Asset protection

”Come to the edge,” He said. They said, ”We are afraid.” ”Come to the edge,” He said. They came. He pushed them… and they flew.

”Come to the edge,” He said. They said, ”We are afraid.” ”Come to the edge,” He said. They came. He pushed them… and they flew.

Guillaume Apollinaire

The answer to this plain question should always be a resounding no: it never pays to give into panic. The smartest option is to derail this emotion before it gains any traction. Once fear takes over, the end is nigh.

When the markets were disintegrating approximately two weeks ago and if you were one of the lucky few that opted against joining the bandwagon of panic, you should have had a feeling of déjà vu; sort of like the movie ground hogs day. The same-old twaddle that was broadcasted before was once again intoxicating the masses; like cockroaches, these naysayers emerge from the woodwork and hum the same-old hymn “the world is going to end” and or financial disaster is around the corner. In each instance, you will find that the same rubbish is spun in a different way; this is recycling at its best. What they so conveniently omit is how each and every single one of these so-called end of the world events proved to be nothing but a mouth-watering opportunity for the astute investor. Now we are not stating that caution should be thrown against the wind. What we are simply stating is that if you become one with the fear, then this useless emotion will take over and blind you from seeing any opportunity, even if it slaps you hard on the face. Never become one with fear; understand that when it comes to trading fear is on par with toilet paper.

Let’s take a sombre look at what is actually going on, and why these events are unfolding.

It’s more than obvious that the market was in a corrective phase or crashing if one joins the naysayer’s camp; the more appropriate term would be letting out steam that was long overdue. The last week of August, was the worst week for equity markets since 2011. One could also point out that the markets have not experienced a significant pullback since 2011.

So what changed over the span of 1-2 weeks to warrant such negativity? Very little actually.

- China devalued its currency to boost exports; it had to; we are in the midst of a currency war, and most nations other than the U.S. are allowing their currencies to literally collapse. However, devaluing the currency affects sales and profits at many multinational companies, including those back in the U.S. So expect the U.S. to do something that has a negative impact on the dollar.

- The next issue is that the world’s second-largest economy is no longer growing as fast. Growth is slowing down and so far it appears the government’s response to address this has been ineffective. In the short term, this will continue to be the case, but over the long term, we think their policies will be conducive for the economy and stock market.

- Manufacturing activity is slowing down in China, and this has a big impact on the commodity markets. This is the primary reason many markets in this sector are experiencing severe corrections. Copper, oil, and iron to name a few have just fallen apart.

- The extreme plunge in energy prices while a relief for consumers, has unnerved investors. Though to be fair, a lot of this had to do with excess supplies. Demand is not keeping up with supplies, which is a clear indication that worldwide demand for oil is softening.

- Up until recently, the Fed’s decision to start raising rates was another factor weighing on the markets. That uncertainty is no longer an issue as the Fed has now signalled that it will not be raising rates. There is really no inflation problem to tackle. We are referring to the manufactured numbers that suggest all is well when the opposite holds true. This is what the masses believe and so this is what counts, as what they believe drives the markets. Energy prices are down significantly, and the raw materials sector is basically in a bear market. Wages are not rising; at best, they are stagnant. Over 50% of the components of the CPI (consumer price index) have declined in the past six months. TIPS are also signalling that for the foreseeable future, inflation is not going to be an issue. Under these circumstances, a rate hike would make no sense, and only further destabilize the markets. Let’s not forget the additional turmoil; a rate hike would cause in the currency markets. A rate hike would further strengthen the dollar, and adversely affect U.S. exports, making them less competitive in the global markets.

- Again, we do not necessarily agree with the low inflation scenario as rents are rising and the cost of many goods over the past several years have risen dramatically. What we believe in is not of importance, for, in the end, it’s the crowd that drives the market, up to a certain point. When emotions hit a boiling point, which they have not, then one can start taking a position that is opposite to that of the masses.

So what’s on the horizon?

Any expert who claims to know precisely what will occur should be ignored. Even a broken clock is correct twice a day. Hence, if an expert makes a large enough number for pronouncements, one of them is bound to come to pass. It does not mean that individuals cannot determine the direction of the markets. As we have stated many times before, there is a vast chasm that separates spotting market bottoming and topping action, with trying to identify the exact top or bottom.

Investor confidence has taken a beating. Under these conditions, many investors will either sit on the sidelines or take some money out of the markets. This is good for it will drive stocks to even more attractive levels. The masses are well-known for their ability to buy and sell at precisely the wrong time.

Some bullish or reassuring factors to consider:

- Traders are not overtly bullish.

- Stocks are selling for roughly 17 times their trailing earnings. While not cheap, these valuations are by no means excessive. The long-term average is roughly 16.5 times earnings.

- Unemployment is down, and U.S. Manufacturing levels are rising.

- Corporations are flush with money.

- Banks are in much better shape than they were in during the financial crisis a few years ago.

- Insiders are not dumping shares; they are actually stepping in and buying them.

The technical outlook

Our proprietary strength indicator has turned negative on the markets and this indicates that the lows will be tested again. The trend based on our Trend indicator has also turned neutral and V readings (our proprietary tool that measures market volatility) has soared to an all-time new high. Hence, we expect extreme moves to be the norm for the next few months. It would not surprise us if the Dow experiences a 1500-2000 point move over the span of one week.

The Dow is having a remarkably hard time of trading above 17000, former support turned into resistance. After the selloff in August, a lot of technical indicators moved into the extremely oversold ranges. Thus, the corresponding rally should have been much stronger. Additionally our own indicators are not validating the current move up, which strongly hints that the lows will have to be tested again. If the Dow closes below 15500 on a weekly basis, then we expect the Dow to make a quick move down to the 14500-14700 ranges; if this were to occur, we could term it a screaming buy event.

Conclusion

Some additional factors to keep in mind:

- The housing sector is relatively strong. Purchase applications are up 18% year over year.

- U.S. employees added 215,000 jobs in July

- Latest data shows that U.S. Economy grew at 3.7% in the 2nd quarter, up from the initial estimate of 2.3%

It is interesting to note that the naysayers like clockwork start their chanting and howling specifically after the markets have started to correct; their screams are rather muted when the market is trending upwards. If you look at history, their record is rather dismal, as every so-called disaster and or end of the world scenario, these naysayers pandered about turned to be exactly the opposite of what they predicted. Instead, each of these so-called disaster scenarios proved to be nothing but splendid buying opportunities in disguise. Disasters will come and go. Depending on the lens you use to view such a situation, it can either represent a splendid opportunity or a monumental tragedy. History is replete with examples quite clearly illustrating that financial disasters usually make for splendid opportunities.

We are not advocating that you run out and lunge into the markets; we have been stating for quite some time that the markets needed to let out some steam. Note, that the markets have not experienced significant correction since 2011. It would be folly to assume that the markets will trend in one direction without letting out a burst of steam. The markets have already shed roughly 15% from high to low. Given the heights they have run to since 2011, a 20% move would still be acceptable and nothing to fear. At this point, prudence is warranted, but a massive sell-off should be viewed as a buying opportunity, in contrast to a colossal tragedy. Our general suggestion would be to buy when panic sets in, and blood is flowing freely in the streets. Be wary when the masses are joyous and delighted when they are not.

I envy paranoids; they actually feel people are paying attention to them.

Susan Sontag

A crucial Shimitah cycle is presently occurring! It is a cycle that was first observed by the Jewish people while living in the Holy Land. Every cycle culminates in a Sabbatical year, (7th year) known as Shemitah; literally translated means “to release.” This Shemitah 7 year cycle is occurring at the same time that the American economy appears to be “on life support”.

After so much excitement within the last couple of weeks, the markets have been somewhat anticlimactic. Which way will we go? Bullish or bearish? I believe, we are totally CONFIRMED bearish, and expecting a re-test of previous lows. We may even see, within the Dow Jones Industrial Average, a lower low, down around 15,000. Lately, the volatility has stabilized and THE MARKETS HAVE BEEN CONSOLIDATING. The base is about 1,000 points so that when the breakout does occur, I expect a move of about that same size. When I decipher my charts, it looks as though this breakout should happen within the month of September, and/or early October 2015. If it breaks bearish, the news media will likely blame it on the FOMC meeting, and if it breaks bullish, they will, most likely, blame it on the Federal Reserve.

This nation has never experienced six years of hyper-low interest rates before! What impact has this had on the restructuring of the balance sheets of insurers and banks? In striving to match assets and liabilities, across 24 consecutive quarters of near-zero rates, what deception might financial institutions have inflicted (reaching-for-yield through derivative positions) that could backfire, and trigger a financial crisis!

It will result in a strong price movement. If the market thinks honestly, the investment community seems much closer to panic and hysteria than it does to euphoria and optimism. It would not take much more to depress the markets further; however, it would take a lot to make it feel confident and secure about the Fed’s ability to stay ahead of “the curve” and manage the transition smoothly.

The SPX is very similar, in structure, in relation to the Dow. It appears as if it was ready to complete its triangle formation, but the pattern has continued to expand into a symmetrical triangle. A triangle normally forecasts a continuation of the trend, which existed prior to its formation; more weakness ahead continues to be the logical forecast. This is also supported by important cycles which should not make their lows until late this September and/or early October 2015.

Since the SPX reached 1,865, it has worked its’ way into a consolidation pattern, which has the appearance of a triangle. If it is a symmetrical triangle, the odds are in favor of a continuation of the selling, after the pattern is completed. This could happen as early as this coming Thursday, September 17th, 2015, when the Fed will announce its decision on interest rates, but since the indexes could also stage a surprise move, in the opposite direction, it is best to wait until we are past that critical period and before hazarding a short-term forecast.

The NASDAQ has a slightly different formation. This one looks like an ascending triangle. Statistically, there is not much difference between ascending and descending triangles. Outside of this triangle formation, the NASDAQ looks like the others do, for the most part. The 100 and 200 simple moving averages have not yet crossed bearish; however, they are headed sideways. I am foreseeing the area around 4,850, as resistance. Otherwise, I see much of the same signals as the other two indexes.

Global Stock markets had modestly rallied last week, following their most serious dramatic plunge since 2011; which lasted from July 20th, 2015 into August 26th, 2015 (declines of over 15%) which occurred in that brief five week period within most of the world’s indexes. Some were much worse. The German DAX, for instance, fell nearly 21% within that time frame, and down nearly 25% from its yearly high, in April 2015. The Chinese Shanghai Index plunge was even more disturbing. Prices dropped nearly 45% from their yearly high of June 15th, 2015. Thus, a rally from that first leg down was well overdue, which has now lasted nearly three weeks.

However, the markets’ form has been unimpressive, and more indicative of a corrective retracement within a bear market, rather than the start of a new bull campaign. This week’s highly anticipated Fed announcement of a rate hike, which is due out on Thursday, September 17th, 2015, nearly guarantees that the bullish or bearish argument in equities, around the world, will be revealed. One course would set the indexes on a bullish trajectory and the other on a bearish one. The rallies off of the lows of August 24th through the 26th of 2015, seem to be losing momentum. Not that they ever had very much to begin with. There have been sharp up days, but, in almost all instances (like last week) they were quickly followed by sharp down days. We are all currently waiting for Dr. Yellen’s announcement. This should be a rather shocking announcement to hear, globally! If one thinks that some world leaders have been judgmental in their policies and behaviors, then you have not seen anything yet, unlike what you are about to witness now, well into 2016, and even into 2017.

While the stock market appears to be on hold during this week’s Fed meetings, gold and silver were also unimpressive. Gold fell below $1100.00/oz., again, during Friday’s session, September 11th, 2015. GLD should retrace itself down to 100 before any BULLISH/BUY confirmation will be given. Silver tried to rally above $15.00/oz., but could not do so after Wednesday, September 9th, 2015, and began a retreat down to $14.25/oz. during Friday’s trade.

Bearish trends of this week are extremely potent. They coincide with the Fed meeting this Thursday, September 17th, 2015, which is expected to result in dramatic market moves. These spurts may still be short-lived, but the amplitude, in any direction, is likely to be both sharper and greater than it is, in any given day. Possibly, two or three days.

The Bank of China devalued the Yuan and depegged it from the US Dollar, most likely, because the leaders of China did not want the Fed to raise US interest rates. Higher US interest rates mean a higher US Dollar value. We are still in a global race to the bottom in currency values, as well as we are in the currency wars zero interest rates policy era of the continued quantitative easing. A rising currency is seen as hurting a nation’s balance of trade. Hence, the unexpected surprise move made by China, has temporarily worked, on a short-term basis. It had paralyzed the Fed’s expected action to raise interest rates. The Federal Reserve has delayed the expected rate hike, until now. If they do not raise their bench mark interest rates, the US risks the possibility of negative interest rates.

I foresee the “hidden signs” that the Federal Reserve will slightly raise its bench market interest rate, which will result in the selling of stocks, following their announcement.

Trade with me and profit from this cycle: www.TheGoldAndOilGuy.com

Chris Vermeulen

The Wall Street Journal on Friday noted that the market for technology initial public offerings has struggled this year, as it did last year. Is that meaningful?

The Wall Street Journal on Friday noted that the market for technology initial public offerings has struggled this year, as it did last year. Is that meaningful?

In April, analyst Jason Goepfert started looking at the percentage of IPOs that were losing money, which has exceeded all-time highs. That kind of risk tolerance was troubling, Goepfert noted, so it has only been a matter of time before investors would have enough of profitless new companies.

IPO volume overall has thinned out, with August being one of the slowest months in three years according to Bloomberg data. And of those, tech offerings are the scarcest of all. Only 5% of new offerings have been in the technology sector.

That’s the lowest in 10 years, according to Goepfert’s data. This only includes pricings through August every year, so the analyst is not comparing partial data this year to full-year data in prior years. Not only is this year the slowest tech year in a decade, it is the third-lowest in 35 years. Only 2003 and 2005 were slower while the peak came in 2000, says Goepfert.

The big question is whether the current low number of tech offerings is a good sign or a bad one. Based on historical market behavior following other extremes in IPO data, Goepfert argues it has served better as a contrary indicator than as a bad omen.

The reason: A high appetite for IPOs — whether profitable or not — has usually suggested too much risk tolerance and lower future returns while a low one has suggested extreme risk aversion and better future returns, the analyst observes. Consider this a modest positive, from a contrarian point of view, for stocks going forward.

* * *

Will They or Won’t They?

Deutsche Bank economist Joseph LaVorgna told clients he sees seven reasons why the Federal Reserve won’t spook markets by raising rates on Thursday.

— Global stock markets are fragile.

— The dollar has been strong, weighing on GDP growth via trade.

— Financial markets continue to assign a low probability of a September rate hike based on futures trading (odds stand at 30% vs. 54% last month).

— Several key Fed officials seem to be subtly backing away from a September move with words like “less compelling” and “complicating factors” and “significant…headwinds.”

— There are meetings in October and December the Fed can hike at.

— The Fed doesn’t fear a loss of credibility if it waits.

— Inflation continues to be soft, with the Fed’s preferred measure up just 1.2% over the past 12 months.

With this in mind, the recent range-bound choppiness in stocks should continue until next week — when a dovish Fed could unleash a powerful rebound. Commodities, especially crude oil and gold, could be the big beneficiaries of a “no hike” decision, though the enthusiasm could be short-lived as it runs smack into the reality of lowered growth expectations for companies in the fourth quarter and next year.

While they put the odds of a September hike at 50-50, citing the cumulative improvement in the economy over the last few years that makes maintaining emergency 0% interest rate hard to justify, the team at Capital Economics believes that higher core inflation driven by rising wages will force Yellen to hike rates much more aggressively next year … something that markets have definitely not priced in yet.

* *

Fed Days in September

And now one last note from an analyst who keeps track of major repeating news and weather events, and the market’s reaction to them over time.

He reports that there have been 11 instances since 1976 when the Federal Reserve has met in September at a time when the Nasdaq is up in the past week.

The market has fallen over the next one, two and nine days in eight of those instances, he says, logging average losses of 0.7% the next day, 1.4% over the next two days, and -1.54% over the next nine days.

History is not destiny, but it’s good to know how investors have reacted in the past to similar stimuli. Combine that with the traditional view that the market often peaks for the autumn in the third week of September and it’s fair to consider exercising caution. On the other hand, if the market breezes through this period without a scratch, essentially whistling past the graveyard, you can consider it a big positive for the rest of the year.

Best wishes,

Jon Markman

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

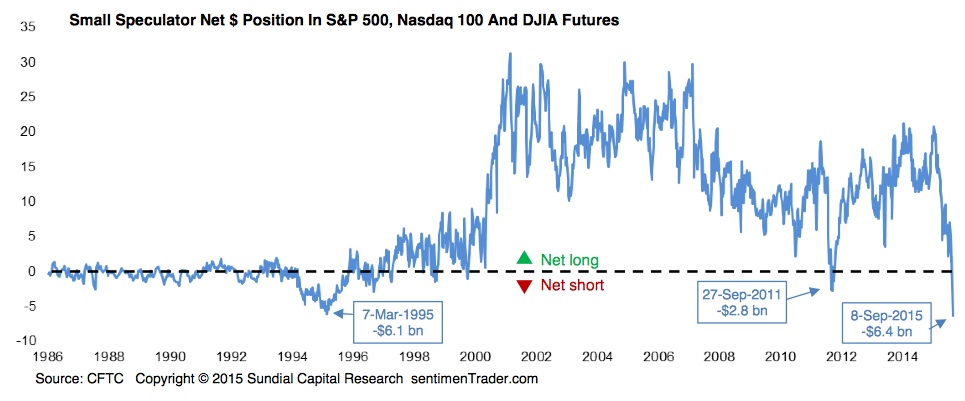

With stocks a bit weaker and crude oil trading lower, today King World News is featuring a stunning piece that reveals small speculators are now gambling on a stock market decline by taking an all-time record short position in stocks. This piece also includes two key illustrations that all KWN readers around the world must see.

With stocks a bit weaker and crude oil trading lower, today King World News is featuring a stunning piece that reveals small speculators are now gambling on a stock market decline by taking an all-time record short position in stocks. This piece also includes two key illustrations that all KWN readers around the world must see.

Jason Goepfert of SentimenTrader warned: “Small speculators in index futures went to $6 billion short this week. New all-time extreme – see charts HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair