Stocks & Equities

Equity indices have climbed off their lows, but they continue to sport slim losses. The Russell 2000 (-0.2%) is the weakest-performing index while the Dow hovers just below its flat line.

Most sectors remain in negative territory, but technology (+0.3%) has joined the telecom services sector (+0.4%) in the green. Chipmakers have contributed to the rebound as the PHLX Semiconductor Index trades higher by 0.3%.

“I continue to think that this bull market will end in an upside explosion. I believe it is fated to go higher than anybody now believes. A wise move here might be buy the farthest out calls as possible on the thesis that the sellers are convinced they will never be hit. Wise heads are now warning that this market has now passed all sane appraisals, and as such it is highly dangerous. Nevertheless I believe that this market is fated to go higher than even the most bullish practitioners can conceive.

“I continue to think that this bull market will end in an upside explosion. I believe it is fated to go higher than anybody now believes. A wise move here might be buy the farthest out calls as possible on the thesis that the sellers are convinced they will never be hit. Wise heads are now warning that this market has now passed all sane appraisals, and as such it is highly dangerous. Nevertheless I believe that this market is fated to go higher than even the most bullish practitioners can conceive.

Reading my favorite advisories, they are overwhelmingly bearish, from the standpoint of the usual technicals, including the margin accounts, and the number of bullish advisories vs. the thin bears. All this aside, my instinct tells me that the stock market is heading into the clouds … I sense that the retail public is moving toward an extreme of bullishness, and that all negative indications will be swept aside. This bull market will not end with the usual and obvious technical indications. It will end with an extreme of bullishness from the crowd.

I note that talk about debt has simmered down. The US debt is so huge that reasonable talk about it is almost impossible. I believe in the end the US will turn to hyperinflation in its effort to minimize the debt. The debt is now so huge that I believe there are only two possible outcomes: default or hyperinflation. With the advent of hyperinflation, gold will come into its own. In the end, those who have been patient enough to hold bullion will be rewarded. Ultimately, a new monetary system will come into being, and its core will be built around gold. I think it may be three to five years before this country moves into hyperinflation, but the only alternative is default.

The government will attempt to diminish our debt by way of printing, to the point of hyperinflation … The miracle of inflation diminishes the power of debt over time. In the face of America’s unbelievable debt, prepare for inflation, rising inflation and finally hyperinflation … For a period of this third phase, speculative positions in the DIAs should be profitable, but only for a short while. In the meantime, position in gold bullion and gold items should be held.”

Too Damn Bullish

- Sentiment extremes flash warning signs

- Sleepwalking investors are finally buying

- Plus: What’s price telling us right now?

The individual investor is back. And he’s too damn bullish, according to about 5,000 reports I stumbled upon over the weekend.

In fact, the “everyone’s too bullish” theme is boiling over into the workweek.

“Stocks Regain Broad Appeal” reads the headline splashed across the front page of the Wall Street Journal this morning…

Of course, stories like this one are filled with quotes from Ma and Pa Investor who just received their third quarter statements in the mail. After sleepwalking through the first four years of this market rally, they’re finally ready to buy in now that they see those always-elusive market gains coming back to life.

Let’s check the stats to find out just where the super-bulls stand:

“A particularly worrisome [measure] is the Investors Intelligence gauge of adviser sentiment. Its last reading showed that 55.2% of respondents were bullish and just 15.6% bearish, tying the highest difference between the two this year,” reads yet another WSJ report. “The last time the gap was bigger was April 8, 2011, which preceded the sharpest stock-market correction of the current bull market.”

Yikes.

On the other hand, there’s also evidence that investors are getting cautious as the broad market reaches toward new highs.

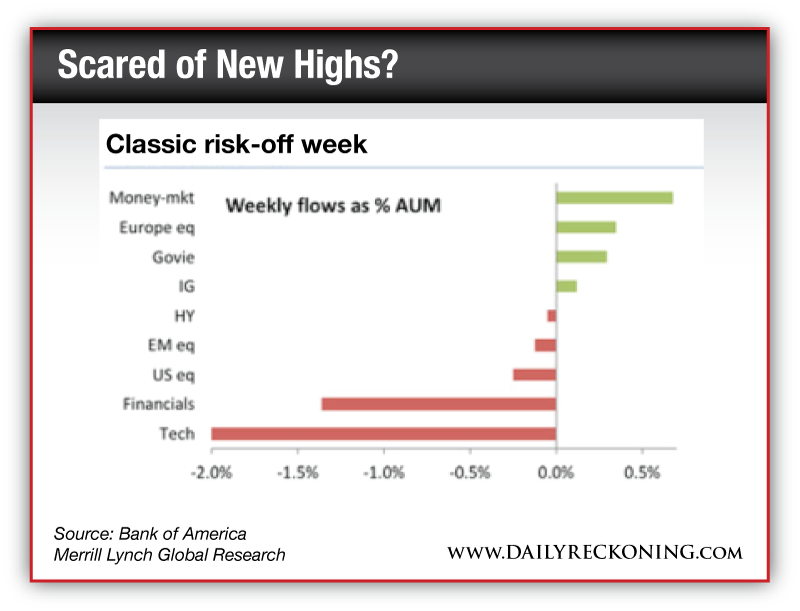

According to Bank of America Merrill Lynch Global Research, investors pulled $7.5 billion from U.S. equity funds last week. Financial and tech names lost the most coin as investors fled to money market funds…

While more investors are embracing the stock market as this year’s historic rally continues to unfold, there’s still a healthy amount of fear out there.

Yes, our end-of-year momentum rally was put on hold late last week. But strong buying Friday proves we’re still in a “buy the dips” market for now. Sentiment extremes could continue to rattle the market as we head into the final stretch of 2013. But until price breaks down, the benefit of the doubt belongs to the rally…

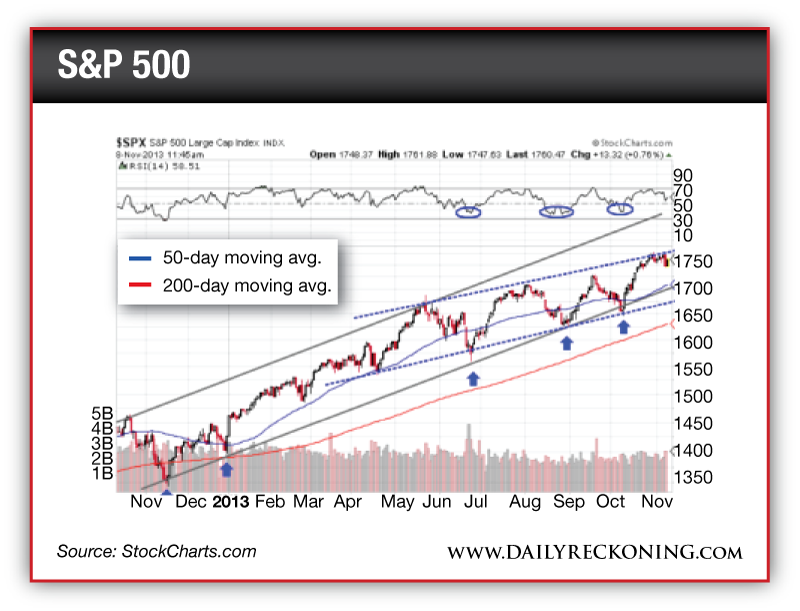

“In the chart above, I’ve annotated the current long-term uptrend in grey,” Jonas continues. “But there’s another uptrend in play that’s marked off by the dashed blue trendlines. So, which one is the ‘correct’ uptrend for stocks? Well, both of them are right now…

“The fact that Mr. Market is hitting his head on resistance at that dashed line definitely gives me more confidence in its ability to hold the S&P’s price action this fall. But we’ll really see which of the two trends wins out on the next move back down to support.”

Right now, Jonas is patiently stalking a new trade. Join him today so you won’t miss his next potentially profitable move…

[Ed. Note: Send your feedback here: rude@agorafinancial.com – and follow me on Twitter: @GregGuenthner]

P.S. Starting November 18th we’ll be delivering the Rude Awakening to you from a different email address: rude@agorafinancial.com. To be sure you won’t miss a single issue, take the time to whitelist this address right now…

And of course, we always welcome feedback from our readers. If you have any questions about this free subscription upgrade, send us an email atrude@agorafinancial.com.

“The Stamp Act was a direct tax imposed on the colonies by King George III. This act inevitably led to the American Revolution. Just as the Stamp Act did in 1765, Obamacare should act as a wake-up call” – Rand Paul

The Future Fiscal Drain of Obamacare

The current debate on Obamacare is not over whether the US needs a system of universal healthcare. That debate has passed, successfully. There was the act in congress, a 2012 Presidential Election centred on the topic, and it was upheld in the Supreme Court. It is instead on whether the Affordable Care Act (Obamacare’s official title) is satisfactory in providing this service of healthcare, or whether it will end up like other failing federal fiscal programs that create a long term burden on their economy. It has the potential to do that because of the individual mandate.

The current debate on Obamacare is not over whether the US needs a system of universal healthcare. That debate has passed, successfully. There was the act in congress, a 2012 Presidential Election centred on the topic, and it was upheld in the Supreme Court. It is instead on whether the Affordable Care Act (Obamacare’s official title) is satisfactory in providing this service of healthcare, or whether it will end up like other failing federal fiscal programs that create a long term burden on their economy. It has the potential to do that because of the individual mandate.

The individual mandate requires Americans to purchase health insurance or pay a tax penalty, and it is showing to be Obamacare’s Achilles heel. One simple reason is that on average, males between the age of 21 and 35 see a doctor six times over that time horizon. To that subgroup, there is no value in buying insurance. It’s not to say males 21 to 35 have no reason to purchase health insurance; moreover, the financially burdening decision to sign up for a plan becomes irrational when compared to paying a penalty tax.

The system relies on the premiums paid by the young generation. From a business perspective, the widest margins are in the instances of the young and healthy adults, whom are exactly the ones not eager to sign up for Obamacare. So as the President of the free world touts about individuals who were formerly denied healthcare due to prior or existing health conditions (because of a requirement in the law that prevents insurers from denying coverage), the fact of the matter is currently the majority of Obamacare enrollees are either Medicaid recipients or individuals with health conditions. These people would represent customers for insurers with quite narrow or even negative profit margins.

Simply put, it’s a law of averages. Everybody buys into the system to pay for the costs of those who will unknowingly require its services. But when the law, from the outskirts, allows individuals who with the highest probability of not requiring health insurance to simply opt out and pay a tax, its longevity becomes questionable.

This leads to another shortcoming with Obamacare. The way the law is structured, excess costs incurred by the private insurance companies in some instances may be recovered from funds by the federal government. For example, according to an article in the Wall Street Journal this week, if insurers underestimate costs, they can be recovered from the Federal Government. That is one way to minimize the risk to insurers; however, back to the original problem, should Obamacare inevitably fail to attract sufficient healthy individuals to subsidize the cost of the more demanding ones in terms of health benefits, premiums will go up in future years as the costs of the program increases.

The individual mandate was the biggest political stalemate when passing the act because conservatives did not believe the government had the authority to force someone to buy a good or service, but the law passed. Inevitably, it is a tax. It costs Americans more via their insurance premiums, or smaller wages as insurance is provided by their employer. The service in return for their tax dollars is healthcare.

Add this to the list of other underfunded American entitlement program.

All investments contain risks and may lose value. This material is the opinion of its author(s) and is not the opinion of Border Gold Corp. This material is shared for informational purposes only. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. Border Gold Corp. (BGC) is a privately owned company located near Vancouver, BC. ©2012, BGC.

Over the past year I have noticed that Cameco (CCO) will make an appearance every few months in the technical and fundamental research that comes across my desk. This week it happened again, with one particular technical analyst making the case for the third time in 12 months as to why the stock is poised to rise to interim highs if it can just break through resistance in the low 20’s. (CCO currently trades near $20). This kind of research is focused on the shorter-term. As a result, when things don’t unfold in a timely manner, repeating the initial call is common practice unless there has been something dramatic to change the viewpoint of the technical analyst.

In addition, there have been a number of fundamental analysts, as well as one of the few newsletter writers that I actually like, who have all made a very compelling long-term case for buying the stock.

The long-term story is fairly simple. The world’s energy needs can’t be met through fossil fuel sources and alternative (green) sources continue to be extremely disappointing at this stage. As a result, relatively clean nuclear energy will be the eventual choice, especially for current energy-importing countries that don’t appear to have potentially dazzling shale deposits to be discovered and tapped.

So, why is CCO stuck in a range? (See chart above).

One word: Fukushima.

The incident in Japan still resonates with the public. In fact, it is still allowing for the press to publish stories that border on extremism. This week, there was a story that highlighted a speech by David Suzuki who stated that if another earthquake of greater than 7.0 were to hit Fukushima right now, the West Coast of North America might have to be evacuated. While there has not been a rush of scientists scrambling to back up Dr. Suzuki’s claim, the mood is sufficient to let the story stand without a whole lot of rebuttal.

So, it will take time for this issue to pass. Eventually, tough choices will have to be made and pragmatism will take charge. At this stage, the cost and benefits of more nuclear energy will have to be given a fair hearing. CCO should look a lot more reasonable and may be able to break the tether to its current trading range. But, waiting for that to happen also has its costs.

Cameco Corporation is not held in the McIver-Jasayko Model Portfolios as of November 8, 2013. Comments about these investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair