Timing & trends

China Deflation Fears Grow

Bad news stories continue in China today with reports of more capital controls, devaluation fallout, and another drop in the Producer Price Index (PPI).

Bad news stories continue in China today with reports of more capital controls, devaluation fallout, and another drop in the Producer Price Index (PPI).

Reuters reports China Deflation Fears Grow as Producer Prices Sink Most in Six Years.

China’s manufacturers slashed prices at the fastest rate in six years in August as commodity prices fell and demand cooled, signaling stubborn deflation risks in the economy and adding to expectations for further stimulus measures.

The producer price index (PPI) fell 5.9 percent in August from the same period last year, its 42nd consecutive month of decline and the biggest drop since the depths of the global financial crisis in late 2009, data showed on Thursday.

Official and private factory surveys last week also showed manufacturers laid off workers at a faster rate last month as their order books shrank.

More Capital Controls

The Financial Rimes reports Beijing Clamps Down on Forex Deals to Stem Capital Flight

China has tightened its capital controls, in a sharp reversal of its market liberalising rhetoric, as it struggles to contain the fallout from last month’s devaluation of the renminbi.

The August 11 devaluation unleashed turmoil on global stock markets and policy confusion at home, forcing the central bank to spend up to $200bn to support the currency. The prospect of an interest rate rise in the US has further encouraged capital flight.

The Safe [State Administration of Foreign Exchange] has ordered banks and financial institutions to pay particular attention to the practice of over-invoicing exports, used to disguise large capital outflows. The administration confirmed the existence of the memo, but declined to comment further.

For the first time since it began internationalising its currency a few years ago, the central bank has also been intervening heavily in the offshore renminbi market to narrow the gap between the onshore (CNY) and offshore (CNH) exchange rates.

Analysts and people familiar with the matter say Beijing has spent up to $200bn defending the currency, but the net impact on the reserves is disguised by fluctuating valuations of reserve assets and other inflows into the reserves.

“They have gone from a credible peg that cost them almost nothing to a weak peg that nobody believes and that is costing them more than $10bn a day to defend. They’re paying huge sums for something they had for free just a few weeks ago,” said one person with close ties to China’s central bank.

In another move to lighten its burden of defending the currency, the central bank informed banks last week that it would soon impose a new 20 per cent reserve requirement on all currency forward positions, in a move aimed at reducing heavy speculation on continued renminbi devaluation.

All market participants will be required to deposit the equivalent of 20 per cent of their forwards book with the central bank for one year at zero interest.

This will considerably increase the cost of currency hedging for Chinese companies, which had a total of $1.2tn in outstanding foreign currency debt by the end of March and are widely expecting further devaluation in the renminbi.

Quite the Reversal

It was not that long ago that hedge funds had massive bets the value of the Yaun would rise. China even took steps to stop “hot money” from flowing into the country.

Hot money, and then some is now going the other way.

By the way, please recall all the inflationists telling China to stockpile copper, lead, and other commodities instead of holding US treasuries, frequently labeled “worthless certificates of confiscation”.

In retrospect, pro-cyclical stockpiling of commodities now looks foolish to nearly everyone. I took the other side of the argument at the time, as did Michael Pettis.

The following was published for our subscribers September 3, 2015.

Perspective

Will the “August Horribilis” turn into an Annus Horribilis?

In which case, the Annus Mirabilis would be over.

The above observation that stocks are down to better valuations is typical of the initial collapse in speculation. Usually made by those who are surprised by the move.

Perhaps the most important part of the setback is that it is global. This should condemn the notion of a national economy forever. Of course interventionist economics was founded on this specious concept. Then there are the widely-publicized efforts by Chinese authorities to prevent the natural collapse of speculation.

The transition from the Great Complacency has been a severe shock to the financial and economic establishment. Is it enough to have cleared the problems consequent to excessive speculation?

Stock Markets

On “Black Monday” (August 24), the plunge in the S&P drove the Daily RSI down to the lowest reading since late August 2011. The eventual low was set in that October. That was a seasonal correction in the cyclical bull market.

Quite likely, the June blow-out in Shanghai completed a fabulous bubble. In which case a cyclical global credit contraction would follow. So far the ups and downs in the SSEC are following the pattern that followed the blow-outs of gold in 1980 or the Nikkei in 1989, for example.

The 45 percent drop in the SSEC in 2 1/2 months compares to the 48 percent drop in the NY market in two months in the fall of 1929.

It is uncertain how tightly the ups and downs will follow the pattern but all of the excesses built up in any bubble eventually get fully washed out. These have happened in unplanned economies in 1825 and in 1873, mixed economies in 1929 as well as in unconstrained mercantilism in 2007. It seems that classic crashes can occur in Communist financial bubbles as well.

No ideology is proof against booms and busts.

Last week, we thought that with the oversold, just the Jackson Hole event itself would prompt a relief rally. Whatever was said would have little actual influence on financial history. Relief could run for a week or so. This could be the appropriate setup for seasonal pressures later in the year.

Of technical interest, the two rebound rallies on the S&P were curbed by the Keltner Channel which is declining. The low was 1867, the first high was 1993 and the low was 1903. At 1975 now it could roll over. Clearly, taking out 1903 would be a strong alert to more pressures.

Sector Review:

Canada’s largest bank (RY) reached its best with the “rotation” in commodities in May. The high was C$80 and the low on the bad day was 68. Now at 72.

The high for US Banks (BKX) was 80.87 in July and the low was 67.80. It is now at 70. For Broker Dealers (XBD) the high was 203 in July and the low was 162. It is now at 173.

IBB plunged from 400 to 284 and is back to 349.

The numbers for TSLA are 286, 195 and 252. For DIS, they are 120, 90 and 102.

Base metal miners (SPTMN) fell from 832 in May to 393 and its back to 449.

Altogether this amounts to serious damage to global equity markets.

This week’s list of headlines includes one about better valuations now available in China. In the fateful summer of 1873 a New York newspaper editorialized that nothing could go wrong. The US did not have a mere central bank. It had the highly-regarded Treasury System which could issue any amount of liquidity by buying bonds. In October the same paper observed that stocks were now more attractively priced.

That contraction started with the crash in 1873 and lasted until the recession low of 1895. In 1884 senior economists in England began calling it the Great Depression.

Link to September 4, 2015 Bob Hoye interview on TalkDigitalNetwork.com:http://talkdigitalnetwork.com/2015/09/central-bankers-powerless-to-stop-market-decline/

Listen to the Bob Hoye Podcast every Friday afternoon at TalkDigitalNetwork.com

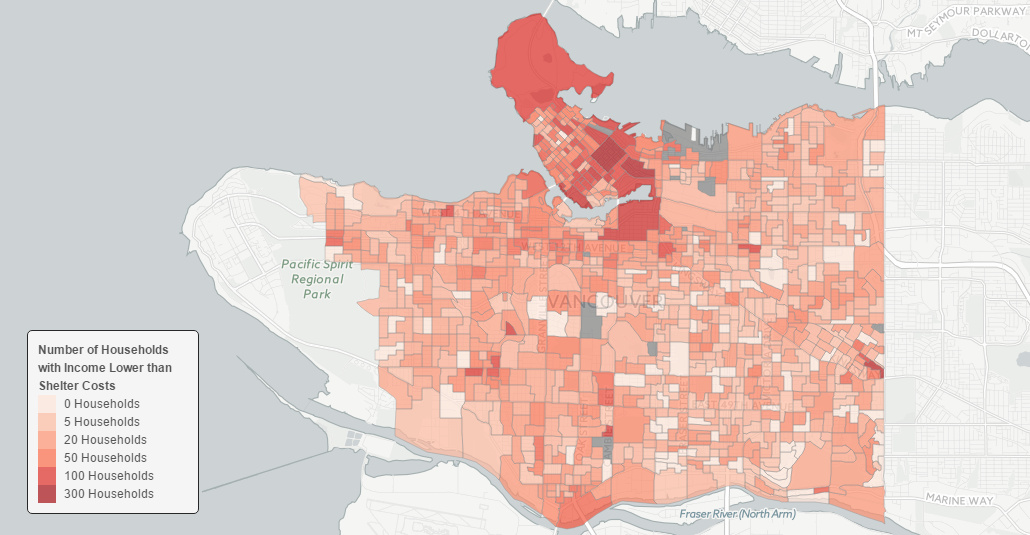

At the epicenter of Canada’s housing bubble, which is now rated as the most overvalued in the world, is the west coast city of Vancouver. It’s there that low interest rates and foreign buying have fueled the average detached home price to a record of C$1.47 million, a 20% increase from the previous year.

While there are many measures of unaffordability, the government and federal agencies use one such measure frequently called the Shelter-cost to Income Ratio. It essentially compares the annual cost of an individual’s housing with the amount of income they have coming in each year. Federal agencies in Canada consider households that spend 30% or more of total before-tax household income on shelter expenses to have a “housing affordability” problem.

In Vancouver, however, the city has become so unaffordable that 25,000 households pay more for their shelter costs than their entire declared income. This works out to 9.5% of the households in the city – far higher than Greater Toronto (5.9%) or Montreal (5%).

We recently stumbled across a data mapping project by Jens von Bergmann, via the Hongcouver blog. Von Bergmann, who runs a data firm in Vancouver, has compiled a series of interactive maps that overlay census data onto the city. In Canada, the mandatory census happens every five years and creates a wealth of granular information.

Here’s the percent of people in each city block that pay more for housing than they take home in income:

A key strength of good investors is being able to handle disappointment and failure. In fact, no matter how intelligent, experienced and skilled you are at investing, mistakes are a cast-iron certainty. That’s because even the best investors cannot consistently and accurately anticipate all challenges that a company will eventually face and, while the risk/reward ratio may have huge appeal at the time of purchase, things always change in the business world.

A key strength of good investors is being able to handle disappointment and failure. In fact, no matter how intelligent, experienced and skilled you are at investing, mistakes are a cast-iron certainty. That’s because even the best investors cannot consistently and accurately anticipate all challenges that a company will eventually face and, while the risk/reward ratio may have huge appeal at the time of purchase, things always change in the business world.

The problem, though, is deciding exactly what to do with the shares that turn out to be disappointing. Clearly, they can fall into any number of categories, with examples being stocks that have plummeted to be worth a small percentage of their original value all the way through to companies that may be in positive return territory, but which have lagged their industry group or the wider index.

On the heels a big surge in Asian markets, today a piece from one of the greats in the business discussing the attempt by the global markets to stabilize with the Dow Theory “sell signal” already triggered. Also included is a quick note from Art Cashin.

On the heels a big surge in Asian markets, today a piece from one of the greats in the business discussing the attempt by the global markets to stabilize with the Dow Theory “sell signal” already triggered. Also included is a quick note from Art Cashin.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair