Bespoke Investment Group was formed in May 2007 by co-founders Paul Hickey and Justin Walters. Prior to founding Bespoke, Mr. Hickey and Mr. Walters worked and studied under the tutelage of famed market strategist Laszlo Birinyi. From the outset, our goal at Bespoke has been to provide clients with timely investment ideas that are presented in a way that’s easy to read and understand. Bespoke’s original content and unique ways of analyzing the market are viewed as a refreshing change from the cookie-cutter research provided by most Wall Street research shops, and this is evidenced by our large following from both individual and institutional investors as well as the financial media, which uses our work on a daily basis.

Stocks & Equities

Gold juniors need to get back to the basics, says Eric Coffin, and it is going to take large discoveries to get the market excited again. In this interview with The Gold Report, the publisher of Hard Rock Analyst explains how the new economics of gold production require investors to concentrate on companies with three specific qualities, and names the regions that could generate breakout projects. Source: Kevin Michael Grace of The Gold Report

The Gold Report: Federal Reserve Chairman Ben Bernanke indicated last month that the Fed would begin to taper quantitative easing in September. The equity markets responded quite negatively to this. In the wake of this response, do you think the Fed is committed to this new policy?

Eric Coffin: I think the Fed is committed to tapering, but I suspect it will happen a little more slowly than some people think. Bernanke’s quite cognizant that when he does taper it’s going to have an impact on the markets. But you can’t keep buying $85 billion worth of bonds a month forever. Bernanke has backed off a bit himself on this issue and was back to using 6.5% as his unemployment target. If the U.S. keeps creating jobs at the pace of 175,000 to 200,000 per month, it will take a long time to get unemployment to 6.5%—probably 18 months or more.

TGR: We’ve seen these hints about a slowing down or an end to quantitative easing (QE) for some time now, haven’t we?

EC: A lot of people in the goldbug community can’t stand Bernanke and I think they give him less credit than he deserves. I think these occasional hints he drops about ending QE early are completely intentional. He’s testing the market to see how it will react and indirectly talking bond yields up in a way that doesn’t induce some full blown panic. I think if we see him say he might move up the QE schedule and the market doesn’t freak out—that will be the time he starts tapering. He’s trying to get us used to the idea.

TGR: We’ve seen gold rebound in July. Why do you think this is happening, and do you think it’s likely to continue?

EC: Some of it, a lot of it really, is due to the Fed backing off on its short-term tapering comments. And it’s partially due to gold falling to $1,180/ounce ($1,180/oz). That’s getting into the range a lot of the technicians were calling as a bottom. I don’t completely accept technical analysis, but a lot of people who trade gold and commodities are chart traders, so you can’t ignore those patterns.

The other factor is that we’ve been getting down to pricing that’s below the all-in cost for the gold mining sector, which means we’re going to see cutbacks in production. This will flush out the supply pipeline pretty quickly. Ironically, it seems the gold market is taking the end of QE more seriously than other markets. I would like to think that means QE ending is partially or even largely priced into the gold market. Unfortunately, we won’t know that for sure until the Fed actually pulls the trigger and decreases the bond buying.

TGR: Do you think that one big discovery could excite the whole market and bring investors back to the table?

EC: This market feels more and more like the markets I saw back in the 1980s and 1990s. That’s not to say I think that the commodity cycle is necessarily over. If you go back to those markets, it was quite common that what would ignite them wasn’t big moves in the commodities. It was almost always two or three big discoveries that really got traders excited and reminded them why they buy these crazy stocks.

I’ve talked myself into chasing companies with resources just because their ounces have gotten cheaper and cheaper over the last two years. While I think those companies will definitely catch bids if the gold price starts moving substantially, my gut feeling is that if you’re looking for really large percentage gains in the near-term, they’re going to come from discoveries.

TGR: Do you think that some regions will come back faster than others?

EC: Areas that are easier from a logistical and permitting point of view, areas that are mining friendly, will probably come back faster. This basically means North America or large swaths of it. Other areas like Central and Eastern Europe also look interesting and have a lot of discovery potential. A number of Central and South American countries—even though they’re good areas geologically—will have a much more difficult time.

TGR: What about Mexico?

EC: Mexico has a couple of pretty big advantages. It has a good mining act and a well-understood and fair permitting system. It has gotten a lot better security-wise. Infrastructure is good in a lot of areas, and basic costs are also good. Mexico’s geology has generated many highly oxidized and relatively soft and brittle deposits. This enables companies to set up heap-leach operations, which means that capital expenditures (capexes) are relatively low.

In the state of Sonora, a half-dozen gold mines have opened up in the last three or four years with average cash costs in the $400–450/oz range. The all-in costs probably aren’t much more than $600–650/oz. By world standards that’s really, really good.

TGR: Do you think the Yukon is still an area play?

EC: Not in the sense that just being in the Yukon is going to give you market cap and financing. It basically comes down to individual companies now and many of the companies involved there a couple of years ago have moved on. There certainly are successful explorers there.

TGR: The three criteria you cited for successful companies are strong management, strong projects and cash. Given how difficult it has been and will be to raise financing, would you say cash is the most important criterion?

EC: It’s definitely a really important one, but I wouldn’t value a company solely in terms of cash. Unless a company has strong targets and management that’s willing to be proactive about those targets, there’s no real rush to buy it.

TGR: Considering how bad it has been for junior mining equities, what is it that keeps you excited? What is it that keeps you in the market?

EC: I’ve always been a discovery guy, and I’m always looking for good development stories. Being there for the big drill hole and swinging for the fences is probably what keeps me interested. I don’t think we’re done discovering new deposits. It has never been easy, and it is probably getting harder, but the big discoveries are what get everybody excited. When they work, you see these stocks going up 400%, 500%, 1,000%. That’s what keeps people in the game.

TGR: Eric, thank you, for speaking to us today.

EC: The Gold Report readers can access my exclusive interview with a company that has made HRA subscribers gains of 750% over the past seven months. Click here to access this and our special subscription offer now.

About Eric Coffin

Eric Coffin is the editor of the HRA (Hard Rock Analyst) family of publications. Responsible for the “financial analysis” side of HRA, Coffin has a degree in corporate and investment finance. He has extensive experience in merger and acquisitions and small-company financing and promotion. For many years, he tracked the financial performance and funding of all exchange-listed Canadian mining companies and has helped with the formation of several successful exploration ventures. Coffin was one of the first analysts to point out the disastrous effects of gold hedging and gold loan-capital financing in 1997. He also predicted the start of the current secular bull market in commodities based on the movement of the U.S. dollar in 2001 and the acceleration of growth in Asia and India. Coffin can be reached at hra@publishers-mgmt.com or the website www.hraadvisory.com.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Gold Report and provides services to The Gold Report as an independent contractor.

2) Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Eric Coffin: I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2013 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

It may have been a modest effort, but modest was still good enough to carry the market to record highs last week. Even more interesting – and perhaps a little surprising – is that volume was growing on the way up. That suggests traders at least have a little faith in the budding rally.

The $64,000 question is, do we/you really believe the market is capable of rallying in late July and early August (historically a tepid time of year) after it’s already advanced 6.3% in just four weeks? Stocks are already over-extended, and shouldn’t be able to keep chugging at their recent pace. The answer: Never say never… especially during earnings season.

We’ll put that answer under the microscope in a moment, after we paint the bigger picture with last week’s and this week’s economic numbers.

Economic Calendar

Contrarian thinking is easy but successful contrarian investing is difficult. Most amateur contrarians neglect that the crowd is right most of the time. It’s only at market turning points where the crowd is wrong and contrarians are right. In recent weeks the voices against precious metals have not only appeared but grown. Weeks ago we debunked a rant of a widely followed mainstream blogger and commentator. He was ranting against the gold stocks and his rant was devoid of any analysis or actionable information. Meanwhile, more mainstream calls to sell gold stocks have popped up and during what likely will be exactly the most inopportune time to sell.

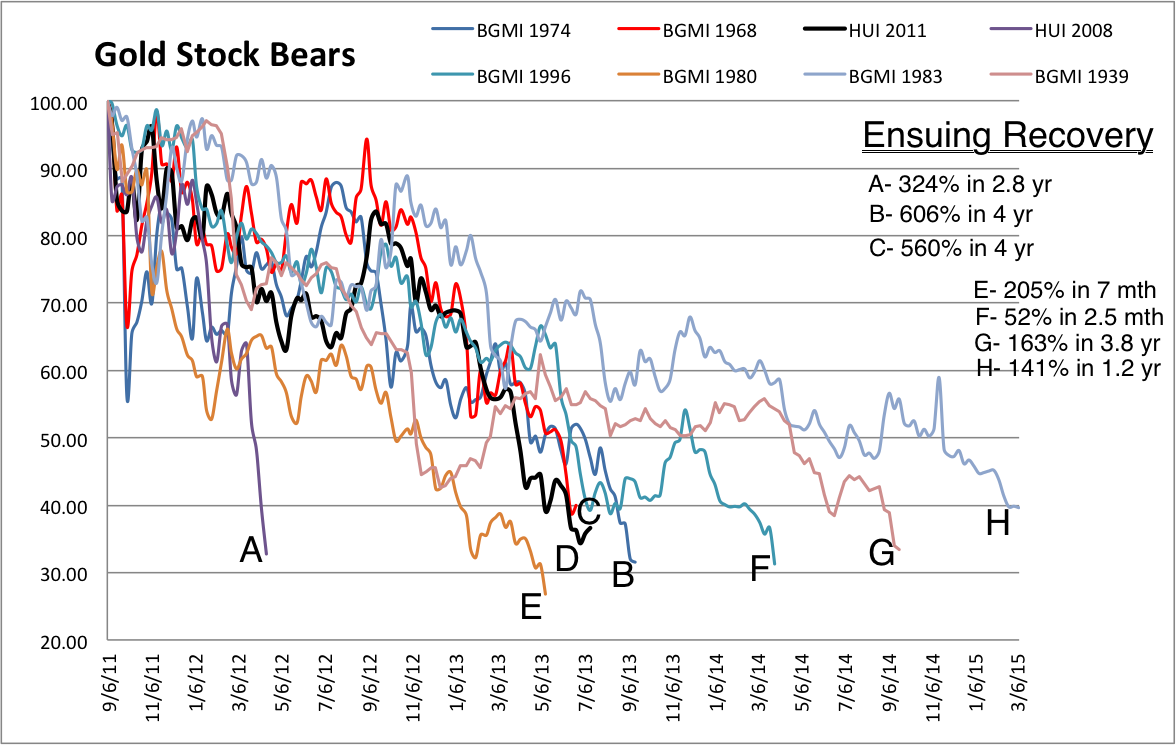

On Yahoo Finance TV, host Jeff Macke and Mike Santoli, a respectable commentator formerly of Barrons tried to analyze the gold stocks on a segment called “The Trade.” While they make a few good points their ignorance is overwhelming. They mention Newmont Mining as the blue-chip stock of the sector. There is no mention of Franco-Nevada which most would consider the blue-chip of the sector and the company that makes the most sense given their discussion of the difficulties of mining. They are telling people to sell the sector after its already declined over 60% and the cyclical bear is long in the tooth. Clearly these gentlemen have not done the historical analysis like we have (the chart below) which shows that this decline is typical during a secular bull market in gold stocks. On a show called “The Trade” these guys couldn’t come up with what is quite obvious from the chart below.

Moving along, an anti-Gold commentator from MarketWatch tried to debunk the bullish supply argument in “Gold is a popping Bubble”:

Another key argument that gold has hit support is the idea that miners are at breakeven on production costs and will not be willing to extract more metal from the ground — thus limiting supply and boosting prices. However, it’s willfully naïve to think that major miners like Barrick Gold or Newmont Mining will simply shut down and bleed cash. They have payrolls to make, operations that require maintenance and — most importantly — debt to service. Consider that Barrick had $14.7 billion in total debt as of its first-quarter earnings report, which isn’t going to pay for itself. Like it or not, these companies will continue to mine simply to keep the lights on, even if it’s not in their long-term interest – which is one of many reasons that gold miners are a bad investment right now.

This is an epic fail. Mine to keep the lights on? At breakeven? Ever heard of turning the lights off? Companies shut down mines because they can’t make money (or enough money) and they can layoff employees as Barrick is doing. Clearly this author spent no time supporting his bizarre assertion with any facts. When the price goes too low, future supply shrinks. This isn’t rocket science. The key word is future. It doesn’t impact the short-term market trend but does so later on.

The root of the problem here is the majority of the mainstream fails to understand not only Gold but the mining industry and the proper way to invest in mining companies.

The mining industry is unlike most industries. It is a venture type industry where performance is skewed and not uniform across the sector. In secular bull markets you can make money buying the mining sector but it does underperform the metals. This is true now and it was from 1960 to 1980. Yet, everyone acts as if today’s underperformance is some revelation. It’s not. It happened in the last secular bull market and will continue in the coming years. Therefore there is little reason to buy and hold the sector. Rick Rule has said if you buy the sector you’ll get killed.

The huge returns and strong outperformance are a result of picking the right companies and buying at the right time. This requires proper due diligence of the industry as well as due diligence on the companies. The mainstream doesn’t have the time for this. These guys are too busy staring at a computer screen, tweeting, hosting shows, and being interviewed to conduct proper due diligence and historical analysis.

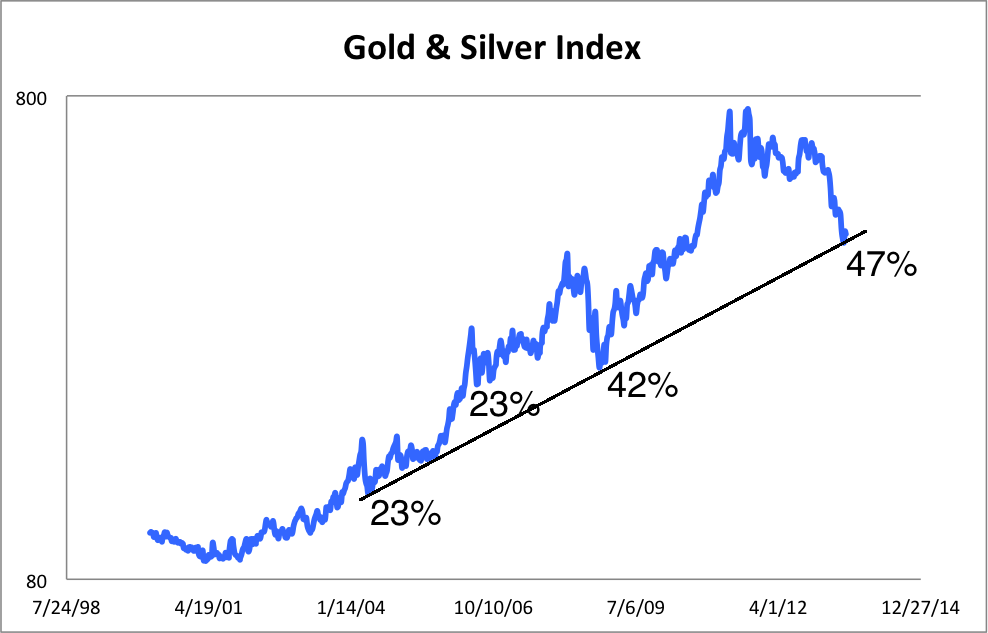

Speaking of historical analysis, many are quick to compare Gold’s decline (36% in nearly two years) to 1980 (40% in two months) without even mentioning 1976 (45% in eighteen months) which is the better comparison. Below is an index of Gold and Silver comprised of half of each. The recent decline bottomed at multi-year trendline support and is closely in-line with the 2008 decline. In 1980 this index declined 54% in two months! After two and a half years it was down 75%.

The bottom line here is twofold. First, the growing mainstream negativity toward the gold stocks (after a 65% decline) is a textbook contrarian buy signal. It comes at a time when historical analysis suggests this is the best time to buy and when valuations are at multi-year lows. Second, one should consider the gold stocks a venture capital type of investment. Don’t buy the entire sector but look to buy specific stocks. That is how wealth is attained. While GDX and GDXJ are starting to rebound there are a fair number of stocks which have spent several months bottoming and look ready to lead the the sector in the coming months. If you’d be interested in our analysis on the companies poised to recover now and lead the next bull market, we invite you to learn more about our service.

Jordan Roy-Byrne, CMT

“High oil prices tend to prick investment bubbles.”

History does not necessarily repeat but it certainly rhymes. Think back five years to July 2008 and oil prices peaked at $147 before giving way to a slump to $33 by December as the global financial crisis struck.

History does not necessarily repeat but it certainly rhymes. Think back five years to July 2008 and oil prices peaked at $147 before giving way to a slump to $33 by December as the global financial crisis struck.

This July WTI crude has jumped to $107 a barrel. That’s a tax on consumers and business. Surging oil prices are a proven recession indicator.

Gulf Wars

Think back to the First and Second Gulf War’s and the recessions that followed. High oil prices tend to prick investment bubbles.

Will it be different this time? Stock markets in advanced nations look very high with the global economy cooling down. House prices have also picked up courtesy of the Fed’s money printing and low interest rate regime.

These are the asset price bubbles that now look vulnerable. Gold and silver have already seen their big correction, and bonds prices have tumbled a huge 40 per cent in two months.

House prices are also now stalling after a hike in mortgage payments over the past couple of months. So why are stocks and oil still going up in price?

This is liquidity driven speculation of the sort that always ends in tears. Buying an asset class close to the top of its price cycle is always a bad idea. You have a lot of risk and little room for gain and much for pain.

Speculators always reckon they can close out their positions before markets reverse. But their track record is not good. Most get caught out in leveraged positions as markets head south and lose their shirts.

Yes the Middle East has geopolitical issues by the bucket load but there is nothing new and local civil wars and social and economic unrest are perhaps too much of a preoccupation for anything really exciting to happen.

Cash is king?

It would be far more sensible to liquidate and go into cash at this point and/or put money into assets that have already hit bottom, or must be very close to it like gold and silver.

We think high oil prices are an obvious red flag warning of trouble dead ahead for global financial markets.

Of course, $107 is lower than $147 in July but the global economy is in a much weaker condition that it was then and will therefore breakdown at lower oil prices than it did in 2008.

About Arabian Money

Arabianmoney.net is the first dedicated financial comment website to be published from Arabia, and provides lively and topical commentary on both local and global news. This is a free website that introduces the more detailed investment analysis and actionable investment ideas and tips available only in our paid-for subscription newsletter. Anybody seriously interested in Arabian investment should get this monthly publication (subscribe here).

First Reading on EPS and Revenue Beat Rates

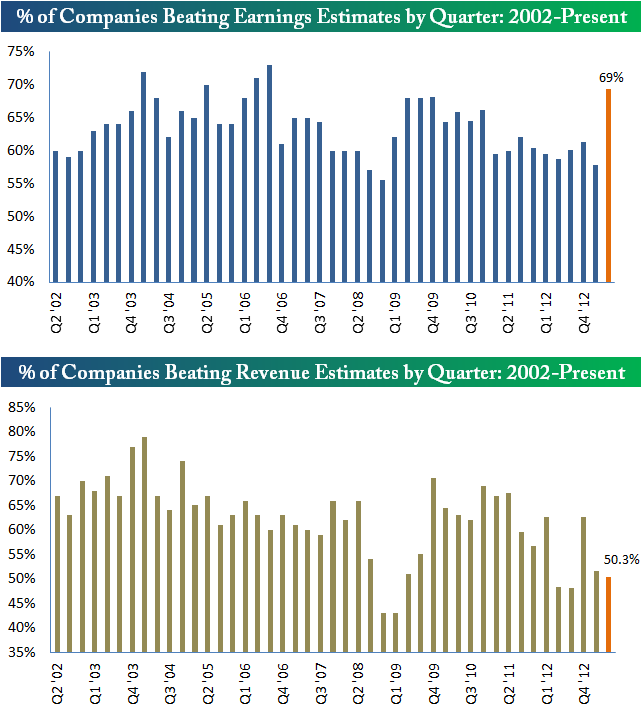

Roughly 150 companies have reported earnings since the second quarter reporting period began on July 8th. While this is less than a tenth of the total amount of companies set to report throughout earnings season, it’s enough to get an initial reading on the percentage of companies beating earnings and revenue estimates.

As shown in the first chart below, 69% of companies have beaten earnings estimates so far this season. It’s still very early, but compared to the final quarterly readings over the past few years, the earnings beat rate has gotten off to a great start. The revenue beat rate, on the other hand, has been below average at just 50%. Top line numbers have struggled in three of the last four quarters, and it’s looking like the same could be in store this quarter as well.

Looking for more earnings season analysis? Sign up for a 5-day free trial to Bespoke Premium and use “earnings” in the coupon code section on our Subscribe page to receive a 10% discount on your membership.

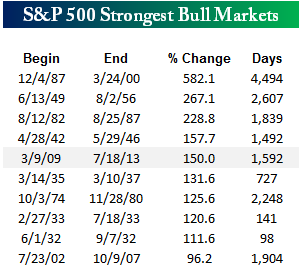

S&P Up 150% But Still in Fifth Place

With today’s rally, the S&P 500 is now up 150% since its closing low on 3/9/09. Relative to other bull markets going back to the late 1920s, the current bull ranks as the fifth strongest of all time. As shown in the table to the right, the strongest bull market for the S&P 500 was a gain of 582.1% from December 1987 through March 2000. In order for the current bull run to move into fourth place, the S&P 500 would need to rise above 1743.4 without a 20% decline on a closing basis. Based on current levels, that translates to a gain of 3.1% from here.

With today’s rally, the S&P 500 is now up 150% since its closing low on 3/9/09. Relative to other bull markets going back to the late 1920s, the current bull ranks as the fifth strongest of all time. As shown in the table to the right, the strongest bull market for the S&P 500 was a gain of 582.1% from December 1987 through March 2000. In order for the current bull run to move into fourth place, the S&P 500 would need to rise above 1743.4 without a 20% decline on a closing basis. Based on current levels, that translates to a gain of 3.1% from here.

For reference, we define a bull market as any period where the S&P 500 rises 20% or more (on a closing basis) without a decline in between of 20%.

About Bespoke

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair