Real Estate

Ozzie tracks down the beneficiaries of the flood of cash escaping the Vancouver area with its foreign buyers tax. Certainly one area is benefiting, Calgary, with the big smart money investing there and other places like Grande Prairie.

….also Josef Schachter: On The Brink of a Wonderful Buying Opportunity

The Federal governments new mortgage rules just announced will have a significant impact on the mortgage industry and could kill a lot of the dreams of millennials and 1st time buyers with low equity.

…also: Live from the trading desk: The Big Themes Keep Making Money

![]()

The Department of Finance threw a major wrench into the gears on Oct 3 by making huge material changes to the way that many borrowers get qualified. Here’s a rundown of what is changing and how it impacts you and the market.

What is changing?

Effective Oct 17th, the qualification rate will apply to all insured mortgages, not just those taking terms shorter than 5 years or choosing variable terms. Currently the qualification rate is 4.64%. Many first time home buyers have been forced to choose a 5-year fixed rate as they would qualify at the actual rate itself instead of 4.64% (currently 5 year fixed rates are at or below 2.49% in most cases).

The rules kick in for any applications received by the insurer after Oct 17th, but in many cases lenders will stop taking new applications a few days in advance to give them time to prepare and submit deals to the insurers.

In order to be sent to an insurer, you must have a live deal (an accepted offer). Pre-approvals do not count.

This will not impact existing mortgages already in effect or existing mortgage applications that have already been approved (not just pre-approved).

Capital Gains for non-residents

Non-residents will no longer be able to claim the capital gains exemption for selling a principal residence if they were not a resident in Canada in the year the individual acquired the residence (a good thing)

This will impact those who attempt to flip houses and not pay the capital gains tax

Impact of the new rules (there are a lot)

Lower borrowing power for buyers, specifically those with 20% down but also those who may need to qualify on a program that banks require to be insured, even if you have over 20% down (like self employed programs, small square footage units, small towns, etc.)

Assuming the median income of $76,000 per year, the maximum borrowing power for someone who used to be able to purchase a $500,000 property with 10% down now qualifies for about a $425,000 purchase

Assuming an income of $100,000 per year, the maximum borrowing power for someone who could purchase a $700,000 property now qualifies to purchase around a $550,000 purchase.

Overall, a decrease in borrowing power of around 15% – 20%

Less competition – Non-bank lenders insure most or all of their mortgages and if they are unable to insure certain mortgages, those clients will have to deal with deposit taking institutions who can place those clients on their own balance sheet

Already the largest non-bank lender has pulled out of financing conventional (more than 20% down) rentals and business for self applications

Higher rates – If banks have to balance sheet applications, interest rates, especially for rentals, self employed, and other hard to insure business, will increase as the cost of funds is higher when they are not able to sell the mortgages in the secondary market as “MBS” (Mortgage-Backed Securities)

Renewals that are conventional (more than 20% equity) coming up that don’t fit the below criteria won’t be able to remain insured which may increase the cost, and so the best rates may not be passed on to those who don’t fit these criteria. These rules apply Nov 30, 2016.

Loan for a purchase of a property or renewal

Owner occupied (sorry, no rentals)

Maximum amortization of 25 years

Maximum purchase price of $1,000,000 at the time the loan is approved

Minimum 600 credit score at time of approval

Max Gross Debt Servicing of 39% (all housing related expenses) and Total Debt Servicing of 44% (all expenses including housing related and credit cards, loans, etc.) by applying the greater of the mortgage rate or the Bank of Canada five-year rate (4.64%)

If there are less non-bank lenders doing rentals, self employed, etc., that business will likely flow to the few remaining banks who are doing them. If this is the case, the banks will likely either tighten guidelines to stem the flow of new business or surcharge the rates for “unique” deals

Margins will shrink for non insured mortgages, which may create a larger gap between insured and uninsured mortgages (currently best rates are for owner occupied with less than 20% down, at about .1% better of a rate)

Revised B-20 guidelines are likely to include qualifying at the Bank of Canada rate even for those with over 20% down, we are being told. News have not been officially announced but seems likely at this point

Amortizations over 25 years may be surcharged or simply not available as banks won’t be able to insure those mortgages

“A-“and “B” lenders’ market share will increase as deals get tougher to do

Credit Union market share may also increase as these rules only apply to federally regulated lenders. Credit Unions are provincially regulated.

A Bank of Canada overnight lending rate (which impacts the Prime rate) drop seems more likely as:

Mortgage rules are often created to slow the housing market in an effort to curb the upward surge of real estate prices due to a low interest rate environment. This could be some foreshadowing, here

There is likely going to be a GDP hit from these new rules as oil and housing are two of the largest determinates of our GDP growth and are both on the ropes

Negative news to foreign buyers via the Capital Gains changes as well as the previous 15% foreign buyers tax in BC will deter foreign investment which Canada needs

What should you do?

If you plan to buy, make sure you know how the new rules will impact you. You may wish to pull the trigger sooner rather than later.

If you are buying a pre-sale, make sure a full application is made through your broker or bank to get an insurer’s approval now. The rate may not be guaranteed but at least the financing will be approved.

Refinance now. You are most likely to get the higher possible appraised value that we will be seeing for the short-medium term and new rules may make this more difficult to obtain

Suck up to your favourite Credit Union. They may become your best friend. I know I am (and will continue to be).

Can we please have a chat with Finance Minister Bill Morneau about the lack of government intervention in CREDIT CARD DEBT which is the main culprit to many personal bankruptcies and bury individuals in debt payments with card rates up to 29%?

Indeed, Kyle!

Their bone-chilling chart

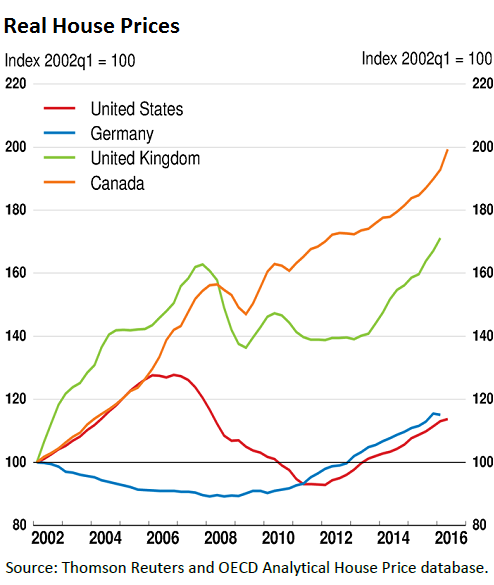

Everyone is fretting about the Canadian house price bubble and the mountain of debt it generates – from the IMF on down to the regular Canadian. Now even the Bank for International Settlement (BIS) and the Organization for Economic Co-operation and Development (OECD) warn about the risks…..continue reading HERE

…related:

It looks like the foreign buyers tax has put the breaks on Chinese buying in vancouver – but the big question is where will the money go now. Ozzie on some of the actual numbers in reaction to the foreign buyers tax. Also this weeks “Hot Properties”.

Michael Campbell’s Editorial: Oh No Not Again

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair