It’s All About Deleveraging

Commercial Woes

The Lights Of Myanmar

A Lively 2010 and Buying Stocks

This is the season when pundits feel compelled to make annual forecasts. I will make mine, as I traditionally do, in the first letter of January. But already we have seen a wide range of forecasted outcomes. Are we going to grow at 5-6% or at 1-2% or dip back into recession? Why such disparity? I think part of the reason is a basic disagreement on the nature of the just-lapsed recession. Today we explore that issue. Then I point you to a way to help those who are desperately in need and only wish they had our problems. For those interested, I enclose a picture of my new granddaughter.

And finally, I start the process of getting ready, after ten years, to actually buy some stocks. Yes, it is true. Am I throwing in the towel and becoming a bull, or do I just see an opportunity? Stay tuned.

It’s All About Deleveraging

I did a very interesting one-hour show this week with Tom Ashbrook on his National Public Radio syndicated radio show called On Point. About 20 minutes into the show, Professor Jeremy Siegel of Wharton came on, and we had a pleasant debate and lively Q and A with listeners. Jeremy of course was the bull, expecting that next year the US will grow by 5-6%. I was the “bear,” expecting growth in the 1-2% range. You can listen in at http://www.onpointradio.org/2009/12/an-economic-warning. It’s also available as a podcast on iTunes (“On Point with Tom Ashbrook”) for a few more days.

I have liked Jeremy the times we have been on the same platform, and we have traded emails over the past few years. He is a consummate gentleman. He is also the author of Stocks for the Long Run. His thesis is buy and hold. Long-time readers know that I find such thinking to be wrong, if not dangerous. I believe that stocks go in long cycles (an average of 17 years) based on valuations, and that we are still in a long-term secular bear phase. I want to see valuations come way down before I suggest that the index-investing waters are once again safe. That day will come. Just not for a while.

In the meantime, Jeremy has given us the reason for his very bullish call. Paraphrasing, he said, “Look at past recoveries from recessions. They were always strong in the first year. Suggesting 5-6% is not all that aggressive.”

And I would agree with him – if the past recession was a typical recession. But we have just gone through a recession that was unlike any other we have experienced since the Great Depression. Typical recessions are inventory-adjustment recessions, caused by businesses getting too optimistic about sales and then having to adjust. You get temporarily higher levels of unemployment as inventories drop, and then you get the rebound. It is not quite as simple as that, but close enough for this letter’s purpose.

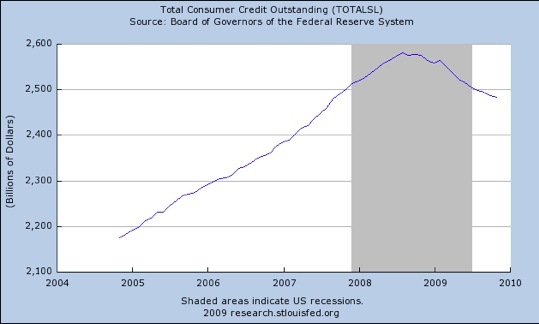

This recession was caused not by too much inventory but by too much credit and leverage in the system. And now we are in the process of deleveraging. It is a process that is nowhere near complete. While the crisis stage is over (at least for now), there is still a lot of debt to be retired on the consumer side of the equation, and a lot of debt to be written off on the financial-system side. And this is true in Europe as well, and maybe more so; but today we will look at some data in the US.

Total consumer debt is shrinking for the first time on 60 years. And the decline shows no sign of abating.

Credit card companies have reduced available credit by $1.6 trillion dollars. And for good reason. My friend and London partner Niels Jensen sent me the following charts from UrbanDigs.com. Credit card delinquencies are hovering near all-time highs. Bank charge-offs for credit cards are going to rise as the unemployment numbers get worse:

…..read more HERE.