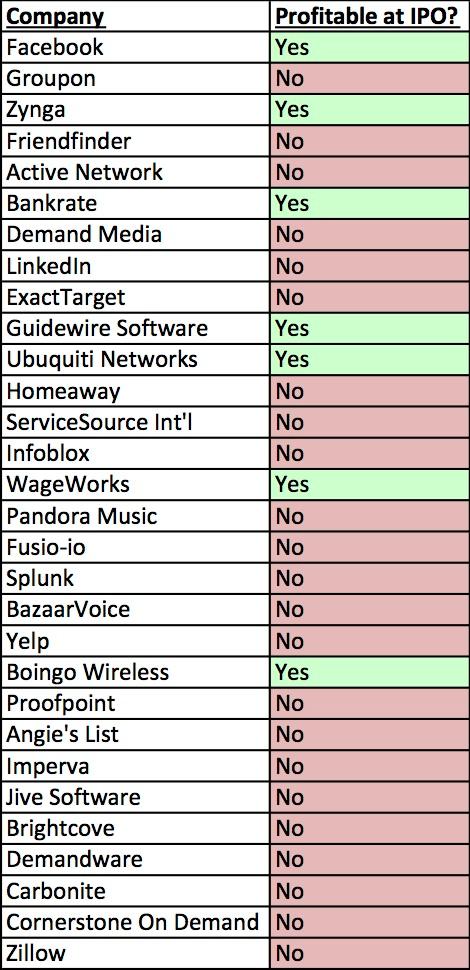

We’re in another Tech Craze, similar to the one in 2000, by the look of things

The last two years have seen a number of high profile Tech IPOs for businesses that are barely profitable or have never turned a profit. Indeed, of the tech firms that went public in 2013 so far, 73% have never turned a profit (compare that to just 27% of the tech IPOs that were unprofitable in 1999).

However, this is not to say that this Fed intervention is not creating tremendous opportunities for stock pickers. After all with the Fed juicing stocks to this degree, there is no shortage of mis-pricings in high quality companies.

To take out an annual subscription to Cigar Butts & Moats…

Best Regards

Phoenix Capital Research

Late yesterday Cisco Systems released its earnings which were significantly below expectations and it gave some pretty dismal guidance with respect to revenue going forward.

This is a stock which under the leadership of CEO John Chambers has been enough of a darling that it has been able to push the limits with its rosy proclamations and withholding bad news until the last minute. This style of investor communications began in 2000 and, yesterday, we were reminded that it is still the way that things are done.

The best analogy to describe this is where Lucy encourages Charlie Brown to take a kick at the football that she is holding only to lift it away at the last minute, causing Charlie Brown to go flying through the air.

Why haven’t investors conditioned themselves to expect this after so many years?

The answer is a little like the situations with Nortel and Blackberry. It is hard for investors to let go after having initial success in these once prominent brands.

The advantage that Cisco has over Nortel and Blackberry is its massive cash pile. The easy-money era of Alan Greenspan & Ben Bernanke at the U.S. Federal Reserve has made it a lot easier for companies with dated and uncompetitive business models to protect themselves.

Cisco has also had the added advantage of favourable U.S. tax laws that permit U.S. multinationals to keep their international earnings offshore. As long as they don’t repatriate earnings, it is like a tax deferral. Cisco has been a major participant in the lobbying effort to maintain this advantage.

It is also hard to let Cisco go because of how dominant it was. Not only did it rule the networking sector, but in March 2000 Cisco became the largest company in the world in terms of stock market value. That kind of valuation pedigree likely helped it in 2009 to be selected as one of the 30 stocks in the Dow Industrials Average.

However, this last earnings release may really sting. The company even suggested that the Chinese internet spying scandal contributed to its poor performance. The reality is that the products in which Cisco used to lead have become commodities and have been copied and heavily marketed by Chinese firms such as Huawei for many years now. Cisco’s competitive advantages have long since eroded. Despite that, not much has changed in terms of product focus or its business model since the 1990s when everything worked so well.

Another issue is that Cisco has an enormous institutional following. That also appears to be a significant source of the “benefit of the doubt” over the years.

It will be interesting to see if investors become more critical going forward rather than taking the company’s sunny comments at par value.

Cisco Systems Inc. is not held in the McIver-Jasayko Model Portfolios as of November 14, 2013. Comments about investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

Late yesterday Cisco Systems released its earnings which were significantly below expectations and it gave some pretty dismal guidance with respect to revenue going forward.

This is a stock which under the leadership of CEO John Chambers has been enough of a darling that it has been able to push the limits with its rosy proclamations and withholding bad news until the last minute. This style of investor communications began in 2000 and, yesterday, we were reminded that it is still the way that things are done.

The best analogy to describe this is where Lucy encourages Charlie Brown to take a kick at the football that she is holding only to lift it away at the last minute, causing Charlie Brown to go flying through the air.

Why haven’t investors conditioned themselves to expect this after so many years?

The answer is a little like the situations with Nortel and Blackberry. It is hard for investors to let go after having initial success in these once prominent brands.

The advantage that Cisco has over Nortel and Blackberry is its massive cash pile. The easy-money era of Alan Greenspan & Ben Bernanke at the U.S. Federal Reserve has made it a lot easier for companies with dated and uncompetitive business models to protect themselves.

Cisco has also had the added advantage of favourable U.S. tax laws that permit U.S. multinationals to keep their international earnings offshore. As long as they don’t repatriate earnings, it is like a tax deferral. Cisco has been a major participant in the lobbying effort to maintain this advantage.

It is also hard to let Cisco go because of how dominant it was. Not only did it rule the networking sector, but in March 2000 Cisco became the largest company in the world in terms of stock market value. That kind of valuation pedigree likely helped it in 2009 to be selected as one of the 30 stocks in the Dow Industrials Average.

However, this last earnings release may really sting. The company even suggested that the Chinese internet spying scandal contributed to its poor performance. The reality is that the products in which Cisco used to lead have become commodities and have been copied and heavily marketed by Chinese firms such as Huawei for many years now. Cisco’s competitive advantages have long since eroded. Despite that, not much has changed in terms of product focus or its business model since the 1990s when everything worked so well.

Another issue is that Cisco has an enormous institutional following. That also appears to be a significant source of the “benefit of the doubt” over the years.

It will be interesting to see if investors become more critical going forward rather than taking the company’s sunny comments at par value.

Cisco Systems Inc. is not held in the McIver-Jasayko Model Portfolios as of November 14, 2013. Comments about investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair