Bonds & Interest Rates

Yellen to Make Bernanke Look Like Hawk

“She will make Mr. Bernanke look like a hawk. She, in 2010, said if could vote for negative interest rates, in other words, you would have a deposit with the bank of $100,000 at the beginning of the year and at the end, you would only get $95,000 back, that she would be voting for that. And that basically her view will be to keep interest rates in real terms, in other words, inflation-adjusted. And don’t believe a minute the inflation figures published by the bureau of labor statistics. You live in New York. You should know very well how much costs of living are increasing every day. Now, the consequences of these monetary policies and artificially low interest rates is of course that the government becomes bigger and bigger and you have less and less freedom and you have people like Mr. De Blasio, who comes in and says let’s tax people who have high incomes more. And, of course, immediately, because in a democracy, there are more poor people than rich people, they all applaud and vote for him. That is the consequence.”

“We Are in ‘QE Unlimited”

“On September 14, 2012, when the Fed announced QE3, that was then extended into QE4, and now basically QE unlimited, the bond markets had peaked out. Interest rates had bottomed out on July 25, 2012–a year ago–at 1.43% on the 10-year Treasury note. Mr. Bernanke said at that time at a press conference, the objective of the Fed is to lower interest rates. Since then, they have doubled. Thank you very much. Great success.”

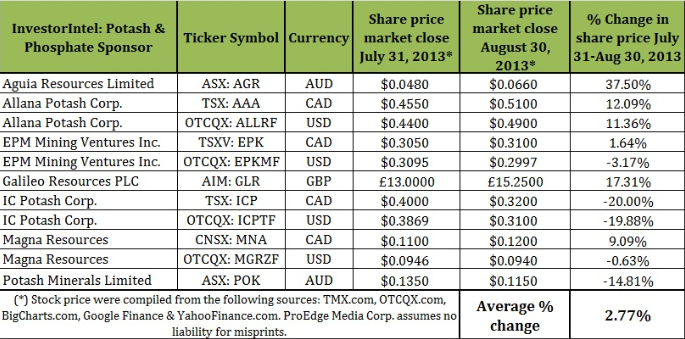

Global population is exploding and demand to feed this growing population is in the early stages of an exponential uptrend.

Potash is a key non-replaceable ingredient in fertiliser, the primary commodity used by farmers worldwide to increase the yield of their fields. Crops that not only deliver fruit, vegetable and grains to the dinner table, but also feed chicken, pork and beef stocks that an ever growing population are demanding.

Companies in the business:

….read more of this authors opinion of companies worth investing in HERE

Feeding the World

by Bob Moriarty 321Gold.com

“Phosphate is a rock that is chemically treated to become phosphate fertilizer. It takes almost two tons of phosphate rock to make one ton of fertilizer. Peak oil is real. Peak oil also means peak food. We have to increase the food grown on limited land to feed the increase in population. That means more use of fertilizer. Phosphate is desirable because of it’s phosphorous content needed for food production.”

….read more about a Canadian company in the business HERE

Hidden Finds from the edge of Biotech & Neurotechnology….

Four Small-Cap Growth Names with Different Value Drivers: Keay Nakae

Source: George S. Mack of The Life Sciences Report (9/19/13)

It’s important to take the emotion out of investing. Keay Nakae, senior research analyst with Ascendiant Capital Markets, looks at micro- and small-cap biotech stocks from an engineer’s perspective: It’s all about the data. In this interview with The Life Sciences Report, Nakae reports on four companies with upcoming catalysts that potentially position them for significant growth—and the ability to grab investors’ attention. More >

Hidden Finds in Regenerative and Medical Technology: Jeff Cohen

Source: Peter Byrne of The Life Sciences Report (9/12/13)

Ladenburg Thalmann & Co. Inc.’s Jeff Cohen regularly explores the frontiers of regenerative and medical technology looking for solid investment opportunities. In this interview with The Life Sciences Report, Cohen reveals promising finds in one of the world’s fastest-growing business sectors. From robotics to skin grafts, Cohen knows his science and his market. More >

Griffin Securities’ Keith Markey Gives Performance Reviews on Four Favorite Biotech Names

Source: Peter Byrne of The Life Sciences Report (9/12/13)

As science director for Griffin Securities, Keith Markey knows his way around the advanced technologies of the most promising research in biotech. In this interview withThe Life Sciences Report, Markey explains the science behind new developments in the antibiotic, diabetic and dermatological fields, highlighting ground-floor investment opportunities that investors will not want to miss. More >

Digging Below the Surface of Neurotechnology: Casey Lynch

Digging Below the Surface of Neurotechnology: Casey Lynch

Source: George S. Mack of The Life Sciences Report (9/5/13)

Neuroscience is about as complex as it gets. The central nervous system contains the brain and spinal cord, where hundreds of billions of neurons are located—and that doesn’t include the peripheral nervous system. Casey Lynch, managing director of NeuroInsights, works to make sense of both the disease processes affecting the nervous system and potential therapies that could help patients and enrich investors. In this interview with The Life Sciences Report, Lynch brings some clarity to the complexity, and speaks frankly about the wild goose that some Alzheimer’s disease investigators have been chasing. More >

Scientific Conferences Create Buzz and Move Biotech Stocks: Michael King

Source: George S. Mack of The Life Sciences Report (9/5/13)

It’s that time again. From Labor Day through the New Year, analysts jet off to conferences across the U.S. and Europe to hear data they’ve been waiting on for years. Michael King, managing director and senior biotechnology analyst at JMP Securities, has been at this game for almost two decades, and he has a firm grip on how data releases about molecules and their targets will affect the biotech stocks in his coverage. In this interview with The Life Sciences Report, King also names four growth companies making important advances in hematologic cancers. Just in time. More >

Yesterday, during his press conference to explain why he decided not to Taper the rate of Quantitative Easing (money-printing), Ben Bernanke mentioned that he was distressed by the fall in the U.S. Labor Force Participation rate.

It is a little late in the game for him to be noticing that. The U.S. Labor Force Participation Rate has been declining for years.

In fact, it has declined at a faster rate during the era of Quantitative Easing! QE appears to contribute to this problem

How might that be the case? It might be that QE degrades the labor market by encouraging companies to focus more on financing and investing activities (taking advantage of low interest rates) instead of operational activities which tend to require labor.

The Fed seems to be in a pickle with this one.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair