The slowdown in retail sales growth has been a big surprise this spring, as lower gasoline pump prices were expected to boost spending. What’s going on?

Analysts at TIS Group have a fascinating if scary answer: The consumer credit cycle is breaking down as families sense the economy is slipping a gear and don’t want to over-leverage themselves. This is happening even as corporate credit continues to boom.

It’s the old story, right? If you don’t need credit, you can get it — and if you do need it, you can’t.

This distinction is important because the world is not on a typical boom-and-bust business cycle. With central banks driving much of the action, the world is instead on a credit cycle, which according to TIS means that everything depends on the availability and price of credit.

With the Fed threatening to raise rates despite a disinflationary environment, credit conditions are changing in the United States as well as in other developed countries.

The chart above, provided by TIS, shows that according to Federal Reserve data, Consumer Credit Revolving fell

sharply in February 2015 (blue circle). The analysts note you have to go back to mid-2010 and then to the dark days of the first quarter of 2009 to see readings as weak. In its commentary, the Fed has focused on consumers’ unwillingness to charge purchases.

This is not about the weather; it is about consumers’ view of the future of their jobs and wages. It can be seen as a warning that consumers are reining in their purchases and not using their windfall from lower gasoline prices in the expected way.

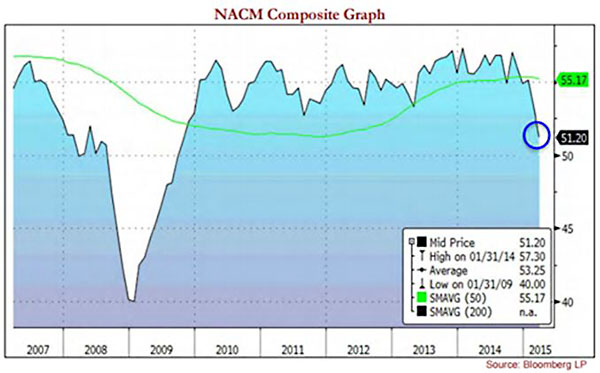

It gets worse. The National Association of Credit Managers produces a monthly report on credit conditions, and the March edition, which you can read here – and you should read it — paints an incredibly gloomy picture of current credit stresses.

This chart above shows the NACM Index Composite and appears to show a problem is developing in the credit system. This is how NACM described it in the March blog:

“We now know the readings of last month were not a fluke or some temporary aberration that could be marked off as something related to the weather. There is quite obviously some serious financial stress manifesting in the data and this does not bode well for growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound.”

TIS analysts note that in the NACM Composite, a reading below 50 signals an economic contraction is underway. The last sub-50 reading was in September 2009. So after 5.5 years, the NACM Composite is closing in on a return to contraction territory, though it is not there yet.

Looking at sub-indexes of the composite, the Service sector’s unfavorable conditions have generated a reading at 48, which signals contraction. Manufacturing was also below 50, at a 48.9 reading. So the consumer’s willingness and ability to borrow is deteriorating. And companies are also experiencing more difficulty accessing credit, the analysts observe.

This begs the big question: Why is this happening?

We need to dig deeper, and look at another NACM gauge called the Rejection of Credit Applications Index. The TIS analysts call it “a real stunner,” and it sure is. Broken down by service and manufacturing sectors, the service reading is at 42, worse than it was during the September 2008 crash. The manufacturing reading is 43.8, also below September 2008 levels. In fact, the March calculation is the largest increase in rejections of applications for credit on record.

TIS goes on to conclude that “this is what a burgeoning credit crunch looks like.” Based on this data, the notion that the Fed is even thinking about raising the price of credit — at a time it is already hard to come by — seems crazy and impossible. It might even be fair to expect the Fed would want to ease credit amid such conditions.

This is a very out-of-consensus idea and may help explain why the stock market remains stuck even as it bumps against the top of its recent range.

Corporate Bonds Rule

So what about the corporate bond market?

For this part of the story, I turn to old friend Fil Zucchi, a money manager and independent analyst in Arlington, Va., who argues that the credit managers report above is consistent with what’s been happening since 2009. “The economy basically sucks for individuals and small companies and their credit is tied to that,” he said.

But Zucchi added that if you are a large company that has access to the public debt markets or syndicated bank lines, pension funds are throwing money at you. The markets are about financial engineering, not fundamentals, these days — and the cash from large debt buyers that allows for such engineering activities like buybacks and dividend increases keeps rolling in, arguably even at an accelerated pace. Even energy credit is improving and there’ve been some very large refinancing deals in that space in the last couple of weeks.

Fil goes on to point out that first quarter corporate bond issuance was $399 billion in 2009, $429 billion in 2011, $457 billion in 2012, and was $496 billion this year.

In short, corporate debt issuance is not broken — it is blowing away all years post-financial crisis. As a point of reference, he notes that veteran credit analyst Brian Reynolds argues that an annual average issuance of approximately $100 billion per month suggests that companies are issuing debt not only to refinance maturities and for operating cash, but to also to fund buybacks.

To see how recent corporate bond issues trade in the secondary market, Fil tracks a cross-section of new bonds, trying to cover most industries and credit quality. His only filter is the size of the offering, a minimum of $750 million. The latest batch is by far the strongest seen in the past three years, he says.

Zucchi also looks at the generic Investment Grade and High Yield Credit Default Swaps indices. In a strong credit cycle, these have become the most important derivatives because they are the instruments that credit bears will attack when they want to disrupt markets.

You may recall from the financial crisis that credit default swaps, or CDS, are essentially insurance contracts for credit. They move higher when credit holders are worried and reach for more insurance, and move lower when credit holders are not worried about defaults and become increasingly complacent.

The chart above, supplied by Zucchi, shows the investment Grade Credit Default Swaps with bands that can be used as guides for when: a) bulls are firmly in control; b) things are getting agitated; and c) bears may be gaining the kind of upper hand that has been a precursor to the 2000-2002 and 2007-2009 financial debacles.

When he captured this screenshot, the IG CDX was a little bit above 65bps. Since then it has fallen lower. Fil observes that the 60 bps area has been a line in the sand for credit bears. Below that level, he says it is likely they would be forced to initiate a whole new round of short covering — an event that would likely spill over into more buying of equities.

The bottom line is that while consumer credit may be freaking out, corporate credit appears to be quite healthy. Perhaps this is just another manifestation of the difference between the 1 percent and everyone else.

Best wishes,

Jon Markman

{kind=link}