Bonds & Interest Rates

Today is an emotional day for Americans. In an instant, on a beautiful blue sky morning 14 years ago, all of our lives changed forever.

Today is an emotional day for Americans. In an instant, on a beautiful blue sky morning 14 years ago, all of our lives changed forever.

September 11 is a day when we pause and reflect on where we were when—when the towers came crumbling down, when our nation’s capital came under attack, when so many lives were cut short, when so many heroes rushed in.

I was in Manhattan with colleagues that day, attending a financial industry conference uptown. At the time, we didn’t know how fortunate we were that our meeting had been changed from 9:00 a.m. to 11:00 a.m. I was en route when everything stopped, and soon after, I saw all the people covered in dust and walking home across the bridge. The cell phones in the city stopped working, but because mine had a San Antonio area code, I was able to get through to the office to let everyone know we were safe.

….continue reading this very comprehensive SWOT analysis of all markets from Stocks, The Economy and Bond Market, Gold, Energy, China, Europe, Leaders, Laggards. Its long and detailed weekend reading – Money Talks Editor

Over the last several week’s I have continued to suggest that the markets could rally back to resistance. During the time the markets have vacillated wildly between sharp declines and monster rallies.

CNBC headlines have been almost laughable as one day’s banner of “biggest rally since 2011” is followed by“biggest decline since 2007.” For the average investor, it has been nothing but nerve wracking.

I have stated many times in previous missives that it had been such a long period without a 10% correction in the market, when it occurred it would feel substantially worse. Well, it has and it did.

But what now?

As I have often written markets do not rise or fall in a straight line. During bull markets there are declines to previous support levels and during bear markets there are rallies to resistance.

Notice that at the peaks of previous bull markets, the initial correction looked much like all previous corrections during the bullish advance. The problem is that many failed to recognize the something had technically changed for the worse.

Currently, it is being argued that this correction is just a blip in an ongoing bull market. However, there are plenty of markings that suggest that the current correction could be “something different.”

A Rally To Sell Into

As shown in the two charts below, sentiment and volatility have reached levels that are normally consistent with short-term bottoms in markets. Sellers, at many levels, have been exhausted which makes any level of buying more exaggerated than normal.

While the volatility index (VIX) is still suppressed relative to historical corrections, it is at the highest level since 2012. When combined with the most bearish sentiment reading we have seen since the summer of 2011, and a currently oversold market condition, the ingredients needed to fuel a short-term (2-4 week) rally are present.

The chart below shows this oversold condition, and is the same “potential reflex rally” chart I have posted for the last three weeks. The dashed blue line that I drew immediately following the initial slide has been marking the exact “reflex rally” I predicted at that time.

However, given the short-term oversold, bearish and fearful condition, it is extremely likely that the markets could advance to the downtrend resistance around 2040 currently. (As time passes these levels will change slightly so DO NOT focus on exact numbers for decision making – these are neighborhoods.)

ANY RALLY TO THOSE LEVELS should be used to rebalance portfolios, raise cash and reduce equity risk. I know it is monotonous, but I cannot stress enough the importance of paying attention to your portfolio at the current time.

Portfolio Management Instructions

Repeating instructions from last week for any continuation of the rally next week:

1) Sell “laggards” and “losers” in FULL. These are positions that have performed very poorly relative to the markets. Positions that are out of favor on the run-up, generally tend to fall faster in declines. (Energy, Industrials, Materials, International, Emerging Markets, etc.)

2) Trim positions that are big winners in your portfolio back to their original portfolio weightings. (ie. Take profits) (Discretionary, Healthcare, Technology, etc.)

3) Positions that performed with the market should also be reduced back to original portfolio weights.

4) Move trailing stop losses up to new levels.

5) Review your portfolio allocation relative to your risk tolerance. If you are aggressively weighted in equities at this point of the market cycle, you may want to try and recall how you felt during 2008. Raise cash levels and increase fixed income accordingly to reduce relative market exposure.

How you personally manage your investments is up to you. I am only suggesting a few guidelines to rebalance portfolio risk accordingly. Therefore, use this information at your own discretion.

Have a great weekend

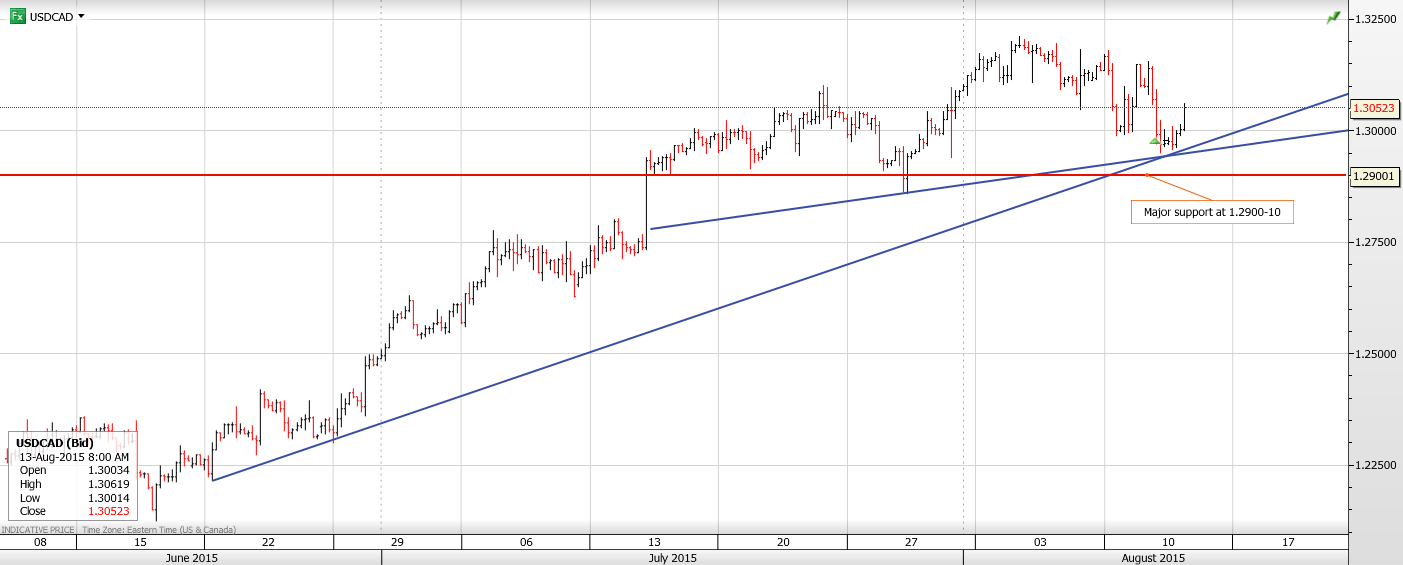

USDCAD Range 1.3219-1.3272

This morning US PPI data failed to have an impact in currency trading. G-10 currencies are content to meander within the confines of yesterday’s ranges while traders kept an eye on equities. US equities are drifting lower, in line with a similar move in Asia and Europe.

FX markets are ending an interesting week on a dull note. Singapore was closed for elections which sucked a ton of liquidity out of markets while a lack of top tier data and quiet politicians did the rest. A fresh report from Goldman Sachs painted a fairly bleak outlook for oil prices which contributed to a small dip in WTI.

USDCAD was sidelined in Asia and a rally in Europe was short-lived. The Canadian dollar outlook remains married to WTI prices and the prevailing sentiment for the US dollar. Wednesday’s Bank of Canada statement was fairly positive except for the references to China risks and comments about how a weak currency has helped the economy. Perhaps the thinking is if USDCAD at 1.3300 is boosting economic growth, then at 1.4500 rate it would turbo-charge the economy.

Technical Outlook

USDCAD continues to chop around within a 1.3160-1.3320 range but unable to generate enough momentum to extend gains or losses. The underlying sentiment is bullish for a test of 1.3450. For today, USD support is at 1.3210 and 1.3160. Resistance is at 1.3270 and 1.3320

Today’s Range 1.3210-1.3290

Chart: USDCAD 4 hour with uptrend Larger Chart

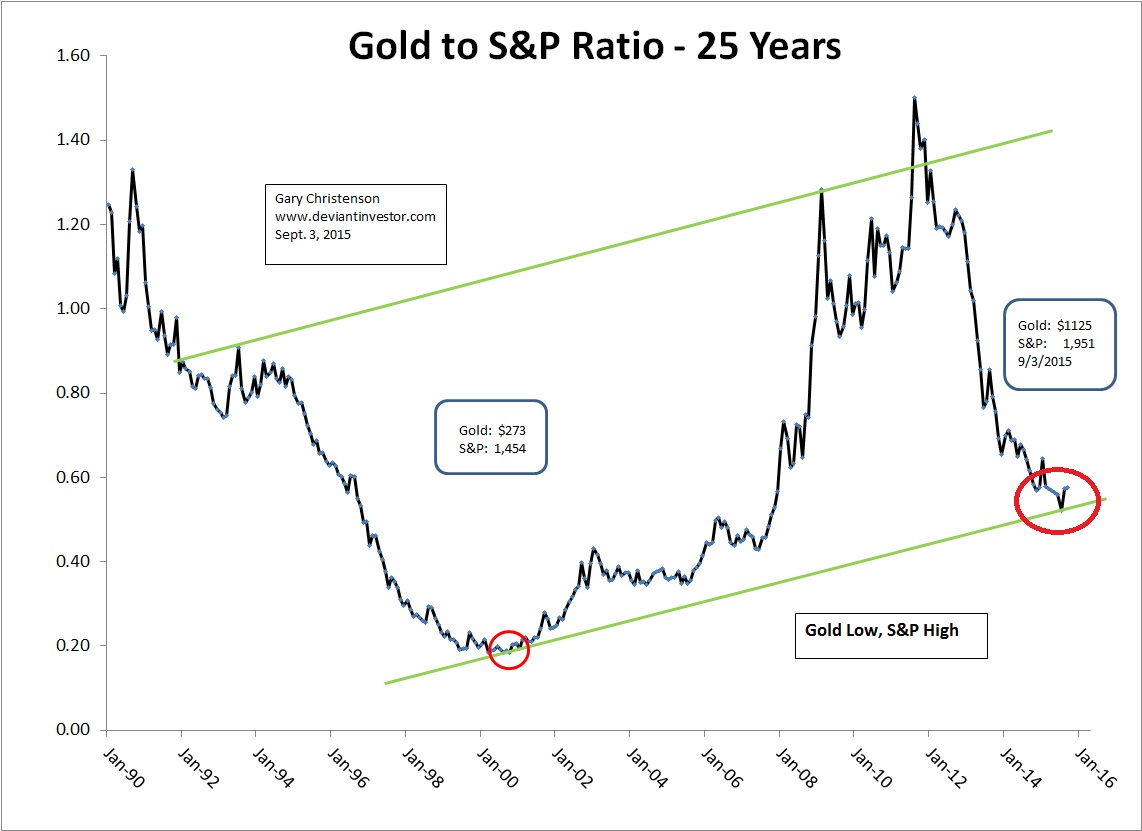

1. Buy Gold, Sell the S&P

by Gary Christenson – The Deviant Investor

Buy low, sell high! As of today, September 3, 2015, the better choices are buying gold and selling the S&P 500 Index and relevant stocks.

Why?

Examine the graph of the ratio of Gold to S&P 500 Index for the past 25 years. The ratio is low now and likely will correct higher. I think gold will move higher and the S&P will move lower.

2. This only happens about once in a decade…

by Simon Black – Sovereign Man

“a once in a decade opportunity” that has to do with a deep flaw in our ability to properly assess risk.

3. World Waits With Bated Breath as Fed Gathering Looms

by Mike Larsen – Money and Markets

I’ve seen a lot of Federal Reserve meetings come and go in the 18 years I’ve been closely following the interest-rate markets. But few have been as momentous as the one that will begin next week on Sept. 16.

I’ve seen a lot of Federal Reserve meetings come and go in the 18 years I’ve been closely following the interest-rate markets. But few have been as momentous as the one that will begin next week on Sept. 16.

That’s because Fed policymakers will have to decide whether to raise short-term interest rates for the first time since June 29, 2006 – with all the potential, resulting market turmoil it may unleash. Judging by what has already happened ahead of that two-day meeting, there could be tons of it.

Think about it: The Fed has spent nine years and three months in easing mode. It has slashed rates to the bone, printed trillions of dollars out of thin air, and forced investors (kicking and screaming) into the most esoteric, highest-risk, overvalued securities in an attempt to kick-start economic growth.

Even the elimination of QE here didn’t technically end the easing process – the Fed has continued to invest the proceeds of maturing bonds into new bonds. And the Bank of Japan, European Central Bank and other foreign institutions were more than happy to pick up the slack.

But now, we’re closer to a hike than we’ve been at any time since a year before the first iPhone hit the market … The Departed wowed gangster film enthusiasts … and (ironically enough) free-market economist Milton Friedman died.

Several Fed officials have already come out and strongly suggested they want to raise interest rates, but are worried about recent events in China and the potential impact of a rate rise on the value of the dollar. That includes Vice Chairman Stanley Fischer.

Other policymakers have basically said they wouldpush for a rate hike no matter what. That includes Richmond Fed President Jeffrey Lacker and St. Louis Fed President James Bullard.

The rest of the world has had a lot to say, too. The Financial Times carried dueling articles on Wednesday from former Treasury Secretary Larry Summers and former Dallas Fed President Richard Fisher. Summers asked the Fed to hold off, while Fisher urged the Fed to just get it over with already.

The chief economist of the World Bank also just warned the Fed that raising rates could cause “panic and turmoil.” That echoed cautionary remarks a few days earlier from the head of the International Monetary Fund (IMF).

In short, everyone and his sister has an opinion on what the Fed should and will do – not just here in the U.S. but around the world. That means there’s no consensus in the markets, and that one side or the other will almost certainly be disappointed. As a result, we could see huge amounts of volatility and wild market moves when the decision is released.

In short, everyone and his sister has an opinion on what the Fed should and will do – not just here in the U.S. but around the world. That means there’s no consensus in the markets, and that one side or the other will almost certainly be disappointed. As a result, we could see huge amounts of volatility and wild market moves when the decision is released.

Personally, I believe the Fed should have started raising interest rates a few quarters ago. Economic and market conditions clearly warranted it. They chickened out at the time, and now I believe there’s a 60%-70% chance they end up hiking right into the teeth of a significant global crisis and a possible U.S. economic slowdown.

Speaking of which, we’re already seeing a ton of the “Bloody Wednesday” market events I forecast months ago … just as a result of the Fed talking about possibly hiking rates. That shows how risky and unstable today’s economic and market backdrop is.

It’s also why I continue to recommend you take prudent steps to protect your capital – regardless of whether the Fed does or doesn’t hike next week. We’re in a new market paradigm, one where investors can no longer count on the willingness OR ability of central bankers to save them every time they get in trouble. And that means you have to change your way of thinking and investing if you want to prosper.

Until next time,

Mike Larson

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair