Economic Outlook

It’s a huge morning for the US economy.

At 8:30 a.m. ET, the Bureau of Economic Analysis will release its first reading on first-quarter gross domestic product, which is expected to show the economy grew at just a 1% pace in the first quarter.

This announcement will be followed at 2 p.m. ET by the Federal Reserve’s latest monetary policy announcement.

In March at its most recent meeting, the Fed said it would not look to raise interest rates at the April meeting.

Moreover, Federal Reserve Chair Janet Yellen will not speak with reporters after the statement is released Wednesday afternoon, and so all the market will have to digest is the statement itself.

But the market will be looking for the Fed’s assessment of one thing in the statement: its outlook for the economy.

In a note to clients over the weekend, Bank of America’s Michael Hanson wrote that the Fed would most likely have a more “somber” outlook on the economy after a first quarter that saw economic data widely disappoint.

Hanson wrote:

At the March FOMC meeting, the Fed took any policy changes in April off the table. We don’t expect similar language about June policy at the April meeting. We do expect a more somber description of recent activity. This dovish shift in the nearterm view should translate into significantly lower odds of a June rate hike in our view. But any market participants who seek an explicit signal that June also is off the table are likely to be disappointed: the FOMC will want to maintain as much policy flexibility as possible.

During the quarter, first-quarter GDP growth was consistently revised down, and some measures like the Atlanta Fed’s GDP tracker indicates the economy may not have grown at all during the first quarter of 2015.

In a note to clients ahead of the GDP report, Joe LaVorgna at Deutsche Bank wrote: “It is possible that GDP growth (specifically productivity) is being understated, because the income side of the economy has not experienced the same degree of weakness evident in the output figures.”

Before the Fed gives its latest statement, however, it will have an answer.

Given that the Fed ruled out a rate hike in April and that Yellen will not speak with the news media after the announcement, markets have more or less been looking past the Fed meeting, or at least expecting to take it in stride with the week’s news flow. Treasury bonds, however, were selling off a bit ahead of Wednesday’s announcement, with the 10-year note rising above 2% for the first time in over a month.

Also, in addition to the big GDP number set for release Wednesday morning, the big data point for Fed policy is probably coming up Thursday with the release of the employment cost index. This report, which captures factors like employee benefits in addition to wages, is expected to show employer costs rose 0.6% in the first quarter, or 2.6% over the prior year.

Anecdotal evidence from the labor market, like the wage increases announced at Wal-Mart and Target in addition to commentary from economic surveys like the Beige Book and Monday’s Dallas Fed report, have hinted that wage pressures might be working their way through the economy. Thursday’s report will be a big test for this growing theme.

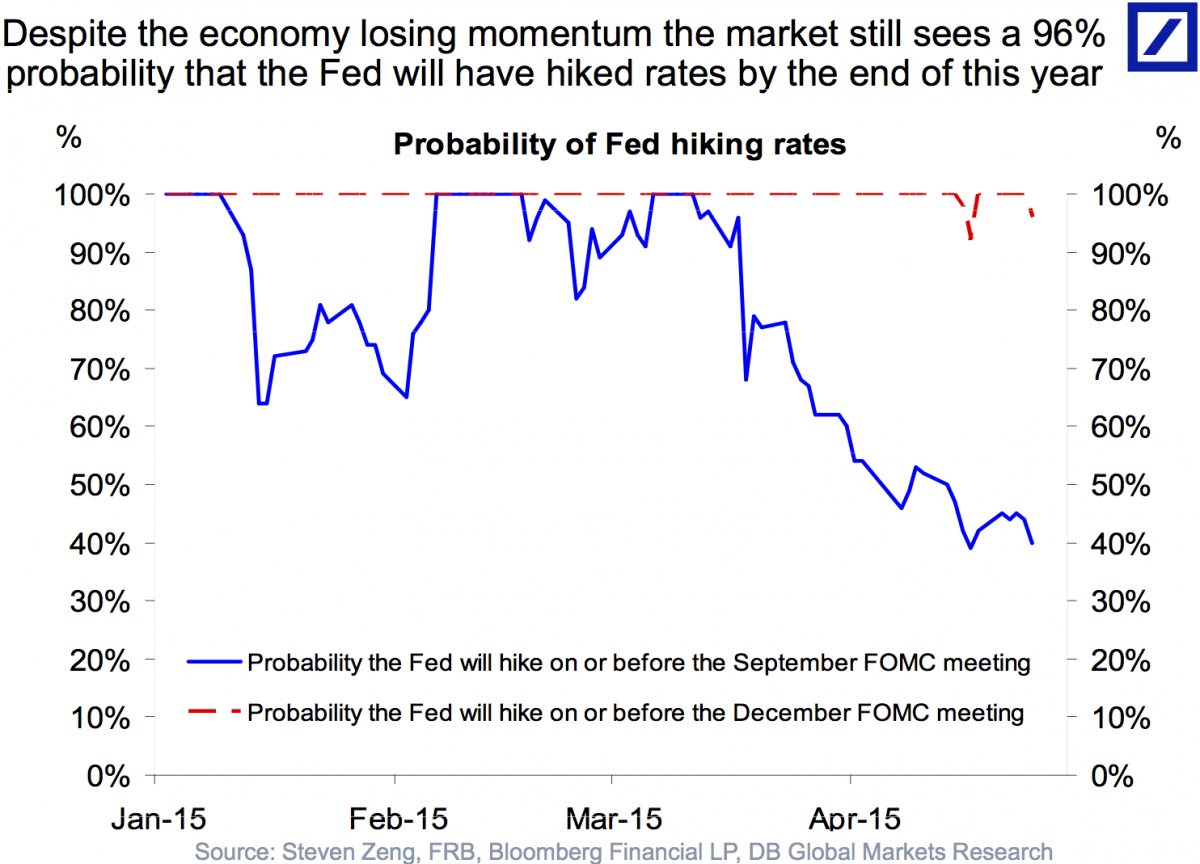

In a post ahead of Wednesday’s Fed announcement, Pimco’s Tony Crescenzi wrote that the firm still expected economic conditions would warrant a rate hike in September.

And in a chart circulated earlier this week, Deutsche Bank economist Torsten Sløk said most everyone in the market expected a rate hike by December.

The slowdown in retail sales growth has been a big surprise this spring, as lower gasoline pump prices were expected to boost spending. What’s going on?

Analysts at TIS Group have a fascinating if scary answer: The consumer credit cycle is breaking down as families sense the economy is slipping a gear and don’t want to over-leverage themselves. This is happening even as corporate credit continues to boom.

It’s the old story, right? If you don’t need credit, you can get it — and if you do need it, you can’t.

This distinction is important because the world is not on a typical boom-and-bust business cycle. With central banks driving much of the action, the world is instead on a credit cycle, which according to TIS means that everything depends on the availability and price of credit.

With the Fed threatening to raise rates despite a disinflationary environment, credit conditions are changing in the United States as well as in other developed countries.

The chart above, provided by TIS, shows that according to Federal Reserve data, Consumer Credit Revolving fell

sharply in February 2015 (blue circle). The analysts note you have to go back to mid-2010 and then to the dark days of the first quarter of 2009 to see readings as weak. In its commentary, the Fed has focused on consumers’ unwillingness to charge purchases.

This is not about the weather; it is about consumers’ view of the future of their jobs and wages. It can be seen as a warning that consumers are reining in their purchases and not using their windfall from lower gasoline prices in the expected way.

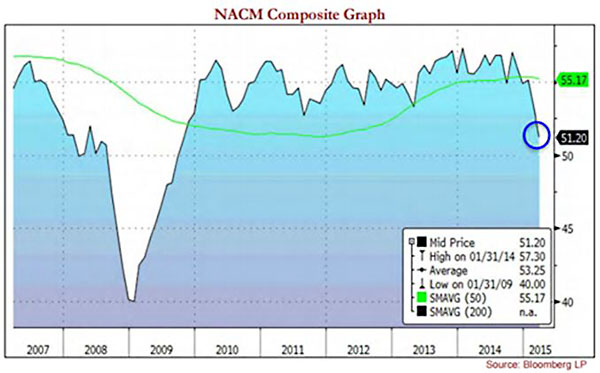

It gets worse. The National Association of Credit Managers produces a monthly report on credit conditions, and the March edition, which you can read here – and you should read it — paints an incredibly gloomy picture of current credit stresses.

{kind=link}

This chart above shows the NACM Index Composite and appears to show a problem is developing in the credit system. This is how NACM described it in the March blog:

“We now know the readings of last month were not a fluke or some temporary aberration that could be marked off as something related to the weather. There is quite obviously some serious financial stress manifesting in the data and this does not bode well for growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound.”

TIS analysts note that in the NACM Composite, a reading below 50 signals an economic contraction is underway. The last sub-50 reading was in September 2009. So after 5.5 years, the NACM Composite is closing in on a return to contraction territory, though it is not there yet.

Looking at sub-indexes of the composite, the Service sector’s unfavorable conditions have generated a reading at 48, which signals contraction. Manufacturing was also below 50, at a 48.9 reading. So the consumer’s willingness and ability to borrow is deteriorating. And companies are also experiencing more difficulty accessing credit, the analysts observe.

This begs the big question: Why is this happening?

We need to dig deeper, and look at another NACM gauge called the Rejection of Credit Applications Index. The TIS analysts call it “a real stunner,” and it sure is. Broken down by service and manufacturing sectors, the service reading is at 42, worse than it was during the September 2008 crash. The manufacturing reading is 43.8, also below September 2008 levels. In fact, the March calculation is the largest increase in rejections of applications for credit on record.

TIS goes on to conclude that “this is what a burgeoning credit crunch looks like.” Based on this data, the notion that the Fed is even thinking about raising the price of credit — at a time it is already hard to come by — seems crazy and impossible. It might even be fair to expect the Fed would want to ease credit amid such conditions.

This is a very out-of-consensus idea and may help explain why the stock market remains stuck even as it bumps against the top of its recent range.

Corporate Bonds Rule

So what about the corporate bond market?

For this part of the story, I turn to old friend Fil Zucchi, a money manager and independent analyst in Arlington, Va., who argues that the credit managers report above is consistent with what’s been happening since 2009. “The economy basically sucks for individuals and small companies and their credit is tied to that,” he said.

But Zucchi added that if you are a large company that has access to the public debt markets or syndicated bank lines, pension funds are throwing money at you. The markets are about financial engineering, not fundamentals, these days — and the cash from large debt buyers that allows for such engineering activities like buybacks and dividend increases keeps rolling in, arguably even at an accelerated pace. Even energy credit is improving and there’ve been some very large refinancing deals in that space in the last couple of weeks.

Fil goes on to point out that first quarter corporate bond issuance was $399 billion in 2009, $429 billion in 2011, $457 billion in 2012, and was $496 billion this year.

In short, corporate debt issuance is not broken — it is blowing away all years post-financial crisis. As a point of reference, he notes that veteran credit analyst Brian Reynolds argues that an annual average issuance of approximately $100 billion per month suggests that companies are issuing debt not only to refinance maturities and for operating cash, but to also to fund buybacks.

To see how recent corporate bond issues trade in the secondary market, Fil tracks a cross-section of new bonds, trying to cover most industries and credit quality. His only filter is the size of the offering, a minimum of $750 million. The latest batch is by far the strongest seen in the past three years, he says.

Zucchi also looks at the generic Investment Grade and High Yield Credit Default Swaps indices. In a strong credit cycle, these have become the most important derivatives because they are the instruments that credit bears will attack when they want to disrupt markets.

You may recall from the financial crisis that credit default swaps, or CDS, are essentially insurance contracts for credit. They move higher when credit holders are worried and reach for more insurance, and move lower when credit holders are not worried about defaults and become increasingly complacent.

The chart above, supplied by Zucchi, shows the investment Grade Credit Default Swaps with bands that can be used as guides for when: a) bulls are firmly in control; b) things are getting agitated; and c) bears may be gaining the kind of upper hand that has been a precursor to the 2000-2002 and 2007-2009 financial debacles.

When he captured this screenshot, the IG CDX was a little bit above 65bps. Since then it has fallen lower. Fil observes that the 60 bps area has been a line in the sand for credit bears. Below that level, he says it is likely they would be forced to initiate a whole new round of short covering — an event that would likely spill over into more buying of equities.

The bottom line is that while consumer credit may be freaking out, corporate credit appears to be quite healthy. Perhaps this is just another manifestation of the difference between the 1 percent and everyone else.

Best wishes,

Jon Markman

Two months ago in Money and Markets, I alerted you to a troubling trend when U.S. economic reports started taking a turn for the worse, with more negative than positive surprises in the data.

Fast forward eight weeks and the downtrend in our economic data has deteriorated even further, telling me an inflection point for the stock market may be close at hand. Let me explain …

The graph below plots the Bloomberg Economic Surprise Index (ESI: blue line, middle panel), which measures the degree to which recent data has been beating economic forecasts (positive surprises), or falling short (negative). Citigroup produces a similar indicator, which I highlighted in my February article, but both tell the same sad story about the U.S. economy; it’s quickly losing momentum.

Just to recap; the line rises when economic reports are exceeding forecasts, like yesterday’s housing data — a rare positive surprise — but the index declines when data misses projections — last Friday’s disappointing Leading Economic Indicators data, for example.

As you can see above, the data has been falling far short of expectations lately.

In fact, the current trend in the ESI turned negative earlier this year, and hasn’t looked back, recently falling to the lowest level since the 2008 financial crisis!

In other words, the U.S. economy is underperforming by the widest margin since the bull market in stocks began six years ago.

And yet, despite the glaring underperformance of the real economy down on Main Street, you wouldn’t have a clue about this by looking at Wall Street’s performance.

The S&P 500 Index, in spite of volatile up-and-down swings this year, is still less than 2 percent off its record high of 2,119.60 notched in February. What gives?

This is an unusually wide disconnect between real economic performance and investor sentiment, and something’s got to give. The gap between perception and reality, must close sooner or later; either with the U.S. economy improving, or with the stock market declining.

As you can see in the chart above, there has been a very strong link between downturns in the ESI warning of trouble ahead for stocks in the past.

Now, don’t get me wrong; this doesn’t necessarily mean stocks will plunge, but a correction is certainly possible, even overdue at this point. But keep in mind, many of the corrections shown in the S&P 500 chart above were relatively brief and minor pullbacks in price of less than 10 percent.

Bottom line: Now is a good time to be cautious. And you may want to consider grabbing some open gains and/or raising your protective stops. For more aggressive investors, an inverse ETF could provide a hedge to help you profit from a correction.

Above all, keep a watchful eye on trends in the economic data, and in the stock market. If we see a string of better-than-expected data, stocks could move higher again. But watch out if the S&P 500 Index begins following recent economic data to the downside.

Good investing,

Mike Burnick

About Mike Burnick

Mike Burnick, who has over 25 years of professional investment experience, is the editor of the Ultimate Stock Options newsletter and associate editor and trader of Martin’s Ultimate Portfolio.

Mike has been a Registered Investment Adviser and portfolio manager responsible for the day-to-day operations of a mutual fund. He also held the position of investment research analyst and Director of Research for Weiss Capital Management, where he assisted with trading and asset-allocation responsibilities for a $5 million ETF portfolio.

An open letter to President Obama was posted on an Iranian website (khodnevis.org) today from Dr. Mahmoud Moradkhani — the nephew of Iranian Supreme Leader Ayatollah Ali Khamenei. This letter is explosive and tells Obama, in essence, that the ayatollah, his uncle, is lying in negotiations, practicing the Shia doctrine of taqiyya in which it is permissible for Muslims to lie to the infidel for the advancement of Islam. He advises the president not to pursue his nuclear deal with Iran and to focus on the atrocious human rights record of that country. But allow the doctor to speak for himself.

An open letter to President Obama was posted on an Iranian website (khodnevis.org) today from Dr. Mahmoud Moradkhani — the nephew of Iranian Supreme Leader Ayatollah Ali Khamenei. This letter is explosive and tells Obama, in essence, that the ayatollah, his uncle, is lying in negotiations, practicing the Shia doctrine of taqiyya in which it is permissible for Muslims to lie to the infidel for the advancement of Islam. He advises the president not to pursue his nuclear deal with Iran and to focus on the atrocious human rights record of that country. But allow the doctor to speak for himself.

Dear Mr. President

I am presenting this open letter as one of the serious opponents of the Islamic republic of Iran on behalf of the like-minded opposition groups and myself. Because of my knowledge of this regime, especially of Ali Khamenei who is my uncle (my mother’s brother), I see it as my duty to inform you about this regime and the issue of nuclear negotiations with the Islamic regime of Iran.

Let me at first inform you that the regime that falsely calls itself a republic came to power in 1979 by deceiving Iranian people and the world through provoking Iranian people against the regime of Mohammad Reza Pahlavi and gaining the support of the world community.

The tragedy of Cinema Rex*, believing in Khomeini’s words and then establishing a backward regime that is violent, medieval and against all international laws are all results of Iranian people and the world community being deceived. We are witnessing that not only a rich and cultured country like Iran has become a victim of this regime but also the Middle East and the whole free world. The intervention of Ali Khamenei’s regime (following Khomeini’s footsteps who had no other intention other that domination of Iraq) in Lebanon, Palestine, Afghanistan, Iraq, and Syria is more than obvious. As if these were not enough, he has now added the Arabian Peninsula to that list.

In any case, this regime has done great damage to Iranians and to the international community.

We can find a historical example of this kind of deception prior to the Second World War. Hitler manipulated and deceived German people and European countries and the hesitation in addressing the problem with Hitler led to a great disaster.

Due to the changes in time, the domain of the disaster might become limited now but breach of human rights is the same, regardless of the number of people who become victimized in the process.

Ali Khamenei and his collaborators know very well that they will never become a nuclear power. They certainly do not have the national interest of Iranian in their mind; they just use the nuclear issue to bully the countries in the region and export their revolution and middle-aged culture to other countries. Obviously, you and European countries do not give the Islamic regime any concession unless you are certain that they comply with the agreement. The Islamic regime of Iran will certainly prolong the verification period the same way that they have delayed and prolonged the nuclear talks. It is in this period that the wounded regime will retaliate with its destructive policies.

The countless breaches of human rights violations, spreading of Islamic fundamentalism, intervention and creating crisis in the Middle East are all unacceptable and contrary to democratic and humane beliefs of yours and ours.

While we can, with some measure of decisiveness and courage, uproot the wicked tree of the Islamic regime of Iran, just settling for cutting its branches is nothing more than avoiding responsibility.

It is clear that the eradication of the Islamic regime of Iran is the responsibility and mission of Iranian people and specially the opposition abroad; however, by putting obstacles in front of Iranian people and the Iranian opposition abroad one prevents them from doing their task.

The Islamic regime of Iran, based on their deceptive nature have sent their mercenaries abroad and even managed to recruit and manipulate some American-Iranians. Individuals who out of self-interest are lobbying for the Islamic regime of Iran and hiding its true nature and giving a false picture of its intentions; in the same manner that while Khomeini was in France, the so-called Iranian intellectuals did not let people of Iran and the world, realize the true meaning “the Islamic republic”. Those so-called intellectuals polished the remarks of Khomeini and converted them to positive, popular, strong and victorious ones.

We see that unfortunately in your country and your state media (the Persian section of Voice of America) and especially in UK (the Persian section of BBC) the remarks of the opposition of Islamic regime of Iran are being censored and instead the indecent habit of analyzing and relaying statements of the Islamic regime of Iran have become a norm.

I have a deep understanding and insight of the habits, morals and true indentions of this regime and I find it necessary to let you and the world know that the true evil of the Islamic regime of Iran is far more damaging and dangerous to be resolved by just signing an agreement.

People who have always lied, deceived and believe in Taqiya**, people whose main goal is supremacy and domination over others can never be trusted.

Instead they should be confronted with the very basic principles that have led to their criminality and

-

- To put an end on breaching of human rights violations; in other words, an end to Qisas***, random executions, discrimination, suppression of dissent, media repression, religious and ideological hegemony.

- Devolving power to the people and the abolition of restrictive laws, such as mandatory supervision in elections.

- Giving freedom to religious minorities and repealing laws limiting the choice of thought and religion.

- Non-interfere policy toward governments of countries such as Afghanistan, Iraq, Lebanon, Syria and Yemen.

- Cancelling the assassination orders of dissidents in the world that have resulted in the killing of journalists, writers and even cartoonists.

I believe that any agreement or concession that is not associated with these basic conditions in reality will only be assisting this regime in achieving its indecent goals.

The possible disaster following this kind of hesitation will be similar to the historical mistake made prior to the Second World War.

Ali Khamenei will not be satisfied with the little that he has today and surely, and in all secrecy, at the first possible moment will attempt to bully and dominate.

Removing the crippling sanctions without fundamental changes in this regime will not be in Iran’s interest and will only facilitates the Islamic regime of Iran in reaching its objectives.

United States of America and Europe should not jeopardize their long-term interests due to short-term ones.

There are powerful and pro-active forces in the Iranian opposition and if the censorship of the media that are supporting the Islamic regime of Iran were to be removed, the opposition can easily organize and assist the powerful civil disobedience of Iranian people.

Iranian people want peace and freedom; without this regime not only can they ensure the resurrection of a civilized country but also a peaceful region.

Yours respectfully

Dr.Mahmoud Moradkhani

The stronger than expected February’s job market report fueled expectations that the Fed will increase interest rates sooner rather than later. We believed that market reaction was a bit exaggerated, and suggested in the Gold News Monitor not taking the hike for granted. The U.S. recovery is not as strong as it is commonly believed (as it was confirmed by the downgraded Fed’s economic projections) and there are many downside risks, such as Greece’s crisis, stubbornly low inflation, sluggish wage growth, the Chinese and global slowdown and too strong a greenback, which may stall the Fed’s hike.

For sure, there are many positive indicators for the American economy: solid GDP growth in 2014, and low unemployment and inflation rates. Consequently, the real disposable personal incomes as standards of living are rising. Indeed, the U.S. economy looks definitely brighter than a few years ago. It also performs better than many other developed countries, thanks mostly to a freer economy and a much more flexible job market.

On the other hand, if you scratch beneath the surface, the outlook for the U.S. economy is grimmer. We have already written in past editions of Gold Monitor News about rising inventories to sales ratio, decreasing new orders for durable goods, falling U.S. retail sales for three months in a row (in February) and the unemployment rate drop in February was mostly because people gave up looking for jobs. Some economists also question the accuracy of the data published by the Labor Department, and rightly so. February was another month with a huge discrepancy between the Labor Department’s job survey and the Census Bureau’s American Household Survey. According to the latter, the U.S. economy added only 96.000 new jobs in February, much below the 215.000 expected and the 295.000 reported by the Labor Department.

Why does such a discrepancy exist? There are many differences between those two reports, but the most important is that the nonfarm payroll survey does not include agricultural workers and the self-employed. It turns out that if we add those categories, the number of jobs actually fell from January to February. Please note that this fact also explains why the Labor Department’s data understate the job losses in the energy sector. The truth is that the U.S. oil and gas industries rely heavily on the use of independent contractors. Therefore, the workers in the energy sector are not counted as part of the nonfarm payroll, so layoffs in this industry are not covered in the establishment of employment statistics.

Another significant difference is that the payroll survey double-counts many workers who change jobs or have few part-time jobs. There are also other problems with the Labor Department’s statistics, such as an inaccurate model of birth and death of companies and seasonal adjustments. It is worth pointing out that the disparity between the payroll and household employment surveys is cyclical and widens during recessions, which may indicate that the U.S. recovery is based on rather fragile foundations. This is perhaps why the Federal Reserve’s labor market condition index, which combines 19 labor market indicators, actually fell from 4.8 in January to 4 in February. Does this look like a strong job market?

Other main macroeconomic indicators also do not look so rosy. First, the revised data show that GDP expanded in the fourth quarter at a 2.2 percent annual pace, down from the estimated 2.6 percent (advance estimates). Even more importantly, the Atlanta Fed’s real-time monitor of the U.S. GDP indicates that the economy has slowed considerably over the first quarter of this year. The FOMC (in its March statement) finally noticed that “economic growth has moderated somewhat.” And ‘somewhat’ means in this case the 0.3 percentage point, since the FOMC’s members downgraded its economic growth median projections for this year from 2.6-3.0 percent in December to 2.3-2.7 percent.

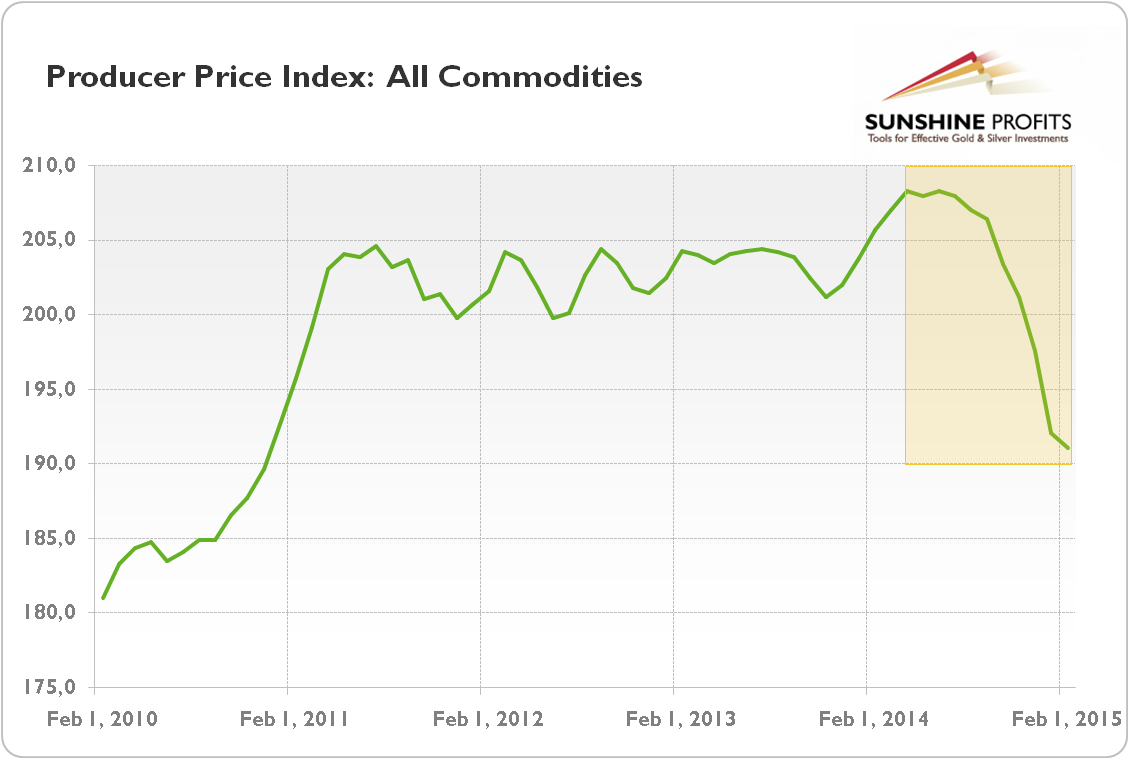

Second, the low inflation may not be transitory as Fed believes, but a sign of a coming recession. We do not consider disinflation or deflation as negative phenomena, but only when they reflect rising productivity. At present, the falling producer prices (see the chart below) signal the economic slowdown in America and globally. How else would you explain the expected fall of all nine key commodity price indices or the decline in new factory orders? No, do not blame the weather.

How does it all affect the gold market? The analysis shows that although the U.S. economy is in much better

shape compared to other countries or to itself a few years ago, the full recovery was probably proclaimed too early. It is unclear whether the Fed examines the whole spectrum of data or focuses on official statistics; however we believe that sooner rather than later it will become obvious that the U.S. economy and labor market are not as strong as the February job report suggested.

To some extent, the Fed admitted it in March, by revising its projections on economic growth (it downgraded its forecasts of the GDP growth in 2016 and 2017, which clearly shows that it is not only a harsh winter which softened the economic activity), however it increased its expectations about the employment rate.

Therefore, the Fed may slow down the hike of its interest rates (or undo it if Fed raises it eventually) even further (the U.S. central bank also cut its expectations for the level of federal funds rate over the next couple of years), which will positively affect the gold prices.

We hope you enjoyed the above article. If you’re interested in reading more, please note that we focus on the economic fundamentals in our monthly Market Overview reports and we also provide Gold & Silver Trading Alerts for traders interested more in the short-term prospects. If you’re not ready to subscribe today, please sign up for our mailing list and stay up-to-date. It’s free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair