Gold & Precious Metals

10-yr Treasury Benchmark Yield: Pointing lower……and some great comments from Dr. Doom – Mark Faber

US Treasury 10-yr Benchmark Yield [last 2.75%]: At a 38.2% retracement, 10-yr yield at 2.38; at 50% retracement, yield at 2.19%…

Mark Faber’s reaction to the Fed decision on Wednesday—this is priceless! “QE infinity”…

Regards,

Jack & JR

MEMBER SERVICES

-

BLACK SWAN FOREX

-

GLOBAL INVESTOR

Research, commentary, analysis and trading advice using ETFs covering global markets and asset classes … delivered each week.

-

THE BLACK SWAN STORY

The annual Canadian inflation came in at 1.1% this morning edging down from a 1.3% July posting. Core CPI,the number watched closely by the Bank of Canada, rose 0.2% in August in line with expectations.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

Whether its mortgage rates, the solvency of your pension or what it costs you to travel, Michael zeroes in on the main force in society affecting your finances.

Whether its mortgage rates, the solvency of your pension or what it costs you to travel, Michael zeroes in on the main force in society affecting your finances.

{mp3}mcbuscom09192{/mp3}

Over the past week, Mario Gabelli has made several guru real time transactions. These transactions involve one new buy and an increase in two others. These real time picks represent purchases or sales of a stock in which a guru owns greater than a 5% stake. These real time picks help to keep you more closely informed.

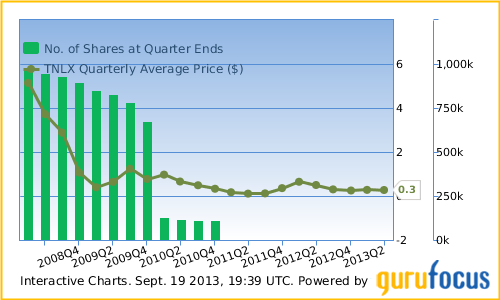

Trans-Lux Corp. (TNLX)

On Sept. 13 Gabelli made his first buy into Trans-Lux. The guru bought a total of 10,087,100 shares of the company’s stock. He bought these shares at an average price of $0.125 per share. Since his buy the price has increased 60% to $0.20 per share.

Gabelli previously held on to Trans-Lux but closed out his position in 2011Q1. His updated position is the largest stake he’s ever taken with the company, with 38.92% of the company’s shares outstanding.

…..view more on Trans Lux & his other 2 positions HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair