Daily Updates

three major bears that are threatening

We have been warning you that the U.S. economy is still sinking fast despite massive government spending, lending and guarantees.

In fact, there are a growing number of uncertainties facing our economy and financial markets today … fully three years after the financial crisis began.

There’s no escaping the impact this is having on fragile financial markets either.

With both negative and positive crosscurrents buffeting the markets each and every day, it’s no wonder we’re witnessing such extreme UP and DOWN moves in stocks!

We’ve never seen such a sharp split in market sentiment either that has led directly to growing tensions in financial markets.

In fact, all year markets have been twisting and turning wildly. One thing is abundantly clear about today’s market climate … sharp volatility is likely here to STAY!

Let’s face it; volatility has become the new normal. There is no question this can be frustrating, because wild swings make it all the more difficult to earn consistent returns.

But rather than offering only a doom-and-gloom investment scenario, today’s uncertain markets can present unique profit opportunities as well. Remember, there are always alternatives … IF you’re willing to follow the right investment strategy for your needs.

Let me explain some of the key steps we’re taking at Weiss Capital Management to cope with market volatility …

For starters, if recent history is any guide, then the old familiar set-it and forget-it strategies of the past may no longer work successfully for you. Your portfolio may end up where you started with little or nothing to show for your efforts.

Instead, adjust to the new market reality — and potentially profit from volatility — by considering an entirely new and different investing approach.

Here are five key steps for investing in volatile markets …

Step #1 — In volatile markets, it’s better to be safe than sorry. This does NOT mean you must abandon markets altogether … it DOES mean that investing today requires harder work to earn consistent profits. Plus, you must recognize that market risk is higher than normal.

Recognize that lower returns are likely in the years ahead. Don’t count on simplistic buy-and-hold strategies … and don’t take on additional risks just to gain a small increase in overall returns — especially with the core part of your portfolio.

Step #2 — Be more flexible with your portfolio, but highly selective about new investments. Don’t take anyone’s recommendations or claims about performance at face value. Ideas are a dime a dozen these days, doing your homework is absolutely critical.

There are still ample opportunities to grow your wealth in today’s difficult markets, but you may need to look for specialized ways to take advantage of volatile markets.

Step #3 — Grab gains off the table sooner … AND be willing to cut losses quicker in effort to preserve your wealth. Consider working with an investment advisor who is experienced using inverse mutual funds or ETFs to help you hedge against downside risks or even profit from them with your speculative capital.

Step #4 — Expect overall market volatility to run rampant in the years ahead and adjust your investments accordingly. Depending on your personal risk tolerance, you may want to consider hedge-fund-like strategies that allow you to earn potential gains as markets fluctuate both up AND down.

Sherri Daniels,

President

Uncommon Wisdom

This investment news is brought to you by Uncommon Wisdom. Uncommon Wisdom is a free daily investment newsletter from Weiss Research analysts offering the latest investing news and financial insights for the stock market, precious metals, natural resources, Asian and South American markets. From time to time, the authors of Uncommon Wisdom also cover other topics they feel can contribute to making you healthy, wealthy and wise. To view archives or subscribe, visit http://www.uncommonwisdomdaily.com.

We’ve gathered a lot of new readers to the Pierce Points list the last few weeks. Glad to have you with us.

You’ll find there are certain themes that reoccur often in this missive. One of them is U.S. credit.

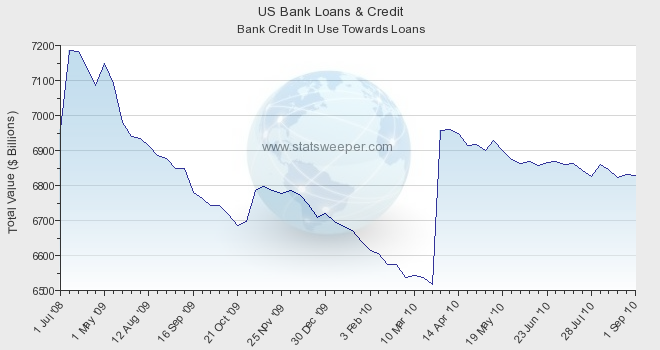

Analysts look at a lot of different numbers to try and figure out which way the global economy is heading. I have a handful that I think cover most of what anyone needs to know. And by far the most important is loans outstanding in America.

Here’s why. Between 1983 and 2008, the economic boom in the U.S. (and largely the world) was accompanied by massive credit growth. Loans outstanding at U.S. commercial banks jumped from $1 trillion to nearly $7.5 trillion in just 25 years.

Credit growth was particularly pronounced between 2003 and 2008. Those five years alone accounted for $3.5 trillion in new loans issued in America.

The interesting thing is this steep jump in loans coincided very closely with China’s “coming of age” as an economic superpower. As Americans borrowed more, they bought more. And increased consumption led to increased imports, particularly from Asia. Helping economies like China super-charge themselves.

Now here’s the rub. Credit growth in America is broken. Since late 2008, the U.S. has seen its first deep and protracted decrease in loans outstanding in the last 40 years. The chart below tells the story well (the “spike” in credit early in 2010 was caused by new accounting rules which brought off-balance sheet loans back onto the books at commercial banks).

If you factor out the accounting adjustments, loans outstanding have fallen by almost $1.5 trillion in just two years. A phenomenal decrease in credit, and thus American spending power.

The most interesting thing is this indicator has not recovered. While investment inflows in many sectors this year have lifted stocks, commodity prices, and trade numbers, loans have continued to fall.

Americans are not borrowing. Even low interest rates can’t make them. Meaning the engine that drove the last few decades of growth is now broken. Without such support, it’s going to be difficult (probably impossible) for America to return to the surging economic times it enjoyed leading up to 2007.

It’s this chart that makes me skeptical on any claims we’re on our way back to a rosy, pre-financial crisis economic world. The financial landscape today in America is much different than it’s been for most of recent memory.

The only encouraging point is loans haven’t been disappearing as fast as they were. Over the last three months, the trend has flattened.

This could help stabilize things. But it’s sure not a recovery. With this indicator lagging, we’re not going to get back to the good old days anytime soon.

Here’s to spending within your means,

Dave Forest

dforest@piercepoints.com

To Sign Up to Dave Forest’s Pierce Points Free Daily E-Letter go HERE

Dave Forest’s analysis on the natural resources sector has been featured on BNN, Kitco.com, Financial Sense and the Daily Reckoning. He has been a recent speaker at conferences in Calgary, Chicago, Las Vegas, Toronto and Vancouver. He is a professional geologist and formerly advised a worldwide client base on oil/gas, mining and renewable energy at Casey Research LLC. Dave currently serves as managing director of Notela Resource Advisors Ltd.

From today’s Financial Times: Gold prices have pushed to a fresh record amid forecasts that central banks will be net buyers of bullion this year for the first time in two decades, the clearest signs of rehabilitation of bullion after the financial crisis.

The shift marks a turnaround after disposals by European central banks over the last 10 years., when gold was seen as non-yielding unattractive asset. Monetary institutions then swapped their bullion for yielding sovereign debt.

Russell Comment –– The know-nothings at the central banks sold their gold at multi-year low prices. Now they are buying back gold near record highs. And these are the yo-yos who are charge of our money. Dow Theory Letters

Precious Metals: Your Game Plan Going Forward

In my last commentary I quickly covered the current outlook of gold, silver, the mining shares and the juniors. The breakout in the sector continued today as gold reached a new high and the mining shares (as per the HUI or GDX) closed near a nine or ten month high. The juniors (GDXJ) and silver continued higher. Most important, both GDX and GDXJ gapped higher and made strong closes and on large volume. Everything is on track and there is little reason to think otherwise.

However, to keep things on track one should have a plan.

…..read the plan HERE

Soros Sees Upside in Gold, Warns of Volatility

In an exclusive interview on Sep. 15 with Thompson Reuters (clip below), Soros says that gold is the ”ultimate bubble,’ and that “this is a period of great uncertainty so nothing is very safe.”

“[In a deflationary environment], Gold is the only actual bull market currently. It just made a new high yesterday. In the present circumstances that may continue. It will be very interesting to see if there is a decline in the next few weeks because practically everything that makes a new high almost immediately afterwards reverses and disappoints.”

“I called gold the ultimate bubble which means it may go higher but it’s certainly not safe and it’s not going to last forever.” – George Soros

Soros first made the “ultimate bubble” comment on gold back in January at the World Economic Forum in Davos, Switzerland. However, his hedge fund–Soros Fund Management LLC–still held 5.24 million shares of the SPDR Gold Trust (GLD), a stake worth about $650 million, and equity holdings in miners of gold and other minerals worth almost $250 million as of June 30. Soros was the third-largest fund in the Gold Trust ETF at the end of the second quarter.

So, it seems Mr. Soros still sees upside in gold, but was warning of the metal’s volatility instead of a bubble burst. Fundamentally, the current global macro environment–prospect of a synchronized slowing growth coupled with ongoing financial turmoil– and supply/demand are also quite supportive of gold.

From a technical standpoint (see chart), $1,300 range looks to be the next resistance with support at around $1,255.

Gold Bubble? Think Again

With gold hitting all-time highs, some are calling gold a bubble. Oh, really?

Gold is a currency. And just like other currencies, we cannot talk about gold in isolation from other currencies. For example, we do not say the yen is expensive. Rather we say the yen is expensive relative to the dollar. So when people say that gold is high or in a bubble, I say, ‘relative to what?’. To see if gold is in a bubble relative to the U.S. dollar, let us look at some historical stats:

….read more HERE

A price war is breaking out in the exchange traded fund (ETF) industry. While it’s not good news for everyone — ETF sponsors, for instance — investors can now get more for their money than ever before! And that makes you the winner of this war.

I talk a lot about the many advantages of ETFs. Very little in this world comes for free, though, and that includes ETFs. The people who design, create, operate and distribute these instruments don’t work for free. Nor should they. But consumers always want value for what they spend, and rightly so.

Today I’m going to tell you a few things about the costs of owning an ETF. As you’ll see, some kinds of expenses are more important than others.

ETF Costs, Inside & Out

The costs of an ETF fall into two broad categories: Internal and external.

Internal costs are the expenses of running the ETF itself. Typically they are paid to the sponsor or other service providers, like lawyers and accountants. These cover things such as management fees, regulatory registration and auditing. Investors never really see these costs because they come out of the ETF assets via the expense ratio of the fund.

External costs are paid separately by investors and are not extracted from the fund. The most common external cost is the commission brokers charge when you buy or sell an ETF.

The good news is that both kinds of costs are falling fast. Why? Part of it is the deflationary economic climate. Wages and many other costs are flat or falling. But the primary reason is growing competition in the ETF industry …

Less than five years ago, at the end of 2005, there were just 224 ETFs and ETNs listed for trading on U.S. stock exchanges. The quantity has more than quadrupled since then hitting 673 by the end of 2007 and 925 last year. So far this year we’ve seen an increase of 130, pushing the total to 1,055.

A few months ago I told you how ETF overload has led to practically identical ETFs from different firms jockeying for a limited audience. And the competition just keeps on growing. I’m sure there will be a shakeout at some point. But for now expenses are one of the few ways sponsors can distinguish their offerings.

For example, just this month Vanguard launched nine new ETFs including Vanguard S&P 500 (VOO). This is a direct attack on the grandfather of all ETFs, SPDR S&P 500 (SPY). SPY alone accounts for about a third of all ETF dollars traded every day. Now VOO is available to cover the same large-cap index at an estimated annual expense ratio one-third lower: 0.06 percent vs. 0.09 percent for SPY.

You might think an advantage of only 0.03 percent a year is negligible. And you’re right. Three basis points on a $100,000 account — which is probably more than most people can or should allocate to any one type of ETF — is only $30.

On the other hand, if you are an institutional portfolio manager with a billion dollars to invest, the difference is about $300,000 a year — enough to buy an exotic sports car.

What about those external costs, especially trading commissions? Well …

Zero Commissions Are Here!

When the price hits zero it is safe to say trading can’t get any cheaper. And that’s where we are — at least for some investors in certain funds.

Three top firms — Fidelity, Charles Schwab, and Vanguard — now have commission-free ETF trading programs. Buy and pay zero. Sell and pay zero. Do it all over again and pay zero. Nice.

There is some fine print, of course. Each program applies only to selected funds. At Schwab and Vanguard, zero commissions are only for their in-house brand of ETFs. At Fidelity, you can trade for free in some of the iShares ETFs as well as the firm’s one proprietary ETF.

There are other restrictions, too. But I’m guessing they will ease over time. ETF sponsors have figured out that their business is now commoditized. One large-cap growth index fund is as good as any other in many cases.

The differences that attract investors relate more to the bottom line after expenses.

f you were actively investing back in the 1990s, you might remember how revolutionary it was when Schwab introduced their “OneSource” no-transaction-fee mutual fund marketplace. I think something similar will develop for ETFs. Furthermore, trade processing, whether stocks or ETFs, is now so automated that the incremental cost for the broker is negligible.

The sponsors affiliated with brokerage firms, like Schwab, will initially favor their own ETF brands. Yet they won’t be able to sustain that model for long. Once investors have a taste for commission-free trading, it will become as expected as free restrooms in service stations.

And if you don’t have it, your customers will go somewhere else.

We’re not to that point yet. Right now you’ll still end up paying for your ETF trades in most cases. However, you can pay quite a bit less if you shop around.

Best wishes,

Ron

Ron Rowland is president and a founder of Capital Cities Asset Management. Mr. Rowland is widely regarded as a leading ETF and mutual fund advisor as well as a sector rotation strategist. In addition to his roles of President and Chief Investment Officer of CCAM, he is Executive Editor and Publisher of the All Star Fund Trader, a highly regarded investment newsletter in its 18th year of publication.

You may have read about Mr. Rowland and his strategies in publications such as The Wall Street Journal, The New York Times, Investor’s Business Daily, Forbes.com, Barron’s, Hulbert Financial Digest and many more. Outside of CCAM, Mr. Rowland served on the Executive Committee of Austin’s American Association of Individuals Investors (AAII) and led the mutual fund special interest group for numerous years.

As a former mutual fund manager from 2000 to 2002, Ron was a pioneer in using ETFs inside of mutual funds. He also served as the manager of a hedge fund from Aug. ‘93 to Dec. ‘94. His formal education includes a BS in Electrical and Computer Engineering from the University of Cincinnati in 1978 with additional studies in the same field at the University of Texas from 1978-1981.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair