Real Estate

The two largest benefits of investing in Commercial Real Estate are as follows;

The two largest benefits of investing in Commercial Real Estate are as follows;

1. The landlord has more power than the tenant (anyone who is a residential landlord in Canada is aware that more often than not, landlords are at the mercy of their tenants); and

2. The owner has myriad opportunities to increase the value of the real estate asset by decreasing expenses, replacing a tenant with a better paying one, dividing space and charging more per square foot, changing the allowed use of the property, redeveloping the property, and so on.

….continue reading HERE

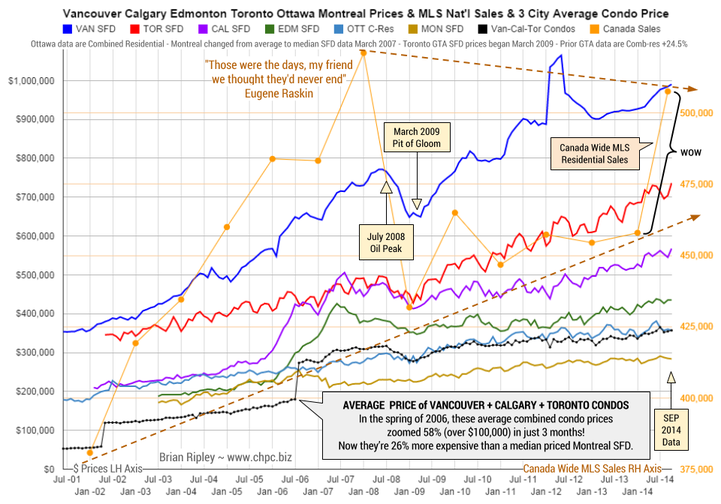

In September 2014 Calgary and Toronto single family detached average prices hit new historical highs on Absorption Rates that are the highest among Canada’s 6 biggest cities. Look also at the total MLS sales across Canada which are projecting the biggest single year since the 2008-2009 plunge. It’s been a banner year for sales.

Click Chart twice for Larger View

The chart above shows the average detached housing prices for Vancouver, Calgary, Edmonton, Toronto, Ottawa* and Montréal* as well as the average of Vancouver, Calgary and Toronto condo (apartment) prices (Left Axis). On the right axis is the MLS Annual Total Residential Sales across Canada; the most recent data point being a projection to year end.

Meanwhile Edmonton, Ottawa and Montreal ticked down in their flat channels and Vancouver ticked up inside Bull Horse Mt.

It remains interesting to note that the combined average price of a Vancouver, Calgary & Toronto condo is currently 26% more expensive than a median priced Montreal SFD and note also that in the spring of 2006, those 3-City average condos zoomed 58% in price (over $100,000) in just 3 months as the buy side of the market freaked out over the inversion of the 10yr less the 2yr spread as it went negative (Yield Curve).

Mattress money has gushed into condos with no respect for fundamentals or plan for contingencies that may be required if Pit of Gloom II develops and one must write off capital gains and rely on employment earnings.

….related:

- 6 BIG METRO SALES & LISTINGS Total Residential

Vancouver, Calgary, Edmonton, Toronto, Ottawa & Montreal - MONTHLY ABSORPTION RATE & MONTHS of INVENTORY Vancouver, Calgary, Edmonton, Toronto, Ottawa & Montreal

- HOUSING STARTS since 1955 Canada, Quebec, Ontario, Alberta & BC

- VANCOUVER Housing Prices of Single Family Detached, Townhouse & Condos as well as total residential Sales and Inventory. The page also includes charts for the Deflator (prime area listings over-under $750,000) and Strata unit prices as a % of SFD prices and a 10 year comparison of increases in SFD prices and Family Income.

- BULL HORSE MOUNTAIN The Bull Trap that is Vancouver Housing; includes the Double Double chart.

- CALGARY Housing Prices of Single Family Detached, Townhouse & Condos as well as total residential Sales and Inventory. The page also includes charts for Strata unit prices as a % of SFD prices and a 10 year comparison of increases in SFD prices and Family Income.

- TORONTO Housing Prices of Single Family Detached, Townhouse & Condos as well as total residential Sales and Inventory. The page also includes charts for Strata unit prices as a % of SFD prices and a 10 year comparison of increases in SFD prices and Family Income.

- TORONTO COMPARED with VANCOUVER Single Family, Townhouse, Condo & Other Metrics including Absorption Rates and charts for Strata unit prices as a % of SFD prices and a 10 year comparison of increases in SFD prices and Family Income.

- HOUSING PRICE MOMENTUM Price Change Y/Y

Vancouver, Calgary, Toronto & TSX Real Estate Index - TSX INDEXES & Canadian Commodities Index

Real Estate, Gold, Energy, Financial Services & Commodities - MILLIONAIRE METRIC Vancouver, Calgary, Toronto SFDs & Cash Millionaires priced in Gold

![]() Are you thinking about selling? Best to consider these factors and avoid the following traps.

Are you thinking about selling? Best to consider these factors and avoid the following traps.

1. Profit has been maximised: When a property has reached maximum value, there is little value in holding onto it for longer. Therefore this is generally considered the optimum time to sell.

2. Property has not performed: Having cash or equity tied up in an investment that has not performed (over a reasonable time period) can prevent an investor from reaching their financial goals.

3. Better opportunity elsewhere: Investors should know how each of their properties are performing relative to a) others in their portfolio and b) those in the market place. If another opportunity presents itself with greater investment prospects then it should be considered.

4. Depreciation has been maximised: Depreciation on a property lasts for up to 40 years from the time of construction. Over time the value of depreciation recedes. This could weaken a property’s cash-flow position to the degree that it becomes better to sell.

While a forced exit can cause investors to panic and make easily avoidable mistakes, there are a number of traps that any investor wanting to exit a property needs to be aware of, according to experts.

These include:

-Selling too soon – before the market has started moving. This can impact on capital gains and, thus, the profit made.

-Holding for too long until demand has dropped off and the market is going down. This can prolong the sales process and result in a lower price.

-Selling to buy in a rising market, but then sitting on the sidelines. If an investor sells in this scenario, they shouldn’t then neglect to buy a property as intended.

-Forgetting to factor in selling costs (eg: agent commissions, legal costs and the like).

-Cross-collateral implications with lenders: Selling might trigger the need for valuations on other properties in a portfolio. This, in turn, could impact on the value of the portfolio.

….related by Canadian Real Estate Wealth:

Calls for more transparency from CMHC denied

Why you should consider commercial investing?

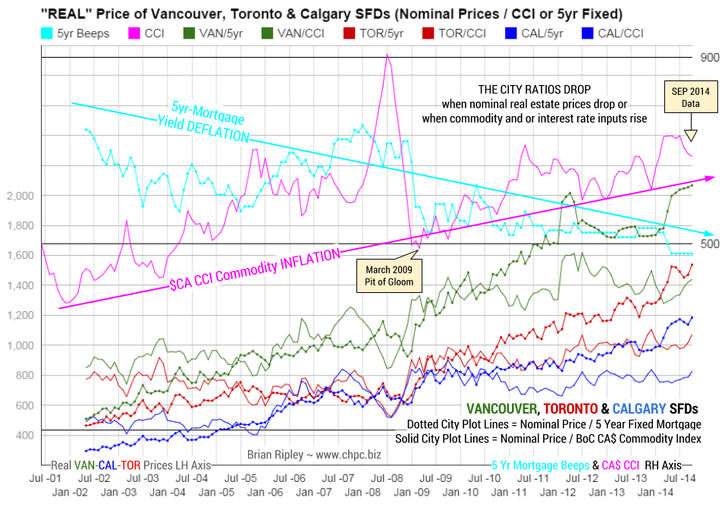

The chart above shows the “real price” of Vancouver, Toronto & Calgary SFDs when looked at from the point of view of the BoC Canadian Commodity Index (CCI) and Borrowing Costs (5yr Mortgage) which are the main input costs apart from operating expenses and tax.

In September 2014 the CCI (solid pink line) continued dropping after a failed breakout above the previous major high set in April 2011. The cost of stuff is still keeping the “real” price of SFDs (solid city lines) well below the Spring 2012 highs, but the gap is closing.

The other major cost input, the retail 5 year fixed mortgage rate (aqua dotted line) remained at the April 2014 record low of 4.79% or 35 bps below the previous 5.14% low of July 2013.

Neighborhood banks are advertising sub 3% five year fixed mortgages. Hello Japan. The fire sale mortgage rates are allowing the real cost of housing (city dotted lines) to continue floating up to new monthly and historical highs.

…related:

TSX Energy, Real Estate, Financial Services, Gold and the Bank of Canada Commodities Indexes

Calgary set to break MLS records… Report highlights income gap between generations… Low rates likely to be the norm says BoC deputy… US existing home sales fall but market is good…

Calgary set for record breaking September

Calgary set for record breaking September

A report from the Calgary Real Estate Board suggests that September could break records for MLS sales. The board says that sales are up 11.6 per cent on the same time last year, with 1,500 sales to 21st September and the pace continues. That could mean that this month will beat the record set in 2005 when 2,197 MLS sales were recorded. Last year came close with 1,919. New and active listings are both higher than last year, while realtors say prices are at a record for September. The luxury market in Calgary is buoyant and there has been a resurgence of single-family home sales after two months of year-over-year decline. Read the full story.

Report highlights generational income gap

Twenty-somethings are the first generation to be financially worse off than their parents. New figures from the Conference Board show that over the last thirty years the gap in incomes between older and younger workers has widened; in the 80’s it was 47 per cent, now it’s 64 per cent. The report shows that in many workplaces older workers are being paid more than younger colleagues for doing the same job and while there is often a premium paid for experience it is not always a factor in the wage differential. For the housing market it highlights a big problem of course; younger first-timers struggling to afford a home and older down-sizers affected by stagnation further down the ladder. While an overheated market may be a current factor, the income gap is a longer term concern for the market. Read the full story.

Low rates still needed says BoC deputy

There are signs that the interest rates may stay low for some time to come. Senior deputy governor of the Bank of Canada, Carolyn Wilkins says that output growth may stay lower than it was before the financial crisis and there may therefore need to be continued stimulus for the economy over a longer period. That would include lower interest rates; not the 1 per cent we have seen over the last four years, but more in the 3 to 4 per cent range rather than the 4.5 per cent of the mid 2000’s. Read the full story.

US existing homes fall back

Investors are scaling back their involvement in the US property market but this is unlikely to mean a return to dark days for the market. Figures from the National Association of Realtors show that August saw declines in existing home sales of 1.8 per cent, however this followed four months of increases and the level of sales is still the second highest of the year so far. The level of investors’ involvement was at its lowest for 5 years with expectation of interest rate rises during 2015. Outside of the investment world the US housing market is still showing positive signs with a steady rate of first-time buyers and buyers sentiment increasing. Read the full story.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair