Energy & Commodities

By Sumit Roy

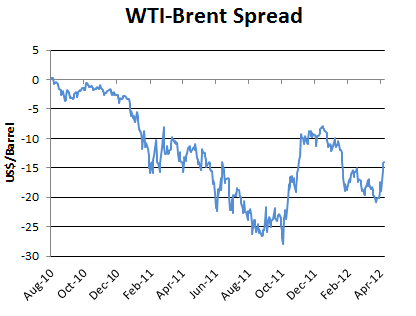

The volatile WTI-Brent spread fell to multimonth lows, but surging production in the U.S. makes further narrowing challenging.

The Department of Energy reported this morning that in the week ending April 13, U.S. crude oil inventories increased by 3.9 million barrels, gasoline inventories decreased by 3.7 million barrels, distillate inventories decreased by 2.9 million barrels and total petroleum inventories decreased by 2.2 million barrels.

As expected, Brent prices continued to drift lower over the past week after breaking below the key $121 support level amid economic concerns and receding Iranian tensions. But in an interesting twist, WTI prices actually rose in the period.

BRENT

WTI

The highly volatile spread between the two benchmarks narrowed to $14 from $17.50 last week and more than $20 at the beginning of the month. That puts it at the smallest level since Feb. 1.

The catalyst for this latest move in the spread was news that the operators of the Seaway Pipeline plan to reverse its flows earlier than expected — at the end of May, rather than June 1. As we’ve written about in the past, the Seaway Pipeline was designed to send crude oil from the Gulf Coast to Cushing, Okla. But surging production in Canada and the U.S. Midwest has created a glut of crude in the region, depressing prices for local benchmarks such as WTI. To reduce the gap between crude such as WTI and global benchmarks such as Brent, transportation capacity out of the Midwest needs to be increased. The reversal of the Seaway Pipeline — after which crude will flow from Cushing to the Gulf Coast — satisfies that need. About 150 Kbbl/d of the pipeline’s capacity is set to be reversed late next month, while another 250 Kbbl/d may be reversed by early 2013. Yet while the reversal of Seaway is a step in the right direction, the market anticipates it alone will not alleviate the Cushing glut completely. Still-wide spreads between WTI and Brent across the futures curve is evidence of that. Rapidly increasing output in the Midwest and Canada necessitates steady increases in transportation capacity. Declining demand across the United States makes the supply and demand balance even more lopsided.

To Read More CLICK HERE

“There is no life I know to compare with pure imagination. Living there, you’ll be free if you truly wish to be.”

– Willy Wonka

Chock another one up to the “let’s look like we’re doing something” category …

Hypothetical scenario:

Suppose all 5th grade teachers at a given elementary school give their students ample amounts of candy before recess each day. This sugar high has led to wilder children on the playground. It has also emboldened the kids to act more dangerously as their risk-taking is near perfectly correlation with their classroom popularity. Taken together, the now rowdier mob of children has led to an increased number of serious injuries on the playground. And pretend for a moment that the rest of the student body is responsible for the hospital bills of these injured 5th graders. And pretend that prior to the teacher’s decision to sugar-up her students before recess the rate of injury was insubstantial. What might they do to mitigate the increased cost the public must pay for the hospital bill?

Easy. Lower the heights of the playground equipment and pay new playground police to monitor the situation closely. But don’t alter the pre-recess candy supply (maybe even increase the supply if the kids begin to look sluggish now that the playground equipment isn’t as inviting …)

President Obama is talking tough – he’s going to crack down on the problem that’s driving gasoline prices beyond tolerable levels. He’s going to crack down on those wretched speculators.

Obama is urging the CFTC use its clout to get tougher on those trading in the crude oil futures market. Specifically, he wants to see higher margin rates per contract and wants them to enact some form of position limits to mitigate any abnormally large long positions that could serve to manipulate crude prices higher.

Ted Butler would be proud. [If you don’t know Ted, he’s been all over the CME and COMEX and the regulators to rain down on such large short positions that are allegedly manipulating precious metals’ prices lower. It will be interesting to see if this do-something attitude being applied to the crude oil market will translate to the precious metals et al.]

All that said, here’s a short list often used on a day-to-day basis to explain the fluctuation in crude oil prices:

Geopolitical risk (e.g. what might result from butting heads with Iran)

Supply/demand changes (e.g. falling energy consumption in the US or depletion of existing well output rates or Saudis pumping overtime or supertankers running out of gas or …)

Inflation hedge (e.g. hold real assets in case prices soar as a result of the declining purchasing power of the US dollar—the currency in which most commodities are priced)

Broad-market risk appetite (e.g. commodities moving in line with “risk assets” driven by growth opimtimism)

Let me say this: speculation is a necessary and natural form of price discovery in the markets. It is this price discovery that sends signals to all market players, financial and real. The pricing system is the core of the market system and what makes capitalism the best and more efficient way to structure an economy. Period! End of story.

Yet politicos, through the ages, have attacked speculators as devious manipulators who are the cause of all ills economic. There is nothing new here; it’s the same tired scapegoat rhetoric.

Granted, there are speculative premiums embedded in prices; that is a fact and will not change as long as you have actively traded markets. Sometimes these premiums will be out of line, and those betting the wrong way will be punished by Mr. Market. But over time the real supply/demand dynamics will rule the day. Not speculation. Though I am not a big believer in so-called equilibrium, I do believe prices will trend toward some supply and demand equilibrium over the longer term. It’s true for oil, wheat, corn and every actively traded commodity. It has always been that way. This doesn’t mean markets or market mechanisms are perfect. They are not. And it doesn’t mean market efficiency can’t be improved. It doesn’t mean politically-protected con-artists—read Jon Corzine—should not be thrown in jail forever.

Liquidity.

Down here in Florida we are represented in the Senate by Republican Marco Rubio and Democrat Bill Nelson. Marco is good, but not perfect. Bill isn’t so good. In fact, he recently delivered the government’s preferred approach to crude speculators in an interview with CNN where he promised these recently proposed efforts were not “political”. He then passed around a YouTube link to that interview. Here is the interview with Mr. Nelson if you can sit through it without a barf-bag at your side: http://youtu.be/Rz3kysPnudU

I felt compelled to write him.

To Read The Rest CLICK HERE

Written by Sumit Roy |

April 12, 2012

The natural gas market is facing an unprecedented glut. We examine the latest outlook.

Natural gas prices were little changed today after the Energy Information Administration reported that storage operators injected 8 bcf into storage last week. That was below market expectations that were calling for an injection close to 18 bcf, but excluding a one-time accounting adjustment of 10 bcf, the figure was in line with estimates.

Earlier this week, natural gas plunged below $2/mmbtu for the first time in 10 years, as the unprecedented glut of inventories in the U.S. and Canada weighed on already-depressed prices.

To Read More CLICK HERE

According to the U.S. government, our corn and wheat surpluses are going to be larger-than-expected this year. Normally, that increased supply would lead to a decline in prices. But that’s not happening this time and, in fact, grain prices are acting darned bullish.

Take a look at the iPath DJ-AIG Grains ETN (JJG). The fund tracks a basket of three commodities traded on U.S. exchanges: Soybeans, corn and wheat. As you can see, it recently broke out to the upside, and I think it could shoot up to $55, and perhaps even higher.

One reason for the rally is that other grain suppliers around the world haven’t been as successful as the United States this year. For example, while our winter was warm, one of Russia’s key growing regions was hit so hard with frost that big sections of it may be replanted. Meanwhile, drought is damaging crops in South America and withering fields across Europe.

You also have to take into account the other side of the equation. U.S. supplies may be rising, but so is demand, especially from China. Last year, China replaced Canada as the largest importer of U.S. agricultural products, bringing in $95 billion worth. That was up from just $12 billion in 2001, a year-over-year increase of 30% for a full decade.

China imports a lot of corn and beef from the U.S., but the No. 1 seller is soybeans. Last year, 60% of all U.S. soybean exports went to China and, this year, that number could be even higher.

But it’s not just China. There are now more than 7 billion people in the world, and many of them want to eat more and better food. The United Nations’ Food and Agriculture Organization confirms that food prices are rising, and will continue to rise.

If you combine all these forces, it paints a picture of higher prices going forward. Luckily, that may prove to be a positive development for America. Heck, we’re the Saudi Arabia of grain exporters, so higher prices should help our trade balance.

There are plenty of ways to invest in this sector, in everything from tractor and seed manufacturers to funds that track agricultural commodities and industries. But make sure to do your own due diligence before investing in anything.

Given the amount of rhetoric we’re exposed to these days about U.S. energy independence, you’d think our addiction to foreign oil would be headed downhill — even if only at a snail’s pace.

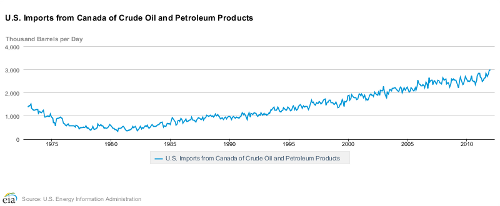

And to a certain extent, our imports have been declining…

According to the EIA, our crude oil imports from OPEC members declined by 358,000 barrels last year compared to 2010.

But there’s one place we keep going for more crude.

Last October, we said our Canadian petroleum imports would soon top three million barrels per day.

It didn’t come as much of a surprise when we hit that benchmark just three months later.

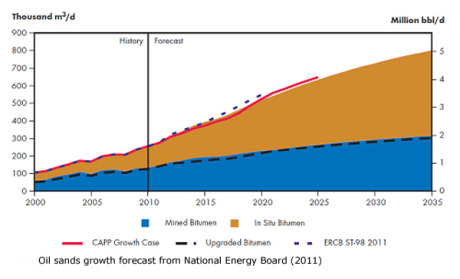

It’s hard not to be bullish on the Canadian oil sands, especially considering it accounts for nearly the country’s total production:

click chart to enlarge

Within the next two decades, that share may be well over 75%.

The only question is how soon it will be until they start shipping us four million barrels per day.

How about five?

Unfortunately, we may be taking our neighbor’s energy for granted, because we’re not the only ones eyeing up Canada’s future barrels…

170 Billion Barrels or Bust

Extracting the 170 billion barrels of bitumen reserves beneath Alberta’s soil seems like an immense task.

I have no doubt you’ve heard the horror stories.

The massive surface mining operations that can be seen from space are enough to keep environmentalists up all night. I’ve seen it firsthand, and it isn’t a particularly pretty sight.

Buy we’re still holding on to my bullish outlook.

Because we realize the future of the oil sands isn’t from the trucks and shovels working day and night to dig up the bitumen.

It’s in extracting the part of the resource that’s too deep for mining.

We’ve mentioned before that about 80% of the bitumen needs to be produced through in-situ methods.

The choice for investors on where to put their money is far simpler than you might think.

They can play both.

How Investors Can Play the Field

Yesterday, Nick Hodge covered a broad spectrum of ETFs and ETNs to help diversify your exposure to the volatility inside the oil and gas industry…

This also holds true in the Canadian oil sands sector.

We’ve already seen the long-term growth expected in the oil sands during the next two decades.

Just some of their top holdings are among the strongest producers in the oil sands patch, including:

-

Suncor Energy

-

Imperial Oil

-

Cenovus Energy

-

Canadian Oil Sands Limited

It’s interesting to note that most U.S. investors don’t realize how close Canada is to adding China to their customer base. That’s a billion new friends willing to buy Canadian crude.

This year, China is expecting to import an average of six million barrels per day.

Now consider how the U.S. government is handling the Keystone XL Pipeline approval process…

Election politics aside, there’s only so much our neighbors to the north will endure.

Canadian Prime Minister Stephen Harper has been making Canada’s position very clear, saying:

Look, I’m a strong believer in the economic importance of our relationship, the security importance, and the importance of the United states and the World. But we cannot take this to the point where we are creating risk and significant economic penalty to the Canadian economy.

Truth is Canadian oil producers are selling their product at a substantial discount to Brent crude.

It’s only a matter of time before they begin to ship their barrels across the Pacific.

And believe me — it’s not just Canadian oil producers that will be taking advantage of the Far East…

Here’s another way to play the burgeoning Chinese-Canadian relationship.

Until next time,

Keith Kohl

@KeithKohl1 on Twitter

@KeithKohl1 on TwitterA true insider in the energy markets, Keith is one of few financial reporters to have visited the Alberta oil sands. His research has helped thousands of investors capitalize from the rapidly changing face of energy. Keith connects with hundreds of thousands of readers as the Managing Editor of Energy & Capital as well as Investment Director of Angel Publishing’s Energy Investor. For years, Keith has been providing in-depth coverage of the Bakken, the Haynesville Shale, and the Marcellus natural gas formations — all ahead of the mainstream media. For more on Keith, go to his editor’spage.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair