Stocks & Equities

These four charts below are just the sort of Big Picture, long cycle perspective that so many investors overlook or simply have no knowledge about. These charts are not about making predictions, but rather, are about putting market action into some broader historical context. What has happened in the past? What is typical? Aberrational?

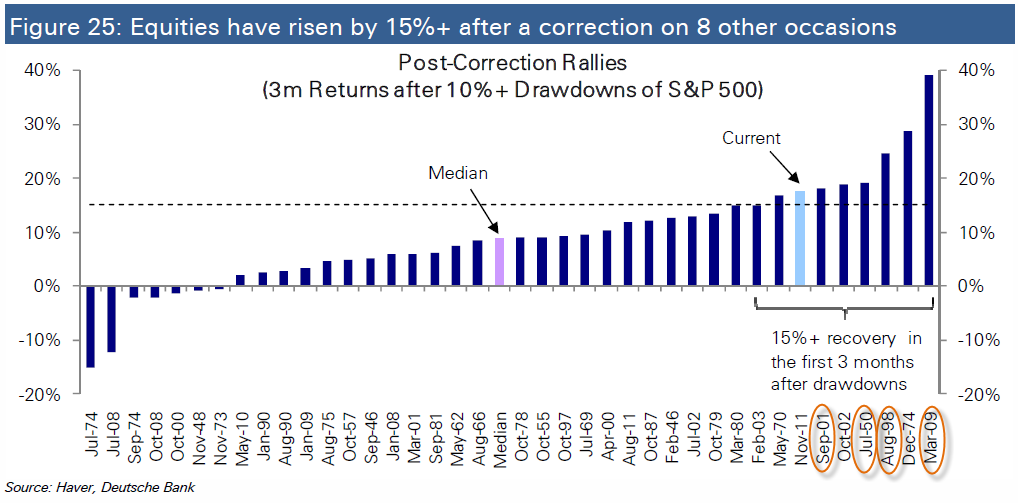

And the S&P 500 has only risen by more than this on six other occasions after a 10% drawdown…and many of those were during some of the most crisis prone periods this nation has ever experienced.

And the S&P 500 has only risen by more than this on six other occasions after a 10% drawdown…and many of those were during some of the most crisis prone periods this nation has ever experienced.

“He may look like an idiot and talk like an idiot, but don’t let that fool you — he really is an idiot.”

– Groucho Marx

John Ross asked me this morning if I could create a scenario whereby stocks fall. I laughed and said, “Well … no!” And maybe that is the point. No doubt ‘if you are not long, you are wrong’ is playing out in spades. But we’ve seen that sentiment many times before near tops.

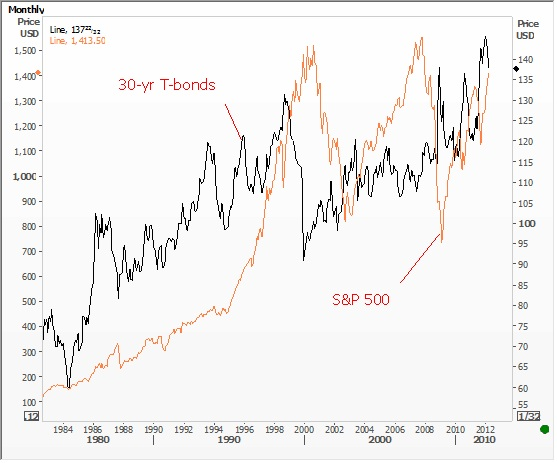

The primary thematic shaping up seems the idea that bonds have topped and as this money leaves bonds it will power stocks higher—globally. The idea seems to make sense; but often it is never that easy. Taking a look at the chart below, there doesn’t seem a heck of a lot of correlation to hang your hat upon, only to say the long-term trend higher in bonds (lower in yields) has been met by a corresponding big run in stocks.

Let’s consider some reasons why US stocks might NOT go a lot higher and, for grins, maybe even, dare I say it, “correct.”

- A recovery in the US economy could mean finally financial assets will start competing for funds and the Bernanke Put, i.e. QE moral hazard liquidity juice, fades. Bonds would get hit here, but stocks might at least correct.

- Bernanke’s concern the job market is still not healed may play out because fiscal stimulus fades as the year progresses. Thus, we have well below trend growth and rising prices for energy and food leading to at least a mild case of stagflation; that isn’t good for either stocks or bonds.

- Germany decides to go “all in” and throws its full faith and credit behind a Eurobond for the Eurozone. Immediately, the risk profile improves in Europe. S&P and Moody’s decide it’s time to upgrade European paper and at the same time downgrade US paper given that Washington can make no real cuts amidst ideological squabbling. Lots of capital flows back to European bonds and stocks and out of the US; a possible triple-whammy out of US assets (stocks, bonds, and the dollar).

- China financial and social unrest ramp up and the Communist Party is at odds on stimulus given their concern about inflation; therefore it’s better to have security locally than worry about Western markets; the additional stimulus never arrives as growth and demand forecasts for China ratchet lower. Likely bad for stocks, but maybe good for bonds.

- Eurozone. ‘Nuff said!

- Rising emerging market capital controls a la Brazil (tacitly condoned by the IMF) are met with rising trade tariffs from developed countries. Money flows out of risk assets (stocks), quickly from the periphery, and back into bonds as global trade falls.

- Republicans win the White House and Congress, fire Ben Bernanke, and make Ron Paul Fed Chairman. They cut the budget deficit twice as much as what Paul Ryan is lobbying for. Ultimately it would be the best thing that happened to the US financial position in a hundred years, but there would be hell to pay as US credit drains from the global economy (and we have to listen to the moochers whining and crying about “fairness” day in, and day out). US bonds rally big time, so does the US dollar; stocks would likely be hit very hard initially, then stage a gargantuan rally. [I know; but a guy can dream.]

For now, “don’t fight the Fed” and “the trend is your friend” are winning the day. And if the bulls are right about US recovery, European healing, and new Chinese stimulus soon on the way, it could keep running. No doubt.

Tags: China, Federal Reserve, Ben Bernanke, US Dollar, US Treasuries, BRICS, US Bonds, eurozone, commodities

There’s no question that China and the rest of Asia are outgrowing the Western world by leaps and bounds. All you have to do is follow the stats coming out of Asia, or take a trip to anywhere in Asia, and you’ll get a firsthand feeling for how vibrant the region is.

But there’s also no question in my mind that there is some slowing going on. Perhaps a bit more slowing than I originally expected.

First, according to a just-released HSBC research report, China’s manufacturing activity fell sharply in March as factory bookings of new orders fell to a four-month low. In addition, overall employment dropped to its lowest level since March 2009.

Second, the CEO of BHP Billiton (BHP) — the largest iron ore supplier in the world — recently stated in a press conference that he saw signs of “flattening” iron ore demand from China. Iron ore, used in steel production, is a very sensitive indicator of overall Chinese and Asian demand.

Third, even auto and truck sales are slowing in China. Total vehicle sales for January and February shrank 6% compared to the same period last year.

A slowdown? Yes. A disaster? No. But all of it fits in perfectly with my overall forecast, which I’ll review now.

Short term, you know I’ve been bearish the commodity sector. I remain so …

For one thing, gold completed an 11-year up-cycle at last year’s record high. This means that a pause and correction for 2012 is the highest-probability course for gold this year. And so far, that’s exactly what the precious yellow metal has been doing — pausing and correcting.

Indeed, gold’s failure to execute a monthly buy signal at the end of February, as I recently told you, is a major signal that gold could head much lower in the short run.

From what I’m seeing in silver, the same holds true. If silver can’t soon get back above the $34.25 level on a closing basis, it’s in danger of a devastating plunge down to the $26 level and probably A LOT lower.

For another, I’m seeing similar corrective signs in nearly all commodity markets. Cocoa is looking very weak. So is coffee. And the grain markets, while biding time largely going sideways, are also in danger of a sharp decline.

At the same time, the price of oil is having a very tough time moving above a key resistance level at the $111 mark. As long as the price of oil remains below $111, it too is in danger of a slide back down.

Fundamentally speaking, demand from the world’s largest single economic zone, Europe, is set to decline due to the region’s high unemployment rate and the austerity measures taking effect as a result of Europe’s sovereign-debt crisis and euro troubles.

Meanwhile, whatever strength we’ve seen in the U.S. economy is nowhere near enough to compensate.

So in the short run, looking ahead over approximately the next six months, I see no reason to be outright bullish the commodity complex. In fact, I still expect to see …

![]() Gold slide to $1,490, then even lower.

Gold slide to $1,490, then even lower.

![]() Silver to at least test the $26.40 level.

Silver to at least test the $26.40 level.

![]() Oil slide to the $80 region.

Oil slide to the $80 region.

![]() Base metals such as copper take a sharp fall.

Base metals such as copper take a sharp fall.

![]() The prices of agricultural commodities also get hit.

The prices of agricultural commodities also get hit.

But in the long run, the seeds are now

being sown for the next big leg up in

commodities and tangible assets.

It will come from much-lower prices overall in the commodity complex. And importantly, it will start when least expected.

The reasons for the longer-term bull market remain very much intact. Although we’re at a lull now in the sovereign-debt crisis, it will come back with a vengeance and we will see …

![]() Europe’s economy crater, with Greece eventually defaulting; Portugal, Italy and Spain cratering; and even France getting hit with major debt issues.

Europe’s economy crater, with Greece eventually defaulting; Portugal, Italy and Spain cratering; and even France getting hit with major debt issues.

This will lead to even more European Central Bank money-printing operations, a weaker euro, and a renewed flight of capital into tangible asset markets.

![]() We will also see the U.S. get hit hard by the sovereign-debt crisis. Keep in mind that Washington is even more indebted than Europe. It’s only a matter of time before it falls, too.

We will also see the U.S. get hit hard by the sovereign-debt crisis. Keep in mind that Washington is even more indebted than Europe. It’s only a matter of time before it falls, too.

Right now, we’re seeing some continuing capital flight from Europe into U.S. equity markets. We will continue to see that, and the long-term prospects for the stock markets remain very bright indeed. But even here, as in commodities, I still expect one more broad market swoon before equities become a safe haven from the public sector’s sovereign debt crisis.

And as far as Asia goes, don’t bet on the downside there, even though the region is perhaps a bit weaker than I had expected.

You’re far better off using any dips in Asia to position yourself for the next leg up in Asian economies and markets, which will be HUGE.

Core long-term positions in vehicles such as the iShares FTSE China 25 Index Fund (FXI) make a lot of sense. I suggest buying on weakness and look to potentially double and triple your money over the next three years.

Best wishes,

Larry

P.S. Speaking of China, I have uncovered new evidence that Beijing is in cahoots with Washington to bankrupt you! Watch my brand-new video “The Great Betrayal of 2012” for all the details … along with specific steps you can take to protect yourself from their collusion. Just click here to watch this urgent video report now.

March 22, 2012 – Russell turns chicken — The retail public usually buys stocks during the opening hours of the session. The pros and the institutions usually do their trading during the waning hours of the session. With today’s market action I took a small profit and sold out my DIAs, yes against the dictates of my PTI. I just didn’t feel that the risk-to-reward was worth sitting with stocks at this juncture. I’m waiting to see the days when the market firms up near the close, which is the opposite of what it’s been doing. I don’t like markets that tend to sell off during the last two hours of trading. I’m now satisfied to be on the sidelines with zero common stocks. I’ll just watch the action for a while. My inclination and feeling — neutral, very neutral. But no sell signal yet from my PTI.

Earlier in the Day Russell Wrote:

The fact is that the Fed is happy with 2% inflation each and every year. Compound 2% inflation year after year, and you know what’s happening? — you’ve effectively wiped out the middle class. Between inflation, stagnant wages, higher taxes, and no jobs, the middle class has hit the brick wall like a fresh egg hitting the trunk of a redwood tree. Whoosh!

The Dow appears to waffle around during the length of each trading day and then at the close the Dow is down 10 to 50 points. What is this? Reverse inflation? Or is the Dow trying to tell us something? Honest, I don’t know what!

Personally, I don’t care for the action, but my PTI still says “bullish.” Most of us are so tired of hearing about Greece that we wish the country would just sink into the Mediterranean and take Portugal and Spain with it.

About Richard Russell (scroll down for his offer for a two week $1.00 “free” trial)

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

In 1989 Russell took over Julian Snyder’s well-known advisory service, “International Moneyline”, a service which Mr. Synder ran from Switzerland. Then, in 1998 Russell took over the Zweig Forecast from famed market analyst, Martin Zweig. Russell has written articles and been quoted in such publications as Bloomberg magazine, Barron’s, Time, Newsweek, Money Magazine, the Wall Street Journal, the New York Times, Reuters, and others. Subscribers to Dow Theory Letters number over 12,000, hailing from all 50 states and dozens of overseas counties.

A native New Yorker (born in 1924) Russell has lived through depressions and booms, through good times and bad, through war and peace. He was educated at Rutgers and received his BA at NYU. Russell flew as a combat bombardier on B-25 Mitchell Bombers with the 12th Air Force during World War II.

One of the favorite features of the Letter is Russell’s daily Primary Trend Index (PTI), which is a proprietary index which has been included in the Letters since 1971. The PTI has been an amazingly accurate and useful guide to the trend of the market, and it often actually differs with Russell’s opinions. But Russell always defers to his PTI. Says Russell, “The PTI is a lot smarter than I am. It’s a great ego-deflator, as far as I’m concerned, and I’ve learned never to fight it.”

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

IMPORTANT: As an added plus for subscribers, the latest Primary Trend Index (PTI) figure for the day will be posted on our web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair