Real Estate

Ozzie Jurock explains his recent newsletter “4 Reasons” headline in the title above. A recent update about what is now being called the “moral” and “ethically” wrong BC tax on foreign buying of Vancouver real estate, the recent numbers on Vancouver real estate as well as Ozzie’s two ‘Hot Properties”.

Don’t miss Featured Guest: Dennis Gartman: Major Markets Are Heading Down

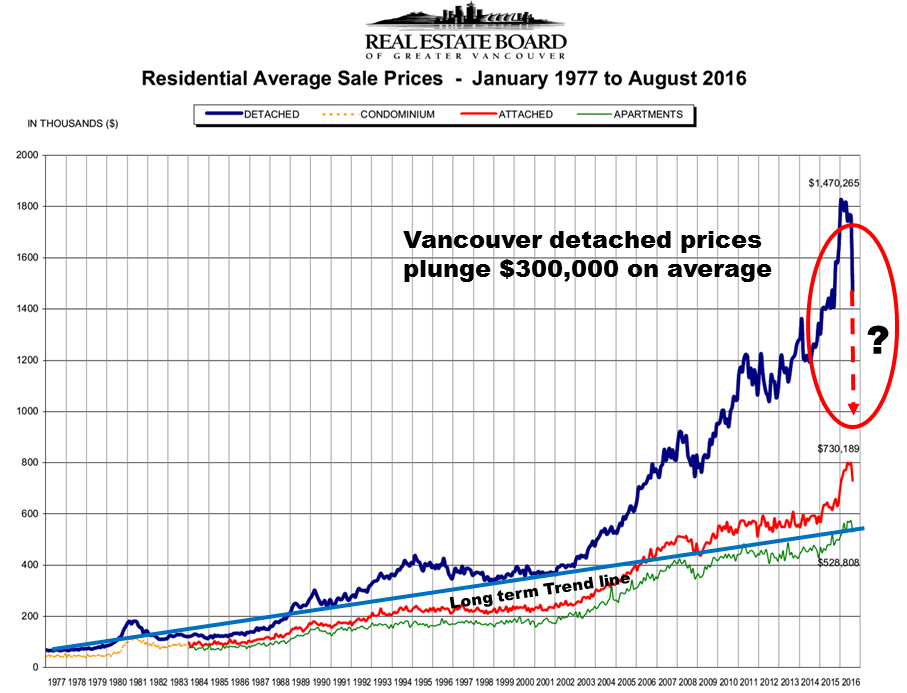

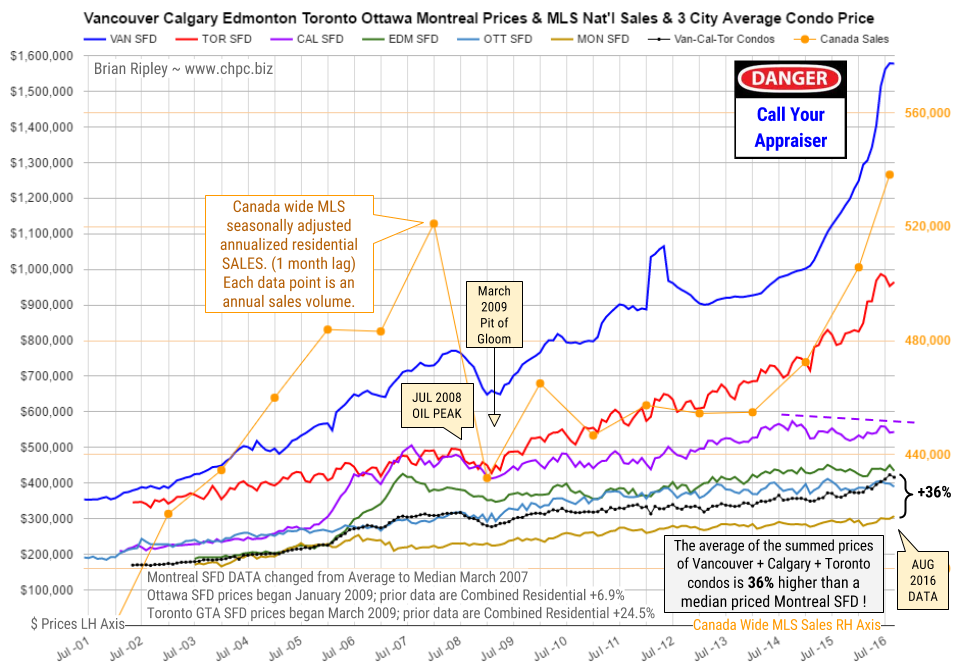

In August 2016 Canada’s big city metro SFD prices hit resistance M/M except in Montreal where a new peak price came in. Toronto absorption rates are at the highs with months of inventory at 1; a new benchmark in mania. Anyone owning a house in the scorching hot Vancouver and Toronto markets is sitting on an unredeemed lottery ticket… if buyers still exist and apparently they do.

The chart above shows the average detached housing prices for Vancouver*, Calgary, Edmonton, Toronto*, Ottawa* and Montréal* (the six Canadian cities with over a million people) as well as the average of the sum of Vancouver, Calgary and Toronto condo (apartment) prices on the left axis. On the right axis is the seasonally adjusted annualized rate (SAAR) of MLS® Residential Sales across Canada (one month lag).

High net worth trophy hunters have spent the last few years picking off well located SFD properties in hot markets while the hoi polloi settled for anything before being “priced out“. Are they going to enjoy being “priced in“?

CMHC is not so sure. In November 2015 CMHC had a private audience in New York City and brought along a stress test of $35/bbl oil and its potential effect on Canada. I covered the bullet points here. Scenario 2 “if global deflation” is worth consideration for anyone heavily leveraged. The search for cash flow could be a buzzkill in 2016. When earnings drop so do asset prices.

….related:

Ozzie Jurock on the declines in Alberta’s top markets. He likes them, but Calgary and Edmonton? Not yet.

Don’t miss Michaels Editorial: Hillary or Donald? Who Cares?

Mortgage penalties are one of the most important aspects of choosing a lender and a mortgage term, but surprisingly one of the least asked questions from prospective clients. Although saving .1% on a $300,000 mortgage would save $300 per year, adding up to $1500 over 5 years, choosing a lender with a more favourable penalty calculation could be the difference between a $2,500 penalty and a $14,500 penalty. Pinching pennies to cost you dollars.

Mortgage penalties are one of the most important aspects of choosing a lender and a mortgage term, but surprisingly one of the least asked questions from prospective clients. Although saving .1% on a $300,000 mortgage would save $300 per year, adding up to $1500 over 5 years, choosing a lender with a more favourable penalty calculation could be the difference between a $2,500 penalty and a $14,500 penalty. Pinching pennies to cost you dollars.

So how do banks and other lenders calculate penalties?

First off, there are closed mortgages and open mortgages. Closed mortgages incur penalties when you break the mortgage and open mortgages have no penalty to break them. Generally, most mortgages are closed because the interest rate is best on closed mortgages. Lines of Credit are open (and a higher rate than a closed variable mortgage), generally fixed mortgages are not open. If the mortgage is closed, there are two primary types of penalties: 3 months interest and Interest Rate Differential (IRD).

3 months interest penalty

Most borrowers are aware of the standard penalty, which is 3 months interest. It’s also quite easy to calculate as well. $300,000 mortgage @3% is $9,000 per year, divided by 4 is $2,250. 3 months interest is the maximum penalty if you are taking a closed variable, although some banks calculate the rate at the Prime rate and some calculate it based on the net rate (most of the time, market rates are Prime minus a discount). This can make choosing a variable rate a more attractive option and in general, we are usually recommending a variable to our investor clients. However, most borrowers don’t realise that this is not the only penalty that may apply if you take a fixed rate mortgage.

Interest Rate Differential

Here’s the big one. I have had some big IRD’s in my career. One from a few years ago was about $76,000 on a $700,000 mortgage. Another was $200,000 on a $1,000,000 commercial mortgage. The whole purpose of the IRD penalty is to ensure the bank doesn’t lose money on your mortgage. An IRD is effective if the current market rates for the same term remaining is lower than your current rate. If it is, the penalty is the difference between the rates, over the remainder of the term. So if you borrow money from the bank at 6% and then a few years later rates are 4%, you would want to refinance to get the better rate, right? The problem is, you signed a contract with the bank to pay that amount. And the bank also likely has a contract in place to pay someone else a rate of return, probably around 1.5% less than what you are paying. The bank is likely paying someone else 4.5% for the money they lent to you for 6%, so they wouldn’t want to just let you get out of the contract for free. So is it fair to penalize you to get out of your contract early? Well, yes….as long as it is fair. The problem is, banks don’t have a “fair” calculation.

How the banks “get you”

First, let’s explain how a “fair” penalty calculation should look. Let’s use current interest rates, and assume rates don’t change over the term of your mortgage.

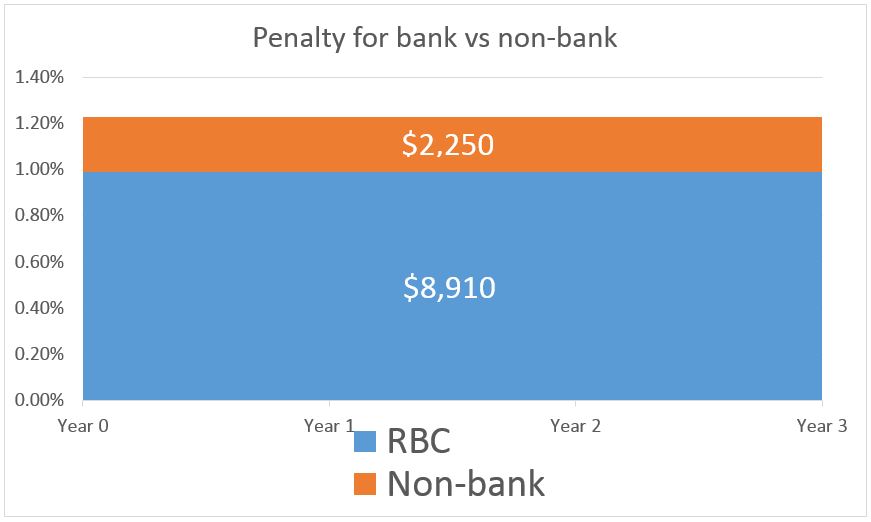

$300,000 mortgage, at 2.49% for 5 year fixed. You keep it for 2 years and break it with 3 years remaining. With a non-bank lender, their current 3 year term is 2.24% so your penalty would be .25% on $300,000 over 3 years, about $2,250 (the 3 month interest penalty would be ~$1,850 but since it is less the IRD applies here).

Let’s try this again with a major bank. How about RBC, just because…well, they’re the biggest. The big difference here is that the banks manipulate posted rates in a way that creates large, unfair penalties. Really, what purpose do posted rates have today anyways? If you pay the full price for posted rates you have probably been living under a rock for the past decade and a half or two.

$300,000 mortgage, 2.49% 5yr fixed (4.64% posted 5 year, so a discount of 2.15%). Posted 3 year rate is 3.65%.

This will probably need some visualization to understand:

So in essence, the non-bank is charging a difference of .25%, and the major bank will use the difference of .99% (2.49% vs 1.5%). This is a quick graph showing the difference in cost:

In essence, it is pure manipulation of the posted rates that cause these high penalties as they heavily discount the long term rates and offer small discounts for short term rates. As of writing this, the discount off a 3 year fixed may be around 1.4% whereas the long term rates are over 2% discounted.

What to watch out for

Keep in mind, most lenders do offer to port your mortgage if you sell but a lot of our clients have been finding it difficult to port when they sell. We have had clients who have actually improved their finances since buying their home but now aren’t able to port their mortgage. An example is when you take a 5 year fixed rate of say 2.49%, they use the actual rate to qualify you. But, if you are porting and have less than 5 years remaining, the “qualifying rate” is actually 4.74% right now. This can put you in a situation where you may be paying a large penalty to break your mortgage and simply getting a similar rate on the market, which can often be a net loss.

How to avoid the penalties

The easiest way to avoid the penalty is to generally take a variable rate or a short term fixed rate, or if taking a long time fixed rate go with a non-bank lender. Make sure you understand how lenders port as well. Credit Unions for instance can’t port outside of their lending area so if you get a mortgage with Vancity in Vancouver and want to sell and buy in another province in a few years, you may be faced with a large penalty.

Most lenders do allow for a pre-payment on your mortgage so if you have some extra cash lying around and you know you will be paying a penalty, check out how much you can pre-pay per year. It usually varies between 10% and 20% per year.

Why you may still want to use a bank

If you are just taking a cookie cuter mortgage and want the best rate and terms, non-bank lenders that are only accessible through mortgage brokers are usually your best bet. They generally have lower rates than the big banks and their penalty calculations are generally better. That said, non-bank lenders cannot offer the same products as major banks can. Some of the products banks can offer that non-banks can’t include:

– Home Equity Lines of Credit

– Best rates and terms on rental properties

– New to Canada and Non-resident mortgages

– Net worth or equity mortgages (which are nearly extinct now)

– Many other types

Just make sure you are aware of the differences and make sure you ask the right questions. IF you think you may be selling shortly and may not buy something else and port, you should probably be taking a short term rate or a variable rate.

If you would like to get a professional opinion to compare different options, contact Kyle Green at 604-229-5515 or Kyle@GreenMortgageTeam.ca.

Ozzie walks through the Vancouver area real estate sales numbers. Some areas up and some sharply down. One thing for certain, foreign buyers are leaving for greener pastures.

…Featured Guest: Be Really Careful Here

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair