Daily Updates

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147…..go to visit Peter’s Website.

The Dollar, Gold, X-Mas and Happy New Year

Barring something unforeseen that can’t wait until January 4th to comment on, this will be my last market commentary of 2009.

Despite knowing year-end market conditions can and will cause markets to move more than normal, I’m going to remove my hold on gold and silver bullion (updated model portfolio) and suggest it’s okay to start easing one’s self back into the water again. While I still believe significant physical bullion buying is not likely to return until we’re closer to the area where India stepped up and bought some IMF gold (about $30 lower from here), the surprises for the most part in gold for almost eight years has been to the upside.

Knowing the “masses” are currently fixated on the U.S. Dollar at the moment (and the gold perma-bears, who have been spanked around and left for dead from $400 and up are all on their knees praying to the dollar gods to somehow drive gold hundreds of dollars lower so their one wrong forecast after another can finally be like a broken clock and be right for once), this bear market rally in the dollar should at least get to the 200-day M.A. around 79.50 in this move. While the dollar is now very overbought near-term, the fact that this rebound comes out of a classic falling bullish wedge suggests the dollar can still go higher longer term. The 83-84 area is fair game.

The long-term fundamental outlook for the U.S. Dollar remains the same – terminal.

The “Don’t Worry, Be Happy” crowd have convinced many that Uncle Sam has gone from this:

to this:

but make no mistake about it. The eye of the storm is just a respite from the economic, political and social upheaval that is well underway in America. We remain in a secular dollar bear market and this counter-trend rally comes with the territory. It would be a gift if it could rally back towards 90, but such a feat is as likely as the Jets and Mets winning the Super Bowl and World Series in the same year.

What should surprise the masses is how gold rebounds in the face of a so-called “stronger dollar,” which I believe can drive gold up to new highs in the first quarter as technicians see major bullish trends in gold in most other currencies.

May you have a most blessed Christmas and a Happy New Year.

US vs China: Watch the power game play out

Dr Faber, in the September issue of the Gloom, Boom & Doom Report you said that the future will be a total disaster with a collapse of our capitalistic system as we know it. Three months later do you still stand by that assessment or did you underestimate the power of the governments to shore up the global economy?

Well, I think we had this huge intervention in the world but if you look at the cause of the financial crisis. The cause of the financial crisis was excessive credit growth and essentially the private sector has reacted rationally. After 2008, the private sector has reduced its leverage, in other words, the consumer credit is declining and business credit is also declining but this is being offset by a huge expansion of government credit. So total credit as a percent of the economy in the US is still growing. Now officially, the debt to GDP is 375%, it was 186% when the US went into depression after 1929. In other words, we start with a much higher debt level. In 1929 we did not have social security and we did not have Medicare and Medicaid and if you add this unfunded liabilities of Medicare and Medicaid and if you add Fannie Mae and Freddie Mac, that have been taken over by the government, we are talking about the debt to GDP of over 600%. In my opinion, in the long run, this is not sustainable. They will have to print money and the fiscal deficits will go up and the problem will be that one day when interest rates go up for whatever reason and may be next year or in three years time, the interest payments on the government debt will balloon and in say seven years time, the interest payments on the US government debt will be between 35% to 50% of tax revenues and when you are in a huge mess.

And so I believe that to get out of this mess, they will monetise and they will have all kind of stimulus packages and they will lead to high inflation and the standards of living of the typical household will go down and it will enrich a few people the elite essentially on Wall Street. But then to distract the attention, the US will escalate its war efforts and then all thing will collapse. But, you know, it can be in ten years time, could be in five years time, could be in three years time, could be 12 years time, who knows but that is essentially my long term very negative view. Now as an investor, you cannot sit there then I don’t do anything at all because by being in cash you have zero interest so you have to do something and so I think that equities are probably a better place to hide than government bonds.

You have also said that somewhere in the future there will be a war and during what times commodity prices go up sharply, don’t you think the threat of war is exaggerated given that nations have shown considerable restraint in international relations during this recession?

I think, the interest of the US and China are further apart than ever before because you have essentially declining superpower the United States and you have a rising superpower China and the current superpower the US will obviously try to contain the rise of China and China will want to have more say in global affairs and you can see their expansion everywhere in Latin America, in the Middle East even in the Indian Ocean, in East Africa and so forth. So that will lead to tensions. We are at war essentially in Iraq and we are at war in Afghanistan, Pakistan and these are wars in my opinion where there is no solution and this is not going to go away. It is going to escalate over time.

So does one then assume that you are still not very optimistic when it’s comes to the US economy or the markets?

Basically, the problem of the United States is that they do not produce enough compared to the whole economy and that its net savings are very low. In other words if you have two countries or let’s put it in more simple terms, you have two households or two businesses; one household spends everything it earns, one spends everything it earns pays out in dividends and borrows money to maintain the lifestyle of the owners of the family to buy a car, to buy a house, to buy appliances, mobile phones and so forth the other household or the other company – out of its earnings puts something aside and invest in education or in terms of a company in research and development or in new plans and in new machinery and so forth who do you think in the long run will be better off. Consuming means exactly what the word says consumption is you have a plate of food in front of you, you consume it then the food is gone and saving is to put it part of the food aside for the wintertime or for emergencies. So, in my opinion, US has badly abused its power to borrow money basically and has not saved at all in the last few years and obviously, in the long run, relatively speaking, your standards of living go down compared to countries like China and India where you have a high savings rate and where people then build factories and develop their infrastructure and develop the educational standards and so on. So if you look at 1950, the US is up here and the emerging economies are down here and now the US is still up here but is not up much and emerging economies stay close the gap, there is still a gap between the US and most emerging economies but you look at educational standards in the US, in many states of the US 20% of their people are illiterate you know this I mean horrible.

The recent rise in gold for the most part has been on the back of a weak dollar now that the dollar is strengthening should one get cautious on gold?

The dollar has been weak but the other currencies are not much better either because they are tied to the dollar one way or the other or they are not tied to the US dollar they have gone up against the US dollar but basically the ECP in Europe is also money printer and the EURO has many problems as well as other currencies that were strong against the US dollar. So what can happen is that essentially the dollar is very strong but gold still holds or even goes up. If you are a European or if you are Swiss may be you decide to shift some money into gold and especially we have now in the world $7 trillion in foreign exchange reserves up from a trillion in 1996. So we have gone up in the foreign exchange reserves, in international reserves seven times. The price of gold has had gone up seven times over that period of time and in Asia we have essentially central banks that hold including Japan 70% of the $7 trillion and they have by enlarge less than 2% of their reserves in gold. So I think that a lot of central banks will follow the example of the Reserve Bank of India. By the way, the Reserve Bank of India deserves applause they have done a very good job by enlarge, is very well run central bank.

In terms of Indian equities which are the best places you would like to invest?

…..continue reading page 2 and 3 HERE.

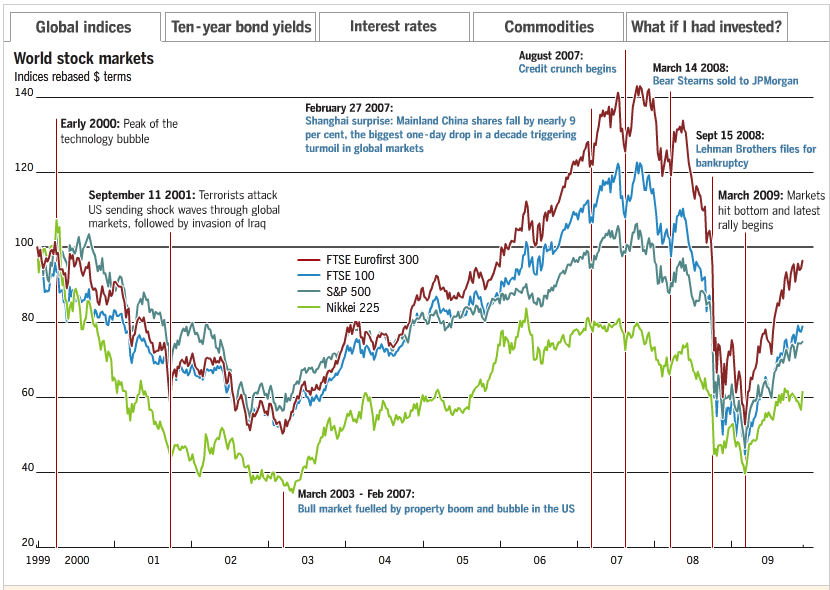

This decade in markets has been turbulent to say the least. The markets have absorbed the technology boom ending, the effects of the September 11 attacks on the United States and the subsequent invasions of Afghanistan and Iraq. Markets recovered and were inflated by the boom times of high house prices and record corporate results only to be shocked by the credit crunch, sending indices around the world sharply lower and instilling fears of a second great depression into the hearts and portfolios of investors. The 2000s ended on a hopeful note that recovery had firmly taken hold and growth would continue.

Our interactive graphic shows performance of the world’s markets in the context of the major global events throughout the last 10 years.

Ed Note: Go HERE to view a larger chart and click on the tabs to see the Decade in Bond Yields, Interest Rates, Commodities and “What if I had invested”

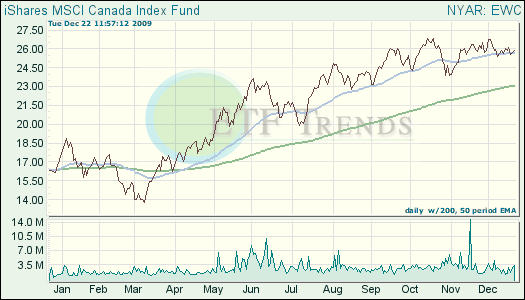

Canada caught a bit of a cold from the United States’ big sneeze, but 2010 is forecast to be a better year for our neighbors to the north and their ETF.

Canada is set to have a bright 2010, according to analysts, as the country boasts a stable banking system. The country branched out and away from relying on the business of the States and has tapped many other foreign markets that need the Canadian resources.

Why else might Canadians be smiling more next year? Money Energy reports:

- The Canadian Real Estate Association said new home sales were up 73% across the country in November, compared with the same month last year, but still slightly below the levels of November 2007.

- High domestic stability and consumption strong enough to withstand the drop-off in worldwide export demand.

- Increasing global demand in emerging markets and developing nations that rely on natural resources that Canada supplies.

- Even if the U.S. dollar strengthens, the Canadian loonie is expected to remain firm.

- May shares in representative companies from the banking, energy and telecommunications sectors are set to have a decent or prosperous 2010.

iShares MSCI Canada Index (NYSEArca: EWC): up 48.1% year-to-date

CurrencyShares Canadian Dollar Trust (NYSEArca: FXC): up 13.6% year-to-date

Tom Lydon is proprietor of ETF Trends, a website with daily news and commentary about the fast-changing trends in the exchange traded fund (ETF) industry. Mr. Lydon is also president of Global Trends Investments, an investment advisory firm specializing in the creation of customized portfolios for high-net worth individuals. He has been involved in money management for more than 25 years. Mr. Lydon began his career with Fidelity Investments and was a founding member of Charles Schwab’s Institutional Advisory Board. He serves on the Board of Directors for US Global Investors, Inc. and Rydex Investments, and is also on the Pacific Investment Management Co., LLC (PIMCO) Advisory Board for RIAs. Mr. Lydon is a regular contributor to major print, radio, and television media and is invited to speak to audiences at financial conferences around the world. Mr. Lydon is the author of The ETF Trend Following Playbook: Profiting from Trends in Bull or Bear Markets with Exchange Traded Funds, as well as iMoney: Profitable Exchange-Traded Fund Strategies for Every Investor.

Visit his site: ETF Trends (http://www.etftrends.com/)

12/21/09 Paris, France – “A nightmare decade for stocks,” says a headline in The Wall Street Journal.

“Investors would have been better off investing in pretty much anything else, from bonds to gold or even just stuffing money under a mattress. Since the end of 1999, stocks traded on the New York Stock Exchange have lost an average of 0.5% a year thanks to the twin bear markets this decade.”

The 1990s was the best calendar decade in history for stocks, with an annual gain on average of 17.5%. This decade, by contrast, was the worst calendar decade for stocks going all the way back to the 1820s…

Which gives us a sense of triumph…you know, that’s the thing that comes before a fall. Ten years ago, we warned readers that the US stock market was going into a bear market that would be like the Japanese market following the stock crash in Tokyo in ’89. It would be “long, soft and slow” we said.

Then, the market rebounded. Investors thought the promises of the ’90s – “stocks for the long run” or even “Dow 36,000” – were still good. As for The Daily Reckoning, it was obvious that we didn’t know what we were talking about, because the Dow just kept going up…first above the high set in 1999…and then all the way to over 14,000. Even we had to admit… If this was a bear market, it was a very strange one!

Ten years later, the decade of the ’00s has proven to be the worst ever. Yes, dear reader, the ’00s were the worst for investors ever, even worse than the 1930s.

Now, we are wondering: what’s next for the stock market? More of…

……read more HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair