“He may look like an idiot and talk like an idiot, but don’t let that fool you — he really is an idiot.”

– Groucho Marx

John Ross asked me this morning if I could create a scenario whereby stocks fall. I laughed and said, “Well … no!” And maybe that is the point. No doubt ‘if you are not long, you are wrong’ is playing out in spades. But we’ve seen that sentiment many times before near tops.

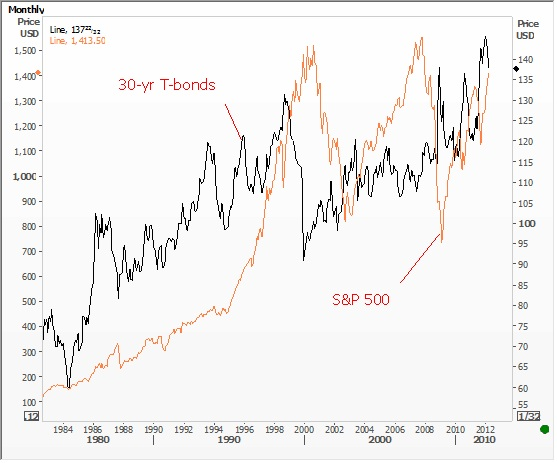

The primary thematic shaping up seems the idea that bonds have topped and as this money leaves bonds it will power stocks higher—globally. The idea seems to make sense; but often it is never that easy. Taking a look at the chart below, there doesn’t seem a heck of a lot of correlation to hang your hat upon, only to say the long-term trend higher in bonds (lower in yields) has been met by a corresponding big run in stocks.

Let’s consider some reasons why US stocks might NOT go a lot higher and, for grins, maybe even, dare I say it, “correct.”

- A recovery in the US economy could mean finally financial assets will start competing for funds and the Bernanke Put, i.e. QE moral hazard liquidity juice, fades. Bonds would get hit here, but stocks might at least correct.

- Bernanke’s concern the job market is still not healed may play out because fiscal stimulus fades as the year progresses. Thus, we have well below trend growth and rising prices for energy and food leading to at least a mild case of stagflation; that isn’t good for either stocks or bonds.

- Germany decides to go “all in” and throws its full faith and credit behind a Eurobond for the Eurozone. Immediately, the risk profile improves in Europe. S&P and Moody’s decide it’s time to upgrade European paper and at the same time downgrade US paper given that Washington can make no real cuts amidst ideological squabbling. Lots of capital flows back to European bonds and stocks and out of the US; a possible triple-whammy out of US assets (stocks, bonds, and the dollar).

- China financial and social unrest ramp up and the Communist Party is at odds on stimulus given their concern about inflation; therefore it’s better to have security locally than worry about Western markets; the additional stimulus never arrives as growth and demand forecasts for China ratchet lower. Likely bad for stocks, but maybe good for bonds.

- Eurozone. ‘Nuff said!

- Rising emerging market capital controls a la Brazil (tacitly condoned by the IMF) are met with rising trade tariffs from developed countries. Money flows out of risk assets (stocks), quickly from the periphery, and back into bonds as global trade falls.

- Republicans win the White House and Congress, fire Ben Bernanke, and make Ron Paul Fed Chairman. They cut the budget deficit twice as much as what Paul Ryan is lobbying for. Ultimately it would be the best thing that happened to the US financial position in a hundred years, but there would be hell to pay as US credit drains from the global economy (and we have to listen to the moochers whining and crying about “fairness” day in, and day out). US bonds rally big time, so does the US dollar; stocks would likely be hit very hard initially, then stage a gargantuan rally. [I know; but a guy can dream.]

For now, “don’t fight the Fed” and “the trend is your friend” are winning the day. And if the bulls are right about US recovery, European healing, and new Chinese stimulus soon on the way, it could keep running. No doubt.

Tags: China, Federal Reserve, Ben Bernanke, US Dollar, US Treasuries, BRICS, US Bonds, eurozone, commodities