Daily Updates

Excerpt from Today’s Letter – whole letter HERE

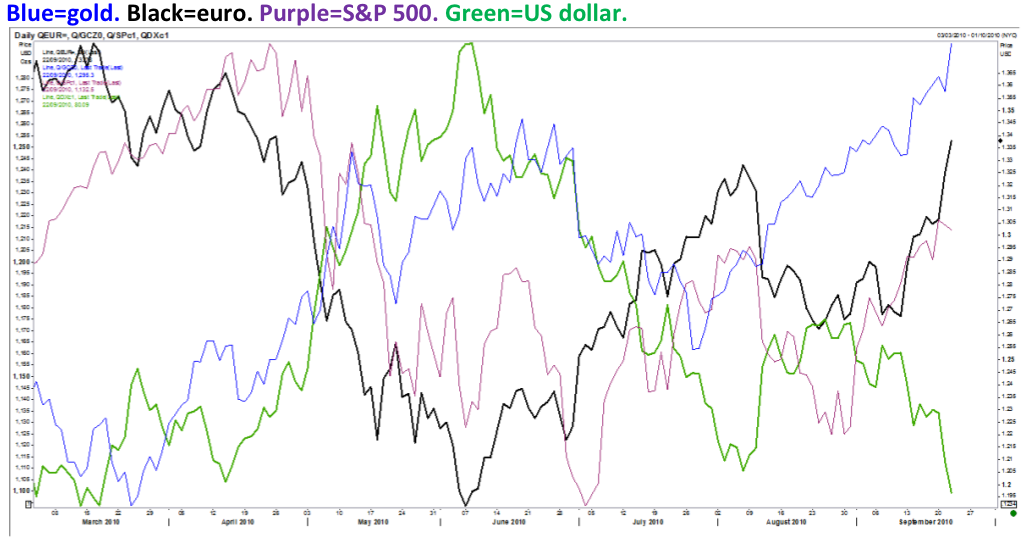

Did you get that? The point is: the Fed’s telegraphed position does not bode well for the US dollar.

There is the obvious poor performance of the US dollar telling the story; but there’s a little more to watch … like the performance of gold. A very broad, long-term theme we still hold to by a few threads is one where the US dollar rallies on major risk aversion. More than likely such an environment will again be sparked by trouble first out of the Eurozone and then less confidence in China.

Gold is taking a bite out of that theme, as the risk-averse dynamics seem to favor gold over the dollar lately.

Larger chart HERE

Perhaps it’s not even being debated, but gold’s move is an absolute safe-haven play that’s capitalizing on investors’ distaste for, or rather their negative perception of, major fiat currencies; nothing more. And the fact that the S&P 500 price action in the wake of yesterday’s Fed move is not sending its own signal of risk appetite (while risk currencies are stronger and US Treasuries are stronger) underscores investors’ distaste for dollars. It may take a Halloween sugar-high to get the dollar moving up again. Unfortunately for the buck, that scary day is more than a month away.

Key Point that Could Change this Quickly: China. It seems US-Chinese relations are getting worse. The saving grace for the buck would be a risk bid. We can’t guess or forecast that … but we have to keep that in mind.

…..read Jack’s whole letter on the Dollar, Euro & Gold HERE

Investing in the Paris Basin Shale Oil Play

The Paris Basin shale oil play in France has the potential to be ten times the size of the Bakken play in North America, and some high profile exploration is beginning soon.

Estimates range from just a few to many tens of billions of barrels of oil in the Paris Basin. Much like the North American shale plays, these formations have been drilled through many times – there are over 1000 wells drilled into the Basin – so exploration risk is low. It’s completion risk – how to best unlock the oil from the rock – that is the main risk.

So there is a lot of data, which makes exploration much less risky. It also means that local residents are used to having oil wells drilled in the region – unlike New York State ;).

Activity by explorers in this part of France has been growing, and is now hitting a fever pitch. A huge land race is underway, with applications for more than 1.6 million acres pending approval for several companies, including Toreador Resources (TRGL-NASD) in the US, Vermillion Energy (VET.UN-TSX) and Realm Energy (RLM-TSXv) in Canada.

Exploration – real drilling – in the Paris Basin will ramp up this fall. Toreador Resources Corporation is the purest play. In May they announced an exploration deal with Hess Corporation (HES-NYSE) that could be worth as much as $265 million for 50% of Toreador’s 600,000 acres in the play. They spud their first well into the play in Q4 2010. It will be one of the most watched wells in the world.

Canada’s Vermilion Energy has also acquired acreage in the play and begun exploration activities. Vermilion is already recognized as France’s largest oil producer.

Craig Steinke, Executive Chairman for Realm Energy, says “The Paris Basin is arguably the most exciting shale play in Europe right now. We expect to acquire a good-sized position in this play.”

As I wrote about earlier, many of the European shale gas plays are being bought up by the majors, there are intermediate and junior producers in the game, which should keep news flow on the play steady for retail investors.

When this happened in North America, there was huge wealth creation as the juniors and intermediates were small enough that their stocks could benefit from a productive land position.

Like the big North American shale oil plays that enriched investors, the Paris Basin has big reserve potential, good existing well data, and a local population that’s familiar with drilling.

Hopefully, history will repeat itself.

*Keith Schaefer owns Toreador

Hello, this is Keith Schaefer, editor and publisher of The Oil & Gas Investments Bulletin. I started my subscription service in mid-2009 because I could see there was no place where retail investors could go to easily find which oil and gas companies were creating huge shareholder wealth by using exciting new technologies, such as horizontal drilling, fracing and 3D seismic.

These companies are increasing cash flows – and stock prices – by finding ways to get more oil and gas out of the ground. And junior and intermediate producers – $2-$20 stocks – are leading the way.

I find the leaders in the new plays that are using these technologies. My research is finding higher and higher flow rates from new wells in old formations as management teams fine tune their use of these new technologies.

It’s amazing how technology is lowering operating costs – and increasing profits – for many publicly traded energy companies.

I find the ones who have the capital and the knowledge to be the fastest growing in their area – this usually means they have a large undeveloped land position in an area where either production costs are very low or production rates can be very high. They are covered by several research analysts, so there is research support and institutional money flow behind them.

Investment guru Jim Rogers in a long comprehensive interview.

Would you be cautious on the Indian markets at the current levels or does everything seem to be hunky-dory?

I am always cautious whenever I am doing anything. The US and the Japanese central banks are intended to print a lot more money around this time. Money supply in the US has grown nearly 8% a year in last months and the Japanese two weeks ago made it clear that they were going to print more money. So we have this money flowing into the world and obviously it is going into the market. Your government, your central bank are going to be more cautious and I hope they are, but in the meantime, the money is going to go somewhere and it is going into stock markets around the world.

How much the market can go up? What kind of an upside could this money really lead to?

I am cautious because as the markets go higher, either they are going to have to continue printing money or come to the currency market from the bond market eventually. My way of playing is to be long commodities because either way whether the world gets better or does not get better, commodities are going to do well. I worry about stocks because I only see the stock markets are pretty high around the world, including India.

Since you mentioned that you would be bullish on commodities, what is it that excites you right now if indeed equities as an asset class does not, especially in India? What is it in the commodity space that you like at this point of time?

Fortunately or unfortunately, depending on how you look at and many of them are going up a lot, cotton is making new highs, sugar has been growing up, and gold you know what has been going on in the markets. I would look at things that have not moved up this much. Buy silver than gold, for instance, if you want to buy precious metal. I would like to buy coffee than some of the things that have moved up so much, but there is still a huge potential. If governments are going to continue to print money, we are going to have higher prices for commodities though you may not have higher prices for stocks somewhere down the road, but as long as you require money, it is going in the commodities, among other prices.

Among commodities, you still believe that despite the run up that we have seen in gold, there is more headroom out there?

….read more HERE

Tony Boeckh’s 4 Different Investment Scenarios:

1. The bull market in gold has just begun.

2. We are headed for a deflationary depression in which high quality bonds would continue to thrive.

3. We are heading into high inflation and a dollar collapse.

4. There will be a return to the good old days of stability and growth.

Zero Hedge’s comment on Tony Boeckh’s 15 page newsletter:

“All in all, some good observations”

…..read or skim the 15 page report & charts at Zero Hedge HERE (click on the Scribd Download, print or Fullscreen button for the entire letter)

Dow Theory non-confirmation

The August highs for the Averages were —

Industrials — 10698.75

Transports — 4516.35.

Today, the D-J Industrial Average closed at 10761 — 63 points above its August high.

Today, the D-J Transportation Average closed at 4511 — 5 points below its August high.

Talk about a “squeaker”! Thus, today, by a smidgen we experienced a classic Dow Theory non-confirmation. What does this mean? We should know by the end of the week. – One of the best values anywhere in the financial world at only a $300 a year, to get his DAILY Dow Theory Letters subscription HERE

Peter Schiff, Why It’s Time To Dump Most US Stocks

Stocks are widely believed to provide inflation protection since factories, equipment and inventories rise in value as prices generally increase. Historically, stocks have in fact tended to rise with inflation rates, but too much inflation has caused volatility and raised a question as to whether stocks really are a reliable inflation hedge.

Stocks in certain sectors have similarly earned a reputation as recession protection. Stocks designated as “defensive” are those in industries that make stuff we’ve simply got to have, such as food and drugs, or items in the category of “sin,” referring to things we may not need but will kill to get – traditionally tobacco and alcohol, and perhaps other things to newer generations.

Such rules of thumb are based on common sense and will always be valid, although whether they result in gains, simply lower losses, or neither, depends on the severity of the recession, the urgency of the demand and a lot of other factors that change as a downturn proceeds.

Of course, we are not talking here about mild inflation or a minor recession except as early or late stages of the main event. The situation we are facing is of a magnitude comparable to the Great Depression of the 1930s and the next-worst bear market, the stagflation period of the 1970s. There are parallels to both cases, but also ways in which the current crisis differs significantly.

….read much more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair