Daily Updates

Today’s Notes:

1. I am very proud to introduce the writings and thinking of my son Chris Berry in this edition. Chris will write from time to time. he has an excellent knowledge of the markets and what is happening in the global economy.

2. A most important event in the life of Quaterra Resources’ shareholders current and future. Please read this Morning Note. Goldcorp has made a major commitment to the Quaterra Team headed by Dr. Thomas Patton. The equity market is recognizing the deal this AM.

For all the ink spilled during the past 18 to 24 months regarding banking woes, there is another, perhaps more sinister problem that has been comparatively overlooked. It is becoming clear that debt on balance sheets of sovereign nations is out of control. For a few countries in particular, it’s time to pay the piper.

A case in point is Greece. The governments of both Iceland and Latvia have preceded this country in collapsing, but what is most surprising is the fact that a member of the Euro zone has followed suit– a developed rather than a developing nation is experiencing these issues for the first time. With a debt to GDP ratio of 138% and skyrocketing short-term bond yields it’s worth looking at how Greece got itself into this mess and what lessons we can learn from it.

A yawning budget deficit (forecast to rise to 12.7% of GDP in 2010) and no apparent political will to change tack, bode ill for the Greek populace and the Euro zone as a whole. EU membership guidelines stipulate that budget deficits must not exceed 3% of GDP. On our shores in the United States, with a yawning budget deficit (12.3% of GDP in 2009 and growing) and also no political will to change, are we far behind?

The title of President Obama’s FY 2010 Budget document (The Budget of the United States Government: Fiscal Year 2010),

“A New Era of Responsibility: Renewing America’s Promise” makes me cringe.

…..read more HERE.

……for the Dollar!

Quotable

“Each thing is of like form from everlasting and comes round again in its cycle.” – Marcus Aurelius

FX Trading – Rising relative yield differential is good for the dollar Last Friday I penned Growth and inflation? Key to our 10 reasons the dollar has bottomed. I hope you believe me now. One of the key points to the dollar move was “Carry trade idea history.” History we think because the Fed may surprise on the interest rate front; we expect US interest rates on the front end of the curve to exceed anything Japan has to offer soon. In that case, the Japanese yen once again inherits the carry trade mantle. It is one reason why we are bearish on the yen going forward and why our Members are positioned for such a move.

….read more HERE.

Gold $1,096

For those interested in gold, keep $100/$1000 in mind. I believe these figures are the risk/reward for gold going forward. The downside worst case scenario is $1,000 and best upside potential is $2,000.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147…..go to visit Peter’s Website.

….continued

I became bullish on gold back in March of 2003 with gold not too far away from $300. I’ve maintained an aggressive position in it albeit on a few occasions calling for a serious correction. I believe while we’re in one of those corrections, gold remains in its greatest secular bull market ever.

I truly believe I’ve managed to stay on the right side for 9+ years because of two key reasons:

I concluded a long time ago that the vast majority of people in and around the financial services community (including the media) will always be slanted against (and in many cases hate) gold because they make their livelihoods thanks to financial assets. Since gold goes against financial assets, gold itself is not their cup of tea.

Despite my enthusiasm for gold, I’m not a gold bug. I don’t sleep with it under my mattress. I don’t hold candlelight vigils around it. I don’t believe the world is ending tomorrow, next week, etc. (It can’t end until the NY Jets are in the Super Bowl again and about to score the winning touchdown). To me, it’s just another asset class that just happens to have numerous bullish fundamentals that are supported by long-term technical chart patterns.

When you realize how slanted the vast majority of people are against gold doing well and how there’s also a small but boisterous group who love it more than life itself, the better you will be when trying to figure out where gold is heading. These factors will help you grasp how biases advice on gold really is from both sides of the playing field.

Let’s cut to the chase on why I remain very bullish long-term.

….continue reading HERE.

I’ve been thinking a lot about gold lately. Especially now that Nouriel Roubini has come out and trashed the noble metal (see Tyler Durden’s article). Anyone who tells you they know what’s going to happen with gold is guessing. Roubini is guessing.

Roubini also makes some fundamental errors in his analysis, and his assumptions are flawed. Since he’s my favorite playboy economist, I should point out that he did study at the Mises Institute, but he must have cut class. He is ½ Keynesian, ½ Monetarist, and ¼ Austrian (according to Keynesian econometrics).

Ed Note: Great detailed article and charts from The Daily Capitalist

Ed Note: Great detailed article and charts from The Daily Capitalist

My conclusion, an admitted guess, is that the trend for gold is up. But … it depends on what the government and the Fed will do. The short term is a trader’s nightmare, so I don’t have a clue if it’s going up or down tomorrow. The bubble seems to be subsiding. If I were to really go out on a limb, I would guess that the fiscal stimulus bump will continue through Q1 2010, but will wear off by Q2–Q3 2010. Good GDP numbers would have negative effect on gold.

Let me explain why I think the way I think. In part it is an answer to Roubini. I could go through his report point by point, but I would rather make my own case. I don’t mean to sound pedantic, but reviewing the basics helps give perspective to the issue.

1. People want gold.

People flee to gold when they believe the future is uncertain. And you can’t tell me people like gold jewelry just because it’s pretty. It has always been that way. There is no secret to its value. People want it, it’s in short supply, you can’t make it, it’s been used as money for millennia, and, well, people want it. Accept this fact.

If you thought your paper money was going to be devalued, or worse, worthless, you’d get into some hard asset. Gold works pretty well in these situations. It’s value will be maintained while fiat money could be wallpaper. People will take anything to get rid of their paper: bread, cigarettes, candy, grenades. Whatever. Gresham’s Law.

This underlies the value of gold.

2. Fear is driving gold.

The big fear out there is that the U.S. will eventually face high inflation, perhaps hyperinflation, and sovereigns and investors who hold dollars see gold as a hedge against that event. Stability in an unstable world.

If it were all trader-driven speculation, the bubble would pop and gold would be back to $*** (pick a number). But when you have China doubling its gold reserves, and India buying tons of gold, when guys like John Paulson, Paul Tudor Jones, and David Einhorn reveal they’ve been loading up on gold, you know something is going on.

There appears to be enough demand to create a floor which would limit a collapse of the price of gold.

3. Perspective.

According to the NBER, this is my 8th cycle. My mother sold her stocks at the bottom of the 1962 cycle (down about 12%). She confided that fact to me later that year when I came home from college after starting Econ 101. She went through the Depression and was afraid. I told her we’d never have another depression: my professor told me so. That was my first cycle.

The point of the experience thing is that during almost every big cycle I’ve been through, the gold bugs came out in force and predicted dire things. Look at the ads on a lot of blogs. Check out the survivalist sites. Gold, guns, and food. Atlas Shrugged. It is not a new thing. The predictions you see today are the same as in the past. It has a big impact on (younger) people who haven’t been through a major cycle before. Everything is new in their eyes.

Also, for the most part, gold bugs always like gold. They believe the world will come to an end, soon.

Because people say it, doesn’t mean it’s so.

4. Is this cycle different?

Yes, it’s different. It’s huge.

See Carmen Reinhart and Kenneth Rogoff, This Time is Different: A Panoramic View of Eight Centuries of Financial Crises who note that cycles all act pretty much the same. What is different is that we’re going through the biggest financial-credit crisis the world has ever seen.

Fueled by cheap Fed money, rising home prices caused U.S. household debt to expand from $6 trillion in 2000 to about $14 trillion in 2007, a 233% increase. Estimates of capital losses on the balance sheets of private institutions range from $2.1 trillion (Goldman Sachs) to $3.6 trillion (Roubini). Worldwide declines in equities and real estate wiped out $28.8 trillion of global wealth in 2008 and the first half of 2009, down from a 2007 a peak of $194 trillion.

The whole world was plunged into recession because the housing boom spread world-wide, aided by central bank cheap money. The CDOs, MBSs, and CDS “insurance” were based on false risk models and spread (mainly) U.S. paper throughout the world.

This means the risks to investors are higher and grander in scope than they’ve ever been.

5. The solutions are worse than the cure.

This is the key to gold.

Fiscal stimulus:

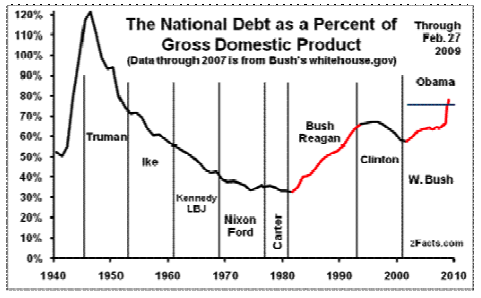

In order to finance Keynesian fiscal stimulus, national debt is now $12.1 trillion and growing (85% of GDP). The Administration recently announced that the deficit over the next 10 years will double the national debt to about $25 trillion by 2019.

This deficit spending is a waste of money, has done nothing to revive the economy, the resulting debt is a tax on our great-great grandchildren (intergenerational theft), and the interest burden will be a substantial drag on our economy.

Money supply:

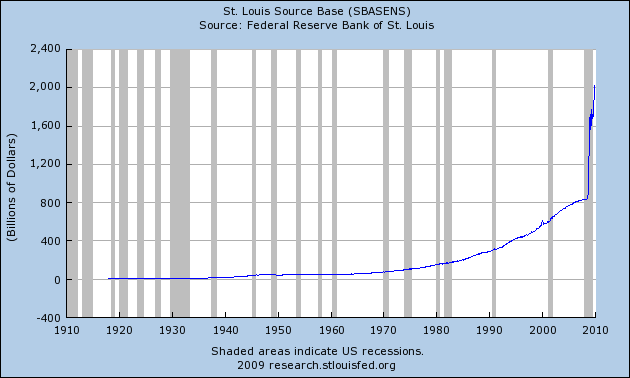

This is where folks get nervous. Money base has exploded:

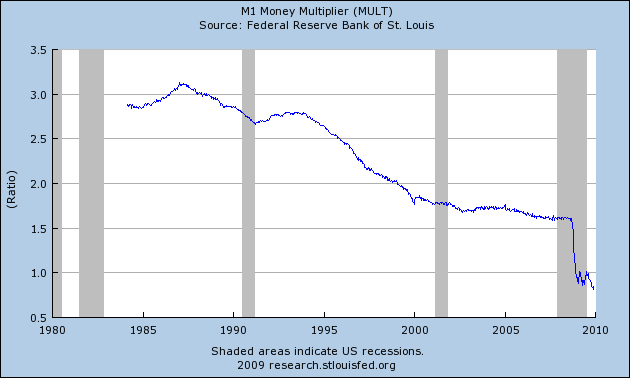

Yet, money supply, M1 for example, has dropped:

And bank reserves are very, very high:

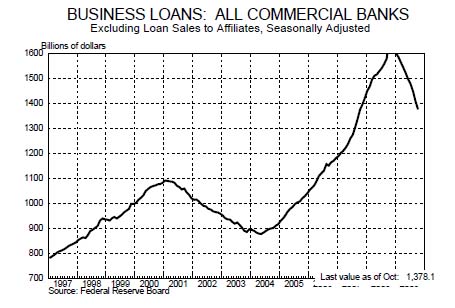

What this means is that credit has dried up. The FDIC reported that bank lending in Q3 contracted by 3%:

Banks aren’t “hoarding” according to that popular Keynesian “liquidity trap” myth. They are properly responding to the risks on their balance sheets. They aren’t going to take loan risks until their balance sheets are stable. Think not only of the bad residential mortgages and subprime paper, but the huge amount of commercial real estate held by small and regional banks–which banks are the lifeblood of most businesses.

Obama can jaw the “fat cats” all he wants, but he can’t make them lend. If he can, watch out.

Exit strategy:

The reason gold is in demand is because gold buyers doubt the Fed’s exit strategy. That is, when banks are healthy, they will lend. They will have access to all that money and credit the Fed has created, and, considering how much was created, it will lead to high inflation. Some people say hyperinflation.

The Fed says they can sop up the funds by raising the Fed Funds rate and increasing banks’ Tier 1 capital reserves. Let’s say they do that and the recovery collapses because of tighter credit, higher interest rates, and the like. Mortgage rates will go up, credit is tight, and Congress screams. You think the Fed is independent? Don’t bet on that.

What about the Fed paying interest on banks’ reserves? The theory is that banks would rather get interest on a safe “loan” of their reserves to the Fed, than make a “risky” loan to the public. That won’t work. Doing this will make it impossible for the Fed to maintain its target interest rate. Also, banks don’t keep customers if they don’t lend, so they will. Please see this article for a thorough explanation of this.

Higher interest rates will stop inflation. Will Bernanke do this? It worked for Volker. If he doesn’t, we’ll have inflation.

6. The dollar.

The decline of the dollar is an intentional yet unofficial policy of the Obama Administration to pull us out of the recession. I don’t know why they believe this, because, while it will stimulate U.S. exports, it will kill businesses which are based on imports.

We’ve been running trade deficits for many years before this crisis, yet the economy expanded and jobs increased rather than decreased. One can clearly conclude from the data that when GDP expands, imports increase. Conversely they shrink during a contraction. It’s been this way for at least 30 years.

Right now, the current account is more “balanced” in that exports have been rising. That has everything to do with the recession–people are buying less. In economic terms, letting the dollar fall in order to boost exports is just old fashioned mercantilism. It was proven wrong with the introduction of free trade.

The result: we all pay more for imported goods, which, these days, is just about everything. The offset in exports won’t be enough to stimulate consumer spending. See, “Economic Megatrends That Will Drive Our Future.”

Don’t expect the Fed or the Treasury to halt the dollar’s decline anytime soon. High inflation will be a big negative for the dollar and a positive for gold.

7. Why did gold go up?

I was hoping this wasn’t as obvious a question as it seems.

The dollar is going down is a more accurate way to put it. That has the most to do with gold’s rise. Here’s a chart of the dollar (DXY):

You will notice from the chart that during the initial stages of the crisis, people flocked to the dollar which shows that it is still the world’s reserve currency, especially during a crisis. But after that, it’s been a slide.

Reason No. 1:

Check out this recent article from the Financial Times:

One factor supporting [gold] prices is the change in attitude by central banks, some of which see buying gold as a way to diversify from the dollar and their holdings of US Treasuries. For many years, central banks were net sellers of gold. Not any more – earlier this year it emerged that Chinese gold reserves had almost doubled. …

There has been speculation this week that China could snap up the remaining 203 tonnes of IMF gold. Brazil has also been touted as a potential buyer.

Michael Lewis, commodities strategist at Deutsche Bank, notes that the majority of central banks banks in the developing world have less than 10 per cent of their reserves in gold.

Mr Lewis combines this list with large holders of US Treasuries who have a strong incentive to diversify into gold given the “non-negligible risk of a US debt and currency crisis”.

China, Japan, Russia, Taiwan, India, Singapore, Brazil and Korea are strong potential candidates to increase their bullion holdings, he says. “We expect central banks, in aggregate, to be net buyers of gold over the coming year for the first time since 1998.”

Reason No. 2:

Private buyers of gold or gold related assets such as GLD and gold futures are the second reason for gold going up. See above about Paulson, Jones, and Einhorn. Lots of buyers in China and Asia.

Reason No. 3:

Speculation. As I said, I have no idea what will happen tomorrow. Note that the dollar rose in December and gold declined.

8. Does the deficit matter?

Foreign buyers finance 30% of our debt. We sell our debt to China, Japan, and the U.K. China holds $1.521 trillion of our debt.

Big exporters like China and Japan can’t do much about their holdings without cutting off an arm or two. They know they are stuck. They’ll grab their ankles and keep buying our debt, perhaps demanding more TIPs. I think the Chinese really believe in the Fed’s exit strategy. But … they are still buying gold as a hedge.

U.S. banks have been investing their reserves in Treasuries. Also, because U.S. consumers are increasing their savings, private holding of Treasuries have also increased. And, it appears the Fed and Treasury have been monetizing some of the debt.

This is why T-rates have been low.

Deficits affect gold only in the long term. I don’t think holders of dollars will not buy our paper. Assume China and Japan cut back on funding our deficit. What will happen? Investors will demand higher returns, interest rates will go up, paper will be sold, and the ultimate tax burden will slow down the economy.

It is printing money and easy credit which causes inflation, drives the dollar down, and causes gold’s rise.

9. Gold will go higher–eventually.

It’s all about inflation and world stability.

Black Swan:

By definition you can’t see the next world-changing negative Black Swan event coming. I’m leaving an economic crash out of this part of the discussion. Volcano. Nuclear terrorism. Iran. Comet. Pakistan. Take your pick. These events create world instability and people run for safety.

These are the reasons you buy some gold anyway. Taleb is completely right on investment strategy. Be conservative on 80% to 90% and bet the farm on the rest. Gold is safety.

Deflation:

It’s not over. This is a controversial issue, but as long as real estate assets fall in value, we won’t see much inflation. I didn’t say “any” inflation, just not much as long as real estate keeps dragging banks down, causing credit to remain tight.

I’ve addressed the continuing problems with housing recently; if you need more on this see “Why The Housing Market Is In Trouble.”

Commercial real estate is as bad. The Administration has adopted a policy of “extend and pretend” for banks with CRE debt. If you can show that you will eventually be able to amortize the loan at least to even when things get better, banks can extend the loan, reduce interest, or whatever it takes.

While many analysts see this as a positive, it isn’t. It is just another way to ignore reality like suspending mark-to-market. This will drag out the recovery as banks are still burdened with make believe debt on their books. More uncertainty for lenders will keep them tight fisted.

This could last several more years. But the government has other ideas about real estate that could shorten deflation: reignite the bubble.

Inflation:

Since I don’t believe the Fed can save us from themselves, I don’t know why we won’t have inflation.

Because the economy will remain sluggish due to the continuing credit contraction noted above, the Fed will keep pumping new money to thwart a “relapse” of the economy. I think inflation will eventually take hold in 2011 because the Administration will reflate the real estate bubble. And that will repair a lot of bank balance sheets. Real estate can be reflated by means other than monetary policy (FNMA, FHMA. FHA, GNMA, and tax policy).

I think inflation will last for some time because it benefits debtors, including the federal government, and will allow them to pay down debt with cheap dollars. The perception of a recovering economy will carry the Democrats and President Obama to victory in 2012. So you will see inflation well into Obama’s second term. Oh, yes, he’ll be re-elected. FDR made the Depression worse yet he was re-elected, so why not Obama. The odds are heavily in favor of incumbents.

So Ben won’t have to muster his courage to raise rates until 2013.

Inflation will drive down the dollar and gold will go up.

Hyperinflation:

Everyone, Austrian, Keynesian, Monetarist, and Marxist knows what causes hyperinflation and no one will let it happen.

Hyperinflation is a popular theme with gold bugs, but I don’t buy it. Hyperinflation is far worse than a recession and Ben, Larry, and Timmy know that.

Let me give you another scenario. When inflation really gets high, say to Jimmy Carter levels (13±%) or higher, we will see a temporary implementation of price and wage controls, as in Carter and Nixon. Since everyone also knows these don’t work, it will just be a smokescreen to allow Bernanke to raise interest rates until inflation comes under control.

10. Remember, this is a guess.

These are the guide posts we should keep watching in order to protect our investments. As I said at the beginning, it all depends on what the government and the Fed do. I’m not going to tell you what to do because I don’t give investment advice. But my analysis points to an increase in gold over the long term because I think a continued dollar decline is inevitable. Gold is a favored hedge against this.

*Disclosure: I am not selling you anything. I don’t want to manage your money. I’m not giving you investment advice. I am peripherally involved in the gold mining business, but if you run out and buy gold it won’t affect me. So, I have nothing to gain by this article. Keep that in mind when you research those selling gold investments.

About The Daily Capitalist

This blog comments on economics, politics, and finance from a free market perspective. We try to present ideas the reader would not find in contemporary media. In addition to the founder of the Classical School of economics, Adam Smith, our influences are from the Austrian school of economics. Among its leading thinkers have been Ludwig von Mises and Friedrich von Hayek. There are many practitioners of this school today and some of their blogs are shown on the blogroll. We trace our political philosophy back to Edmund Burke, David Hume, John Locke, and Thomas Jefferson, to name a few.

Our goal is to challenge contemporary thinking, mainly from those who promote Keynesian economics (almost everyone) and those who rely on statist solutions to problems.

We also have an interest in investments and finance, and specifically investment risk and the role of the business cycle.

We don’t consider ourselves Democrats or Republicans, right wing or left wing. We’re on the freedom wing.

We also publish articles in Zero Hedge, Noozhawk.com, and The Montecito Journal.

We hope you enjoy our commentary, and please join in the discussion.

About Jeff Harding

Jeff Harding is a real estate investor and former lawyer in Santa Barbara, California. He is a principal of Montecito Realty Investors, LLC. He has many years of experience in business cycles related to real estate investments and finance. He also was financing director of a home builder. Also, he wrote the great American unpublished novel several years ago.

If you wish to engage Jeff Harding to speak at your function, please contact him:

To contact Jeff Harding: econophile@dailycapitalist.com

People often associate “big” with “safe.” They think big ships are safer than small boats. Big banks are safer than small banks. Big stocks are safer than small stocks.

Of course, it doesn’t always work out that way … the gigantic Titanic turned out to be quite a bit more dangerous than the Skipper’s S.S. Minnow. And on average, you are much safer aboard a small plane than you are in your supersize SUV.

Nonetheless, stock investors who want to apply the “Big = Safe” principle often lean toward “mega-cap” stocks. These are the largest of the large — big companies that are often household names because they’re everywhere. Think of stocks such as …

ExxonMobil (XOM)

Coca-Cola (KO)

AT&T (T)

Microsoft (MSFT)

Procter & Gamble (PG)

You’ve probably spent money with all these companies — one way or the other. And most people find it hard to remember a time when they didn’t exist!

Many of the largest foreign companies are also familiar names. In fact, many have a significant, or even a dominant, market share with U.S. consumers. Examples include …

Nestle

Bayer

BP

Toyota

Canon

Like mountains and valleys, mega-cap stocks are simply part of the landscape. They’re the bedrock — the foundation on which smaller things are built.

This quality gives mega-cap stocks an extra value. For instance, ExxonMobil isn’t worth as much as it is just because it represents oil in the ground … its shares fetch a premium price for no reason other than being ExxonMobil.

Is this fair to smaller companies? No, it’s not. But I could argue that mega-caps have a handicap, too. After all, they cannot grow as fast as small-cap stocks because they are simply too big.

The point is that mega-caps are a category of their own.

ETFs Cover the Mega-Caps …

Exchange traded fund (ETF) sponsors want to cover every possible investment niche, so they’ve created a number of mega-cap funds. Here’s an overview for you.

To start off with, I think investors should always take a global approach to their investing. But if you’ve been reluctant to invest internationally, these first two ETFs might help you take a step in that direction since most of the foreign holdings will be names you are already familiar with:

SPDR DJ Global Titans (DGT) typically holds the 50 largest stocks from around the world. The “smallest” holding is Nokia, the cell phone giant located in Finland. Stocks from the U.S. comprise about 60 percent of these global titans, while the U.K., Switzerland, and France are the next largest of the 12 countries represented.

iShares S&P Global 100 Index Fund (IOO) is similar to DGT in that it takes a global approach to mega-cap stocks. The major difference is that it holds twice as many stocks. This approach brings the U.S. weighting down to about 43 percent of the fund. The “smallest” stock in IOO is Philips Electronics of the Netherlands.

However, if you prefer to focus just on the U.S., there are numerous mega-cap ETFs to choose from:

Rydex Russell Top 50 ETF (XLG) holds the largest U.S. listed stocks. And even though it consists of only 50 stocks, it represents nearly 40 percent of the total market cap of the U.S. stock market.

DIAMONDS Trust (DIA) consists of 30 blue-chip stocks in one ETF, but they are not just any 30 stocks. They are the same ones that make up the Dow Jones Industrial Average, the most well-known stock market index in the world.

iShares S&P 100 Index Fund (OEF) is another way to capture many of the largest U.S. listed companies with an ETF. As its name suggests, OEF consists of the 100 largest stocks that make up the famous S&P 500 index.

There are also two “families” of mega-cap ETFs …

You may be familiar with the nine-square style box from Morningstar that divides the market into three capitalization segments (large, mid, and small) and three valuation segments (value, blend, and growth). Well, think of these mega-cap families as adding another row across the top of that matrix:

Vanguard Mega Cap 300 Index ETF (MGC) is based on the largest 300 U.S. listed stocks. This group is then further divided into ETFs representing value (MGV) and growth (MGK).

iShares Russell Top 200 Index Fund (IWL) is a relatively new offering focused on the largest 200 U.S. listed stocks. This group is then further divided into ETFs representing value (IWX) and growth (IWY).

In the interest of completeness, I’m going to tell you about a few other mega-cap ETFs:

iShares NYSE 100 Index (NY) simply consists of the largest 100 stocks listed on the New York Stock Exchange.

SPDR DJ STOXX 50 ETF (FEU) holds the 50 largest stocks in the pan-European Dow Jones STOXX Total Market Index.

PowerShares Active MegaCap (PMA) takes an “active” approach to mega-cap investing while all the others listed above are index-based ETFs. The managers of PMA attempt to pick the 40 or so stocks they think will do best from the Russell Top 200 Index.

One of the characteristics of my favorite ETFs is their ability to provide access to various segments of the market. So when you want a stake in the largest stocks in the world — the mega-cap stocks — consider the ETFs outlined above.

Best wishes,

Ron

P.S. I’m now on Twitter. You can follow me at http://www.twitter.com/ron_rowland for frequent updates, personal insights and observations about the world of ETFs.

If you don’t have a Twitter account, sign up today at http://www.twitter.com/signup and then click on the ‘Follow’ button from http://www.twitter.com/ron_rowland to receive updates on either your cell phone or Twitter page.

Ron Rowland is president and a founder of Capital Cities Asset Management. Mr. Rowland is widely regarded as a leading ETF and mutual fund advisor as well as a sector rotation strategist. In addition to his roles of President and Chief Investment Officer of CCAM, he is Executive Editor and Publisher of the All Star Fund Trader, a highly regarded investment newsletter in its 18th year of publication.

You may have read about Mr. Rowland and his strategies in publications such as The Wall Street Journal, The New York Times, Investor’s Business Daily, Forbes.com, Barron’s, Hulbert Financial Digest and many more. Outside of CCAM, Mr. Rowland served on the Executive Committee of Austin’s American Association of Individuals Investors (AAII) and led the mutual fund special interest group for numerous years.

As a former mutual fund manager from 2000 to 2002, Ron was a pioneer in using ETFs inside of mutual funds. He also served as the manager of a hedge fund from Aug. ‘93 to Dec. ‘94. His formal education includes a BS in Electrical and Computer Engineering from the University of Cincinnati in 1978 with additional studies in the same field at the University of Texas from 1978-1981.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair