Energy & Commodities

Ivor Ries Most investors may not have Australian resource companies on their radar screens, but that doesn’t mean that there aren’t some great opportunities worth pursuing Down Under. In this exclusive interview with The Energy Report, Ivor Ries, utilities and energy analyst at E.L. & C. Baillieu Stockbroking Ltd., one of Australia’s oldest securities firms, describes the challenges faced by energy-related companies in his country and how they are taking advantage of the opportunities available both at home and in the U.S., Canada and South America.

Companies Mentioned: Approach Resources Inc. – BHP Billiton Ltd. – ConocoPhillips – Devon Energy Corp. – El Paso Pipeline Partners, L.P. – EOG Resources, Inc. – Karoon Gas Australia Ltd. – Molopo Energy Ltd. – Origin Energy Ltd. – Pioneer Southwest Energy Partners, L.P. – Red Fork Energy Ltd. – Rio Tinto – Woodside Petroleum Ltd.

The Energy Report: Your firm has been in the investment business for over 120 years. Can you give us an overview of the energy markets and the challenges and opportunities that energy companies in Australia face?

Ivor Ries: Australia has historically been the quarry and energy source to emerging Asian economies. As a result, our economy is inextricably linked with the progress of China, Korea, Japan, India and the other Southeast Asian economies. Initially, we were mostly a supplier of minerals, but in recent years, the liquefied natural gas (LNG) markets have become a very large part of our economy. We have two very large LNG projects in production and a third smaller one in Darwin. Another five LNG projects are now under construction, which will more than triple Australia’s LNG output over the next five or six years.

The LNG boom has its pros and cons. The investment spending is a huge boost to our economy, but it also has caused a huge shortage of contractors and manpower. The price of labor has gone through the roof in any business related to oil and gas. An unskilled laborer working on an LNG project in Australia is probably paid somewhere between two and four times as much as he or she would be elsewhere. Australia has very tight restrictions on labor coming in. At the moment, the industry is forcing the government to change that. The government recently announced it is going to reduce the visa requirements for American and Canadian oil and gas workers, so they can help plug that gap. That would be a huge relief for the industry. We have a very heavy-handed set of regulations here, and there has been a lot of media hysteria surrounding fracking, particularly in the coal-seam gas areas and a very strong campaign to have fracking stopped. Anyone running coal-seam gas or unconventional gas here has to run through a very stringent and time-consuming environmental approvals process, which probably adds two to three years to getting a project off the ground. When it comes to the cost of getting things done, everything takes longer and is more expensive than expected. That’s frustrating.

TER: What’s the breakdown of Australia’s energy production versus its consumption of oil, gas, coal and other energy sources?

IR: The domestic market in Australia is overwhelmingly coal driven. Australia is the world’s largest seaborne coal exporter, and our domestic power industry runs about 80–85% off coal and to a smaller extent off hydroelectric power and gas. Cheap coal gives us very low-cost baseload power across the entire economy. A population of only 23 million (M) people is just not enough to create a significant market for gas, and that has resulted in a terrible oversupply. Until we started shipping LNG, gas prices were incredibly low. We’re just now starting to see the connection between the domestic gas price and export prices. Typically, for the last five years, the price for gas on the east coast of Australia was about $3.50 per million British thermal units (MMBtu). Now we’re starting to see some longer contracts being signed at about $7–8/MMBtu.

TER: Do LNG exports offer a big potential opportunity?

To Read More CLICK HERE

Intermediate natural gas weighted stocks in Canada are valued higher—sometimes a LOT higher—than oil stocks, despite oil being worth 35 times more than gas.

And that could mean significant price weakness for already battered natural gas stocks, says Haywood Securities analyst Alan Knowles.

“People think (the stocks of) gas companies have corrected, but they’ve only partially corrected,” he told me in a phone interview. “The correction hasn’t kept pace with how far it should have gone,” given how low natural gas prices have moved.

At first glance, Knowles’ says the gas companies are NOT valued more highly than the oils—but that’s comparing the two groups at the industry standard of 6:1; where 6 barrels of natural gas are considered equal to one barrel of oil. See his chart below that shows this. The green dots are the leading intermediate oil producers—Crescent Point, Legacy Oil and Gas, Baytex and Petrobakken, and the red triangles are the gas weighted companies.

The gas stocks are clearly cheaper on this chart, which measures them in terms of the value of their production — $50,000 per flowing barrel up to $250,000; again all based on the industry standard 6:1 ratio.

To Read More CLICK HERE

There’s an old saying that goes something like this: “In the valley of the blind, the ‘one-eyed man’ is king.”

If you seriously consider what I’m about to show you, this old saying could well ring true for your investment portfolio at the end of this year. Perhaps even before. Let me explain…

At roughly $2.41 per million Btu, U.S. natural gas prices are in the dumpster. The truth is, they’ve been declining for years. But the recent shale gas boom accelerated their fall. Now they’re the lowest they’ve been in over a decade.

If it gets any cheaper, the companies that supply it will be paying you to take it. You see, they have a huge problem.

They have to keep producing in order to generate revenue, even in the face of declining prices. The problem here in the United States is that supply exceeds demand by a wide margin. And it’s getting wider all the time.

Why? Stores of natural gas at record levels… A mild winter… New wells coming online every month…

No wonder it’s eviscerating shares of explorers and producers. Take a look at the six-month chart for Chesapeake Energy Corporation (NYSE: CHK), for instance.

It looks like the first big drop on a roller-coaster. Shares are off 38% since last July.

To Read More CLICK HERE

By Marin Katusa, Chief Energy Investment Strategist

I recently gave an interview on Business News Network (BNN) about natural gas. BNN is Canada’s largest news channel dedicated exclusively to business and financial news, so all kinds of market players rely on BNN to provide them with comprehensive coverage of global market activity from a Canadian perspective. Like similar news channels in the US, BNN intersperses real-time news coverage with economic forecasting and analysis, company profiles, and tips for personal finance.

I have been interviewed on BNN numerous times over the last five years, quizzed on the impacts of fracking, the forecast for uranium following Fukushima, the potential of new frontier oil regions, and the future for coal. This time, the topic was “Five Tips for Natural Gas Investors.” You can watch the interview if you want; I highly recommend it – the education is worth the time.

On-air interviews are usually pretty speedy affairs, so my BNN interview didn’t give me enough time to discuss each point in depth. The Dispatch gives me that opportunity, so here are my five tips for natural gas investors in a bit more detail.

1. Watch for Looming Reserve Writedowns

A resource estimate is a geologic best guess of how much of a commodity exists within a particular deposit, be it ounces of gold, barrels of oil, or cubic feet of natural gas. A geologist gleans information about the deposit’s size and grade from drilling results and then creates a statistical model of the deposit. From that model he or she can estimate the commodity count.

However, the amount in the ground is not the amount that can be produced. That’s where the reserve estimate comes in. Reserves are an estimate of the amount of a commodity within a deposit that can be extracted economically, which means reserves are a whittled-down subset of total resources. That whittling down process has two steps. First, geologic and technologic factors determine a resource’s recovery rate, reducing the resource to the parts that are “technically recoverable.” Then, economic considerations further reduce the resource to only the bits that are “economically recoverable.”

With natural gas, the advent of horizontal drilling and multi-stage fracturing altered the first parameter dramatically, ballooning North America’s technically recoverable gas resources to many times their earlier volume. And while gas prices held, reserves counts ballooned too.

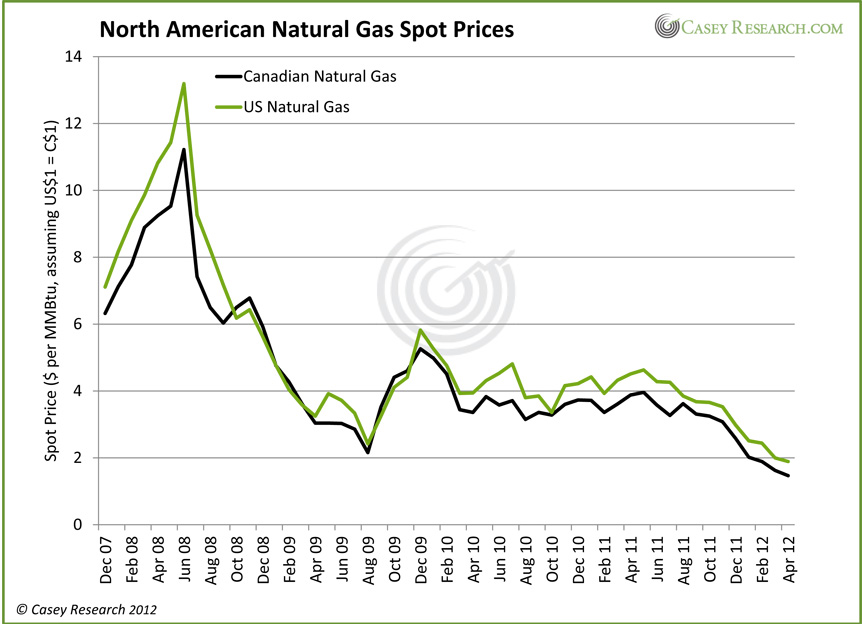

The key bit there was “while gas prices held” – that honeymoon is over. Natural gas prices in North America have declined roughly 35% this year and are down approximately 60% over the last 12 months. Compared to the unsustainable highs reached prior to the recession, gas prices have fallen more than 80%.

To Read More CLICK HERE

By James Hamilton

Joseph P. Kennedy II, former Congressional Representative from Massachusetts, and founder, chairman, and president of Citizens Energy Corporation, has a proposal to make energy affordable for all. All we have to do, Kennedy claims, is “bar pure oil speculators entirely from commodity exchanges in the United States.”

Writing in the New York Times last week, Joseph Kennedy (D-MA) explained why he believes that speculators are responsible for the high price that we currently have to pay for oil:

Today, speculators dominate the trading of oil futures. According to Congressional testimony by the commodities specialist Michael W. Masters in 2009, the oil futures markets routinely trade more than one billion barrels of oil per day. Given that the entire world produces only around 85 million actual “wet” barrels a day, this means that more than 90 percent of trading involves speculators’ exchanging “paper” barrels with one another.

It’s true that most buyers of futures contracts don’t actually want to take physical delivery of oil. If I buy the contract at some date, I usually plan on selling the contract back to somebody else at a later date, so that I leave the market with a cash profit or loss but no physical oil. But remember that for every buyer of a futures contract, there is a seller. The person who sold the initial contract to me also likely wants to buy out of the contract at some later date. I buy and he sells at the initial contract date, he buys and I sell at a later date. One of us leaves the market with a cash profit, the other with a cash loss, and neither of us ever obtains any physical oil.

Let’s take a look, for example, at NYMEX trading in the May crude oil futures contract. A single contract, if held to maturity, would require the seller to deliver 1,000 barrels of oil in Cushing, OK some time in the month of May. Last Friday, 227,000 contracts were traded corresponding to 227 million barrels of oil, which is indeed a large multiple of daily production. But it is worth noting that at the end of Friday, total open interest– the number of contracts people actually held as of the end of the day– was only 128,000 contracts, much smaller than the total number of trades during the day, and not much changed from the total open interest as of the end of Thursday. Many of the traders who bought a contract on Friday turned around and sold that same contract later in the day. If the purchase in the morning is argued to have driven the price up, one would think that the sale in the afternoon would bring the price back down. It is unclear by what mechanism Representative Kennedy maintains that the combined effect of a purchase and subsequent sale produces any net effect on the price. But the only way he gets big numbers like this is to count the purchase and subsequent sale of the same contract by the same person as two different trades.

It’s also worth noting that on that same day, there were 146,000 May natural gas contracts traded, which if held to maturity would call for delivery of natural gas at Henry Hub in Louisiana. A single contract represents about 10 million cubic feet, so Kennedy’s calculations would invite us to compare the 1,146 billion cubic feet of “paper” natural gas traded on Friday with the total of 78 billion cubic feet of natural gas that the U.S. physically produced on an average each day in 2011. Once again, the vast majority of Friday’s natural gas futures trades were matched by an offsetting trade during the same day so as to have little effect on end-of-day open interest.

By what mysterious process can all this within-day buying and selling of “paper” energy be the factor that is responsible for both a price of oil in excess of $100/barrel and a price of natural gas at record lows below $2 per thousand cubic feet? I suspect the reason that Kennedy does not explain the details to us is because he does not have a clue himself.

To Continue Reading CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair