Daily Updates

Gold – GDXJ Junior Gold’s & GDX Gold Miners

GDX Market Vectors Gold Miners

HAC took a position in GDX towards the beginning of July. This has proven itself to be a very good entry point. Gold stocks have performed very well, but investors should note that the seasonal period for gold stocks is typically from July 27th to September 25th. Gold the metal has a similar period with its seasonal period lasting from July 12th to October 9th.

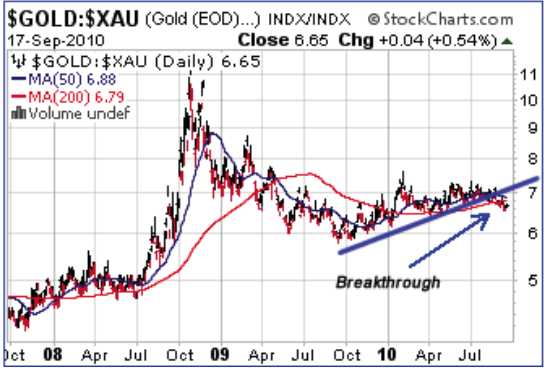

This year gold stocks are outperforming the bullion, despite bullion reaching all time highs. The gold (bullion) to gold stocks ratio chart illustrates that gold stock have recently started to outperform bullion. This is good news for the sector.

The difficulty with GDX is that October tends to be a weak period for both gold and gold stocks. In the past this has largely been the result of the European Central Banks, at this time of year, allocating the amount of gold each country can sell throughout the year. Historically, this has caused a the gold price to fall as the banks were eager to sell. Times have changed, and the central banks have not been selling their gold.

GFMS (Gold Fields Mineral Service) predicts that the world’s central banks will be net buyers of gold for the first time since the late 1980s. In fact, only the International Monetary Fund appears to be a seller this year – its latest deal is a sale of 10 metric tons (321,500 ounces) this month to the Central Bank of Bangladesh (US Global

Investors).

Despite the positive dynamics for gold and gold bullion, investors should consider taking profits on the sector, particularly towards the end of the month. Using technical analysis should help in determining the if and when to exit the sector.

It is important to note that gold also does well during November and December. Historically, it has underperformed the markets, but it has been positive. Large moves can occur at this time of year if there is a lot of momentum behind gold and gold stocks.

Investors can consider exiting the position for the month of October and then reassessing at the end of October to determine if reentry is justified.

GDXJ Market Vectors Junior Gold Miners

HAC entered GDXJ (junior gold stocks) at the beginning of August and the sector has basically shot straight up. It has outperformed bullion and senior gold stocks, as junior companies have been the targets of takeovers.

The same seasonal comments that applied to GDX apply to GDXJ.

Upcoming Opportunities:

Most of the seasonal opportunities for October will be discussed in the next newsletter.

There are two sectors that investors should watch and consider in the second week of October if the market warrants such action – the technology sector and Canadian banks. The next newsletter will be published at the time when these sectors can start their outperformance and I will comment on theses sectors at the time.

Subscribe to the Thackray Market Letter: To subscribe send an email to subscribe@alphamountain.com with SUBSCRIBE in the subject line. Also state your fi rst and last name, city and country.

Brooke Thackray is a Research Analyst along wth Don Vialoux for the Horizons AlphaPro Seasonal Rotation ETF that trades under the symbol HAC on the Toronto Stock Exchange. The objective of HAC is long-term capital appreciation in all marketcycles by tactically allocating its exposure amongst equities, fixed income, commodities and currencies during periods that have historically demonstrated seasonal trends. The Thackray Market Letter is for educational purposes and is meant to demonstrate the advantages of seasonal investing by descibing many of the trades and strategies in HAC.

Like many innovations in finance that emerge from nowhere to explode in popularity with unknown consequences, exchange-traded funds (ETFs) have gone from obscurity when they were first invented in 1993 to making up more than half of all the daily trading volume on American stock exchanges today. They also made up 70% of all the canceled trades during the Flash Crash on May 6, despite representing just 11% of listed securities in the United States, suggesting that ETFs remain poorly understood by both investors and regulators.

The extraordinary popularity of exchange-traded funds, open-ended mutual funds that trade like stocks on an exchange, is undeniable. However, the source of this popularity would seem to have two very different origins. ETFs are bought by many retail and institutional investors looking for low cost and highly liquid vehicles with which to buy whole indices in a single trade, and ETFs serve that noble function well. But, they are also extremely popular with and widely used by hedge funds and other traders looking for a simple way to mitigate broad-market risks, or neutralize beta, with a single trade. The appeal to a hedge fund manager of being able to short an entire market index or a whole sector with one transaction, instead of say 500 separate stock shorts to span the S&P 500 Index, makes ETFs very widely used as hedging vehicles by short-sellers. It increasingly looks like many new ETFs are now being designed for the purpose of marketing them to short-sellers.

These seemingly opposite interests in ETFs make for a large and lucrative market not just for the ETF operators like BlackRock’s iShares and State Street Global Advisors SPDRs, but also for the authorized participants–institutions that can create or redeem large blocks of new shares in an ETF (called creation units) for sale, and countless brokers that profit by trading ETF shares.

While ETFs often appear to be a benign innovation as compared to some of Wall Street’s arcane derivatives, a closer look at the mechanics of short selling ETFs (which have become one of the most prevalent securities to short) raises some serious concerns. While an ETF owner believes their ETF shares represent ownership of the underlying shares of stock in the index that the ETF tracks, that stock is not always all there. Because of explosive short interest in some ETFs, owners of ETF shares often far outnumber the actual ownership of the underlying index equities by the ETF operator. One might ask how that can be possible, but the creation and redemption mechanisms inherent to ETFs mean that short sellers need not be concerned about the availability of shares outstanding when they sell an ETF short—since they can always create new shares using creation units to cover short positions in ETFs in the future. In essence, there appears to be no risk to being naked short an ETF since the short seller can always “create to cover”. This has led to some ETFs having shockingly large short interest as compared to their number of shares outstanding and for every additional ETF share sold short, there is another owner of that share.

Take the SPDR S&P Retail ETF (NYSE: XRT) as an example. The number of shares short was nearly 95 million at the end of June, while the shares outstanding of the ETF were just 17 million. The ETF was over 500% net short! Or to look at it from another perspective, the ETF’s operator, State Street Global Advisors, believed that there were 17 million shares of the SPDR S&P Retail ETF in existence and owned shares in the S&P Retail Index portfolio to underlie those 17 million ETF shares. But, in the marketplace there were another 95 million shares of the ETF owned by investors who had purchased them (unknowingly) from short sellers. 78 million of those ETF shares were naked short–the short seller had promised their prime broker to create those non-existent shares if necessary to cover their short in the future. In both cases the share buyer, however, is completely unaware his ETF shares were purchased from a short-seller and no doubt assumes the underlying assets in the index are being held by the ETF operator on his behalf, but no such underlying stock is actually held by anyone. Clearly this creates a serious counterparty risk and quite possibly the potential for a run on an ETF—where the assets held by the fund operator could become insufficient to meet redemptions.

Even more alarming was the recent rate of redemptions from the SPDR S&P Retail ETF in July and August 2010. Redemptions occur when more owners wish to sell out of their holding in the ETF than there are new buyers for the existing shares, so unwanted blocks of 50,000 ETF shares each are redeemed through the authorized participants with the ETF operator for cash, or more typically for in-kind shares in the ETF’s underlying index’s stocks. The SDPR S&P Retail ETF was one of the fastest contracting ETFs in July due to redemptions and as of July 31, it had just 7 million shares outstanding. However, the short interest was little changed—still over 80 million shares short. Suddenly, 11 times the number of shares outstanding was short, which is even more worrisome than 5 times back in June. By late August, the shares outstanding in XRT had dipped briefly below 5 million shares with 80 million shares still short (16 times the shares outstanding). Mercifully, net buying interest has rebounded somewhat for the SDPR S&P Retail ETF with the improving outlook for retailers and shares outstanding in XRT had rebounded to 12 million by mid-September. But if the rate of contraction last month had continued, the ETF was just days away from running out of underlying shares altogether.

So what happens if the recent monthly redemption rates return and 15 million more shares in the ETF were redeemed by the end of this month? Presumably the SPDR S&P Retail ETF would simply close and cease to exist once its remaining 12 million ETF shares outstanding had been redeemed and all its underlying equity holdings had been delivered to redeeming authorized participants. But where does that leave all the ETF owners who unknowingly bought their shares in the ETF from naked short sellers? If the ETF is all out of underlying equities and is essentially shut down, what happens to the remaining owners of the 80 million shares of the ETF? The ETF operator would have no more underlying shares (or cash) in the fund and the ETF would have essentially collapsed since all the shares outstanding were already redeemed. At recent prices the unfunded remaining ownership in the marketplace for which nobody currently owns any shares would be over $3 billion for just this one ETF! Extend this hidden unfunded liability from massive scale short-selling of ETFs (both traditional and naked) across the entire ETF spectrum and it is a $100 billion potential problem.

Who gets left holding the bag? Is it the retail account holders who own defunct shares in a closed ETF? The prime brokers that were counterparties to all those short sellers? The hedge funds that sold non-existent shares in an ETF assuming they could always be created another day? The ETF operator? Or the Federal Reserve?

Taken from the Financial Times Blog @ http://ftalphaville.ft.com/

Authors of The Study:

Andrew A. Bogan, Ph.D. is Managing Member of Bogan Associates, LLC, a global equity fund management firm based in Boston, Massachusetts.

Brendan Connor is an investment analyst in New York City.

Elizabeth C. Bogan, Ph.D. is Senior Lecturer in Economics in the Department of Economics at Princeton University in Princeton, New Jersey.

Has silver been coupled to gold?

For the last few years silver has moved in relative tandem with the gold price up to now. We called it the ‘long shadow of gold’ because it would rise further and fall further than gold, but they did move together. Occasionally silver did pause as gold rose but the ‘shunt’ effect [when a train pulls forward with a line of carriages in tow and each jumps forward as their links tighten] kicked in and it jerked forward to catch up with gold’s moves. Many investors keep their eyes focused on the Gold: Silver Ratio [one ounce of gold buys x number of ounces of silver] and trade it regularly. Right now that ratio is at 1: 60. However, by coupling we also mean will they continue to act and react together on a daily basis, apart from price differentials.

Moving together

When it comes to market prices moving up and down and sideways together, we are not looking at the commodity aspects of the metals, but the market perception that these two are precious metals that were money for the bulk of man’s history. Savings were expressed almost entirely in these metals and once deemed as the only valid money around.

Money or Precious metals?

This is where the relationship between the two metals is anchored. Despite any industrial or jewelry [solely for decoration] uses that do not relate to wealth retention, gold in so many parts of the world is considered money. The developed West does not consider it so, even in the face of over 30,000 tonnes of gold held in central banks worldwide and many central banks now buying it. But even developed world central banks are keeping a firm hold on what they do have. So we must ask, are these simply precious metals or do they serve some as real money. This is critical to the movements of gold and silver prices. If the overall perception of the two is of future ‘money’ [as a measure of value] then they will reflect the levels of uncertainty over fiat money. In support of this come the comments by Alan Greenspan spoken as recently as this week. At a Council on Foreign Relations meeting Mr Greenspan commented, that he’d “thought a lot about gold prices over the years and decided the supply and demand explanations treating gold like other commodities ‘simply don’t pan out’. Mr. Greenspan had concluded that gold is simply different. He said, “If all currencies are moving up or down together, the question is: relative to what? Gold is the canary in the coal mine. It signals problems with respect to currency markets. Central banks should pay attention to it”. We believe central banks are doing just that.

As we enter what could be a volatile period for international currencies as Treasury Secretary Timothy Geithner begins a more aggressive tact against China’s Yuan exchange rate [the Dollar is slipping again] and Japan intervenes to weaken the Yen, confidence in fiat currencies ability to truly measures value is waning. That’s why the two are moving together and will do so in the future.

We qualify that to some extent, as some fundamental factors affecting the two precious metals are affecting the silver price in particular [see below].

Another change is emerging in the silver market in the developing world. In both India and China amongst smaller investors, silver is far more affordable as the gold price roars out of their range. So the concept of silver being the ‘poor man’s gold’ is rising fast and showing itself in the rapidly rising demand for silver in those nations. This represents a small but significant diversion of demand away from gold to silver as prices rise for the two metals.

Silver prices affected by fundamentals

Gold has seen a halt to central bank selling in the first year of the third Central Bank Gold Agreement. Silver has only now seen an end to ‘official’ selling by India, China and last of all Russia. This has allowed a good source of supply to disappear and forced the buyers of that silver to go to the open market to get its silver. In addition, the decline in uses in photography is being overtaken in the new uses for silver in solar panels, ‘rfids’, medicine and other electronic uses. All this silver is being consumed and will be until its monetary role in the long-term prices it out of the consuming markets and, like gold, it is simply stored not consumed. Most of you will not believe that is a possibility. The net result of these two changes in silver’s fundamentals will be for silver’s price to rise much faster than the gold price in percentage terms.

It is not our purpose to detail where the silver price is going [that has to be reserved for Subscribers] but we can say that we expect a narrowing of the gold: silver ratio.

De-Couple?

We do not think that the gold and silver prices will de-couple in terms of moving in relative tandem, but in percentage terms there will be a widening of that coupling.

As to where the silver price is headed, we find ourselves at odds with most analyst’s forecasts, but as we said above that is for…..

Subscribers only – Subscribe through www.silverforecaster.com and www.GoldForecaster.com

I turned 60 a year ago, pretty much a year after the economic meltdown of August 2008. For my birthday, I decided it would be wise to rethink my retirement plan, which at the time was “work until I dropped.” Back then my savings account had a balance of $5, my IRA was valued at $3000, and Social Security would give me around $800 a month if I started collecting at 62½.

The first decision was how to approach putting away enough money to retire. There were two paths: go after a big score, a lump sum sufficient to retire on; or set up multiple revenue streams of $500/month here, $1200/month there, $900/month over there, etc. so that there’s enough money coming in each month to live comfortably.

Since my track record on get rich quick projects wasn’t successful (otherwise I wouldn’t be in the predicament I was in) I chose to attempt to setup multiple revenue streams. So far I’ve invested a total of one thousand dollars of my own money and have four sources of revenue streams that are online and growing. I’ve also strengthened my core entrepreneurial endeavor and have had back-to-back, my two most successful years ever.

The key to me pulling this off is not that I’m a slick salesman. I’m anything but. Last week I talked about the importance of offering customer service. I go beyond traditional customer service. I’m more than fair with my clients; I work with them on price to keep things within their budgets while delivering what they need to make sure the project is successful. It’s reverse greed, or at the least the absolute opposite of corporate greed.

It’s pretty simple: my success can only happen if my clients are successful, otherwise where does my income come from? Social Security is not yet a viable option. Therefore, whatever I can do that is of benefit to my clients is of benefit to me. Sort of like the enemy of my enemy is my friend.

This is the Living Vision — you’re detailed vision of YOUR future. For instance, “I envision myself living in a safe neighborhood, in a protected home, with myself and my valuables safe and secure.” It’s positioning yourself correctly — both strategically and ethically. The latter is important. The people of the United States are very angry right now. I submit that whether they know it or not, what they are angry at is the greed that put us in this s—storm. Corporate greed that plundered the middle class. Wall Street greed that raped and pillaged the middle class. Political greed that sold the middle class down the river. Personal greed that convinced us to buy houses we really couldn’t afford. Reverse greed; it’s why I’ve been successful.

When people are feeling they are getting screwed every time they walk out the door, you will be successful as soon as you can figure out how to dispel those feelings. Your Living Vision is your strategy for doing so. Here’s a hint. If you’re not a “me first” person, if you’re not greedy, then you can just be yourself to achieve your Living Vision, and that makes everything a whole lot easier. If you give to get you won’t see any rewards. If you give to help, you will reap enormous benefits.

One other thing. Surround yourself with positive people. Economic collapse, the Greater Depression are certainly possible, maybe even probable [maybe even underway as you read this — ed.]. Economic strain is much more likely to affect you adversely if you give into gloom and doom, surround yourself with people who are negative, and don’t create a Living Vision. Your Living Vision is your way out of “here.”

Certainly there is plenty of blame to go around for how we got into this mess. But getting angry about it, participating in the anger won’t solve anything on the grand scale and will divert your attention and energy from what’s important: your survival. You can’t help anyone, not even yourself, if you are not doing better than just surviving. The key is to disengage from Wall Street, politics, big business — the centers of greed and corruption that will suck the last drop out of you if you play their game. Disengage and play your own game with your own rules.

I hope the majority of those reading this are younger than me. You still have time. Here’s some free advice from an elder; remember, I’m not old for nothing. Start creating revenue streams today…or at least start strategizing about them. Nobody knows what the future will bring so diversity is a good thing; both in life and in business.

And that’s where “The Fall of America and the Western World” comes in. Not only does it explain how we got in this mess, and the likelihood that the best-case scenario is that things never improve — at least not for most of us — this movie also starts you thinking. So start thinking. Come up with your own Living Vision. I recommend “The Fall of America and the Western World” to get your thought processes going.

Regards,

Henry Daniels

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair