Daily Updates

The Bottom Line

The “hoped for” short term correction has arrived. The correction will set up seasonal trades in several sectors including silver, mines & metals, basic materials and energy. However, the technicals for these sectors currently are unfavourable. Please be patient.

Ed Note: a small selection of the 41 Charts Analysed on Don Vialoux’s Monday Morning comment HERE.

The S&P 500 Index fell another 17.89 points (1.64%) last week and 6.66% from its peak on January 14th. The Index remains below its 50 day moving average and could be testing support at 1,029.38 and its 200 day moving average at 1,013.05. Short term momentum indicators are oversold, but continue to trend lower. Seasonal influences remain positive.

The TSX Composite Index dropped another 249.12 points (2.20%) last week (8.09% since January 11th). Downside risk is to its 200 day moving average at 10,865.53 and support at 10,745.25. Short term momentum indicators are oversold, but have yet to show signs of bottoming. Strength relative to the S&P 500 Index remains negative. Seasonal influences remain negative.

The U.S. Dollar Index added another 1.19 last week. Intermediate trend is up. It moved above its 200 day moving average and is testing resistance at 79.51. Next resistance is at 81.47. Seasonal influences are positive until April Short term momentum indicators are overbought, but have yet to show signs of peaking. Stochastics are above 80% and RSI are above 70%, levels where a correction frequently is imminent.

The Canadian Dollar fell another 1.10 U.S. cents last week in response to strength in the U.S. Dollar Index and weak commodity prices. The Dollar remains in a four month trading range between 92.16 and 97.79. Short term momentum indicators continue to trend down.

Gold lost another $17.80 U.S. per ounce last week mainly in response to strength in the U.S. Dollar. It closed below support at $1,075 on Friday. Next support is at $1,025 and long term support at its 200 day moving average currently at $1,012.93.

You can check out Don Vialoux’s Long Term Forecast at January 22,23rds

![]()

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Don earned his Chartered Market Technician (CMT) designation from the Market Technician Association in 1995. His CMT paper entitled “Seasonality in Canadian Equity Markets” was published in the Spring-Summer 1996 edition of the MTA Journal. Don also has extensive experience with Exchange Traded Funds (also know as Index Participation Units) as well as conservative option strategies. In 1990 he wrote a report that was released in the International Federation of Technical Analyst Journal entitled “Profiting from a Combination of Technical and Fundamental Analysis”. The report introduced ” The Eight Phases of the Stock Market Cycle”, an investment concept that continues to identify profitable entry and exit points for North American equity markets. He is currently a member of the Toronto Society of Fundamental Analyst’s Derivatives Committee. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

ACTION ALERT:

Keep your powder dry for likely buying opportunity between now and mid-March. That trade may or may not result in a move to new highs, but we’ll update you accordingly along the way. Meanwhile, we’re in a downtrend and there is no definitive sign of abottom, so stay tuned!

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). The weekly VR Gold Letter focuses on Gold and Gold shares.Go HERE and use the Money Talks promo code CBC12210

Since my December 3 ‘Sell’ signal for Gold, this market has reasonably con- formed to my expectations. I had discussed seeing the 1070 level as a pullback zone and indeedshortly afterwards we saw 1073. I also anticipated the formation of a 1070 to 1170 trading range which to date has been in force. We are clearly in a corrective phase and volume has been negative since the December high. My job is to follow the market and if the market says down I report it that to you. I, too, am a long-term bull on Gold and theprecious metals but we have to expect intermediate corrections. For the past ten years each year has seen periods of correction to varying degrees and the potential exists for very sharp corrections much as we saw in 2008 where Gold traded in the 600s. We could in theory see Gold back to the 800s and nothing would change the bigger picture uptrend. Current technical signals suggest risk down to the 960-970 level in the months ahead and there is always the potential generating lower downside targets. As a result, I am on the sidelines in the Gold market, but watching for trades in all the metals including Platinum, Silver, Palladium, Lithium, Copper and the base metals as opportunity arises.

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Mark Leibovit’s forecast at the World Outlook Conference Jan 22, 23rd available HERE.

![]()

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). Go HERE and use the Money Talks promo code CBC12210

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

Beginning about Wednesday, last week, the markets decided to get ugly and turn down. This is an event we had predicted for some time admonishing those with significant profits to take some. The attack on the U.S. banking system by the Obama Administration has certainly had its impact as has the negativity by certain in Congress (both sides) over the re-nomination of Chairman Bernanke. We do expect Dr. Bernanke to be re nominated. Today we shall see the two most recent Treasury secretaries (Paulson and Geithner) testify. The finger pointing will now be directed toward the history of the AIG and possibly the Fannie and Freddie fiascos.

There is a very powerful populous sentiment seeking to place blame today and these all these actors are now in the cross hairs. Congressmen and Senators (from both sides of the aisle) are hearing populous footsteps – and they are scared. Power can dissipate quickly. Only the Administration seems tone deaf on this building tsunami. Couple this with the political shifts we have seen in Virginia, New Jersey and Massachusetts and you must conclude that there is change coming – and probably not from this Administration or Congress.

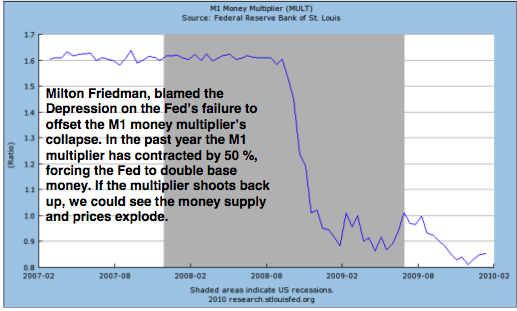

At present the financial system in the US is still broken. What we do know is that over the past two years as the crisis heightened, debt was simply shifted from failing entities (AIG for example) to the Federal Reserve and eventually the public. At the Fed the leverage ratio is now 50 to 1. Everyone is watching China. Will that become a bubble that will eventually burst? In other words the new global economic engine, at least in the minds of many people, is now China – and China is beginning to tighten.

The St Louis Fed’s multiplier ratio and the velocity of money (MZM/GDP) are still flashing red. Unemployment, a lagging indicator, is dragging the economy down. Housing numbers released yesterday were horrible. Sales of previously owned US homes suffered the worst drop in December. The boost from the tax credit is over. Can a housing market recovery be sustained? Existing home sales fell 16.7% in December – the sharpest decline since 1968. Sales were 450,000 below expectations. As long as the government spends on housing we recover – once Washington stops ….? Low mortgage rates also subsidized by Federal Reserve buying of mortgage-backed securities willcore of the US recovery.

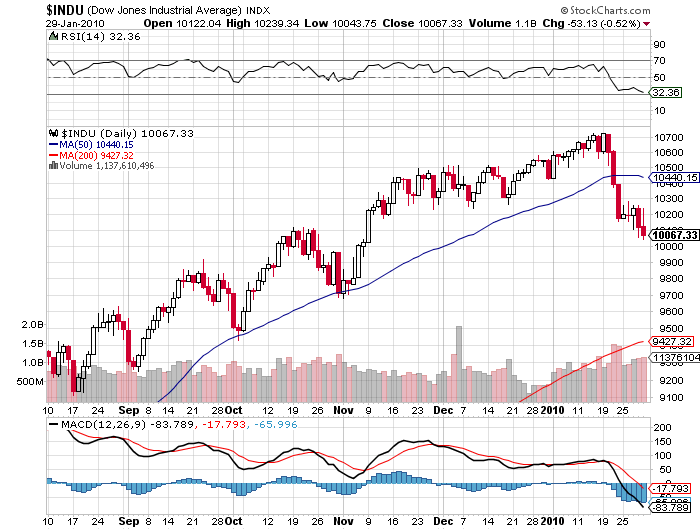

It seems quite likely that equity markets need a break after almost a full year of this equity market run-up. I have often maintained, during the past year, that this was a bear market rally. I still hold that opinion today. As you can see in the chart below, this pullback is the largest since July 0f 2009 and it has broken through its 50 day moving average – for the first time since July. It would appear that the psychology of the market has changed. Those in Washington (on both sides of the aisle) have started to place blame (Bernanke, Geithner and bankers) in order to deflect public dissatisfaction with a 10.4% unemployment rate and a 17.8% underemployment rate. The unknown is just how much damage will ultimately be done by the overreaction to the events of the past three years beginning in July 2007 and the gutting of the financial system by the newly anointed Washington Paul Volcker.

To sign up for Michael Berry’s Discovery Investing FREE letter go HERE.

Michael Berry has been a portfolio manager for both Heartland Advisors and Kemper Scudder where he successfully managed small and mid cap value portfolios. Dr. Berry has specialized in the study of behavioral strategies for investing and has been published in a number of academic and practitioner journals. His definitive work on earnings surprise, with David Dreman, was published in 1995 in the Financial Analysts Journal.

Previously, Dr. Berry was a professor of investments at the Colgate Darden Graduate School of Business Administration at the University of Virginia and has also held the Wheat First Endowed Chair at James Madison University.

Dr. Berry is a respected and dynamic speaker. He regularly presents around the world on topics such as value investing, the role of Austrian Economics in investment management, behavioral investing strategies and is a specialist in developing case studies to teach investors how to invest. While a professor, he published a case book, Managing Investments: A Case Approach.

He has recently focused on the role of precious metals in the asset allocation of the individual investor.

“to create more of these clean energy jobs, we need more production, more efficiency, more incentives. And that means building a new generation of safe, clean nuclear power plants in this country.“ – President Obama in his State of the Union Address

Update – Obama Set to Go Nuclear? [William Tucker]

Hip, hip, hooray! President Obama is reportedly about to announce an expansion of the loan guarantee for nuclear plants from $18 billion to $54 billion — probably after hearing that applause, the biggest outburst of the night, when he mentioned nuclear in his State of the Union Address.

I know people are going to say, “Oh, he doesn’t mean it” or “It’s still a drop in the bucket,” but don’t be fooled. This is going to get the ball rolling. The thing to recognize is that nuclear already has so much momentum behind it, all it will take is a little push and it will be all downhill from there……read more HERE

Current Price $42.50

Current Price $42.50

“The decarbonization of energy. With global concerns about carbon footprints, the move to nuclear energy is a foregone conclusion in much of the world. Why? Just look at the numbers:

1 kg of firewood produces about 1kWh of electricity.

1 kg of coal or oil produces about 3 or 4 kWh of electricity.

1 kg of natural uranium produces nearly 50,000 kWh of electricity!

China has taken the lead, with plans to build 10 new reactors a year for the next decade. India and Russia aren’t far behind. The U.S. has 17 applications to build 26 reactors waiting for approval. Energy consumption is expected to grow by 40% by 2030. And nuclear is the only source that can meet that demand.

That, briefly, is the case for a long-term bull market in uranium. It’s a simple case of supply and demand. Current uranium production doesn’t meet current demand. And demand will do nothing but increase as more reactors come online.” – Bob Irish Investors Daily Edge

“When I was head of an electric utility, I pushed for a greater position in nuclear, only to be shouted down by the environmentalists who carried the guilt of Hiroshima and took advantage of the two nuclear ‘events’ you mentioned.

Sadly, we are now behind other nations in utilizing this technology. It is not perfect, but is certainly the best of all currently available electric energy sources”.- Paul Cunningham

“We still have to address spent fuel storage and conversion, and get over the NIMBY behavior that has not allowed that to happen in the past. Meanwhile, uranium mining seems a good investment.” Bob Irish Investors Daily Edge

Information on Uranium Stocks http://www.uraniumstox.com/

Via the Daily Reckoning:

The Case for Commodities in 2010

The biggest emerging economies have ambitious plans that require a greater share of the world’s limited commodities. This trend is spurring profound and permanent disruptions in how these resources are allocated now and in the future. For investors, these disruptions present opportunities.

Simply put, an investment in natural resources is a vote of confidence in global economic growth.

Rapid urbanization and industrialization, better infrastructure and growing consumption in emerging markets are among the key themes in the global growth story. They are also key drivers in the rising demand for oil, steel, copper, cement and other resources.

Here are just a few of the many available data points to help gauge the scale of opportunity:

- Just over half of the world’s people now live in cities – that figure is likely to rise to 70 percent over the next four decades. The urban population in emerging nations has expanded by an average of 3 million per week for the past 20 years.

- India has embarked on a $500 billion plan to expand and upgrade its highways, airports and other transportation assets by 2012.

- More than 13 million cars and light trucks were sold in China in 2009, transforming a land once dominated by bicycles into the largest auto market in the world. Forecasts for 2010 call for vehicle sales to increase by as much as 10 percent.

…..read all HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair