Op/Ed

Each week Josef Schachter gives you his insights into global events, price forecasts and the fundamentals of the energy sector. Josef offers a twice monthly Black Gold newsletter covering the general energy market and 30 energy, energy service and pipeline & infrastructure companies with regular updates. We also hold quarterly webinars and provide Action BUY and SELL Alerts for paid subscribers. Learn more.

EIA Weekly Oil Data: The EIA data of Wednesday December 15th was initially seen as positive for crude prices. US Commercial Crude Stocks fell 4.6Mb (forecast a decline of 2.1Mb). A key component was a rise in Exports of 1.375Mb/d or 9.63Mb on the week. If not for this large export increase there would have been a build of over 5Mb. As a result of these events crude has now fallen below US$70/b. Refinery Utilization was unchanged at 89.8% from the prior week. Total Motor Gasoline Inventories fell 0.7Mb while Distillate volumes fell 2.9Mb. US Crude Production was unchanged at 11.7Mb/d. Total Demand rose by 3.35Mb/d as Distillate heating oil demand rose by 1.32Mb/d due to the cold weather. Gasoline consumption rose by 509Kb/d to 9.47Mb/d which is just above the 9.41Mb/d consumed in 2019 at this time. Jet Fuel Consumption rose 387Kb/d to 1.61Mb/d versus 2.06Mb/d consumed in 2019. Cushing Inventories rose 1.3Mb to 32.2Mb/d.

OPEC December Monthly: On December 13th OPEC released their December Monthly Forecast Report (November data). As we have seen in the past few months they have not added the 400Kb/d in their stated monthly production increase. In October, they only added 213Kb/d and in November only 285Kb/d. Some countries like Angola continue to have underinvested in their industry and saw declines of 38Kb/d in November.

The biggest increase came from Saudi Arabia at 101Kb/d, followed by Iraq at 91Kb/d and then by Nigeria at 85Kb/d. Surprisingly Kuwait only added 29Kb/d, even though they could have easily added 156Kb/d more, just to get back to 2019 pre-pandemic levels. Sanctioned Iran saw production fall by 9Kb/d to 2.47Mb/d and Venezuela saw a modest rise of 15Kb/d to 625Kb/d (down from 796Kb/d in 2019). OPEC sees 2021 consumption at 96.6Mb/d (Q4/21 at 99.5Mb/d). For 2022 they see world demand at 100.8Mb/d up 4.15Mb/d with Q4/22 at 102.63Mb/d. If there is no recession in the US and/or China they might be right but we see slowing economies in both areas. Our 2022 world demand forecast is for 97-98Mb/d or 3-4Mb/d less than OPEC’s positive economic view. The health of world economic activity is the key divergence between energy bull and near term bears like us.

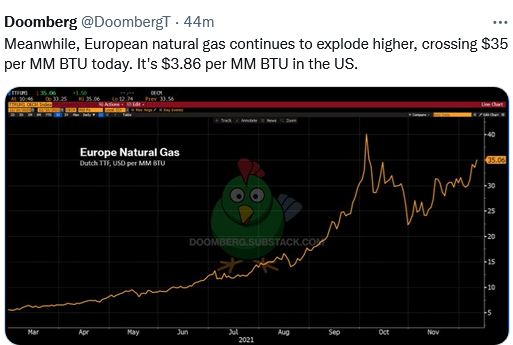

EIA Weekly Natural Gas Data: Weekly withdrawals started three weeks ago as winter demand picked up. Last week, there was a withdrawal of 59 Bcf, lowering storage to 3.505Tcf. The five year average for last week was a withdrawal of 87 Bcf. Storage on a five-year basis was 3.595Tcf so storage is only 2.5% below the five-year average. NYMEX today is US$3.88/mcf down from the high in early October of US$6.47/mcf. AECO spot is at $3.48/mcf, down $3/mcf from 2021 highs. As to be expected, natural gas stocks have retreated from their 2021 highs. With the two key months for natural gas demand ahead of us (January and February) we should still expect large price moves to the upside on very cold days. Spikes over $6/mcf should be seen on both sides of the border when weekly withdrawals over 200 Bcf on a cold week occur. After winter is over natural gas prices will retreat and if the general stock market decline unfolds as we expect, then a great buying window could develop at much lower levels for natural gas stocks in Q2/22.

Baker Hughes Rig Data: The data for the week ending December 10th showed the US rig count rose seven rigs (unchanged the prior week) to 576 rigs last week. Of the total working last week, 471 were drilling for oil and the rest were focused on natural gas activity. This overall US rig count is up 73% from 323 rigs working a year ago. The US oil rig count is up 83% from 258 rigs last year at this time. The natural gas rig count is up a more modest 33% from last year’s 79 rigs, now at 105 rigs. The Permian saw an increase of three rigs last week (five rigs in the prior week) to 286 rigs and was up 70% from 168 rigs last year.The Permian is the hottest basin followed by the Haynesville with 46 rigs working.

Canada had a decline of three rigs (after a rise of nine rigs in the prior week) to 177 rigs. Canadian activity is now up 59% from 111 rigs last year. There were three less oil rigs working last week and the count is now 110 oil rigs working, up from 52 last year. There are 67 rigs working on natural gas projects now, up from 59 last year.

The material increase in rig activity over a year ago in both the US and Canada should continue to translate into rising liquids over the coming months, especially with the DUC count (drilled but uncompleted well count) at very low levels. The data from many companies on their plans for 2022 support this rising production profile expectation. We expect to see US crude oil production reaching 12.0Mb/d during winter 2021-2022. Companies are taking advantage of attractive drilling and completion costs and want to lock up experienced rigs and crews as staffing issues are getting tougher for the sector.

Conclusion:

Bearish pressure on crude prices:

- The US is slowing its bond purchases which will remove 6%+ of monetary stimulus from the economy when completed in March 2022. The FOMC meeting (which ends today) is expected to announce a speed up of the tapering of bond purchases. They may also show their intent to increase interest rates starting in 2022. Some forecasters expect three increases in rates in 2022 and three in 2023, so that the terminal rate rises to 2.3% from 0.25% currently. Note, a 1% rise in interest rates adds US$300B of interest costs and with deficits continuing for many years into the future, this will add to deficits and depress the US economy. Recent economic data in the US is slowing. Retail Sales out Wednesday showed a rise of 0.3% down from 1.8% in the previous month against an expected rise of 0.8%. The PPI rose to a 40 year record high of 9.6% on Tuesday. The PPI for finished goods rose to an all time high of 13.6% exceeding the previous high of 12.9% seen in October 1980, just before the Fed Chairman of that time Paul Volcker jacked up interest rates quickly to stem the rampant inflation and caused a severe recession. The current Fed Chairman is boxed in and may be forced to reverse his accommodating stance. How he shifts and how fast he shifts will determine the vigor of the US economy in 2022.

- China is seeing slower growth as well due to a prolonged property slump and sluggish consumer spending. Retail Sales only rose 3.9% in November (year over year) down from 4.9% (year over year) in October and below the annual inflation rate.

- Covid caseloads are growing around the world with Omicron now exceeding Delta in many countries. This new variant is impacting both the vaccinated and unvaccinated with the unvaxxed filling the ICU wards. Concern is rising that in the next one to two months hospitals will need to triage again. In the US, the death rate is over 800K deaths. Worldwide, the death count is now 5.31M. Single case records are rising in Europe particularly in Denmark, Norway and Switzerland.

- Energy demand is under pressure as high prices for most food, rent, taxes, child care, health expenses, auto costs and other daily necessities make spending decisions tougher for consumers. This gouge in prices will surely impact consumers’ buying behavior in the coming months. The spending pie of consumers is shrinking and some spending habits of the past will have to be dropped. Demand destruction is on the way.

- The International Energy Agency (IEA) in a report released this week sees a surge in Covid-19 cases denting global demand for oil at the same time as they see supply exceeding demand by 1.7Mb/d starting in Q1/22. This view is in stark contrast to OPEC’s and consistent with ours.

Bullish pressure on crude prices:

- While approving an increase of 400,000 b/d of new production for January 2022, OPEC has not achieved their target once again as seen from the December Monthly Report released earlier this week.

- The Iran deal is not seeing progress as the Iranians continue to want removal of sanctions to sell oil but do not want to slow down their nuclear weapons program or allow intrusive UN inspections. The bulls are rejoicing that the 1-2Mb/d of new Iranian oil that could come on is now more unlikely.

- If Russia invades Ukraine, sanctions will be added to pressure Russia to desist. Russia may face OECD blockages of sales of crude oil. This would be positive for China but would hurt Europe which would need to find other more expensive suppliers.

- JP Morgan and other US investment banks see world demand exceeding pre-pandemic levels in Q2/22. Their fearless forecasts see US$80/b in early 2022 and US$100/b in 2H/22.

CONCLUSION:

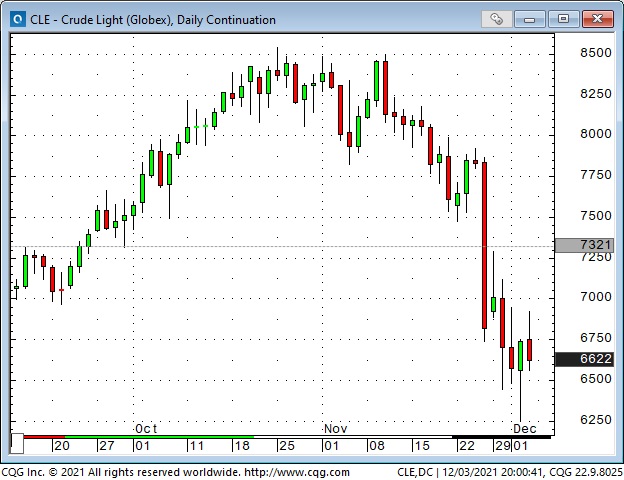

WTI fell today to an intra-day low (so far) of US$69.39/b and is now hovering just below US$70/b. From the late October high of US$85.41/b WTI crude has fallen 18%. Today’s Federal Reserve conference call will be critical to the go forward health of the US economy and for crude prices. Tightening of the economy is the antithesis for energy bulls. With our concern about the strength of the US and China economies (the largest two in the world) we still see prices having US$15-20/b of speculative value which should disappear as demand weakens once winter is over. Leveraged speculative longs in crude oil futures are vulnerable to nasty margin calls and this should add momentum to the recent downside pressure. In the next few weeks the price of crude should retreat to US$62-65/b and then bounce around for a while. Our target for WTI in Q2/22 once winter demand is over is US$48-54/b. This should set up an important low before our key signals should turn bullish again.

Energy Stock Market: The S&P/TSX Energy Index currently trades at 152, down 12 points or over 7% from last week. From the start of the crude price decline, the Index has fallen from 172 or down by 12%. As crude prices retreat in the coming weeks we see downside for this Index to the 95-105 level during Q2/22, implying severe downside. Oil stocks are the most vulnerable as are any companies in the sector with over-leveraged balance sheets.

Our December Joint Monthly Report comes out tomorrow Thursday December 16th. We go over the history of bear markets and why we see us just entering another one. The magnitude of the declines are discussed in comparison to other overvalued markets since 1900 and we project potential downside targets for the overall stock markets and the energy sector during this market decline/plunge. A key section is our 2022 Fearless Forecasts.

Once this bear phase exhausts itself, a lengthy and powerful new Bull Market will arise and energy will be a prime beneficiary. We intend to send out multiple Action Alert BUY ideas once the next low risk entry point arrives.

Our next quarterly webinar will be held on Thursday February 24th at 7PM MT.

If you would like to access this upcoming 2022 Forecast Report and all previous reports and the webinar archives, go to https://bit.ly/34iKcRt to subscribe.

Please feel free to forward our weekly ‘Eye on Energy’ to friends and colleagues. We always welcome new subscribers to our complimentary macro energy newsletter.

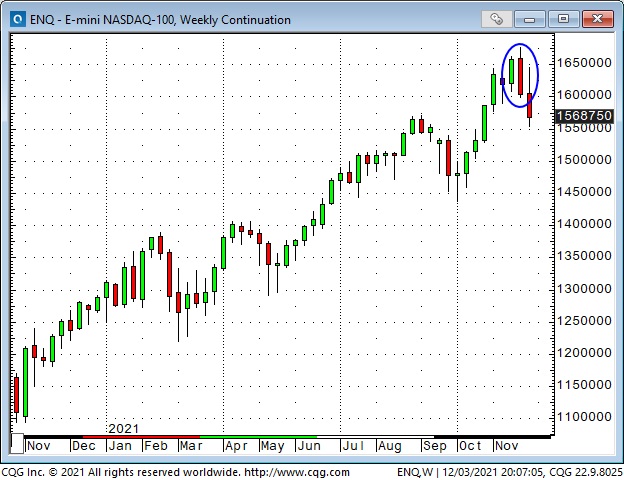

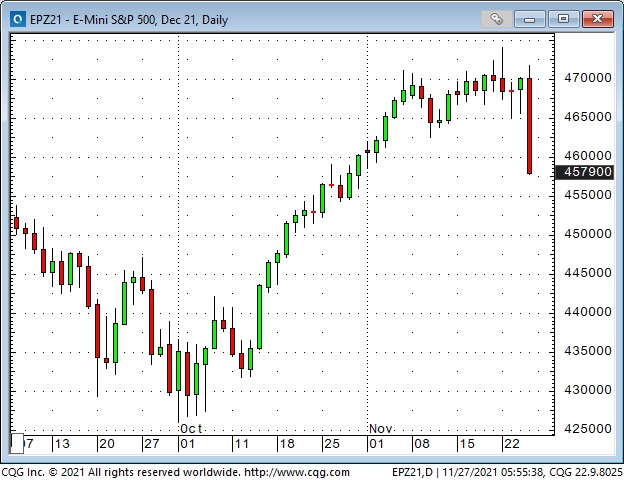

Bullish enthusiasm came roaring back this week – the S+P registered an All-Time High close – the DJIA rallied >2,000 points from last week’s lows

The S+P hit All-Time Highs Monday, November 22, but closed down on the day. Three sessions later, waves of heavy selling in illiquid conditions on Thanksgiving Friday caused the index to close 163 points below Monday’s high – the biggest down week since January (and a Weekly Key Reversal Down on the chart.)

The following week saw violent intra-day price swings. Late in the day on Friday, December 3, the S+P traded ~250 points below the previous week’s highs, volatility levels had soared to near the highest levels YTD – and then, the tide turned, the index bounced and closed ~40 points off its lows.

The Sunday, December 5th afternoon futures session opened higher, and by mid-morning Tuesday, the S+P had rallied ~170 points from Friday’s lows. The market chopped sideways within a narrow range the next three days, and Friday registered an All-Time High close (~27 points below the November 22 ATH.)

The “cash” DJIA (not the futures) registered a big “Island Reversal” on the charts. Some folks see that as a bullish pattern.

AAPL surged to New All-Time Highs this week with a market cap of ~$3 Trillion – up ~ $500 Billion from month-ago levels. (See a great list of global company market caps at https://companiesmarketcap.com/)

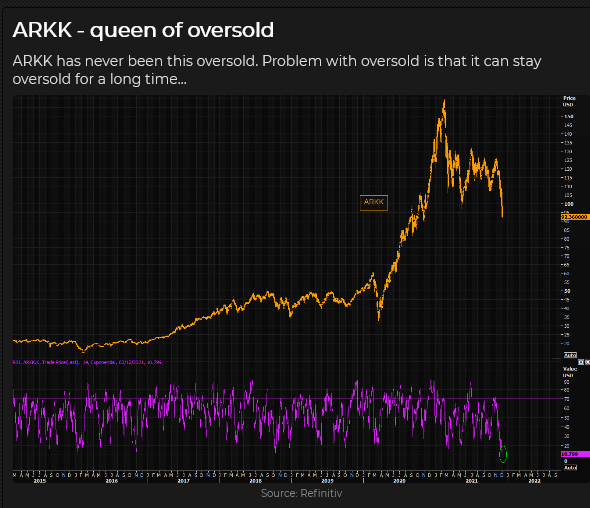

ARKK (last year’s darling) is down ~44% from its February highs – while the S+P is up ~18% since mid-February.

Concentration

Everybody knows that a handful of Big Cap tech stocks account for ~25% of the weighting of the S+P 500 – but here’s another look at concentration: The Nasdaq total YTD return is ~21%. Five stocks (AAPL, MSFT, GOOGL, TSLA, NVDA) account for ~2/3 of those returns. The Nasdaq total YTD return is less than 6% without those five stocks.

Passive capital flows boost Big Cap stocks

One of the reasons Big Cap companies keep getting bigger is that a tidal wave of money has flowed into the markets this year. More than half of that money has gone into passive investments, which track/mimic the indices. (There has also been a flow of capital leaving actively managed investments for passive investments.)

The PMs who “manage” passive funds allocate money according to the index weightings. So, for every dollar of new money they invest in S+P tracking funds, ~16 cents goes into AAPL, MSFT, and AMZN. It’s a bit like a perpetual motion machine; the more money coming in, the bigger the biggest cap stocks get relative to other stocks.

Active capital flows boost options volume (and meme stocks)

The smaller half of the tidal wave of money flowing into the markets goes into “active investments.” This covers everything that is not “passive” and includes both managed and self-directed “investments.” “Active” could range from old-fashioned mutual funds with stock picking, “value-seeking” portfolio managers to YOLO kids rolling the dice on short-dated OTM options.

Interest Rates

Prices of long-dated Treasuries have been trending higher for the past several weeks (yields have been falling), and they rose to new YTD highs when the stock market rattled investors’ nerves last week. With the stock market rising this week, bond prices fell.

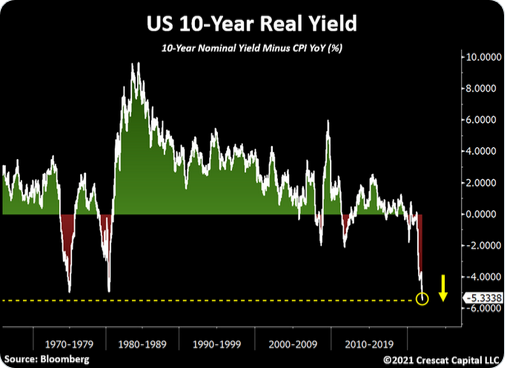

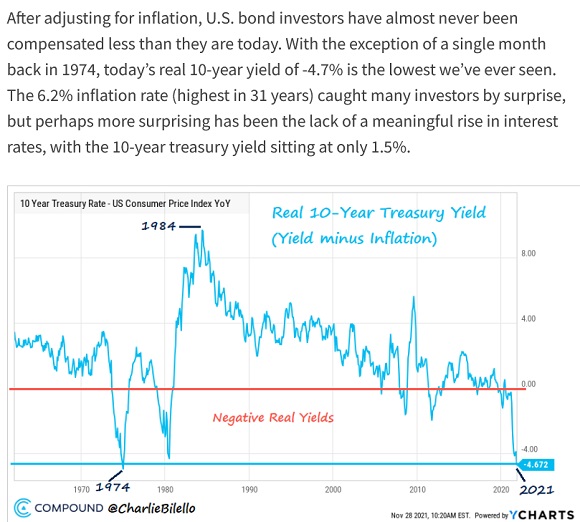

With the CPI at 6.8% and the ten-year Treasury yield at 1.47%, the 10 Year Real Yield = negative 5.33%. This is not the best “measure” of inflation (for instance, the 10-year Tips/Treasury breakeven rate is 2.52%), but MSM will feature this (sensational) number.

Currencies

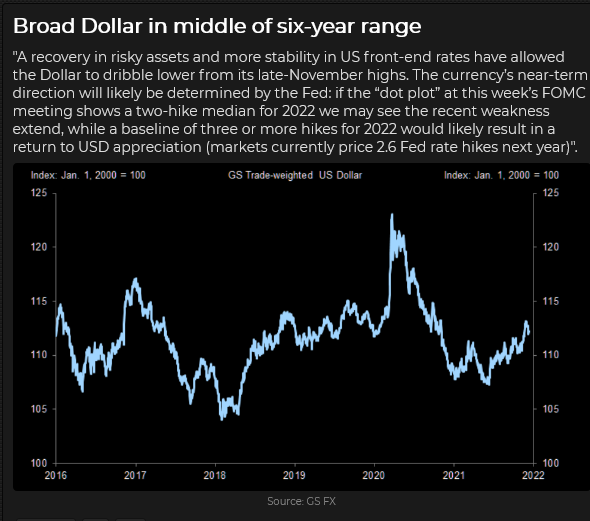

The US Dollar Index has been relatively steady at ~96 for the past four weeks, a 16 month high. Speculators have accumulated the largest net long USD position in the currency futures market since June 2019.

The Canadian Dollar fell for six consecutive weeks as the USD rallied and commodities (especially crude oil) fell, but it bounced a bit this week (WTI rallied ~$10 from last week’s lows and stock markets surged higher.)

The CAD may have rallied ahead of Wednesday’s BoC meeting in anticipation of a more hawkish tone, but that hawkish tone was not forthcoming, and the CAD fell Wednesday through Friday.

Commodities

The broad Goldman Sachs Spot Index reached a 7-year high in October as crude oil hit a 7-year high. The index drifted lower and then took a sharp drop late in November as WTI crude extended its decline from ~$85 to ~$62. The index bounced back the past few days as investor sentiment improved and WTI bounced ~$10.

My Short-Term Trading

Last week I bought the S+P and the CAD a few times – expecting investor sentiment to bounce after the sharp tumble that began on Thanksgiving Friday. Net, net my P+L was down ~0.50% on the week. I was early on my “rebound” call.

As noted above, the S+P made its low last week late Friday and rallied ~40 points into the close. When the market opened higher Sunday afternoon, I maintained my BTD mentality, but I waited for the Monday day session (for confirmation) before buying the S+P.

The market rallied during the Monday day session and soared in the overnight session. I covered the trade mid-day Tuesday for a gain of ~120 points (roughly equivalent to ~1,200 Dow points.)

I shorted the S+P a couple of times later in the week, thinking the market had rallied too far, too fast, but I was stopped for small losses on those trades.

I shorted the CAD when it fell back following the Wednesday BoC meeting. I’ve remained short CAD, which is the only position I hold going into the weekend. My P+L is up ~1.25% on the week, not counting unrealized gains on the short CAD.

On my radar

I’ve generally been bullish on the USD this year, but I haven’t capitalized on that view. (There is always room for improvement in trading!) Over the years, I’ve noticed that currency trends often go WAY further than what seems to “make sense,” and then turn on a dime and go the other way. Those reversals often happen around the end of the year, so I’ll watch for that over the next month or two.

Too many people believe that it’s easy to make money buying stocks – so we may see a correction there.

Thoughts on trading

Stories: Last week I wrote that I don’t like to “buy” stories. For instance, I don’t want to buy copper (simply) because the “story” says electrification demand and limited new mine supply automatically means that copper prices will go up.

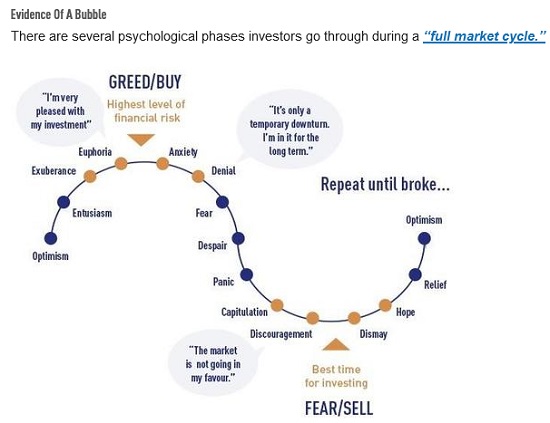

That doesn’t mean that I ignore stories. Stories have a life cycle, and I think it is essential to know where they are in their cycle. For instance, George Soros liked to say that when he saw a bubble forming, he bought the market in anticipation of the bubble growing and taking prices much higher.

I’m skeptical of stories because they cause people to focus on the “why” to buy rather than the “when” to buy. A good story is also seductive, which may encourage poor risk management practices – and I genuinely believe that good risk management contributes more to long-term trading success than any crystal ball.

When I hear a good story my first thought is always: “Who doesn’t already know that?”

Wizards: In the past two weeks, I’ve referred to the RTV interview Jack (Market Wizards) Schwager recently did with Peter Brandt. In that interview, Jack talks about what the “Wizards” have in common. He said that most of them started their trading career with poor performance, and it took years for them to “find their way” to becoming super successful, and they had to change their methodology as markets changed.

Jack also noted that some wizards had no problem managing other people’s money. Other wizards could not do it – they felt bad/guilty every time they took a loss, which killed their ability to trade freely.

Reminiscences: My bedtime reading lately has been Reminiscences Of A Stock Operator by Edwin Lefevere. I bought my first copy of that book more than 40 years ago (it was written over 100 years ago) and I have re-read it every couple of years. I had forgotten how good it is. It is the story of a trader learning how to trade (he “reads the tape“) but at another level, it is a fantastic and very honest, story about The Trading Life. I recommend it to you.

Quotes from the notebook

“It is normal/typical to think, “I’ve missed the move…I can’t buy it here after it has rallied so much!” But most money is made not by picking bottoms but by going with the trend and especially as the trend accelerates near the end of the move.” John Burbank, RTV interview with Alex Gurevich 2019

My comment: I picked this quote because I wish I were more like that! Some guys make it look easy!

When a market is going down, you have no idea how far down, down is!

It’s not a problem until it’s a problem, and then it’s really a problem.

There is never just one cockroach.

Do more of what is working and less of what is not working.

Dennis Gartman, many times, over the years

My Comment: Dennis was a trader in the old “South Room” at the CBOT, trading GNMAs and T-Bonds, in the late 1970s when I first visited the Chicago trading floors. I didn’t meet him then – we didn’t meet until the early 1990s (when his daily letter used to come by fax), and we became good friends over the years. He put a lot of work into writing his daily letter and passed along many good insights and observations – such as the quotes above.

A Small Request

If you like reading the Trading Desk Notes, please do me a favour and forward a copy or a link to a friend. Also, I genuinely welcome your comments. Please let me know if there is something you would like to see included in the TD Notes. Thanks, Victor

Barney is getting ready to show me around the golf course.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.

Each week Josef Schachter gives you his insights into global events, price forecasts and the fundamentals of the energy sector. Josef offers a twice monthly Black Gold newsletter covering the general energy market and 30 energy, energy service and pipeline & infrastructure companies with regular updates. We also hold quarterly webinars and provide Action BUY and SELL Alerts for paid subscribers. Learn more.

EIA Weekly Oil Data: The EIA data of Wednesday December 8th was mixed. US Commercial Crude Stocks fell 0.2Mb (forecast a decline of 1.71Mb). A key component was a decline in Exports of 434Kb/d. Refinery Utilization Rose by 1.0 points to 89.8% from 88.8% in the prior week. With the pick up in refinery activity Total Motor Gasoline Inventories rose 3.9Mb while Distillate volumes rose 2.7Mb. Overall Storage rose by 4.2Mb. US Crude Production rose by 100Kb/d to 11.7Mb/d, to a new yearly high and nearing our 12.0Mb/d target for late 2021 or during winter 2021 – 2022. Total Demand fell by 385Kb/d to 19.84Mb/d. Gasoline consumption rose by 167Kb/d to 8.96Mb/d which is just above the 8.88Mb/d consumed in 2019 at this time. Jet Fuel Consumption fell 507Kb/d to 1.22Mb/d versus 1.58Mb/d consumed in 2019. Cushing Inventories rose 2.4Mb to 30.9Mb/d.

EIA Weekly Natural Gas Data: Weekly withdrawals started two weeks ago as winter demand picked up. Last week, there was a withdrawal of 59 Bcf, lowering storage to 3.564Tcf. The five year average for last week was a withdrawal of 31 Bcf. Storage on a five-year basis was 3.650Tcf so storage is only 2.4% below the five-year average. NYMEX today is US$3.84/mcf down from the high in early October of US$6.47/mcf. AECO spot is at $3.48/mcf, down over $3/mcf from recent highs. As to be expected, natural gas stocks have retreated from their 2021 highs. With the two key months for natural gas demand ahead of us (January and February) we should still expect large price moves to the upside on very cold days. Spikes over $6/mcf should be seen on both sides of the border in the coming months when weekly withdrawals over 200 Bcf on a cold week occur. After winter is over natural gas prices will retreat and if the general stock market decline unfolds as we expect, then a great buying window could develop at much lower levels for natural gas stocks in Q2/22.

Baker Hughes Rig Data: The data for the week ending December 3rd showed the US rig count unchanged at 569 rigs last week. Of the total of 569 rigs working last week, 467 were drilling for oil and the rest were focused on natural gas activity. This overall US rig count is up 76% from 323 rigs working a year ago. The US oil rig count is up 90% from 246 rigs last year at this time. The natural gas rig count is up a more modest 36% from last year’s 75 rigs, now at 102 rigs. New Mexico saw an increase of five rigs last week to 88 rigs and was up 49% from 59 rigs last year as energy companies focused on the Permian potential in their state.

Canada had a rise of nine rigs to 180 rigs. Canadian activity is now up 76% from 102 rigs last year. There were seven more oil rigs working last week and the count is now 113 oil rigs working, up from 40 last year. There are 67 rigs working on natural gas projects now, up from 62 last year.

The material increase in rig activity over a year ago in both the US and Canada should continue to translate into rising liquids over the coming months, especially with the DUC count (drilled but uncompleted well count) at very low levels. The data from many companies on their plans for 2022 support this rising production profile expectation. We expect to see US crude oil production reaching 12.0Mb/d this winter. Companies are taking advantage of attractive drilling and completion costs and want to lock up experienced rigs and crews as staffing issues are getting tougher for the sector.

Conclusion:

Bearish pressure on crude prices:

- A coordinated effort by consuming nations to lower rising gasoline prices by opening their strategic reserves (SPR’s) with total releases in the range of 100-120Mb (US 50Mb) is being offset by OPEC. OPEC is not fully adding their planned 400Kb/d each month. The US is also considering a renewed ban on crude exports which was allowed to start in 2015 by President Obama after a 40-year ban. The US is also considering restricting all buying from OPEC+ members.

- Covid caseloads are growing around the world. In the US, the death rate is over 790K deaths. Worldwide, the death count is now 5.26M. Deaths are rising in Europe particularly in Austria (imposing full lockdowns on the unvaccinated). Belgium and Germany (which has now over 58K new daily cases) plan to tighten restrictions next week. New York is planning to require all private-sector workers to be fully vaccinated. Many may quit their jobs if they don’t want to vaccinate and opposition to this will mean lots of court cases.

- Energy demand is under pressure as high prices for most food, rent, taxes, child care, health expenses, auto costs and other daily necessities make spending decisions tougher for consumers. This gouge in prices will surely impact consumers’ buying behavior in the coming months. The spending pie of consumers is shrinking and some spending habits of the past will have to be dropped. Demand destruction is on the way. Recent US economic releases indicate that we may already be in the early stages of a recession.

- China has seen a rising wave of new infections in 19 of its 31 provinces. Many industrial plants in China have been closed due to the high cost of fuel and the Government’s plan to lower emissions in the Beijing area for the upcoming 2022 winter Olympics from February 4th to the 20th. Clean air is needed for the event and China wants to show it is making progress on its climate initiatives. They are importing large amounts of LNG to meet their electricity needs.

Bullish pressure on crude prices:

- While approving an increase of 400,000 b/d of new production for January 2022, OPEC may not achieve this target once again. It is an issue of following what they say versus following what they are doing. In October they only brought on an additional 217Kb/d versus the 400Kb/d announced. Preliminary reports show that in November they may have added just over 200Kb/d of real new volumes.

- The Omicron new Covid-19 variant does not appear to be more deadly, just more transmissible and vaccine manufacturers expect that with the booster shot individuals will be adequately protected. Most people in hospital ICU’s with this variant were not vaccinated at all.

- The Iran deal is not seeing progress as the Iranians continue to want removal of sanctions to sell oil but do not want to slow down their nuclear weapons program or allow intrusive UN inspections. The bulls are rejoicing that the 1-2Mb/d of new Iranian oil that could come on is now more unlikely.

- If Russia invades Ukraine, sanctions will be added to pressure Russia to desist. Russia may face OECD blockages of sales of crude oil. This would be positive for China but would hurt Europe which would need to find other more expensive suppliers.

- JP Morgan and other US investment banks see world demand exceeding pre-pandemic levels in Q2/22. Their fearless forecasts see US$80/b in early 2022 and US$100/b in 2H/22.

CONCLUSION:

WTI fell on Friday November 26th by US$10.24/b (down over 13% on the day) to US$68.15/b as the fear of Omicron spreading around the world hit the markets. The Dow Jones Industrials closed down that day by 905 points to 34,899 and was down the largest point amount for 2021. With some reassurance about Omicron, the price of crude has rebounded back upward. The low intraday bottom was US$62.42/b (four days ago) and now stands at US$71.86/b (down US$7/b from our last report two weeks ago). With our concern about the strength of the US and China economies we still see prices having US$20-25/b of speculative value which should disappear as demand weakens once winter is over. Leveraged speculative longs in crude oil futures were vulnerable to nasty margin calls and this added to the recent downside pressure. Our target for WTI in Q2/22 is US$48-54/b implying much more downside for the sector.

Energy Stock Market: The S&P/TSX Energy Index currently trades at 164, down five points from our last issue. During the crude price decline of the last two weeks the Index fell to 152 and has since rebounded as crude prices recovered. As crude prices retreat in the coming weeks we see downside for this Index to the 95-105 level implying some severe downside. Oil stocks are the most vulnerable as are any companies in the sector with over-leveraged balance sheets.

Our December Joint Monthly Report comes out on Thursday December 16th. We go over the history of bear markets and why we see us entering another one. The magnitude of the decline is discussed in comparison to other overvalued markets since 1900 and we project potential downside targets for the overall stock markets and the energy sector during this market decline/plunge. A key section is our 2022 Fearless Forecasts. Once this bear phase exhausts itself, a lengthy and powerful new bull market will arise and energy will be a prime beneficiary. We intend to send out multiple Action Alert BUY ideas once the next low risk entry point arrives.

Our next quarterly webinar will be held on Thursday February 24th at 7PM MT.

If you would like to access this report and all previous reports as well as the webinar archives, go to https://bit.ly/3jjCPgH to subscribe.

If you enjoy reading our weekly ‘Eye on Energy’ feel free to forward it off to friends and colleagues. We always welcome new subscribers to our complimentary macro energy newsletter.

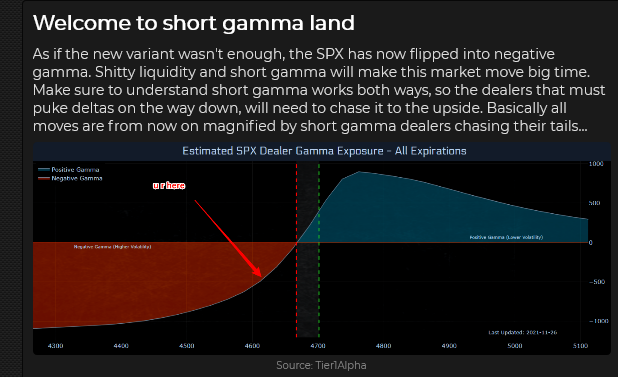

A vicious circle of aggressive selling, thin liquidity, volatility and fear

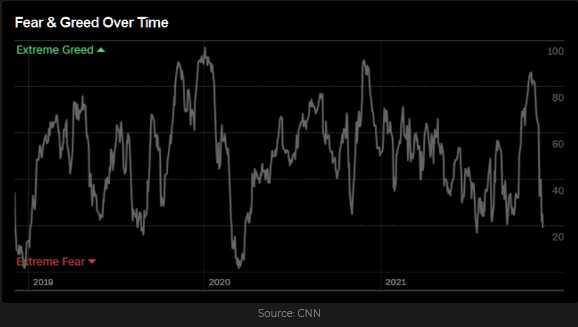

Given the drama since Thanksgiving Friday, it’s hard to believe that the leading North American stock indices were at All-Time Highs Monday of last week. It’s also hard to believe that, with the DJIA, S+P, NAZ, TSE and VTI indices down only ~6% on average, implied volatility has doubled, and the fear/greed index has plunged to levels not seen since March 2020.

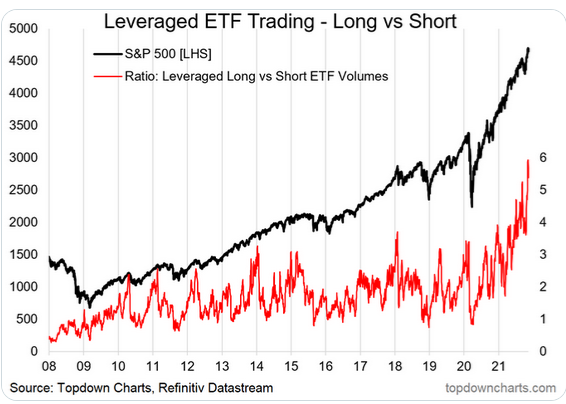

This year, a tidal wave of retail money has flowed into the stock market. Market risk has increased because of all that extra “new” money

More than half of that money has gone into passive, index-linked investments – boosting the value of those indices – and especially the value of the handful of large-cap stocks which dominate those indices.

Passive investors expect “small corrections,” but they plan to “stay the course” because, inevitably, stocks only go up. I don’t expect any significant selling from that sector – unless the indices remain in a bear trend for six months or more. If those folks ever start selling, we will see what a real bear market looks like! (Who will take the other side of that trade?)

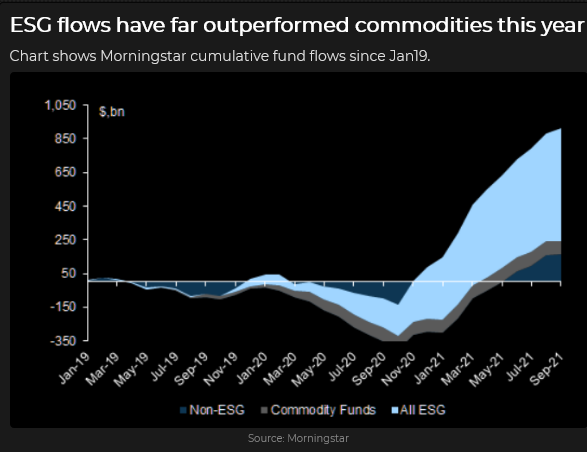

Other retail money has gone into “active” investments – everything from niche hedge funds (especially anything with ESG in the name) to YOLO kids buying deep OTM options. Some of that money has been Buying the Dip since last Friday (ouch), but I bet you some hedge funds/ CTAs have sensed trouble ahead and are hitting the bid to lock in a good performance record for 2021.

Regardless of who has been doing what, the short-term price action has been very choppy (up or down the equivalent of 500 Dow points in less than an hour a few times this week), and the trend has been down. Volume has been relatively high, sentiment across asset classes has taken no prisoners.

Last week, the S+P and NAZ charts registered a Bearish Weekly Key Reversal Down from All-Time Highs.

Bonds have soared as stocks and commodities have tanked

The TLT (20+ year maturity) and the Ultra-long T-Bond futures contract (25+ year maturity) closed the week at their highest prices YTD. If the bond markets were worried sick about inflation, that wouldn’t be happening – so this must be a fear-induced bid, given that the short end is pricing in at least two Fed interest rate increases next year. The ULA is up 11 points from last Friday’s low – the biggest/fastest increase since the Covid ramp in February 2020.

The US Dollar Index had its highest weekly close in 16 months

When market sentiment gets fearful, the USD gets bid. The following currencies closed this week at their lowest YTD levels: GBP, CAD, AUD, NZD, NOR, SWE, IND, and, of course, Turkey. Many other currencies are very close to their lowest levels in (at least) a year. (Notable exceptions, Israel, China.)

The Canadian Dollar has closed lower for seven consecutive weeks, as has the Goldman Sachs Commodity Index. (WTI has closed lower for six straight weeks.) The CAD had a brief rally this Friday on the much-stronger-than-expected employment report, but as stocks and crude fell and the USD rose, the CAD reversed to close on its lows.

Gold rallied ~$120 on the “inflation” story in early November – but gave it all back the last two weeks

The Open interest on Comex gold futures shows speculators chased the gold price higher and then bailed out as the price fell back to month-ago levels.

Silver tumbled as much as $3.50 (14%) from mid-November highs, with Comex open interest falling to near 8-year lows.

WTI crude oil dropped 27% from a 7-year high of ~$85 to ~$62

Front-month WTI tumbled more than $11 on Black Friday. The HUGE premium of front-month WTI over the deferred months evaporated. OPEC+ went ahead with their scheduled increase of 400,000BPD.

My Short-Term Trading

In the On MY Radar section of last week’s Notes, I said that I didn’t know if Black Friday’s dramatic (Omicron inspired?) plunge in ultra-thin liquidity conditions was the start of “something” or just a flash-in-the-pan – but I was leaning towards “something.“

Stock index futures and WTI opened sharply higher Sunday afternoon (Omicron wasn’t so bad after all.) Stock indices took out Friday’s day session highs before the opening of the Monday day session. Friday’s nose-dive looked like a flash-in-the-pan, so I bought the Dow and the CAD.

Those positions were stopped for small losses Tuesday morning when Powell kissed “transitory” goodbye.

Over the next few days, I traded the S+P and the CAD, looking for a bounce. I bought futures and sold OTM S+P puts with a 30 vol. Every trade initially worked in my favour. I made some money and lost some money, but my P+L was down ~0.50% on the week.

I was flat going into the weekend – ruefully wondering how I missed making money on the short side.

On My Radar

If I think in terms of a multi-month time frame, my bias is to believe that the “chasing” of risk assets is WAY overdue for a correction. In terms of a day-to-day time frame, I think we’ve had a pretty good correction over the past two weeks.

I try to avoid taking a position based on a “story” (for instance, copper has to go a lot higher because of global electrification and a shortage of new mine supply.) I understand that many successful traders have made fortunes because they bet big and were right on a story. (The Big Short.)

You don’t hear about all the people who believed a story, bet big, and went down with the ship because they knew they “had to give it a little more time.”

Stories are seductive, and maybe you have to believe in something to make money from trading/investing. Or perhaps you have to believe in yourself and your method.

Last week, I referenced a clip of the Peter Brandt interview with (Market Wizards) Jack Schwager. I watched the full interview on RTV this week. Jack said that the 70 very successful traders he featured in his books seemed to have no personality or educational traits in common but that they all had found a way to participate in markets that suited them. They all had a great appreciation of risk management/control – to the degree that their long-term success depended more upon risk management than upon their methodology.

Jack succinctly said that the Wizards had “no loyalty to a position.” I took that to mean that they did not believe in stories.

Some folks would argue that you need some degree of “belief” in a trade to be able to stick with it during a short-term setback (however you define “short-term setback.“) I would counter by saying that I would stay with a trade until my trailing stop was hit.

I believe that every person has to find their own way to trade/invest – that successful traders have found a unique way to trade that suits their personality, time frame, and risk tolerance.

Thoughts On Trading

Reminiscences of a Stock Operator has been my bedtime reading lately. I bought my first copy of that book over 40 years ago, and I’ve re-read it every couple of years since. It was written ~100 years ago, but it still rings true today. It’s the story of a man finding his way to successful trading through trial and error. His style is probably WAY too aggressive for most people (including me), but his observations of himself, the people around him, and the markets make it a good read. I recommend it to you.

Quotes From The Notebook

“I don’t believe in much, but I sure do believe in reversion to the mean.” James Clarke, Successful Options Trader, 2019

My comment: Back in the 1980s, Jimmy worked for a prop trading firm in an office with no name of the door, 19 floors above the CBOE. He described his trading methodology as “being the buyer of last resort for OTM S+P options.” We were having dinner in 2019 – the first time we had seen each other in several years – and the subject of “what do you believe in” came up.

“Anything that will generate yield is being monetized.” Diego Parrilla, 2016

My comment: I had been impressed with the book Diego Parrilla, and Daniel Lacalle wrote – The Energy World Is Flat. This quote is from a subsequent interview. One of my “opinions” back then was that option volatility was WAY lower than it “should be” because people were selling vol to generate yield – that reaching for yield had become the most crowded trade in the world.

The lust for yield has overwhelmed Prudence. Bob Hoye, 2017

My comment: My friend Bob Hoye has been a treasure trove of quotes, and this one ties in beautifully with Diego’s selection.

A Small Request

If you like reading the Trading Desk Notes, please do me a favour and forward a copy or a link to a friend. Also, I genuinely welcome your comments. Please let me know if there is something you would like to see included in the TD Notes. Thanks, Victor

Barney: (13 weeks old, 20 pounds) Yeah, hit that bid before it disappears!

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.

Risk Happens Fast

The S+P 500 hit All-Time Highs on Monday’s opening – but closed 165 points (3.5%) lower by Friday’s close. The daily S+P futures volume on Friday was the highest since early October – and was probably the highest EVER for a Thanksgiving Friday.

The DJIA closed at a 7-week low, down ~1,800 points (5%) from the All-Time High reached three weeks ago.

The Acid Test

My recent thinking has been that market complacency would likely continue – unless the September/October lows are taken out. I think people who have put money into “passive” investment strategies have been told to expect minor corrections and short-term spikes in volatility – but to stay the course because, inevitably, stocks will keep rising.

I think those folks also “feel” as though the unrealized gains in their investment accounts are as “good as cash” when it comes to calculating their net worth, and that, while the market could have a dip now and then, it will NEVER AGAIN drop like it did in March 2020.

When Complacency Turns To Panic, Volatility Soars

There was complacency with “risk-on” sentiment across asset classes early this week, but as sentiment turned “risk-off” Thursday afternoon and prices began to slide, “liquidity risk” accelerated the panic, and volatility soared.

Position Unwinding Added To Volatility

For the past few weeks, traders (especially in the interest rate and currency markets) have been building positions around the idea that the Fed would be “forced” to raise interest rates much more, and much faster, than previously expected – because of “inflation.” There was severe unwinding of some of those positions in illiquid market conditions during the last 24 hours of the trading week.

Interest rates: As stock indices tumbled on Thursday/Friday, bonds rallied hard, and short-term interest rate futures “un-priced” at least one Fed rate increase next year.

Currencies: The US Dollar Index surged to a new 16-month high early this week on expectations that the Fed would be much more hawkish next year than previously expected. The USD reversed those gains on Friday to close unchanged for the week.

The Japanese Yen plunged to a new 5-year low against the US Dollar early this week but reversed HUGE on Friday. Speculators have amassed a HUGE net short Yen position over the past few months.

The Swiss Franc caught a “haven” bid Friday after tumbling the past two weeks on expectations of Fed tightening next year.

The Canadian Dollar hit a 6-year high against the USD at 83 cents in June but fell back as the USD began to rally against all currencies.

The CAD rallied to a lower high (81 cents) in October as commodity indices (especially crude oil) surged to 7-year highs. When the commodity indices (especially crude oil) began to roll over and slide lower, the CAD also began to trend lower.

WTI rallied from ~$62 to ~$85 (37%) in two months, from mid-August to mid-October. The strong demand for near-term delivery over deferred delivery caused a severe steepening of the forward curve. Front-month WTI fell from ~$85 three weeks ago to a low of ~$68 Friday, with more than half that decline happening in illiquid conditions on Friday. Implied volatility in WTI options spiked sharply.

Gold rallied ~$110 the first two weeks of November and fell ~$100 the next two weeks. Gold’s initial rally phase happened in sync with a USD rally (an unusual occurrence) as both markets reacted to the “soaring inflation” narrative. Gold’s tumble happened as the USD continued to rally (the more typical gold/dollar relationship), and as real interest rates reversed from record negative levels.

Open interest in the gold futures market (circled above) increased sharply as gold rallied in early November as speculators “chased” it higher. As gold fell, some of those speculators “bailed out,” exacerbating the decline.

My Short Term Trading

The only position I held as this week began was short gold, and I covered that for a good profit on Monday. Gold had tumbled ~$75 in three days – I was only short because I was looking for some “give-back” after the early November rally – so I covered the position.

I shorted the NAZ about an hour after the Monday floor session opened. The market had surged to an All-Time High on the opening but then dropped below the opening range. I had been looking to sell “irrational exuberance,” so I saw a nice setup and got short with tight stops. The market fell during the day, and I lowered my stops – and was stopped for a small gain later in the day.

The falling bond market on Monday increased my confidence to short NAZ as that index is heavily weighted with “long duration” stocks.

I shorted NAZ again on Tuesday but I was also watching the Dow futures and noticed they were not falling. I covered the short NAZ for a small gain and bought Dow futures. I was stopped for a small loss.

I bought the S+P on Wednesday, was stopped for a small loss, but then I bought it again. The market closed right on its highs so I decided to stay with the trade into the Thanksgiving holiday. (This was a decision to give the trade an opportunity to run. The market had been trending strongly higher, had dipped Monday and Tuesday, and was now closing right on the highs. Staying with the trade was the right thing to do.)

The market continued to rally in the Wednesday overnight session. I raised my stops. The market drifted sideways during the Thursday holiday session, but then began to tumble as soon as the Thursday overnight session began and I was stopped for a small gain.

I made the right decision to stay with the trade when it closed on its highs. At its best levels, I was ahead nearly 40 points but was stopped for a gain of only four points. I have no regrets about that. Given what happened next, I’m thankful that I use stops.

I bought the CAD and gold on Wednesday. I was stopped for a small loss on the CAD in the Thursday overnight session and covered the gold for a small gain Friday morning.

I did not establish any new positions Friday and was flat going into this weekend. My P+L was up just short of 1% on the week.

On My Radar

I don’t know if Friday’s market action was the start of something BIG or a one-day flash-in-the-pan. I’m willing to go either way, although I’m leaning towards the start of something.

My bias has been that too much money has been flooding into risk assets without appreciating just how risky those assets can be. The risk in those assets has increased “because” of the money flooding in.

Thoughts On Trading

For years I had a small yellow sticky note on my screens saying, “Anything Can Happen.” I put it there to remind myself that I had no idea what was going to happen next.

A few weeks back, in the Quotes From The Notebook section, I featured the Godfather saying, “I spent my entire life trying not to be careless.”

If I wanted to briefly explain the essence of my trading style, I would say that I never want to take a big loss. I never “fall in love” with a trade.

Several years ago, I started working with another broker that I didn’t know very well. We were opening a new office for a Chicago commodity firm in Vancouver. One day I overheard him talking to his best client. He was telling his client why they had to stay with a trade that was relentlessly going against them. I couldn’t believe what I was hearing.

A few days later, I had an epiphany while taking a shower before I headed to work (I get a lot of good ideas in the shower or in the pool – there’s something about water that does that – and, of course, you can’t make a note to yourself when you’re in the water!) My epiphany was that the broker was, first and foremost, a stockbroker – who also happened to be a commodity broker – and that stockbrokers believe and tell stories – good commodity brokers don’t do that.

Here’s a 90-second video of Jack Schwager (author of the Market Wizards series) explaining that one of the things the 70 Wizards he interviewed for his books had in common was their ability to have no loyalty to a position. (This is a fantastic insight – and great trading advice!)

Quotes From The Notebook

“Don’t count your chickens before they hatch.” My Grandmother kept telling me that from the time I was a little boy until she died.

My comment: My friend Peter Brandt likes to say that he never counts unrealized gains as “his money” it’s not his until he closes the trade. I can’t tell you how many times I’ve assumed that a trade would be a big winner – only to have it go sour on me.

Peter also likes to ask this question, “Let’s say you hold a position with an unrealized gain of $10,000. The market moves against you and you liquidate the trade to realize a $5,000 gain. Do you feel like you made $5,000 or lost $5,000 ?”

My guess is that if you feel like you lost $5,000 (because you didn’t get out at the top) you’re going to have an unhappy life as a trader. Have I mentioned before that trading is not a game of perfect?

“WHEN you make a trade is WAY more important than WHY you make a trade.” Raoul Pal, Founder of Real Vision TV, 2021

My comment: I agree 100%. Focusing on “why” you are making a trade may cause you to be too “loyal” to the trade. (Refer to Jack Schwager’s interview above.) Focusing on “when” you make a trade means you realize that there is a time to make the trade, and a time to NOT make the trade.

A Small Request

If you like reading the Trading Desk Notes, please do me a favour and forward a copy or a link to a friend. Also, I genuinely welcome your comments. Please let me know if there is something you would like to see included in the TD Notes. Thanks, Victor

Barney (now 12 weeks old) “Papa, leave your computers alone and play with me!”

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair