I’ve been thinking a lot about gold lately. Especially now that Nouriel Roubini has come out and trashed the noble metal (see Tyler Durden’s article). Anyone who tells you they know what’s going to happen with gold is guessing. Roubini is guessing.

Roubini also makes some fundamental errors in his analysis, and his assumptions are flawed. Since he’s my favorite playboy economist, I should point out that he did study at the Mises Institute, but he must have cut class. He is ½ Keynesian, ½ Monetarist, and ¼ Austrian (according to Keynesian econometrics).

Ed Note: Great detailed article and charts from The Daily Capitalist

Ed Note: Great detailed article and charts from The Daily Capitalist

My conclusion, an admitted guess, is that the trend for gold is up. But … it depends on what the government and the Fed will do. The short term is a trader’s nightmare, so I don’t have a clue if it’s going up or down tomorrow. The bubble seems to be subsiding. If I were to really go out on a limb, I would guess that the fiscal stimulus bump will continue through Q1 2010, but will wear off by Q2–Q3 2010. Good GDP numbers would have negative effect on gold.

Let me explain why I think the way I think. In part it is an answer to Roubini. I could go through his report point by point, but I would rather make my own case. I don’t mean to sound pedantic, but reviewing the basics helps give perspective to the issue.

1. People want gold.

People flee to gold when they believe the future is uncertain. And you can’t tell me people like gold jewelry just because it’s pretty. It has always been that way. There is no secret to its value. People want it, it’s in short supply, you can’t make it, it’s been used as money for millennia, and, well, people want it. Accept this fact.

If you thought your paper money was going to be devalued, or worse, worthless, you’d get into some hard asset. Gold works pretty well in these situations. It’s value will be maintained while fiat money could be wallpaper. People will take anything to get rid of their paper: bread, cigarettes, candy, grenades. Whatever. Gresham’s Law.

This underlies the value of gold.

2. Fear is driving gold.

The big fear out there is that the U.S. will eventually face high inflation, perhaps hyperinflation, and sovereigns and investors who hold dollars see gold as a hedge against that event. Stability in an unstable world.

If it were all trader-driven speculation, the bubble would pop and gold would be back to $*** (pick a number). But when you have China doubling its gold reserves, and India buying tons of gold, when guys like John Paulson, Paul Tudor Jones, and David Einhorn reveal they’ve been loading up on gold, you know something is going on.

There appears to be enough demand to create a floor which would limit a collapse of the price of gold.

3. Perspective.

According to the NBER, this is my 8th cycle. My mother sold her stocks at the bottom of the 1962 cycle (down about 12%). She confided that fact to me later that year when I came home from college after starting Econ 101. She went through the Depression and was afraid. I told her we’d never have another depression: my professor told me so. That was my first cycle.

The point of the experience thing is that during almost every big cycle I’ve been through, the gold bugs came out in force and predicted dire things. Look at the ads on a lot of blogs. Check out the survivalist sites. Gold, guns, and food. Atlas Shrugged. It is not a new thing. The predictions you see today are the same as in the past. It has a big impact on (younger) people who haven’t been through a major cycle before. Everything is new in their eyes.

Also, for the most part, gold bugs always like gold. They believe the world will come to an end, soon.

Because people say it, doesn’t mean it’s so.

4. Is this cycle different?

Yes, it’s different. It’s huge.

See Carmen Reinhart and Kenneth Rogoff, This Time is Different: A Panoramic View of Eight Centuries of Financial Crises who note that cycles all act pretty much the same. What is different is that we’re going through the biggest financial-credit crisis the world has ever seen.

Fueled by cheap Fed money, rising home prices caused U.S. household debt to expand from $6 trillion in 2000 to about $14 trillion in 2007, a 233% increase. Estimates of capital losses on the balance sheets of private institutions range from $2.1 trillion (Goldman Sachs) to $3.6 trillion (Roubini). Worldwide declines in equities and real estate wiped out $28.8 trillion of global wealth in 2008 and the first half of 2009, down from a 2007 a peak of $194 trillion.

The whole world was plunged into recession because the housing boom spread world-wide, aided by central bank cheap money. The CDOs, MBSs, and CDS “insurance” were based on false risk models and spread (mainly) U.S. paper throughout the world.

This means the risks to investors are higher and grander in scope than they’ve ever been.

5. The solutions are worse than the cure.

This is the key to gold.

Fiscal stimulus:

In order to finance Keynesian fiscal stimulus, national debt is now $12.1 trillion and growing (85% of GDP). The Administration recently announced that the deficit over the next 10 years will double the national debt to about $25 trillion by 2019.

This deficit spending is a waste of money, has done nothing to revive the economy, the resulting debt is a tax on our great-great grandchildren (intergenerational theft), and the interest burden will be a substantial drag on our economy.

Money supply:

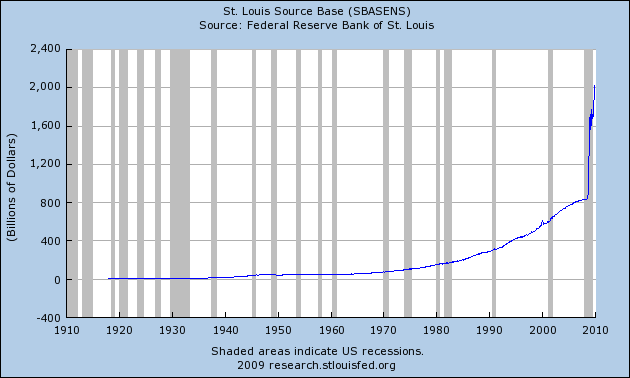

This is where folks get nervous. Money base has exploded:

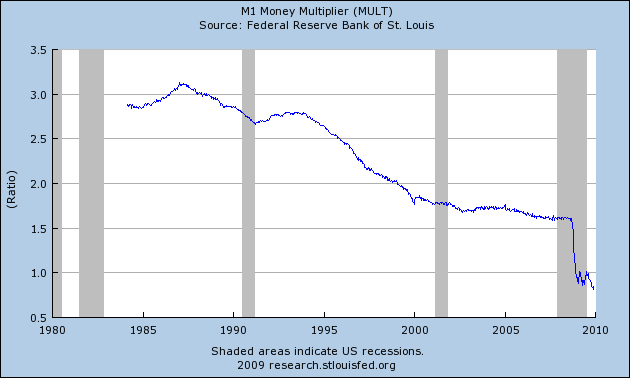

Yet, money supply, M1 for example, has dropped:

And bank reserves are very, very high:

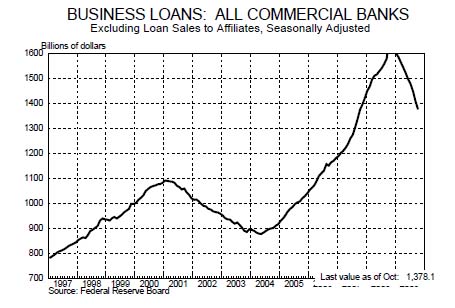

What this means is that credit has dried up. The FDIC reported that bank lending in Q3 contracted by 3%:

Banks aren’t “hoarding” according to that popular Keynesian “liquidity trap” myth. They are properly responding to the risks on their balance sheets. They aren’t going to take loan risks until their balance sheets are stable. Think not only of the bad residential mortgages and subprime paper, but the huge amount of commercial real estate held by small and regional banks–which banks are the lifeblood of most businesses.

Obama can jaw the “fat cats” all he wants, but he can’t make them lend. If he can, watch out.

Exit strategy:

The reason gold is in demand is because gold buyers doubt the Fed’s exit strategy. That is, when banks are healthy, they will lend. They will have access to all that money and credit the Fed has created, and, considering how much was created, it will lead to high inflation. Some people say hyperinflation.

The Fed says they can sop up the funds by raising the Fed Funds rate and increasing banks’ Tier 1 capital reserves. Let’s say they do that and the recovery collapses because of tighter credit, higher interest rates, and the like. Mortgage rates will go up, credit is tight, and Congress screams. You think the Fed is independent? Don’t bet on that.

What about the Fed paying interest on banks’ reserves? The theory is that banks would rather get interest on a safe “loan” of their reserves to the Fed, than make a “risky” loan to the public. That won’t work. Doing this will make it impossible for the Fed to maintain its target interest rate. Also, banks don’t keep customers if they don’t lend, so they will. Please see this article for a thorough explanation of this.

Higher interest rates will stop inflation. Will Bernanke do this? It worked for Volker. If he doesn’t, we’ll have inflation.

6. The dollar.

The decline of the dollar is an intentional yet unofficial policy of the Obama Administration to pull us out of the recession. I don’t know why they believe this, because, while it will stimulate U.S. exports, it will kill businesses which are based on imports.

We’ve been running trade deficits for many years before this crisis, yet the economy expanded and jobs increased rather than decreased. One can clearly conclude from the data that when GDP expands, imports increase. Conversely they shrink during a contraction. It’s been this way for at least 30 years.

Right now, the current account is more “balanced” in that exports have been rising. That has everything to do with the recession–people are buying less. In economic terms, letting the dollar fall in order to boost exports is just old fashioned mercantilism. It was proven wrong with the introduction of free trade.

The result: we all pay more for imported goods, which, these days, is just about everything. The offset in exports won’t be enough to stimulate consumer spending. See, “Economic Megatrends That Will Drive Our Future.”

Don’t expect the Fed or the Treasury to halt the dollar’s decline anytime soon. High inflation will be a big negative for the dollar and a positive for gold.

7. Why did gold go up?

I was hoping this wasn’t as obvious a question as it seems.

The dollar is going down is a more accurate way to put it. That has the most to do with gold’s rise. Here’s a chart of the dollar (DXY):

You will notice from the chart that during the initial stages of the crisis, people flocked to the dollar which shows that it is still the world’s reserve currency, especially during a crisis. But after that, it’s been a slide.

Reason No. 1:

Check out this recent article from the Financial Times:

One factor supporting [gold] prices is the change in attitude by central banks, some of which see buying gold as a way to diversify from the dollar and their holdings of US Treasuries. For many years, central banks were net sellers of gold. Not any more – earlier this year it emerged that Chinese gold reserves had almost doubled. …

There has been speculation this week that China could snap up the remaining 203 tonnes of IMF gold. Brazil has also been touted as a potential buyer.

Michael Lewis, commodities strategist at Deutsche Bank, notes that the majority of central banks banks in the developing world have less than 10 per cent of their reserves in gold.

Mr Lewis combines this list with large holders of US Treasuries who have a strong incentive to diversify into gold given the “non-negligible risk of a US debt and currency crisis”.

China, Japan, Russia, Taiwan, India, Singapore, Brazil and Korea are strong potential candidates to increase their bullion holdings, he says. “We expect central banks, in aggregate, to be net buyers of gold over the coming year for the first time since 1998.”

Reason No. 2:

Private buyers of gold or gold related assets such as GLD and gold futures are the second reason for gold going up. See above about Paulson, Jones, and Einhorn. Lots of buyers in China and Asia.

Reason No. 3:

Speculation. As I said, I have no idea what will happen tomorrow. Note that the dollar rose in December and gold declined.

8. Does the deficit matter?

Foreign buyers finance 30% of our debt. We sell our debt to China, Japan, and the U.K. China holds $1.521 trillion of our debt.

Big exporters like China and Japan can’t do much about their holdings without cutting off an arm or two. They know they are stuck. They’ll grab their ankles and keep buying our debt, perhaps demanding more TIPs. I think the Chinese really believe in the Fed’s exit strategy. But … they are still buying gold as a hedge.

U.S. banks have been investing their reserves in Treasuries. Also, because U.S. consumers are increasing their savings, private holding of Treasuries have also increased. And, it appears the Fed and Treasury have been monetizing some of the debt.

This is why T-rates have been low.

Deficits affect gold only in the long term. I don’t think holders of dollars will not buy our paper. Assume China and Japan cut back on funding our deficit. What will happen? Investors will demand higher returns, interest rates will go up, paper will be sold, and the ultimate tax burden will slow down the economy.

It is printing money and easy credit which causes inflation, drives the dollar down, and causes gold’s rise.

9. Gold will go higher–eventually.

It’s all about inflation and world stability.

Black Swan:

By definition you can’t see the next world-changing negative Black Swan event coming. I’m leaving an economic crash out of this part of the discussion. Volcano. Nuclear terrorism. Iran. Comet. Pakistan. Take your pick. These events create world instability and people run for safety.

These are the reasons you buy some gold anyway. Taleb is completely right on investment strategy. Be conservative on 80% to 90% and bet the farm on the rest. Gold is safety.

Deflation:

It’s not over. This is a controversial issue, but as long as real estate assets fall in value, we won’t see much inflation. I didn’t say “any” inflation, just not much as long as real estate keeps dragging banks down, causing credit to remain tight.

I’ve addressed the continuing problems with housing recently; if you need more on this see “Why The Housing Market Is In Trouble.”

Commercial real estate is as bad. The Administration has adopted a policy of “extend and pretend” for banks with CRE debt. If you can show that you will eventually be able to amortize the loan at least to even when things get better, banks can extend the loan, reduce interest, or whatever it takes.

While many analysts see this as a positive, it isn’t. It is just another way to ignore reality like suspending mark-to-market. This will drag out the recovery as banks are still burdened with make believe debt on their books. More uncertainty for lenders will keep them tight fisted.

This could last several more years. But the government has other ideas about real estate that could shorten deflation: reignite the bubble.

Inflation:

Since I don’t believe the Fed can save us from themselves, I don’t know why we won’t have inflation.

Because the economy will remain sluggish due to the continuing credit contraction noted above, the Fed will keep pumping new money to thwart a “relapse” of the economy. I think inflation will eventually take hold in 2011 because the Administration will reflate the real estate bubble. And that will repair a lot of bank balance sheets. Real estate can be reflated by means other than monetary policy (FNMA, FHMA. FHA, GNMA, and tax policy).

I think inflation will last for some time because it benefits debtors, including the federal government, and will allow them to pay down debt with cheap dollars. The perception of a recovering economy will carry the Democrats and President Obama to victory in 2012. So you will see inflation well into Obama’s second term. Oh, yes, he’ll be re-elected. FDR made the Depression worse yet he was re-elected, so why not Obama. The odds are heavily in favor of incumbents.

So Ben won’t have to muster his courage to raise rates until 2013.

Inflation will drive down the dollar and gold will go up.

Hyperinflation:

Everyone, Austrian, Keynesian, Monetarist, and Marxist knows what causes hyperinflation and no one will let it happen.

Hyperinflation is a popular theme with gold bugs, but I don’t buy it. Hyperinflation is far worse than a recession and Ben, Larry, and Timmy know that.

Let me give you another scenario. When inflation really gets high, say to Jimmy Carter levels (13±%) or higher, we will see a temporary implementation of price and wage controls, as in Carter and Nixon. Since everyone also knows these don’t work, it will just be a smokescreen to allow Bernanke to raise interest rates until inflation comes under control.

10. Remember, this is a guess.

These are the guide posts we should keep watching in order to protect our investments. As I said at the beginning, it all depends on what the government and the Fed do. I’m not going to tell you what to do because I don’t give investment advice. But my analysis points to an increase in gold over the long term because I think a continued dollar decline is inevitable. Gold is a favored hedge against this.

*Disclosure: I am not selling you anything. I don’t want to manage your money. I’m not giving you investment advice. I am peripherally involved in the gold mining business, but if you run out and buy gold it won’t affect me. So, I have nothing to gain by this article. Keep that in mind when you research those selling gold investments.

About The Daily Capitalist

This blog comments on economics, politics, and finance from a free market perspective. We try to present ideas the reader would not find in contemporary media. In addition to the founder of the Classical School of economics, Adam Smith, our influences are from the Austrian school of economics. Among its leading thinkers have been Ludwig von Mises and Friedrich von Hayek. There are many practitioners of this school today and some of their blogs are shown on the blogroll. We trace our political philosophy back to Edmund Burke, David Hume, John Locke, and Thomas Jefferson, to name a few.

Our goal is to challenge contemporary thinking, mainly from those who promote Keynesian economics (almost everyone) and those who rely on statist solutions to problems.

We also have an interest in investments and finance, and specifically investment risk and the role of the business cycle.

We don’t consider ourselves Democrats or Republicans, right wing or left wing. We’re on the freedom wing.

We also publish articles in Zero Hedge, Noozhawk.com, and The Montecito Journal.

We hope you enjoy our commentary, and please join in the discussion.

About Jeff Harding

Jeff Harding is a real estate investor and former lawyer in Santa Barbara, California. He is a principal of Montecito Realty Investors, LLC. He has many years of experience in business cycles related to real estate investments and finance. He also was financing director of a home builder. Also, he wrote the great American unpublished novel several years ago.

If you wish to engage Jeff Harding to speak at your function, please contact him:

To contact Jeff Harding: econophile@dailycapitalist.com