Stocks & Equities

Wednesday morning I wrote the following:

“Another all-time high in the Dow Industrials this morning with non-confirmation from the S&P and Russell. Tomorrow we will get the Twitter IPO hooplah which might very well coincide with another all-time high for the S&P 500, a confluence which will only serve to stir the animal spirits more than they already are.

The Investor’s Intelligence survey confirms that the spread between bullish investors and bearish investors is the widest it’s been since April 2011 (a particularly frothy month for markets which preceded a major top in stocks).

Would it be too perfect for the Twitter IPO to mark the top of the rally? Probably. However, savvy investors should probably cast at least one skeptical eye towards a $20 billion valuation for a money losing business that for all intents & purposes has been sliding backwards in terms of its “coolness” factor for many months.”

This morning we got another marginal all-time high in the S&P E-mini futures following the surprise ECB rate cut announcement:

The 1774.50 high print was hit shortly after the 7:45am ECB announcement, however, sellers showed up in aggressive fashion as soon as the US market opened at 9:30am EST and they did not let up all the way through to the closing bell.

The Twitter IPO turned out to be a major distraction which captured headlines…..

….read more HERE

A true American icon. Its motorcycles are so distinctive that the company actually tried to trademark the “Harley sound,” that familiar rumble of the bikes’ exhaust, back in the mid-1990s.

It’s also a well-managed company and one of those true rarities: a successful turnaround story. This is a company that was facing bankruptcy in the early 1980s yet managed to rebuild itself into the pride of American manufacturing … and the subject of countless case studies in MBA programs worldwide.

Harley’s management was able to pull off that coup by leveraging that intangible quality that is so hard to imitate: brand cachet. For a particular breed of leather-wearing motorcycle enthusiast, there is simply nothing on par with a Harley.

But all of that said, I wouldn’t touch the stock … at least not at today’s prices.

At first glance, Harley would appear only modestly overpriced. It trades for 20 times trailing earnings and 2.5 times sales. This compares to 19 times earnings and 1.6 times sales for the S&P 500.

A modest premium is appropriate for an iconic company with Harley’s branding power (and not to mention its high return on equity of 26.1%), right?

Well, maybe. But Daimler ( DDAIF ) — a company that knows a thing or two about vehicle branding — trades for just 10 times trailing earnings and 0.60 times sales. Yes, I realize it’s not an apples-to-apples comparison and that Harley runs a higher-margin operation in a business with fewer direct competitors. All else equal, Harley should trade at a slight premium to a larger automaker like Daimler. [Daimler, incidentally, is currently the leader in InvestorPlace’s Best Stocks of 2013 contest with year-to-date returns of over 50%.]

But all else is not equal. Harley has a serious growth problem, and it’s not one that will go away with a recovering economy.

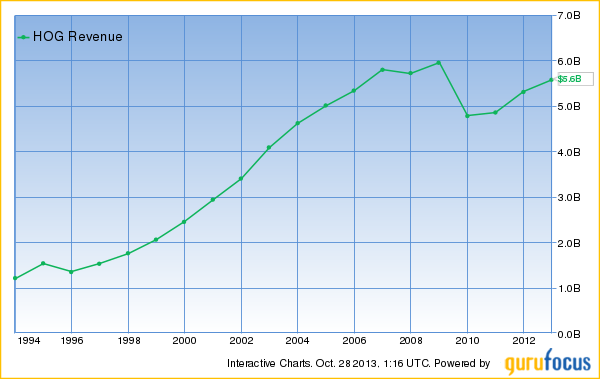

Harley’s revenues are still below their pre-crisis highs (see Figure 1), and unit sales paint an even bleaker picture. Harley sold 349,196 bikes in 2006, and sales dropped to just 247,625 in 2012.That’s a unit decrease of nearly 30%.

To be fair, revenues and unit sales have enjoyed a nice bounce since the pits of the financial crisis. But Harley will never get its old mojo back for one critical reason that is completely outside of its control:demographics.

Down the road from my house in Dallas, there is greasy drive-in burger joint called Keller’s … a place I’ve been known to frequent a little more often than my doctor might recommend. On any given weekend, you might see a dozen or more bikers parked in the lot, showing off their chrome-laden Harleys. And nearly all of them are over the age of 45. Most are over 50.

This isn’t a coincidence. Harley-Davidson is a brand whose sales depend disproportionately — almost exclusively, in fact — on middle-aged Caucasian males. Riders younger than 40 generally lack the time, interest or the bankroll to buy a Harley. But by the time they get into their 60s or older, the noise and joint pain have begun to make riding lose its allure. You might still ride in your 60s, but you’re doing it less frequently and you probably aren’t buying a new bike.

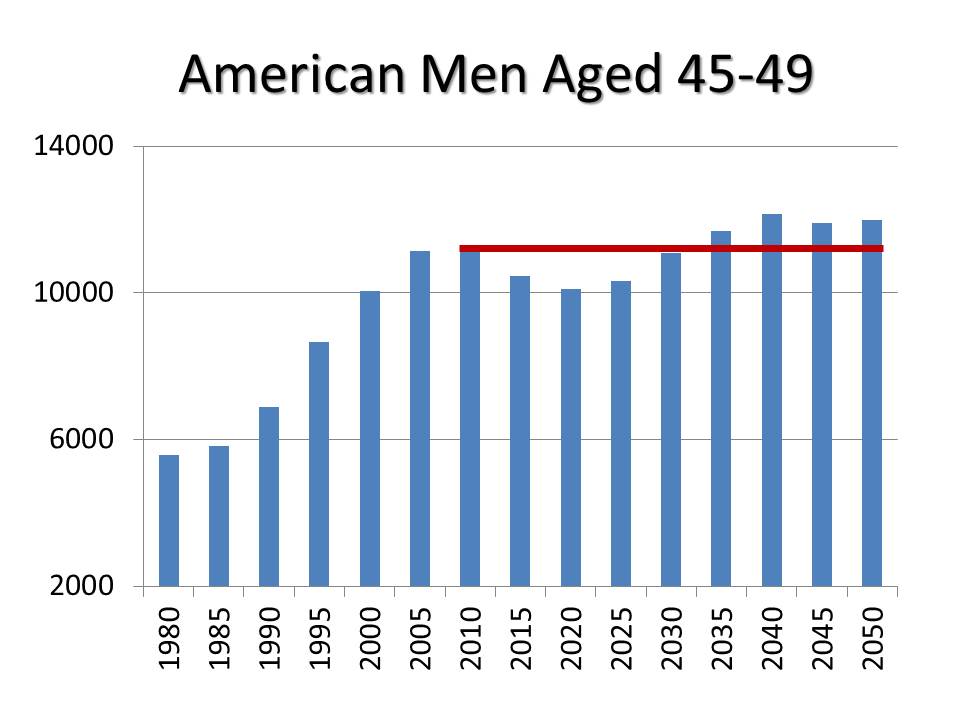

Figure 2: American Men Aged 45-49 by Year

The sweet spot is the mid-40s to early 50s. And with the Baby Boomers — the largest and wealthiest generation in history — now largely aged out of this key demographic bracket, Harley has a serious problem. Generation X — my generation — is not nearly large enough to pick up the slack, and Generation Y (aka “the Millennials” or “Echo Boomers”) are decades away from being in the demographic sweet spot for Harley, and this assumes they take to riding like their dads did. The number of American men aged 40-49 is set to decline through the early 2020s and won’t reach its old 2010 peak until 2035 (see Figure 2).

CNN Money reported on this as far back as 2010, and demographic strategist Harry Dent — my old boss — has used Harley as a case study for decades.

Harley-Davidson’s management is not stupid. They understand the issues they face, and they have gone so far as to address it with a dedicated page on their Investor Relations site: Harley-Davidson Demographics.

Stop and think about that for a minute. Have you ever seen a company dedicate prime website real estate to the demographics of their customer base before? I haven’t. But then, few companies face the severe demographic issues that Harley does.

The company has aggressively expanded its marketing efforts to attract younger men, non-Caucasian men, and women, to modest success. Per the demographic site, management writes:

“In 2012, U.S. sales of new Harley-Davidson motorcycles to our ‘outreach’ customers — young adults 18-34, women, African-Americans and Hispanics – grew overall at more than twice the rate as sales to our traditional U.S. customer base of Caucasian men, ages 35-plus.”

But realistically, there is no replacing white Baby Boomer men. And this means a very rough decade ahead for Harley-Davidson.

Stocks in gently declining industries are not necessarily bad investments, as tobacco stock investors have no doubt noticed.

Under the right set of circumstances — strong financial health, large barriers to entry, good dividend growth and share buybacks — stocks in no-growth industries can make better investments than those in high-growth industries.

But for this to be the case, the stock has to be priced appropriately. Big Tobacco has had a great decade-long run because it started out cheap and paid a monster dividend. Harley-Davidson, in contrast, trades at a slight premium to the market and yields only 1.3%.

Harley-Davidson might be a good buy … eventually. But given the demographic headwinds it faces, it’s not cheap enough for serious consideration at this time. An intrepid investor might even consider it as a short.

About the author:

Charles Lewis Sizemore is the Editor of the Sizemore Investment Letter premium newsletter and Chief Investment Officer of Sizemore Capital Management.

Mr. Sizemore has been a repeat guest on Fox Business News, has been quoted in Barron’s Magazine and the Wall Street Journal, and has been published in many respected financial websites, including MarketWatch, TheStreet.com, InvestorPlace, MSN Money, Seeking Alpha, Stocks, Futures, and Options Magazine and The Daily Reckoning.

Wowee! More highs in the stock market. The Dow rose 128 points yesterday.

Wowee! More highs in the stock market. The Dow rose 128 points yesterday.

Is the US stock market headed for a bubble? Maybe… but what do we know?

Our guess is that the people who are buying stocks today have a lot more confidence in the Fed than we have. As near as we can tell, today’s stock prices owe a lot to the Fed’s manipulation of asset prices and little to the fact that the companies are more intrinsically valuable… or more likely to produce higher earnings per share.

In fact, as Chris reported yesterday, earnings-per-share estimates have been falling as US stocks have been rising.

Watch out. Artificially priced markets are like huge bungee cords. You can stretch them out. But the further they get pulled out, the greater the sting when they snap back.

When will that happen? We don’t know that, either. But we’re not going to stand in front of it waiting for it to happen.

There are two groups of people in the world.

In one group are those who think they know things. In the other are the people who think those in the first group are idiots.

These are not absolutely separate categories. Instead, they share a long border and plenty of spots for crossing under cover of night.

Aristotle was perhaps the first and foremost of those who thought he knew something. He had it all figured out more than 2,000 years ago. There was a natural order to things, he thought.

Civilized people should live in city states; anyone beyond the city walls was either a “beast or a god.” And the city state itself – the ideal form of political organization – was to be ruled by… well… the rulers.

That was just the way it worked. Aristotle: “For ruling and being ruled are not only necessary, they are also beneficial, and some things are distinguished right from birth, some suited to rule and others to being ruled.”

Why a city state and not a country state? Why couldn’t people rule themselves? Who was to say who the ruler should be?

You could ask as many questions as you wanted. Aristotle would have just as many silly answers. But even the ancients were on to him.

“None of us knows anything, not even whether we know anything or not,” said Metrodorus of Chios, aiming for Aristotle’s head.

But it was the great Pyrrho from Elis who developed the philosophy we know today as “skepticism.” Loosely, a skeptic is someone who suspects that other people don’t know nearly as much as they think they do.

And loosely speaking, the skeptics are mostly right. When it comes to central banking and central economic planning, they are always right.

The planners and world improvers are reliable sources of amusement, and not much more.

Tom Friedman, Ben Bernanke and Paul Krugman reduce the sum of human wisdom every time they open their mouths. Bernanke thinks he can solve a debt problem… with more debt.

Krugman thinks he can solve a spending problem with more spending. Friedman doesn’t think at all. But that doesn’t stop him having a solution for every problem. (And if you applied his solution, you’d have a much bigger problem.)

Our old friend Pierre Lemieux reminds us of Adam Smith’s comment:

The man of system […] is apt to be very wise in his own conceit, and is often so enamored with the supposed beauty of his own ideal plan of government, that he cannot suffer the smallest deviation from any part of it.

He goes on to establish it completely and in all its parts, without any regard either to the great interests or to the strong prejudices which may oppose it: he seems to imagine that he can arrange the different members of a great society with as much ease as the hand arranges the different pieces upon a chessboard; he does not consider that the pieces upon the chessboard have no other principle of motion besides that which the hand impresses upon them; but that, in the great chessboard of human society, every single piece has a principle of motion of its own, altogether different from that which the legislature might choose to impress upon it.

The idea that you can organize a society according to your own prejudices is ancient. Old, too, is the notion on which it depends: that you have some knowledge that others don’t.

In fact, all you know is what everyone else knows: nothing! And we’re not even sure about that.

Regards,

Bill

More from Bill:

Repeat After Me: Economics Is NOT a Science

So it would seem to me that Karl Marx might prove to have been right in his contention that crises become more and more destructive as the capitalistic system matures (and as the “financial economy” referred to earlier grows like a cancer) and that the ultimate breakdown will occur in a final crisis that will be so disastrous as to set fire to the framework of our capitalistic society.

So it would seem to me that Karl Marx might prove to have been right in his contention that crises become more and more destructive as the capitalistic system matures (and as the “financial economy” referred to earlier grows like a cancer) and that the ultimate breakdown will occur in a final crisis that will be so disastrous as to set fire to the framework of our capitalistic society.

Not so, Bernanke and co. argue, since central banks can print an unlimited amount of money and take extraordinary measures, which, by intervening directly in the markets, support asset prices such as bonds, equities and homes, and therefore avoid economic downturns, especially deflationary ones. There is some truth in this. If a central bank prints a sufficient quantity of money and is prepared to extend an unlimited amount of credit, then deflation in the domestic price level can easily be avoided, but at a considerable cost.

….read Faber’s Real US Economy Trampled by White Elephants HERE

In June of 2012, we added Eagle Energy Trust to our High-Yield Pool that we manage and which is a part of the McIver/Jasayko Model Portfolios. It has been a bit of a roller- coaster ride in the units of the Trust. The most challenging period was a cut in distributions and some operational concerns which hit the news in the autumn of last year.

About a month and a half after we had invested in Eagle, another similar foreign income trust named Argent was launched. At least we now had the potential for some comparable metrics. The main difference was that the new Trust had less history and, as a result, it was a little more of an unknown quantity.

The attractiveness of the foreign income trust structure is that it reintroduced Canadian investors to the potential for relatively high flow-through income that was once a feature of the domestic income trusts, an enormous fad that met its demise when legislation was changed to nullify their advantages. The main stipulation of the new trusts is that the income had to be from a foreign source. And, there was no motivation for the Canada Revenue Agency to fight their formation since their existence represented a net increase in the amount of total taxation whereas the old domestic income trusts ended up cannibalizing much of the existing corporate and personal tax revenue.

Since Eagle’s challenges late last year, it has quietly recovered to draw even with Argent again in terms of price and yield (see the chart above). Again, the benefit of Eagle is a longer track record. More of its laundry has been revealed. However, Argent is still considered an attractive investment by many brokerage firm analysts.

The business plans of Eagle and Argent have the potential for pitfalls because of the lack of critical mass and the lack of operational diversification. Their businesses are focused because the overall size of both companies is relatively small compared to the larger energy producers. There is always a chance that either can get tripped up by one or two issues. Hence, they high current yields which serve to compensate for these risks (both are near 12.5%).

And, now that the two are in a relative dead heat again in terms of price and yield, it will be an interest race to follow going forward.

Eagle Energy Trust is held and Argent Energy Trust is not held in the McIver-Jasayko Model Portfolios as of November 6, 2013. Comments about these investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair