Stocks & Equities

Perspective

The stock market is included in the orthodox calculation of Leading Indicators. Problem is that at the end of a great financial bubble, such as in 1929 and 1873, the recession started virtually with the collapse of speculation, which was also the case in 2007. This is one of the features of a bubble and its collapse. Stocks peaked in October 2007 and the recession started in that fateful December.

Essentially, both the stock market and the economy recovered when the panic ended in March 2009. We have thought that the relation would continue such that the first business expansion out of the crash would end with the end of the first bull market. It should be admitted that we had thought that the US expansion would end with the commodity-high of last April. Usually we leave the discussion about recoveries and recessions to the cult of economics, but sometimes it’s worth a try. After all, the NBER typically determines the start of the recession – one year after the actual start.

Naturally, we can’t help but wonder if the life that recently came into the economic numbers will turn down with the stock market – with little delay. Taking out 1340 on the S&P would set the downtrend. What would set the downtrend in GDP?

A couple of weeks ago central bankers were comfortable that stimulus and fixes had – well – fixed things. No more easing was required. Then, this week’s hit to the markets seems to have dislocated policymaker confidence such that Bernanke had to state that he would not raise administered rates. Our view has been that it has been market forces that have lowered such rates. In troubled times conservative funds go to the most liquid items and they are short-dated instruments in the senior currency and gold. This drives the former down in yield and the latter up in price.

The swing in Fed opinion reminds of Tokyo at its extraordinary peak at the end of 1989. Speculation was radical and policymakers were trying to talk the action down – which is always impossible because such speculation will run to collapse. With the initial break in the Nikkei, policymakers became nervous and talked about lowering margin requirements. Shortly after the top of a bubble??? Japan’s subsequent contraction has been one for the history books.

Our “new financial era” recorded a number of cyclical speculative thrusts and cyclical bear markets until a classical bubble was accomplished in 2007. Despite easing that exceeds the determined efforts by the Fed at the start of the post-1929 contraction,

financial history remains on the typical post-bubble path. One could even say that central bankers have been extremely belligerent in attacking the normal forces of contraction.

However, sovereign debt markets are saying that it is not working well. An updated chart on the “Spanish Fandango” follows.

CREDIT MARKETS

With the break in overall confidence, the long bond jumped almost 5 points in three trading days. Junk, high-yield bonds, and sovereign debt sold off. The sub-prime which had rallied from 38 in October to 52.5 in February has slumped to 47.4. The chart has broken down and the target is the 38 of last October. Municipals are close to ending their test of the highs in February.

This year’s seasonal reversal to widening in May could lead to very unsettled credit markets later in the year.

The long bond was oversold and the bounce has corrected this condition and the price is likely to drift down to test the low.

Action in lower-grade stuff has not been healthy, and an economist at an orthodox place (IMF) has discovered that there is not enough collateral behind all of the debt. In Victorian times this was called “over trading” and today its “leveraging”. No matter what the term, it is always followed by liquidation or in today’s terms “de-leveraging”. The next stage could inspire articles that it is impossible for the world’s economy to generate enough income to service the debt burden.

There will be plenty of opportunity for a “new” wave of young economists to point out the glaring blunders of the ancient and “barbarous relic” of interventionist economics.

Commodities

Base metals and crude oil declined enough to prompt a rebound with the Fed turning on the speculation switch again. Neither were oversold enough to set an intermediate bottom. Natural gas got headlines in declining below $2.00, but it is not as oversold as at the 2.23 low in January. Also, late April often sets a seasonal high.

Agricultural prices suffered a hit last week, but not enough to break the chart out of the narrow trading range. Coffee clearly needs a jolt as it has given up most of the huge gain to April last year. It seems that the sector is being keep together by strong action in soybeans and soybean meal. These are becoming rather overbought at close to last year’s highs.

After mid-year, adverse credit spreads, a slowing global economy and a firming dollar could trash most commodities – again. The chart shows three “over-boughts” – at 474 in 2008, 370 last April and at 326 in February.

Currencies

Bernanke renewed his vows to depreciate the dollar, which brought the DX back into its trading range. However, this is still within the pattern leading to a significant advance.

Getting above overhead resistance at 81 could set the launch button. For day-traders May is a long time away, but for investors it is nearby and could record a reversal in credit spreads and forex markets.

BOOM SAYERS to OOOPS!

Signs of the Times:

We ran “Boom Sayer” exclamations for four weeks and considering the nature of volatility it is reasonable to conclude that current excesses will eventually be followed by “Doom Sayers”.

But, let’s not be hasty – usually the next step from complacency is “Ooops!”.

And that might have begun with this week’s discovery that the “fix” on Euroland debt won’t last as long as even the shorter maturities become due.

Pity.

This Year

“The biggest wave of state-and-local government debt refinancing in two decades is helping fuel the longest winning streak for municipal bonds since 2007.”

– Bloomberg, April 2

“Taxable municipal bonds are poised to extend their best rally in 18 years.”

– Bloomberg, April 4

“Across the Eurozone, and beyond, hedge fund managers are now pointing to ‘significant’ pricing anomalies not seen since 2008.”

– Bloomberg, April 6

“JP Morgan trader of credit-derivative indexes [linked to the health of corporations] has amassed positions so large that he is driving price moves in the $10 trillion market.”

– Bloomberg, April 6

Of course, these preceded Tuesday’s setback, but their significance is that there is considerable speculation in credit markets. As we have been noting, favourable trends in corporate spreads ended in February. This could reverse to widening over the next four to six weeks.

As we have been noting, “Boom Sayer” exclamations from March and April last year were remarkably similar to this year’s list. The best of last year’s have been published and, essentially, they ended in April, which suggests a pattern.

Stock market action in both years set a momentum high in February with positive sentiment recorded in March and April – accompanied by bullish raves.

This week saw some “sudden” exclamations of dismay. Does it indicate a new trend?

Link to April 13 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2012/04/gold-gloom/

- Its a broadly mixed start to the day. Asian equities are down yet again, even in the face of a bigger-than-expected rate cut out of India

- On the data front, the German ZEW investor index improved in April – both the current conditions and expectations components picked up nicely.

Another deja vu?

- The ‘Sell in May and go away’ mantra worked so well in the past two years that it can’t be ignored

The rain in Spain is not contained

Even with the ECB buying more Spanish Bonds, the problems within Spain have obviously not been solved

One dismal U.S. macro backdrop

- It’s so easy to get caught up in the high-frequency data flow that it is not difficult to lose sight of just how bad it is out there.

But retail sales hang in

- The consensus on March retail sales was for a 0.3% gain but instead we got +0.8% and the gains were fairly broad based

April data bring on some showers

- It’s merely a diffusion index, but the New York Fed Empire Survey did disappoint in a major way

Nothing loonie here

- Despite the pullback in global investor risk appetitie and faltering commodity prices, the Canadian dollar has managed to remain at par against its strong ‘safe haven’ U.S. counterpart

Getting high on yield Conference

Many readers have heard me discuss the vitures of a S.I.R.P. strategy. We continue to believe in well thought out S.I.R.P. investments and my colleague Reno Giancola and I will be discussing investment strategies and investment ideas as a conference May 31st at the Design Exchange in support of Mount Sinai Hospital.

Great Opportunity below:

I subscribed to a Free 7 Day Trial to David Rosenberg’s great Breakfast with Dave daily report so that you can piggyback on the trial. Just put in my username and password below and try it out! I have read it for years and really like the full report (the above “While You Were Sleeping” is just a minor part of the daily letter) it so see what you think. Only 3 more days on the trial but every report that’s ever been issued is available by putting in my email address and Password. Regards Robert Zurrer Editor-Moneytalks.net email – zurrermoneytalks@shaw.ca or zurrer@shaw.ca

|

Dear reader, As one of David Rosenberg’s long-standing followers, we have set up a free no-commitment seven day trial with full access to all reports using the new platform. All you need to do is login using the details below:

Should you choose to purchase a subscription, login to the Gluskin Sheff Research platform, go to My Account on the top right, click My User Profile, select Subscription Status on the left hand side menu, click Change/Upgrade Subscription, and follow the instructions to complete the upgrade. You can also read Breakfast with Dave reports on your iPad, iPhone, PlayBook or Android device using our free Gluskin Sheff Research app. Follow the links below to download the app to your mobile devices:    If you have any questions, please do not hesitate to contact us at research@gluskinsheff.com“>research@gluskinsheff.com. Thank you, Gluskin Sheff Research |

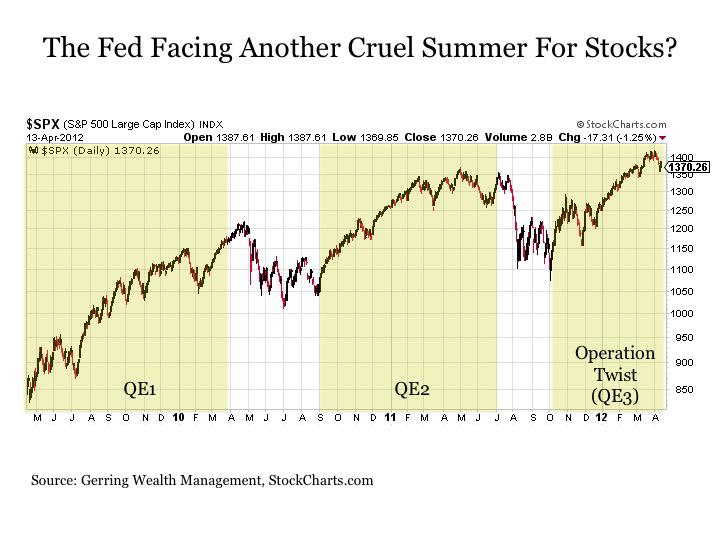

By: Eric Parnell

The stock market has made one thing abundantly clear in the early days of the second quarter: It still cannot stand on its own at current levels without the continued support of additional stimulus from the U.S. Federal Reserve. And with the latest Fed stimulus program set to end in June, it may be shaping up to be another cruel summer for stocks.

It all began on April 3 with the release of the latest Fed minutes from the March Open Market Committee meeting. Although nothing was included or discussed that we haven’t already heard from the Fed many times before over the last several years, the market decided that the key take away from the latest minutes was that no further quantitative easing would be coming from the Fed any time soon. Stocks (SPY) immediately recoiled on the news, sliding lower for the remainder of the holiday shortened trading week. Then came the disappointing employment numbers on Friday and the uneasy response by investors once the stock market reopened early this past week. All of the sudden, the additional Fed stimulus that so many had concluded was off the table merely one week earlier was all of the sudden back on once again.

To Read More CLICK HERE

Via Richard Russell of Dow Theory Letters – Title: “Be Careful” With This Stock Market

These stock and bond markets may not make us happy, but we might as well get used to them, because they’re all we’ve got!

I’ve had a lot of time while in bed to watch TV and particularly Bloomberg. And I note that 90% of the time the so-called experts try to predict the path of the stock market by the way the current news is going. If the news is getting better and unemployment is looking brighter, then the stock market “should” be rallying. If the European picture is darkening, then the market “should” be shaky to weak. Follow the fundamentals, not the market!

So far, the stock market isn’t giving off any definitive hints as to what it’s doing or which way the trend is heading. I study my PTI, and its last trend signal was bullish. But as you may have noticed from the recent point and figure chart, my PTI has not been climbing to new highs. Instead, it’s forming a column of descending metrics, although it has NOT yet issued a clear bear signal.

Lowry’s Selling Pressure Index is still above their Buying Power Index, a formation that always bears careful watching. Joe Granville’s on-balance-volume statistics remain bearish as does Joe, and I always take Granville’s work seriously. My astute friend, A. Gary Shilling, is bearish because he thinks US consumers have exhausted their buying power.

Actually, the reason I so frequently talk about Lowry’s and Granville is that they are about the only two who stick strictly to technical analysis of the stock market while putting the market first and ignoring all the news of the day and the much-talked about fundamentals.

I note that the futures in the Dow are almost always the opposite of the way the market has closed. If the market closes down, the futures are usually higher, and the opposite is true if the stock market closes higher. BUT, if the market closes higher and the futures are higher, it usually means that next day will be a positive day.

This is a grinding back-and-forth market, one that is better to watch than to play.

Nowadays, it seems as though the market is always teetering on the knife’s edge. Depending upon which way the wind is blowing on any given day, or what chatter is coming across the newswires, markets around the globe are moving at lightning fast speed. Sentiment can change instantly, with the release of unexpected economic data, market movements, or surprising actions of central bankers. The effect of high frequency trading (HFT) has turned the decades old profession of investing into a high stakes gambling operation, and more characteristic of commodity trading. Such erratic behavior on a daily basis makes it difficult, if not impossible, for analysts to formulate a long-term view, and for investors to maintain a long-term, “Buy and hold” position. “As soon as you think you’ve got the key to the stock market, they change the lock,” said long-time market guru, Joe Granville.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair