Daily Updates

Ed Note: Michael Campbell calls Greg Weldon – “The One Analyst other Analysts can’t Wait to Read.”

Our research indicates that the phrase “like two peas in a pod” was first used, in literary form, within the 1580 publication of “Euphues and his England” to describe the “Twins of Hippocrates” …

… “Wherin I am not unlike unto the unskillful Painter, who having drawen the Twinnes of Hippocrates, who were as lyke as one pease is to an other”

Appropriate, even in the ‘old-school’ Tudor ‘script’ … that this phrase originates in the UK, giving us a segue to our macro-theme for the day, derived from data released in the last twenty-four hours in “England”, and, in Canada … where the macro-peas look eerily similar. (article written Sept. 11th)

Indeed, RECORD TRADE DEFICITS in both countries.

And, RENEWED DEFLATION IN HOUSE PRICES in both countries.

In this vein, on the back of this specific macro-data, England and Canada are “as lyke as one pease is to an other.”

They are … two peas in a pod.

We shine the spotlight on the following features:

…. Canada posts RECORD trade deficit in July, as Exports fall, and Imports rise

….. UK posts RECORD trade deficit in July, as Exports fall, and Imports rise

… Canada posts DEFLATION in Average Home Price during August

…. UK posts DEFLATION in Average Home Price during August

…. UK and Canadian Deficit-to-GDP Ratios exceed (-) 3%

…. UK and Canadian short-term interest rates on the rise

…. UK and Canadian currencies continue to be debased, relative to Gold

…. Silver breaking out, priced in both British Pounds and Canadian Dollars.

Indeed, Canada and the UK are ‘like two peas in a pod’ this week, from the macro perspective.

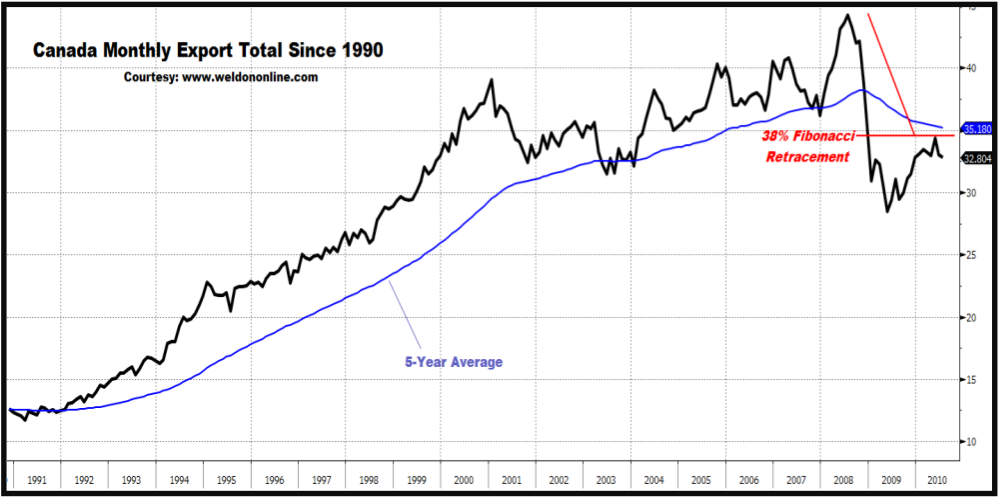

We note that Exports to the US account for a massive majority of total Exports from Canada, pegged at 74% … and … that the single-month decline in Exports to the US, at C$ 545 million, accounted for 227% of the total July monthly decline (ie: Exports to non-US countries rose). With that in mind we observe the chart below revealing the decline in Canada‟s Export during July, with the downturn taking place following text-book 38% retracement to the upside, amid a rally that failed just shy of the 5-Year Average (which continues to trend to the downside, directionally).

“Two-peas-in-a-pod … the UK and Canada … as it also applies to the data released this week for Average Home Prices, with BOTH countries posting an intensified near-term deflation dynamic.”

“Like two-peas-in-a-pod … both Canada and the UK are “at war” with downward spiraling fiscal deficits.”

“With deflation still lurking as the “bigger” risk … we think global Central Banks, including the Bank of Canada and the Bank of England, will continue to promote and pursue “easy money” policies, regardless of the fiscal dynamic.”

We remain bullish on several commodities and the Agricultural sector in general via the ETF markets.

For a look at the entire 13 page with 18 Charts Weldon Money Monitor focused on Canada Weldon’s Money Monitor offers a FREE 30 Day Trial Subscription. For subscription information Visit www.Weldononline.com for a FREE Trial. Or contact Eileen @Weldononline.com

A FREE 30 Day Trial Subscription is defined as a single Trial that is limited to a one-time Signup. Signing up for multiple trials under different names, Fraudulent contact information is illegal. Weldon’s Money Monitor takes this seriously..

Michael Campbell: My guest today is Ryan Irvine of Keystone Small Cap Research Services that looks for companies that may not be large enough at this point to be owned by an insurance company, a major mutual fund or a pension fund that needs buy millions of shares. Ryan looks for companies that aren’t there yet. They maybe on somebody else’s radar screen but they haven’t been initiated as a big buy for some of these major pools of capital. If they meet his criterion of cash flow and profitability and he doesn’t have to pay too much for them then the Keystone small cap research service is interested.

Ryan, lets start with your overall view of the market?

Ryan Irvine: We really fundamentally look at the broader market and for the last year I’d say, since a year ago September, we have really found the markets were not attractive at any given point. We’ve think they’ve been relatively fairly priced. So if we look broadly we haven’t really been buying the market but we’ve been buying some select situations within the markets. Geographical areas such as within China where we see some growth, we’ve bought in some. Specific gold stocks, some specific tech stocks and some other stocks that we see specific value in. In a lot of markets it hasn’t been really cheap.

Michael: I think it was January of 09 and you were saying to us that you really thought it would be a stock picker’s market going forward. I think the market’s proven your anticipation to be absolutely correct.

Ryan: We still feel it’s really a stock picker’s market right now. And that does excite because exactly what we do is pick stocks. You really could have, literally after the March lows of 2009 you could have literally thrown a dart at the dart board and done pretty well. It when our job really becomes interesting is where we think the markets will be flat and in that type of environment what we endeavor to do is beat the market. Its a time where we can prove our worth to our clients over time and we think we’ve done that this last year and we’ll continue to do it.

Michael: I remember a stock that you’ve been recommending for quite a while on a show called Cash Store Australia Holdings Inc. on the TSX.

Ryan: Yes the specific companies are the Cash Store and Cash Store Australia. We had bought both of them just last summer this time. A good way to buy the Cash Store Australia too was to buy the Cash Store because of the fact that it owns 20% of that company. We like both companies still. To start with Cash Store Australia is the smaller one which has about 61 stores in Australia. The Cash Store is a pay day Loan Company and its Symbol is AUC on the TSX venture. It is a company that we bought at a $1:25. Three months ago sold it at $3.75. It now trades around $2.80 and right now we have a hold on it. Its parent company which we ought last year just around $7 is the Cash Store Financial symbol CSS on the TSX. It is a company that we sold half our positions at around $18 and now it’s trailed down to the $16, 16.50 range. We still like it at these levels, it’s trading at reasonable PE, good solid cash in the bank and we like the value there so we’d hold that.

Michael: One of the things I like there is that sometimes you’ll say hold this stock, other times you’ll say sell half of your stock. The Cash Store is a great example where you had more than doubled the money but you sold half of it to protect your original capital. I really, really encourage people to take what I call partial decisions like that. Don’t get frozen like a dear in the head lights saying I’m all in or all out as I think that’s a huge mistake that a lot of people make. And I hope people are listening very clearly and keep in mind when I talk about these mistakes is because I’ve made them myself so regularly. It’s been drilled into me and I just find when you start making what I call partial decisions you go okay the stock still meets my criteria, I’ve got a 1000 shares maybe I’ll sell 500. That way I’ve still got a foot in the water, I still like the company but I’ve got capital out that I can deploy else where. Your service obviously does that and I really like that approach.

Ryan: The math is simple on that. We had a stock that doubled so we sold half our position to take away all of the market risk to our original capital. Yet we can still participate in the upside going forward because we believe the company still has good values and growth for the future. We just think the Cash Store is trading at a reasonable price in the market right now and it’s fairly valued at this time.

Michael: Ryan do you have other words for us?

Ryan: Yes, a company that was part of our portfolio at the world outlet conference and a company we recommended about three months ago on the show is a gold producer named Orvana Minerals Corp it’s ORV on the TSX. the company was part of our recommended portfolio at the world outlet conference when it traded around a $1:00. We’d made a timely buy on this at 52 cents for our clients back in 2008 and we’re happy to report that on Friday the stock closed above $1.90. It is a junior Gold producer that operates in three regions, one in Bolivia, one in Spain which is its main asset and another project in Michigan. Now Orvana for us is a bit of a departure in the junior mining business having built its business and portfolio through internally generated cash well not by constantly tapping the market with shares and diluting shareholder value. We do not like companies that build themselves that way. Since 2002, this company has operated a low cost gold mine in Bolivia which given the geopolitical environment there is no small feat in itself.

Subsequently the company has used this strong cash flow base where it generated $150 million in cash to buy a gold mine in Spain at a very opportune time following the 2008 credit crash. This mine in Spain is now set to produce around 100,000 ounces of gold in 2011 and will pay back the purchase of that asset in just over two years, which is a very effective payback period. Most importantly the company has now transformed itself from a single mine producer in a poor geopolitical region into a multi-mine producer in more stable political arenas, in just a over years timeframe. Shareholders are beginning to reap these rewards in the market and the share price has nearly doubled this year. In the calendar 2011 we think the company will earn between 30 and 40 cents, a large earnings range but it’s due to the fact that two new mines are coming online during the year and there is a lot if moving parts. The company has been part of our fall 2011 junior gold and metal survey of all of producers which looks at over a thousand mining companies based on production growth, asset based revenue earnings growth and comparative evaluations. We run the numbers on about 50 producers and rank the top five to ten recommendations and we can tell you that Orvana, despite its rise, still ranks in our top five in terms of evaluation. So it’s a good company, despite its rise and we still like it here. We are not taking any profits at this point as we think it’s still cheap.

Michael: Where do we get a hold of that Junior Gold and Metal Survey. Do we go to www.keystocks.com?

Ryan: Yes, it will be released in about 10 days as we’re just finishing it up. If you go our website all of our current clients will get access to that in about ten days and there is actually a special offer for it there for new customers.

Michael: Do you have another one for us?

Ryan: There is a value growth stock that we are looking at right now. It’s a company that we’ve mentioned once in the past when it was at higher levels than it is now. It’s come down now to price point where we think it’s very much on sale. Zuni Holdings Inc. symbol ZUN on the TSX Venture. It’s a China based athletic apparel manufacturer that basically makes athletic shoes and casual leather footware. What we like about the company is the numbers. This company trades at a $1.90 and it will post annual revenues of $150 million and we believe it will earn around 40 cents per share this year. Now that it’s trading at a $1:80, will earn 40 cents per share that’s under five times earnings. On top of that this company has a pristine balance sheet. There is over a $1:00 per share in cash which translates to about $58 million. It has no debt, so if we strip out that cash, that $1:00 per share, you’re actually paying about 90 cents for the 40 cents in earnings that we believe this company will make this year.

This company fits what we call our classic investment portfolio. No debt is one thing, a history of growing earnings, revenue and a strong cash position. It does not need to go to the market deluding shareholders; it’s fully funded for growth initiatives and ready for opportune acquisition. It’s selling into a growing market in China, it’s basically a play on the domestic economy there and it’s trading at low valuations relative to its peers. Again, after saying all of this this does not guarantee the stock will be a successful investment but for us we believe is the more companies you add to your portfolio with a similar profile the more successful you will be over time. Conversely the more companies you add with a opposite profile to this loaded with debt, not good earnings relative to its peers those type of positions are the least successful you’ll be over time so we’ll add this as part of our diversified growth stock portfolio.

Michael: How do you factor in geographical risks because certainly in the case of the mining Bolivia isn’t considered one of the top places to have my money.

Ryan: In a specific case with a company like Orvana Minerals Corp we were originally very cautious specifically because it was operating in Bolivia. We wouldn’t think it would have been a good choice except it had 90 cents per share in cash and we could buy it at 50 cents. It actually was trading at a discount to its cash value. That cash was actually not held in Bolivia either it was held in a North American bank account. If that cash had been in Bolivia it wouldn’t have been a situation that we’d invest in. Now their main asset is now in Spain which is a mining friendly district an area of the world that we’re confident investing in a mine. About 85% of production will now come from Spain and we believe that it is a safe region to be in. As far as your broader question, diversifying geo-politically across the world is definitely something that we always suggest within a diversified portfolio. So when we mention one company like Orvana or one company like ZUN, that cannot make up the sole position within your gross stock portfolio, they have to be intermingled with 8 to 12 other companies that operate in all regions of the world. We still have a bias towards Canada and safer regions like that but right now we feel to get extreme growth or good growth we’re looking to other areas of the world.

Michael: I’m personally more comfortable with companies who’ve got a cash position, companies who are not going to the credit markets all the time.

Ryan: I agree completely. We always look for solid net cash. They can have a good cash position but if they’ve got a lot of debt there it’s something that doesn’t attract us as much. We are looking at companies with that good cash position and limited to no debt as well so not only can they weather a storm but they can take advantage of like Orvana did. Orvana had that solid cash position and when the credit siezed up there was no money to fund that mine in Spain and they were in ideal position to buy it. Now they’re going to earn the purchase price back in just over two years which is a very fast pay back period.

Michael: It’s a time to be nimble on our feet and be disciplined with companies financial foundation going forward. Ryan I really appreciate you’re taking the time and my apologies for keeping you a bit longer.

Ryan: No problem love to be here and if anybody needs to get a hold of us it’s 1-888-27-STOCK across the country or www.keystocks.com. You can also or go to our income stock research, it’s www.incomestockreport.com.

Silver and gold prices are on the rise, making physically backed exchange-traded-funds very tempting investments. Before you buy, here’s what you need to know.

There are five physically backed ETFs traded in the U.S.: The biggest, SPDR Gold Shares(GLD); the cheapest, iShares Comex Gold Trust(IAU); the newest ETFS Physical Gold Shares(SGOL) and the two silvers, iShares Silver Trust(SLV) and ETFS Physical Silver Shares(SIVR).

When you buy gold and silver physically backed ETFs you do not own the physical metal, you own a paper representation. With respect to the gold ETFs for every share you buy, you “own” one tenth of an ounce of gold, while for silver, it’s one ounce.

The actual metal is stored by a custodian, usually one of the large banks like JPMorgan(JPM) or HSBC. The share-to-metal correlation erodes the longer you hold the shares. The fund must sell gold, for example, periodically to pay for expenses which decreases the amount of gold allocated to each share.

If investor demand outpaces available shares then the issuer/trustee must buy more physical metal to convert it into stock. Conversely, when investors sell, if there are no buyers, then the metal is redeemed, the trustee must then sell the metal equivalent. Precious metal ETFs are not owned for leverage, but simply as a vehicle to track the spot price.

Investors are not typically encouraged to redeem their shares for the metal although it is possible. With respect to the SGOL, for example, an investor would have to redeem in whole lots of 50,000 shares (5,000 ounces, or $6.25 million) but only through an authorized participant. This is more feasible for high net worth individuals and funds but not really for retail investors.

Because you own shares and not the physical metal, precious metal ETFs may be sold short, so two people can own the same “gold” — the original owner and the investor who is borrowing the shares. Although baskets of shares are allocated to specific gold bars, which can be found in the ETF’s prospectus, an investor must share ownership.

Owning a precious metal ETF can also be more expensive than owning and storing the physical metal. Expense ratios can range from 0.25% to 0.50%, while storage fees at GoldMoney.com, according to founder James Turk, cost 0.15% to 0.18%.

Profits made on investments in physically backed ETFs are also taxed like collectables, at around 28%. Basically an investor gets taxed as if he owned bullion, when in reality he just owns paper.

There are also two types of gold stored in the ETFs, allocated and unallocated. Allocated gold is the bullion held by the custodian. Custodians provide a bar list of all the individual allocated bars daily and are typically audited twice a year, paid for by the sponsor, by an independent party like Inspector International.

Unallocated gold relates to authorized participants like JPMorgan or Goldman Sachs who trade gold futures. Futures contracts are often bought if the trustee needs to create new shares fast and doesn’t have the time to buy and deliver the bullion. Typically allocated gold far outweighs the unallocated gold and the amounts are tallied each day by the custodian.

….read page 2 – 7 HERE

Author and publisher Marc Faber appeared on CNBC to discuss several topics such as global equities, gold and current economic conditions in the U.S and abroad.Faber is expecting a trading range for the rest of the year with a slight dip coming in the next month or so followed by a rally to close out the volatile. According to Faber, one of the most important decisions asset allocators face is where to invest their money when interest rates are at near zero. Faber states that dividend yields will attract investors into equities and cause a possible rally.

“I think the difficulty is what to do with money when interest rates are essentially at zero on US dollar then obviously people look at their portfolios and they see stocks that have dividend yields. In Singapore, Thailand, Malaysia, you can have stocks yielding 5% on the dividend. So, the money flows essentially into these stocks.” (video 7:28)

Michael Campbell: Joining me on the line right now I’ve got the head analyst for Black Swan Capital. There’s so much that Jack Crooks does and I love his work because he writes some terrific things. Last year at this time you were telling us to keep an eye on the Euro. You said you think it’s going down at the outlook conference, that its a no-brainer trade. You said Greece is going to really cause trouble before it had hit the headlines. Obviously a very successful move as the Euro did have a major downward leg vis-à-vis the US dollar and the Canadian dollar so its a fortuitous time to get you on the line right now. You’ve been writing about the concept that when people feel like they don’t want any risk, they go to the US dollar and when they feel a little more risk friendly then they leave the US dollar. Where do you think we’re at generally with that now?

Jack Crooks: The risk, the so called risk on, risk off is still the co-relation that’s in play here to a degree. What we’re going to see is more political unrest throughout the Euro zone just because Germany is just sucking the wind out of everybody and nobody else is really able to participate in the growth there. Near term it looks like the dollar may correct in here from a trader’s stand point but longer term we still think that Euro theme is in play once we get past this sort of bit of growth optimism that we’ve seen recently based on just some of the global growth not only in the US. I think the US numbers have been okay but the Asian numbers have been very strong and that’s what really drives this risk appetite trade.

Michael: So it’s all about either aversion to risk or taking on a little bit more risk. That’s such an important concept for people to get.

Jack: Yes, it’s huge. It is a relevant game and the US dollar is the World reserve currency because the US’s capital markets are deeper than any other capital markets in the world. So the US can be very ugly but the US dollar can still go up because people have to move money for reasons of safety. Big money international investors that don’t have any other place to hide have to come to US. They might not like the US economy but they’re forced into the depths of the US capital markets.

Michael: For these huge pools of money there’s only three games in town, either going to be in the Euro, the US, or the Yen. The Canadian dollar just couldn’t absorb that kind of money movement and wouldn’t be considered because of it. New Zealand or Australia are in the same boat. My goodness though, if you list the problems in Japan it’s been in a 20 years of low growth, a recessionary environment and the demographics just suck. Yet the Yen’s done very well recently.

Jack: Japan is a perfect analogy. When people point to the US and note that the GDP is rising therefore the dollar has to fall, all we have to do is look at the Japanese Yen. These things are never that simple. That said, we think the game is about over for the yen.

.

Michael: Luckily as an investor I can now play a currency move with an exchange traded fund now, which trade just like stocks do. While it does look right now like the yen can’t go any further I know that markets can stay irrational longer than I can stay solvent. So how do you determine when its time to make a move?

Jack: I think you summed it up very well; things can always go lower than we think and always go higher than we think. In a piece that we wrote a few weeks ago, we talked about Barton Biggs back in 1995 who said that trade of the decade, may be the trade of the life time was to sell Japanese government bonds. Well he still probably hasn’t broken even on that trade if he did it. For 10 or 15 years now those interest rates have stayed low in Japan. Ultimately you have to look for some reason for a major trend change and it has to from some consolidation or some major fundamental change. We are actually starting to see a little bit around the edges in Japan. One of the things that we track very closely is the 20 year bond yield versus the Japanese Yen and they are usually just dead on the money. If your listeners can get to a 20 year bond yield chart and pull it up, bond yields have actually backed up in a very big way over the last week or so in Japan but the Yen is still near it’s low. So there’s a giant divergence to it. It hasn’t developed in that chart for a very long time but it’s something that we’re watching and we’re actually starting to pack on the Yen for that reason. That’s a fundamental capital flow change that’s not really showing up in the headlines.

Michael: What else do you think is happening out there?

Jack: Other than the Yen move which we think is very close here, the Euro we think ultimately it goes to par because we just don’t see the system surviving politically. We could see Ireland, Spain and Greece some going back to their own local currencies because they’re in a straight jacket. So the Euro coming apart eventually economically and politically still makes sense. We do think ultimately the Yen is really the next big trade because what we’re seeing in this isn’t new. One of the reasons the Yen has always been so strong is they have been historically able to fund themselves domestically because Japanese are savers. Now they are are not making 20% saving rates instead they’re about zero right now. There comes a point when they’re going to have start raising those long bond interest rates to attract international capital now in Japan. I think the game is about over in domestic funding and that we think it is going to be the next really big long term trade.

Michael: There’s just so much money swashing around the world, about 3.5 trillion dollars a day that trades a day in the currency markets. Which to put into perspective is two and a half to three times the size of the entire Canadian economy output in a year trading each day. So we’re talking massive amounts of money which is why governments and central banks can only talk the game because they learned a long time ago they couldn’t influence it directly.

Jack: Exactly, you’re exactly right. The markets are so big now there has to be some type of fundamental change in capital flow to change these trends it cannot come from a government or central bank. They don’t have the power to move these markets any longer.

Michael: I want to stay in Asia for a second and just get your comments on China because so much of our growth scenario, our rescue scenario takes place coming out of China.

Jack: Yes it sure does. Last week China’s purchasing index was above fifty for the month of August and they were below 50, so more vibrancy again. India is still growing well, Singapore looks pretty good, Australia looks very strong. We have to consider Australia an Asian economy at the moment. So there is growth there. A move to the risk appetite trade would mean the dollars starts to get hit again and we saw that this week. But while the numbers keep coming through in China the real concern continues to be for us a consumer in China just hasn’t been there. Also the fact that China continues to basically subsidize its interest rates. The interest rates in China are very, very suppressed artificially below the market. It’s creating huge implications for capital across a lot of different sectors. China knows this, but they continue to keep their interest rates suppressed and their currency suppressed because they play have to still export.

They are off the charts in terms of anything we’ve ever seen in history as an economy that’s weighted export versus consumer. Just nothing has even been close to where China is here. And the scenario that we draw from a major global metric change is exactly like of Japan. Japan was going to take over the world in the mid 1980’s and China has done the exact same from a financial and economic standpoint. Very much a parallel. We are not alone in this concern but that’s something that we continue to watch and if it does play out that China just cannot support its own growth domestically, it’s going to be very, very nasty for the global economy. So it’s something we continue to watch on our radar screen. But the near term numbers are strong and you got to go with it.

Michael: What about the Canadian dollar?

Jack: We like that a lot here from a trade standpoint because of the growth in Asia. Also the Canadian and Australian dollars are both commodity currencies and If we pull up the Canadian dollar against the Australian dollar chart, the Canadian dollar is extremely cheap here relative to the other commodity currency out there. That’s another reason we like it

Michael: That’s an easy one for Canadians cause we don’t have to trade it we just own it, we are it.

Jack: That’s right

Michael: Jack I want to thank you for taking the time as I say I know you are busy with other things there. But it’s always a pleasure to talk to you. And as I say I think the understanding of how the currencies are moving and why they are moving is the key to understanding really what the heck’s going on in the world and we appreciate your insights.

Jack: Thanks for having me Mike always my pleasure.

Michael: Just go to www.blackswantrading.com I read Jack’s comments every day I recommend them to people as I say that’s how you keep a handle on what’s going on in the world.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair