Daily Updates

This small excerpt was from Mark Leibovit’s 12 page The VR Gold LetterThe VR Letter is published WEEKLY and Mark Leibvit has been the Awarded #1 Gold Timer by Timers Digest in 2007, 2008 and is in postition to win 2009 with his fine Gold forecasts throughout the year so far. Money Talks highly recommends subscribing to Mark’s VR Gold Letter.

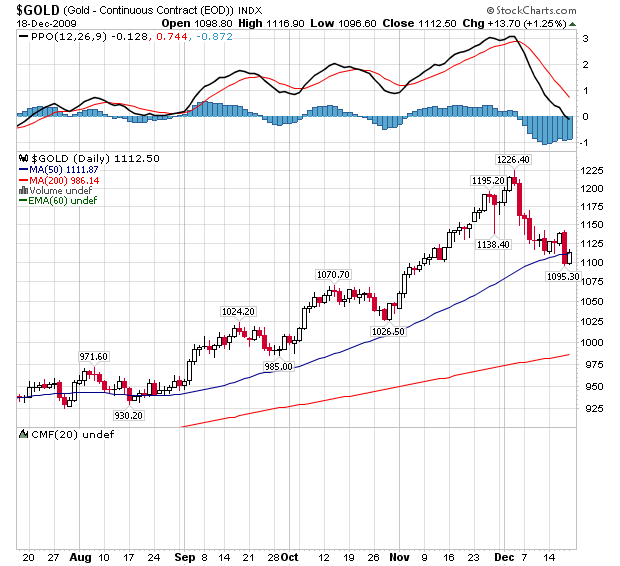

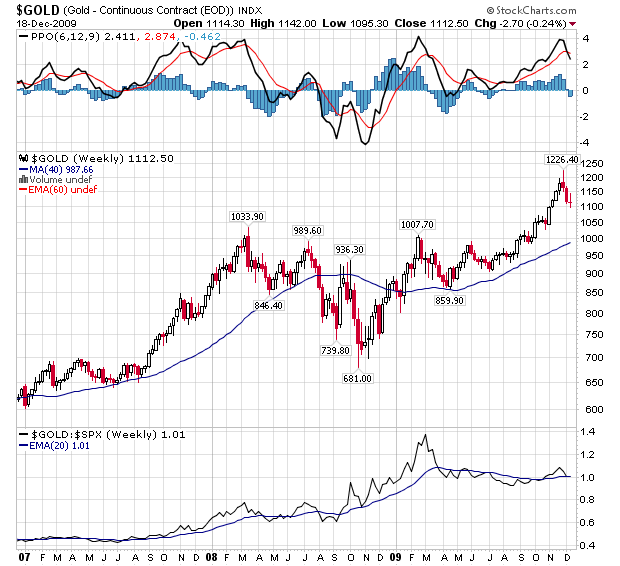

Gold continued south this week still responding to my December 3 ‘Sell’ signal. My Annual Forecast Model (AFM) constructed nearly 12 months ago (depicted below) correctly called the major move in Gold this year. Hopefully, future years continue to perform even half as well.

Though the decline has been sharp and swift – usually a characteristic of bull market corrections – there is presently little confirmation that a bottom is in place. Of course, this could change quickly, so we will keep you posted either herein via a Bulletin or within my commentary at VRtrader.com.

The bottom line, folks, is that the party is only beginning for Gold. Seeing 1500 or 1600 in the next twelve months is a very reasonable expectation. I am still on record for my prediction for $3000+ Gold which I’ve been making on PBS’ Nightly Business Report program for several years. Frankly, I wouldn’t be surprised if that forecast is conservative. I feel the next big market ‘bubble’ could be in Gold, just as we saw bubbles in internet stocks and real estate in prior years. I do not accept the fact that everyone is in Gold and that bullish sentiment currently defines a major long-term peak. We’re in a 20 year ‘up cycle’ which conceivably could carry well into the year 2020. If we top out before that, so be it, but for now keep the faith. Manipulative forces are quite strong and there are rumors minute to minute in this market. Central governments do not wish to see Gold strong because it reflects on their gross ineptitude, but these same governments are now beginning to recognize that without Gold they will not have a medium of exchange to conduct trade going forward as the debauchery of the currencies themselves is occurring right before their eyes. As you know, there are strong indications that the European Union may itself break apart ceiling the fate of the Euro. Other ‘wrenches’ in the works include rumors of phony tungsten Gold bars showing up in various locations around the world, possibly originating in China. If you want read more about the tungsten rumors, Google it. If true, this could cause havoc in the Gold market, as more and more investors will begin to seek physical delivery to protect themselves. We live in interesting times.”

All Charts below posted by MoneyTalks

This small excerpt was from Mark Leibovit’s 12 page The VR Gold LetterThe VR Letter is published WEEKLY and Mark Leibvit has been the Awarded #1 Gold Timer by Timers Digest in 2007, 2008 and is in postition to win 2009 with his fine Gold forecasts throughout the year so far including Gold zooming to another new High of $1,131 in tonights overnight trading. Money Talks highly recommends subscribing to Mark’s Gold

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

Market Buzz – The Investor’s Christmas

‘Twas the night before Christmas, and all through the brokerage house,

Not a trader was stirring, not even Madoff that louse;

All portfolios repositioned by the advisors with care,

In hopes that the strong rally would continue to be there;

The clients were restful, snuggled tight in their beds,

While visions of ten-baggers danced in their heads;

And mamma with her calculator, and I in my cap,

Had just looked at our statement, no longer a piece of crap,

When there on the TV there arose such a clatter,

I sprang from my calculations to see whom I could batter.

Away to the set I flew like a flash,

Stepped on a skateboard and tripped over the trash.

The reporters on CNBC so cheery and upbeat,

Made me sick to the stomach as I fell from my feet,

When, what to my half-glazed eyes should appear,

But U.S. Treasury Secretary Geithner, and eight empty beer,

With a swig and a wink, so lively and quick,

I thought for a moment, “Who was this young prick?”

More rapid than eagles, his bailouts they came,

As he trumpeted, and boasted, and called them by name;

“For, Bear Stearns! For, AIG! Cash for clunkers and more!

On, GM! On Chrysler! But nothing for Ford!

To the top of the index! This liquidity’s a ball!

Now rally away! Rally away! Rally away all!”

And I heard him exclaim, ere he drove out of sight,

“PROFITABLE INVESTING KEYSTONE CLIENTS, AND TO ALL A GOOD-NIGHT”

Looniversity – The Santa Clause Rally & January Effect

The oft-spoken-of Santa Claus Rally refers to a surge in the price of stocks that can occur in the week between Christmas and New Year’s. There are numerous explanations for this phenomenon, including tax considerations, a generally jovial mood around Wall Street (Christmas bonuses), and the fact that the pessimists are usually on vacation this week.

Many consider the Santa Claus Rally to be a result of people buying stocks in anticipation a rise in stock prices during the month of January, otherwise known as the January Effect, which many postulate is the result of excessive tax-loss selling up until Christmas Eve.

For its part, the “January Effect” is a tendency of the stock market to rise between December 31 and the end of the first week in January. The January Effect occurs because many investors choose to sell some of their stock before the end of the year (early to mid December) in order to claim a capital loss for tax purposes. Once the tax calendar rolls over to a new year on January 1st these same investors quickly reinvest their money in the market, causing stock prices to rise. Although the January Effect has been observed numerous times throughout history, it is difficult for investors to profit from it since the market, as a whole, expects it to happen and therefore adjusts its prices accordingly.

Put it to Us?

Q. My discount brokerage offers a “DRIP” program. Does this differ from traditional DRIPs offered by the companies themselves and how does it work?

– Ronald Mah; Calgary, Alberta

A. Many discount brokerages now offer their own “quasi DRIP programs”. Under these plans, your broker automatically reinvests dividends from eligible companies in new shares. Rather than incur a full commission, you are charged a minimal fee ($1.00 – $3.00). Essentially, this method eliminates the need for you to register and store your own certificate, making the process more convenient.

For those new to the wonderful world of DRIP investing, a brief explanation is in order. With DRIPs, the dividends that an investor receives from a company (stock) go toward the purchase of more stocks, making the investment in the company grow little by little.

The “dripping” of dividends is not limited to whole shares, which makes these plans somewhat unique. The corporation keeps detailed records of share ownership percentages. For example, if ABC Big Co. paid a $1 dividend on a stock that traded at $10, every time there was a dividend payment, investors with the DRIP plan would receive 1/10 of a share in ABC Big Co. Another feature that makes DRIPs popular is that there are no commissions or brokerage fees involved because the investor deals directly with the company.

KeyStone’s Latest Reports Section (must be a premium member)

- Canadian Small-Cap with Dominant Position in a Fragmented Market Ripe for Consolidation, Trading with Solid Fundamentals – Slow & Steady (New Buy Report)

- Strong Q1 2010 Revenue Growth, Aggressive Growth Plan, & Attractive Valuations Allow Us to Maintain Our BUY Rating on Alternative Financial Services Provider Despite 40% Plus Gain in 4 Months (Flash Update)

- Emerging Australian Alternative Financial Stock Posts Encouraging Q1, Narrowing Losses on 200%+ Increase in Revenues – Maintain Rating (Flash Update)

- China-based Organic Fertilizer Producer Posts Strong Q2, Graduates to NASDAQ & Sets Stage for Growth Phase – Rating Upgraded (Flash Update)

- Profit Taking in Order for our Top Canadian Wireless Software Pick After Shares Jump over 250% in 2009 – SELL HALF (Flash Update)

KeyStone -Why Subscribe?

- First coverage on high growth, profitable stocks, trading at low prices

- Independent and updated BUY/SELL/HOLD Stock Reports

- Unsurpassed 9-year track record of uncovering great small caps with strong fundamentals

- About Keystone Financial HERE – Go HERE to subscribe

It’s All About Deleveraging

Commercial Woes

The Lights Of Myanmar

A Lively 2010 and Buying Stocks

This is the season when pundits feel compelled to make annual forecasts. I will make mine, as I traditionally do, in the first letter of January. But already we have seen a wide range of forecasted outcomes. Are we going to grow at 5-6% or at 1-2% or dip back into recession? Why such disparity? I think part of the reason is a basic disagreement on the nature of the just-lapsed recession. Today we explore that issue. Then I point you to a way to help those who are desperately in need and only wish they had our problems. For those interested, I enclose a picture of my new granddaughter.

And finally, I start the process of getting ready, after ten years, to actually buy some stocks. Yes, it is true. Am I throwing in the towel and becoming a bull, or do I just see an opportunity? Stay tuned.

It’s All About Deleveraging

I did a very interesting one-hour show this week with Tom Ashbrook on his National Public Radio syndicated radio show called On Point. About 20 minutes into the show, Professor Jeremy Siegel of Wharton came on, and we had a pleasant debate and lively Q and A with listeners. Jeremy of course was the bull, expecting that next year the US will grow by 5-6%. I was the “bear,” expecting growth in the 1-2% range. You can listen in at http://www.onpointradio.org/2009/12/an-economic-warning. It’s also available as a podcast on iTunes (“On Point with Tom Ashbrook”) for a few more days.

I have liked Jeremy the times we have been on the same platform, and we have traded emails over the past few years. He is a consummate gentleman. He is also the author of Stocks for the Long Run. His thesis is buy and hold. Long-time readers know that I find such thinking to be wrong, if not dangerous. I believe that stocks go in long cycles (an average of 17 years) based on valuations, and that we are still in a long-term secular bear phase. I want to see valuations come way down before I suggest that the index-investing waters are once again safe. That day will come. Just not for a while.

In the meantime, Jeremy has given us the reason for his very bullish call. Paraphrasing, he said, “Look at past recoveries from recessions. They were always strong in the first year. Suggesting 5-6% is not all that aggressive.”

And I would agree with him – if the past recession was a typical recession. But we have just gone through a recession that was unlike any other we have experienced since the Great Depression. Typical recessions are inventory-adjustment recessions, caused by businesses getting too optimistic about sales and then having to adjust. You get temporarily higher levels of unemployment as inventories drop, and then you get the rebound. It is not quite as simple as that, but close enough for this letter’s purpose.

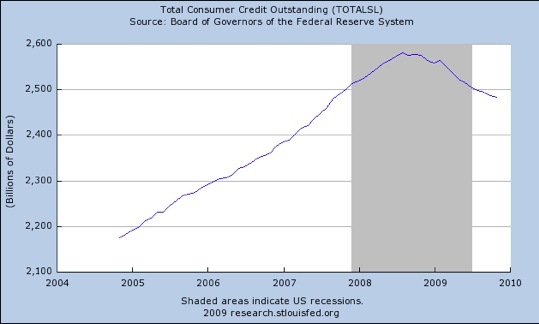

This recession was caused not by too much inventory but by too much credit and leverage in the system. And now we are in the process of deleveraging. It is a process that is nowhere near complete. While the crisis stage is over (at least for now), there is still a lot of debt to be retired on the consumer side of the equation, and a lot of debt to be written off on the financial-system side. And this is true in Europe as well, and maybe more so; but today we will look at some data in the US.

Total consumer debt is shrinking for the first time on 60 years. And the decline shows no sign of abating.

Credit card companies have reduced available credit by $1.6 trillion dollars. And for good reason. My friend and London partner Niels Jensen sent me the following charts from UrbanDigs.com. Credit card delinquencies are hovering near all-time highs. Bank charge-offs for credit cards are going to rise as the unemployment numbers get worse:

…..read more HERE.

Treasuries, Treasuries Everywhere, but Not an Aggressive Bidder to Bid

The holiday season is here — and in just a couple of weeks, 2009 will fade into the history books. I truly hope that you and your family enjoy these happy times.

But before I sign off for the year, I feel obligated to address one of the biggest threats to your wealth that’s looming in 2010. I’m talking about the very real prospect of “failed” Treasury auctions, plunging bond prices, and a big spike in long-term interest rates.

We touched on this issue briefly a week ago. But this time, we’re really going to get our hands dirty!

The Warning Signs Are There.

Please Don’t Ignore Them!

Each and every week, the U.S. government sells Treasuries to fund its operations. Four-week bills. Three-month bills. Six-month bills. One-month bills. Two-, 3-, 5-, 7-, and 10-year notes. And of course, the granddaddy of them all, the 30-year Treasury Bond.

The Treasury auctions offer those securities to all kinds of bidders — individual investors, banks, insurers, pension funds, mutual funds, and foreign central banks are among them.

The more aggressive the bidding, the lower the yields Treasury has to pay on the securities it sells. And the lower the yields, the lower the U.S. government’s financing costs.

For a while, the Treasury Department was able to sell almost anything and everything at rock-bottom yields. It didn’t matter if it was the shortest of short-term bills or the longest of long-term bonds. Investors were willing to pay up. That helped keep our cost of borrowing low and underwrote the massive deficit with little-to-no financial pain.

But now that’s starting to change.

Slowly but surely, investors are beginning to appreciate the seriousness of the dangers we highlighted many months ago. All the mega-bailouts … all the Fed money-printing … all the fiscal recklessness being practiced by both Democrats and Republicans alike are starting to spook bond market players.

Sure, they’re still buying very short-term Treasuries like mad. It’s not like the government is going to default tomorrow, or that inflation is going to surge overnight. But auctions of 10-year and 30-year bonds are getting progressively worse, with demand dropping as supply ramps up …

Weak Auctions a Prelude to Failed Ones?

One key measure of auction strength is the “bid-to-cover ratio.” This measures the dollar volume of bids versus the volume of Treasuries being sold. The higher the number, the more demand you have relative to supply.

At the last 30-year bond auction, held on December 10, the bid-to-cover ratio came in at 2.45. That was substantially below the recent peak of 2.92. The 10-year note auction, held one day prior, registered a ratio of 2.62. That too was sharply below the recent high of 3.28.

Another way to gauge auction strength is to see who’s doing the buying …

The number of central banks buying

Treasuries has declined drastically.

If you have a high percentage of notes and bonds going to so-called “indirect bidders,” you can breathe a sigh of relief. That’s because important buyers like foreign central banks fall into that category, and we desperately need them to step up to the plate to keep rates low.

Unfortunately, the numbers don’t look good there, either. Indirect bidders only took down 40.2 percent of the 30-year bonds sold in mid-December. That was down from the 2009 peak of 50.2 percent in July. Their share in the 10-year auction was even worse — just 34.9 percent. As recently as September, indirect bidders were snapping up 55.3 percent of the notes being sold.

Bottom line: Long-term Treasury auctions are getting weaker and weaker.

We haven’t seen a so-called “failed” auction yet. That’s when the bid-to-cover ratio drops below 1 — meaning the government can’t even get $1 in bids for every $1 in securities being sold. But that has already happened in the U.K., and I believe it’s only a matter of time before it happens here.

Defensive Measures to Take …

If you’re a defensive investor, your course of action is simple: Avoid long-term Treasury debt. Don’t put in bids for long-term notes and bonds via the Treasury Direct system or through your broker, and consider selling whatever long-term holdings you already own.

That strategy is one I’ve been advocating for a long time. And boy do I hope you’ve been listening! Just consider this: If you purchased the iShares Barclays 20+ Year Treasury Bond Fund (TLT), an exchange traded fund (ETF) that owns long-term Treasuries, at the end of 2008, you would have already lost more than 20.5 percent! That INCLUDES interest payments, by the way.

As a matter of fact, 2009 has been the absolute WORST year for total return on long-term Treasuries since at least 1973. That includes dismal years such as 1994 and 1999, which occurred during Fed rate-hiking cycles.

Until next time,

Mike

Mike Larsen: Among the first analysts to call the housing slide, Mr. Larson’s policy paper, “How Federal Regulators, Lenders and Wall Street Created America’s Housing Crisis: Nine Proposals for a Long-Term Recovery,” received broad media coverage following its July 2007 submission to the Federal Reserve and FDIC. In the paper, Mr. Larson accurately predicted the long-term impact of the deepening subprime mortgage crisis on the broader economy that the nation faces today.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

As the first decade of the new millennium rapidly comes to a close, today’s chart takes a look back at the decade that was. Today’s chart begins shortly after the stock market as well as the nation was partying like it’s 1999 (i.e. dot-com boom). The proverbial punch bowl was taken away early in 2000 and the Nasdaq suffered its 2 1/2 year dot-com bust. The market eventually bottomed and began a five-year rally thanks in part some infamous financial innovations (i.e. Ninja loans — No Income, No Job, and no Assets). Then as it became apparent that those financial innovations weren’t quite as innovative as first hoped, the system went into near meltdown. Over the past nine months, the Nasdaq has been rallying (albeit at a pace that is slowing over time) and is currently testing resistance. All in all, a tough decade.

Sign up for FREE ChartoftheDay HERE or at http://www.chartoftheday.com/

Rogers Turns On A Dime

Or more accurately, on the dollar. Guess what he thinks of sterling!

Yes, Jim Rogers has been doing the interview rounds again, having extended interviews with Bloomberg and CNBC in particular, and he’s as outspoken and entertaining as ever.

And what has surprised many is the fact that he’s expecting a short-term surge in the dollar. His thinking is contrarian: He’s seeing everyone taking a shot at the dollar and deciding it must be time to buy. “Everybody’s short the dollar right now.” Claiming, as always, to be the world’s worst trader, he has been accumulating dollars recently.

But don’t for a moment think he’s gone soft on the issues facing the US. He sees the rally lasting for three to 12 months, but long term he still regards the dollar as doomed. He is particularly scathing of at Treasury Secretary, Tim Geithner, and his attempts to solve a debt- and consumption-fueled problem with more debt and more consumption.

In classic Rogers style he says “that’s like saying to Tiger Woods ‘you get another girlfriend and you’ll solve your problems’, or ‘five more girlfriends and you’ll solve your problems'”!

Sterling under pressure

But before you start feeling too comfortable, Rogers is extremely bearish about sterling. The former business partner of George Soros (who famously speculated against sterling during the 1992 crisis), says that for the first time in over thirty years he doesn’t have any sterling investments.

“The UK is not going to keep its AAA rating — I don’t know why it has one still … The Prime Minister there has been ruining things. It grieves me to see what’s happening in the UK.”

He expects 2010 to be a year of currency crises, and puts Britain in the same league as Argentina and Ukraine as regards countries that will suffer.

Gold

Gold, which many consider a currency more than a commodity, may also see a correction, but only short term. At some stage over the next decade he expects to see it hit $2,000 per ounce. He owns gold, but if it gets to $2,000 already in 2010 he’d be a seller; if it drops below $1,000, he says, “I hope that I’m smart enough to buy more”.

Commodities

Having said that, he prefers silver, which is 70% off its all-time high, and also palladium. The commodity guru would not be surprised to see some short-term correction in the oil price, but maintains his long-term bullish position on commodities in general.

He is particularly keen on agricultural commodities at the moment, and says “inventories of food are the lowest they’ve been in decades”.

The next bubble?

Despite some gloomy predictions, Rogers has no short positions at present, and that’s extremely unusual for him. The next bubble he expects to see is in long-term US government bonds, and he expects to be taking a short position on those. “Would you lend money to the US government for thirty years at 4% or 5%, and in US dollars?”

While he always issues health warnings with his predictions, Rogers is always worth listening to.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair