Mike's Content

Michael focuses on what caused the financial crisis of 2008 and the repercussions that are still with us to this day.

Michael focuses on what caused the financial crisis of 2008 and the repercussions that are still with us to this day.

{mp3}mcbuscom09192{/mp3}

…. Says Bearish Precious Metal View Was “Incorrect”

…. Says Bearish Precious Metal View Was “Incorrect”

Yesterday it was Goldman capitulating on their near-term gold, er, capitulation reco (expectedly so after gold ripped over $75 in the span of 24 hours). Now, it is Bank of America’s turn to close their silver short.

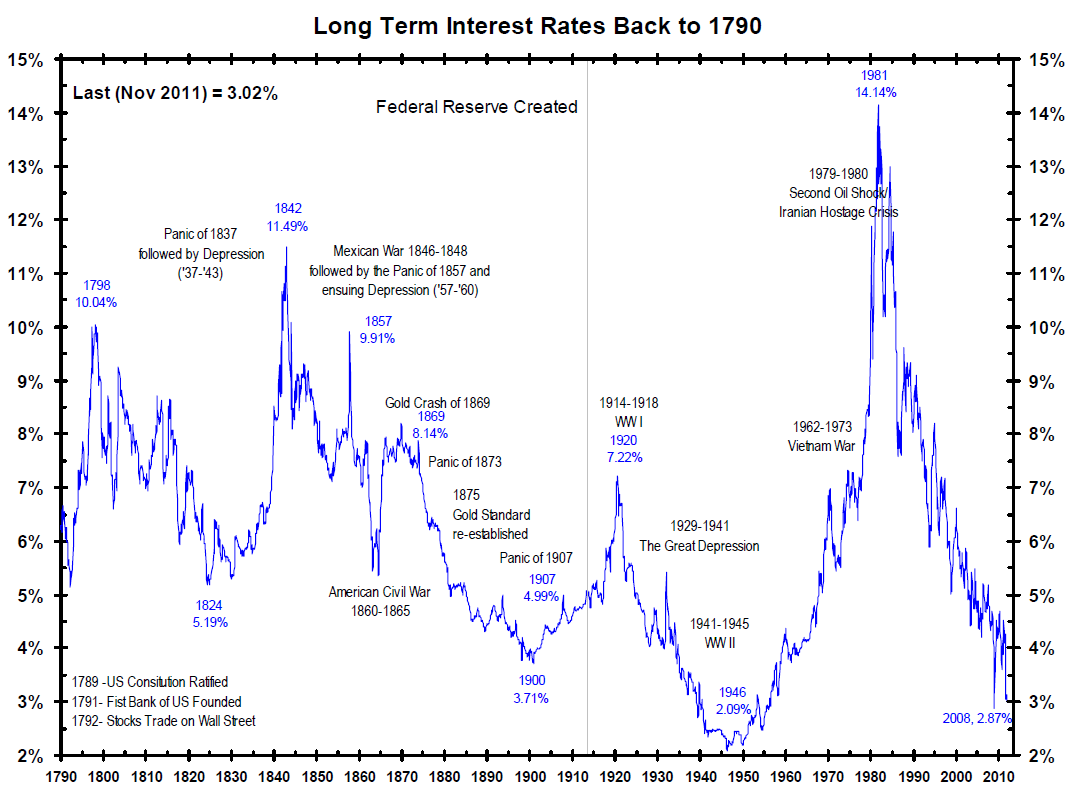

….more commentary and great chart HERE

After four months of huffing and puffing about the possibility of scaling back asset purchases (money-printing) by just a little bit, Ben Bernanke, the Chairman of the Federal Reserve Board decided to do nothing. In fact, when looking at the Fed’s communication policy, it was worse than nothing.

The Fed has grown in terms of influence over the last few decades as its mandates and oversight have expanded dramatically. The Fed has also been seduced into to thinking that it can steer the economy (which is not the job of central bankers, by the way) and has responded by implementing multi-trillion dollar monetary experiments.

The Fed is so massive now that it was rather stunning that Bernanke failed to grasp the crucial need to get the communications policy right. Back in May, he was a bit surprised that investors were bidding up prices in the investment markets as though the Fed would never end its policy of Quantitative Easing (or QE3, as the current iteration is called) and he appeared during a Congressional testimony to say that this wasn’t the appropriate assumption and that investors should expect the Fed to “Taper” is rate of QE3 as early as September.

Now, Bernanke might have been patting himself on the back at that point thinking that he was upholding his general promise of being more transparent than his predecessors. After all, transparency is certainly a virtue when it comes to communications.

However, regardless of transparency, the message needs to be consistent over time and acted upon if trust is to be maintained. Bernanke essentially laid down a line (similar to another politician recently). However, as the summer drew to a close, Bernanke clearly became concerned about this line when contrasted against the fact that employment was not improving as fast as he had forecast. This lead to yesterday’s “Do Nothing” announcement.

However, “doing nothing” crashes right into the narrative that he has established back in May. Going forward, every time he talks, the markets will now be more confused. Is he serious? Is he not serious? Which metrics are really important to him? Are his comments politically influenced?

Sometimes “doing nothing” is doing a lot. But sometimes it can create a worse situation when one suggested that something was going to happen.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

The Shanghai free-trade zone, China’s first, will officially open for business on September 29. Just about every China economy maven has been following the months-long saga regarding the establishment of the zone because in Shanghai the central government will punch a gaping hole in the country’s currency wall.

The Shanghai free-trade zone, China’s first, will officially open for business on September 29. Just about every China economy maven has been following the months-long saga regarding the establishment of the zone because in Shanghai the central government will punch a gaping hole in the country’s currency wall.

….read the whole article HERE

First: There are lots of reasons to be fully invested in the stock market right now. And that’s why it’s so important to keep an eye on all the bubbles. They’re everywhere. And we have plenty of reasons to fear any number of them bursting, especially this one…

No fewer than 165 stocks on the major exchanges hit new 52-week highs yesterday, which is all the more reason to take notes today… Shah’s been identifying bubbles for decades, ever since his hedge fund days. And now that he uncovers them for individual investors, his readers know firsthand that “bubble watching” is more than a wealth protection strategy.

There are lots of reasons to be fully invested in the stock market. And that’s why it’s so important right now to keep an eye on all the bubbles.

They’re everywhere. And we have plenty of reasons to fear any number of them bursting.

So let’s look at these bubbles now, while you still have time to prepare. And I’m not just talking “capital preservation” here…

You can make a killing when a bubble bursts, especially the one we’ll start with today.

It’s the biggest of the big bubbles. And it could start hissing at any moment.

The hissing will be loud, too…

How to Prepare for “The Mother of All Bubbles”

It may not be classified as a bubble, but it is. We know what bubble-bursting effects it has because it burst in 2008 and shook the life out of global financial markets.

I’m talking about “interconnectedness.”

Manifest and growing interconnectedness creates its own bubble. The bubble enlarges as masses of banks and financial institutions and private investors end up on the same side of the same bets. The bubble bursts when they want out, when they all head for the exit doors at the same time.

In 2008, the bubble, on the outside, stretched around mortgages, subprime and prime mortgages. But on the inside, the massively inflating mortgage bubble resulted from a desperate clamor by investors of all stripes. The hunt for yield took investors further and farther out on the risk spectrum.

Low interest rates were the conduits through which hot air filled the mortgage market balloon.

Why is that important now?

Because the same-as-before manipulation of interest rates by governments and central banks has forced investors into riskier and riskier assets in the hunt for yield across the global low-rate environment, again.

In order to maximize low-yielding investments in bonds, namely sovereign and corporate bonds, collectively far and away the largest asset class on the planet, investors leverage themselves by borrowing to increase exposure to magnify their returns. It is this debt surge that underlies the interconnectedness pumping up the interconnectedness bubble.

As long as interest rates are low and yield curves around the globe are fairly steep, which means short-term rates are a lot lower than long-term rates, the leverage that investors have employed in the form of short-term borrowings to pay for higher-yielding longer-term bonds will work in their favor.

But if short-term rates rise faster than long-term rates…

(chart via Barry Ritholtz – The Big Picture)

The “Hissing” Will Be Loud

It’s bad enough if long-term rates rise, knocking down the price of existing bonds that offer lower yields, such that investors holding those long-term bonds have mark-to-market capital losses on their books. Investors, like banks, have to contend with reserve ratios, and losses on their portfolios will cause them to have to raise capital or deleverage. Still, they don’t have to sell the bonds and actually take capital losses.

The Federal Reserve is the best example of this.

It is sitting on over $3 trillion in bonds and has an approximate loss on its portfolio of some $200 billion as rates have ticked higher. But it doesn’t have to mark-to-market its portfolio (like banks do), and it doesn’t have to sell its bonds, ever.

The hissing sound of the debt interconnectedness bubble deflating will start to be heard if short rates start to rise, and it will be heard loudly.

Mass panic could ensue if investors’ cost of carrying their inventory of relatively low-yielding longer-term bonds rises.

Because most institutional investors and all banks borrow short term on a huge scale, if short-term interest rates they have to pay start rising and they keep having to rollover and borrow more when their short-term borrowings mature in days, weeks, and months, they will start losing the “spread” on the investment they bet on. If at the same time long-term rates move up (causing capital losses), then the “trade” becomes increasingly unprofitable, and to unwind positions, investors will sell their long inventory of bonds before their capital losses mount.

Selling, on a massive scale, would create a global panic as leveraged investors everywhere rush for the exit doors.

It’s the global interconnected of the same debt bubble caused by low rates that worries central bankers and governments.

And rates are starting to rise.

But, so far, central banks have kept a lid on short rates. Long rates can rise, and although they are causing many problems already, a steady and measured rise in long rates can be absorbed by most economies without dire consequences.

However, if long rates jump precipitously or if short-term rates rise unexpectedly and central bankers can’t keep a lid on them, look out!

What to Watch

Investors have to watch the yield curve and know at what rates the long end of the curve and the short end of the curve are rising, both in absolute terms and relative to each other.

Rising rates will cause massive problems, economic disruptions, and losses everywhere, in some places and on some assets more than others. We’ll cover all of those scenarios in this series.

But as far as interconnectedness and the bubble brewing in global debt interconnectedness, investors can hedge their exposure to rising interest rates by buying inverse bond ETFs, by buying puts on debt-denominated ETFs, and by managing their own bond portfolios by deleveraging themselves and keeping portfolios short term in duration.

For investors seeking to profit from the debt interconnectedness bubble bursting, taking longer-term positions, meaning buying inverse ETF instruments and ETFs that will rise if bond prices fall, is much better than buying options, which if you don’t get the timing right will expire and have to be continually rolled over.

But don’t worry…

I’ll be covering this situation for you right here in Money Morning. And I’ll be suggesting specific positions you can take to either hedge yourself or play the bursting of these bubbles for pure profit.

Stay tuned…

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair