Daily Updates

The financial crisis hasn’t been fixed. And then, there’s government debt…

FEAR GIVES FOOLS intelligence, says an old proverb. Turning it around a bit, we might say that lack of fear makes fools of wise men, writes Chris Mayer in The Daily Reckoning.

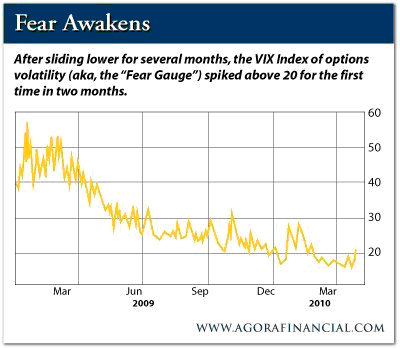

In the market, fear – or the lack of it – finds expression in many forms. The Volatility Index, or VIX, is one of them. Known as the “fear gauge”, the VIX bounces up and down based on what people are paying for options on the S&P 500.

For example, if people are fearful, they tend to buy put options. Put options are like insurance against a fall in price. They pay off if the market falls. When investors pile into put options, they make the price of such options rise, and that pushes the VIX up, too.

Conversely, when people are not worried, they sell those options – or at least they don’t buy them. So the price falls, and so does the VIX. There has been a lot of that going on in the last year. The VIX recently hit its lowest point in 30 months, as shown by the nearby chart.Fear looks cheap. Given all that is going on in the world, it is remarkable to find investors so complacent.

The financial system is still a rather creaky affair. Leverage is still high. Banks remain undercapitalized. The credit cycle has not yet run its full course, as there are still significant credit losses hiding in the cupboards of banks.

Then there are the governments of the world. The US has awful credit metrics. It is bleeding money and owes huge debts. Most of the 50 states are also bleeding money and have large debts, including giant gaps in unfunded pension liabilities. They are perhaps worse off, because unlike the US government, the states cannot print their own money. Then there is the EU. And Japan.

There are only a few ways to cure such ills, and none are painless. One thing is for sure: These ills can’t go on forever.

So in the context of all this, fear looks cheap.

Conveniently, Wall Street has made fear a tradable commodity. One way to play it is through the iPath S&P 500 VIX Short-Term Futures fund. Though a mouthful, it simply aims to mimic the VIX. It trades under the ticker VXX, and started trading only this year. It’s done horribly, as you would expect given the fall in the VIX.

Yet it could be a nice play should we have another spike in the VIX. If fear should rear its head again, as it undoubtedly will, the VXX ought to prove nice insurance. More than just insurance, it could return three or four times your money, depending on the spike.

Whether buying the Vix or some other insurance, however, fear is cheap. Buy some before the price goes up.

Chris Mayer

Want Physical Gold in your name – and your name alone? Choose secure storage from New York, London or Zurich for just $4 per month, only at BullionVault…

A keen student of financial history, Christopher W. Mayer gained an MBA in finance before beginning his banking career in corporate lending.

He soon launched Capital & Crisis, a monthly newsletter now excerpted by leading financial publications including the Mises Institute, LewRockwell.com, PrudentBear.com, Grant’s Investor and Individual Investor Magazine.

Chris’s unique brand of “value” investing has earned him a strong reputation as an analyst and writer. You can learn more here…

New York University economist Nouriel Roubini says the euro zone’s days may be numbered, and he’s not talking about some day far off in the future.

“In a few days, there might not be a euro zone for us to discuss,” he said at a Los Angeles conference sponsored by the Milken Institute, Reuters reports.

European policy makers may have to fork over 600 billion euros ($794 billion) in aid or buy government bonds to erase the debt crisis, economists tell Bloomberg.

Roubini says Greece can’t come up with the 10 percent spending reduction necessary to prevent its debt from exploding out of control.

And even if it could, its economy would get ruined in the process, he maintains.

Roubini compares Greece to Argentina in 2001, shortly before it defaulted on its debt.

Greece’s budget deficit, at 13.6 percent of GDP, is much higher than Argentina’s back then. Greece’s debt-to-GDP ratio and current account deficit also are much higher, Roubini points out.

The solution, Roubini says: a debt restructuring that reduces interest rates and extends maturities. In addition, Greece should exit the euro, he says.

Roubini’s not the only one calling for drastic measures.

“It may now be time for the euro area to do something much more dramatic in order to prevent the stress from creating another broad-based financial crisis which pushes the region back into recession.”David Mackie, chief European economist at JPMorgan, told Bloomberg.

Roubini: Debt Crisis Will Spark Defaults, Higher Inflation

April 30th/2010

The exploding government debt burden in nations ranging from Greece, to the United States, to Japan will end in government defaults or higher inflation, says New York University economist Nouriel Roubini.

“The bond vigilantes are walking out on Greece, Spain, Portugal, the U.K. and Iceland,” Roubini said at a recent conference, Bloomberg reports.

“Unfortunately in the U.S., the bond-market vigilantes are not walking out.”

Bond vigilantes are traders who sell bonds in markets where the country pursues lax fiscal and monetary policy.

“The thing I worry about is the buildup of sovereign debt,” Roubini said.

If the debt problems aren’t solved soon, nations will either default on their government debt or monetize them by printing money, which would create inflation, he maintains.

“Greece is just the tip of the iceberg, or the canary in the coal mine for a much broader range of fiscal problems.”

The U.S. budget deficit totaled $1.4 trillion last year, and the Congressional Budget Office predicts the government debt burden will total 60 percent of GDP this year.

As for Greece, “It could eventually be forced to get out of the euro,” Roubini told Bloomberg.

But don’t expect the U.S. to intervene in Europe’s crisis, says Randall Stone, a political scientist at the University of Rochester.

“There’s a sense in the Obama administration that it’s Europe’s responsibility to straighten out problems in the euro zone,” he told The New York Times.

Market Buzz – Deficit Shrinking, No Need to Celebrate “Cashing” in Again Just Yet

In a relatively jittery week, Toronto’s main index fought back from what looked like significant losses mid-week to end the five day session only 28.94 points or just 0.24 per cent.

Gold stocks supported the index this past week, handily outperforming the rest of the market with a 7 per cent rise. The price of gold hit a 2010 high (above $1,180 per ounce) on Friday in a flight to safety bid spurred by concern over whether a rescue plan for Greece will emerge and news that Goldman Sachs faces a criminal investigation.

Federally, there was some relatively good news on the debt front as Canadians may incur a smaller deficit for the current fiscal year than previously feared, thanks to a quicker and stronger than expected recovery in economic activity. Ottawa reported Friday that its deficit increased by a “modest” $902 million in February compared to an $800-million surplus the year before. The trend is improving as Ottawa had reported monthly shortfalls of $5 billion and more from last June to October. The data has steadily improved to the point that the last two months have both seen deficits of under $1 billion.

For the fiscal year, which has one more month to run, Ottawa’s shortfall has now risen to $40.5 billion. But that is still well below the record $53.8 billion deficit Finance Minister Jim Flaherty had projected in the March budget.

Before you all run out in the streets and party like the good times are here once again, remember that the year-to-date $40.5 billion deficit is a sharp contrast to the $1.3 billion surplus Ottawa enjoyed at this time last year, with $18 billion of the shortfall attributed to stimulus spending intended to arrest the economic slide. There still remains some tough sledding ahead my friends.

This past week, our Canadian Small-Cap Universe was rewarded with another set of strong quarterly results from The Cash Store Financial Services Inc. (CSF:TSX). Cash Store Financial is the largest provider of alternative financial products and other financial services in Canada with a rapidly growing network of branches in over 200 communities nationwide. The company operates two of the most recognizable brands in Canada’s expanding payday loan services market – The Cash Store and Instaloans.

This past week, the company’s shares jumped to $18.00 (recommended last year at $7.12) after reporting results for the three and nine months ended March 31, 2010. Quarterly revenue rose 12.4 per cent to $40.8 million from $36.3 million in the same quarter last year. Earnings per share (diluted) before non-recurring class action settlement costs rose 27.8 per cent to $0.23 from $0.18 in the same quarter last year. Net income before non-recurring class action settlement costs and related taxes were up 29.0 per cent to $4.0 million from $3.1 million for the same quarter last year.

Branch count was 489, up 66 net new branches from 423 at March 31, 2009. 20 new branches opened in the quarter. Subsequent to quarter-end, The Cash Store announced that its branch count surpassed 500 in operation.

Finally, the company reported a dividend of $0.10 payable May 26, 2010, to shareholders of record on May 11, 2010.

Looniversity –Understand Your Tolerance for Risk

In the wonderful world of investing there is a direct relationship between expected returns and risk – the higher the expected payback from your investment, the higher the risk. Before you can decide on a personal investment strategy, you must consider how much or how little risk you are prepared to take with your hard earned dollars.

Your risk tolerance can be affected by:

Time horizons

The amount of time you have to meet your financial goals and to make up for any losses you might experience. People with long-term horizons may be more willing to endure periodic fluctuations in the value of their investments.

Cash requirements

The extent to which you depend on your investments to meet day-to-day expenses. Investors who rely on their investments to meet daily living expenses will be much less comfortable with the risk of losses.

Emotional factors

Your emotional response to risk and to changes in the value of your investments. Some people are quite comfortable with the ups and downs of the market, while others find it difficult to sleep at night when their investments fluctuate in value.

There is no ‘right’ answer to the question, “How much risk should I take?” Risk tolerance is a personal issue. You should never feel obliged or pressured to take more investment risk than you are comfortable with. Remember, though, that there is no such thing as a high-return risk-free investment. You cannot expect to be rewarded with high returns on your investments if you are not prepared to accept the risks that go with them.

Put it to Us?

Q. A friend of mine trades often on the AMEX exchange in the U.S. Can you give me a brief rundown on it?

– Jamie Hughes; Calgary, Alberta

A. With a rich history that dates back to the late 1700s, when outdoor brokers made markets in securities (i.e. stocks) in what became known as The New York Curb Market, the American Stock Exchange (AMEX) has evolved dramatically over the past century. Now located at 86 Trinity Place in downtown Manhattan, today’s AMEX boasts the third highest volume of all exchanges trading in the U.S.

The bulk of trading on the AMEX consists of index options (computer technology index, institutional index, and major market index) and shares of small to medium-sized companies. The exchange also hosts an unrivaled listing of more than 100 exchange traded funds (ETFs), a securities category it helped pioneer.

In 1998, the AMEX merged with the National Association of Securities Dealers (NASD), but continues to operate as an independent entity within the NASD family of companies.

KeyStone’s Latest Reports Section

- Diversified Mining & Environmental Drilling Company Posts Resilient 2009, Solid Fundamentals Relative to Peers, Produces 74% Share Price Gain in Eight Months – Long-term Rating Upgraded (Flash Update)

- Canada’s Leading Industrial Services Firm Posts Solid Q1 – Rating Maintained (Flash Update)

- Pull-back in China-Based Stable Good Manufacturer Presents Opportunity – Rating Change (New Buy Report)

- Specialty Paper Manufacturer Shares Hit New All Time High, Up 134% in 3-months, Announce Acquisition – Rating Change (Flash Update)

- World Point Announced Going Private Transaction, Shares Gain 81% in 10-months – SELL (Tender Shares) (Flash Update)

Something like this …

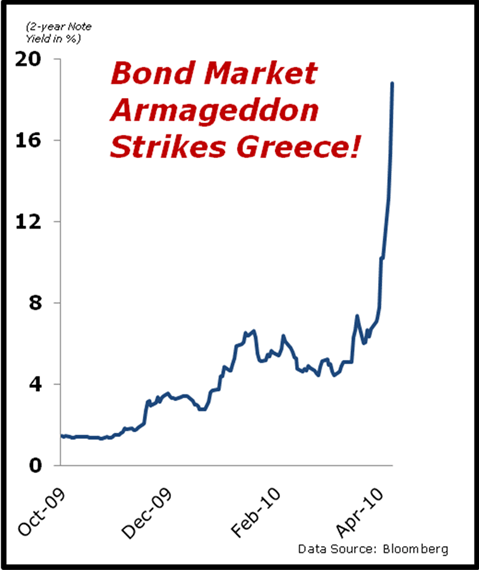

Financial Ebola Sweeps Through Global Bond Markets

The chart above shows the yield on the benchmark 2-year note in Greece. Just a few short months ago, Greek sovereign yields were hovering around 2.1 percent. On Wednesday, they shot up as high as 18.9 percent!

Translation? The cost of borrowing for the Greek government — not some subprime mortgage customer or deadbeat credit card holder — shot up almost NINE-FOLD in the span of six months.

During this same time, the price of Greece’s 6 percent 10-year notes due July 19, 2019 plunged from 112.4 to 68.1. That’s a loss of more than 39 percent. Not on some dot-bomb stock … not even on a high-yield, or “junk” piece of paper …

… but on a sovereign government bond!

Folks, THAT is bond market Armageddon. And it’s playing out now. Right on the trading screen of every investor around the world.

Think Greece Is Alone?

Think Again!

Worse, the pain isn’t confined to Greece …

Portugal’s benchmark 2-year note yield just blew out to 4.82 percent from 1.58 percent. That’s a tripling in interest rates in less than a month.

Ireland? Its 2-year yield rocketed to 3.83 percent from 1.62 percent in 23 days.

Even bigger European economies, like Spain, are getting whacked. Yields there recently shot up to 2.08 percent from 1.36 percent.

Standard & Poor’s has taken the hatchet to its sovereign debt ratings in response. The agency cut its Spanish debt rating to AA just a day after slashing its Portuguese debt rating by two notches to A-. It also cut its Greek debt rating by three notches to BB+, “junk” territory.

Bottom line: A virulent sovereign debt contagion is spreading like wildfire throughout the euro zone. In the short run, that will likely get the Germans to back down on their bailout opposition.

They’ve been holding up a package that would give Greece up to $60 billion in aid from richer European Union nations and the International Monetary Fund. The crisis may temporarily take a breather if the package gets approved.

But here’s the thing: If the Greeks get bailed out, who’s next? And where the heck is all the bailout money going to come from? Policymakers may need to cough up almost $800 billion to “save” everyone, according to economists at firms such as Goldman Sachs and JPMorgan Chase.

The problem is that nobody has that kind of money laying around! So it’ll have to be borrowed. And if it has to be borrowed … from a European bond market that’s already falling apart at the seams … what’s likely to happen? Even more selling, which would drive bond prices down and interest rates up!

Coming Soon to a Bond Market

Near You: Financial “Ebola!”

So far, this is predominately a problem for continental Europe. Our Treasury prices actually rose a bit during the worst of the European debt selling.

But I believe it is woefully ignorant, provincial, and arrogant for us to assume something similar can’t or won’t happen here.

Even the Secretary General of the Organization for Economic Cooperation and Development likened the crisis to the “Ebola” virus, saying “it’s threatening the stability of the financial system.”

When you think it through logically, you can’t help but ask: Why wouldn’t the Grim Reaper eventually come knocking at OUR door?

After all, OUR deficits are out of control! OUR debt level is through the roof! OUR politicians are burying their heads in the sand, just assuming they’ll be able to keep funding their profligacy at rock-bottom rates forever. Those are precisely the same problems that built up in Greece for months on end.

Then one day, the lid blew!

Think about it:

- Our total debt load is set to double to $18.6 trillion over the next decade,

- Weekly benchmark Treasury auctions have surged from $20 billion to $30 billion to more than $120 billion,

- And we’re dumping more than $375,000 in debt onto the market every second in some weeks, all in an effort to fund a budget deficit that’s closing in on $1.6 trillion!

Do I expect a nine-fold rise in U.S. 2-year note yields? A 40 percent plunge in bond prices in just a couple of months? Not really.

But I do believe the bond market will force us to take our fiscal medicine. I do believe a sovereign debt crisis is brewing here. And I do believe it will be just one reason our interest rates will head significantly higher.

So please, invest and prepare accordingly. By the time the bond market bleeding starts, it’ll be too late.

Until next time,

Mike Larson

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

Market Overview: Unfortunately, most of the commentary we see about markets has been unusually ignorant, myth driven, and based on rationalizing bad decision making.

Our views:

1. Cyclical Bull, Secular Bear: The secular bear market collapse of 55% was right in line with other such debacles. The collapse was faster and more furious than typical, but the depth was normal. The snapback is also well within the range of bear market rallies — cyclical bull runs that last 6 to 24 months and range from 25% to 135%.

While it is possible that we are witnessing the start of a new 1982-like Secular bull market, the valuations argue against it. Stocks most likely simply did not get cheap enough — or despised enough — to initiate a multi-decade bull run. My best guess about that bottom is its likely 3-7 years away.

2. Snapback: The 75% bounce over a year seems like a lot — until you put it into the context of a six month 5,000 point collapse. we call that the Armageddon trade — Dow 5000! 3000! We’re going to zero! – was a spasm of panic. It has been mostly unwound this past year.

3. Correction coming (eventually): The cyclical bull tends to end with ~25% correction that lasts about a year. So we are always looking for signs that this run is over. Despite the recent turmoil, we have not found confirmation that the bull run is over — yet.

We look at many factors to help identify that inflection point:

4. Liquidity: Institutional fund managers seem to be all in (only 3% cash), while Investors are at only median levels of equity exposure. Liquidity is still abundant, free money abides. Money flows for the past few months have gone into US equities — that is a new element — at about $2B per week.

5. Internals: The market technical/internals remain constructive: Breadth and momentum are positive. New 52 week highs are also strong. Earnings are supporting some of the move, as year over year comparos are absurdly easy. The uptrend remains in place, and until it is broken we maintain an upside bias.

6. Sentiment: The biggest risk is the unusually high level of bulls. Note however that even that has moderated over the past week. We are not at the sorts of extremes yet that make the contrarian in us scream SELL.

…..read about the US Macro-Economy HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair