By Sumit Roy

The volatile WTI-Brent spread fell to multimonth lows, but surging production in the U.S. makes further narrowing challenging.

The Department of Energy reported this morning that in the week ending April 13, U.S. crude oil inventories increased by 3.9 million barrels, gasoline inventories decreased by 3.7 million barrels, distillate inventories decreased by 2.9 million barrels and total petroleum inventories decreased by 2.2 million barrels.

As expected, Brent prices continued to drift lower over the past week after breaking below the key $121 support level amid economic concerns and receding Iranian tensions. But in an interesting twist, WTI prices actually rose in the period.

BRENT

WTI

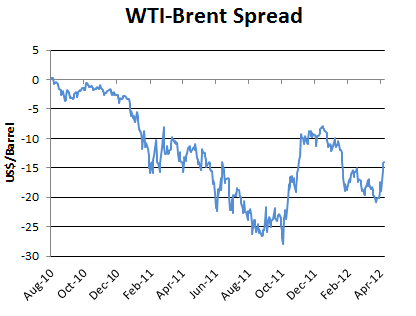

The highly volatile spread between the two benchmarks narrowed to $14 from $17.50 last week and more than $20 at the beginning of the month. That puts it at the smallest level since Feb. 1.

The catalyst for this latest move in the spread was news that the operators of the Seaway Pipeline plan to reverse its flows earlier than expected — at the end of May, rather than June 1. As we’ve written about in the past, the Seaway Pipeline was designed to send crude oil from the Gulf Coast to Cushing, Okla. But surging production in Canada and the U.S. Midwest has created a glut of crude in the region, depressing prices for local benchmarks such as WTI. To reduce the gap between crude such as WTI and global benchmarks such as Brent, transportation capacity out of the Midwest needs to be increased. The reversal of the Seaway Pipeline — after which crude will flow from Cushing to the Gulf Coast — satisfies that need. About 150 Kbbl/d of the pipeline’s capacity is set to be reversed late next month, while another 250 Kbbl/d may be reversed by early 2013. Yet while the reversal of Seaway is a step in the right direction, the market anticipates it alone will not alleviate the Cushing glut completely. Still-wide spreads between WTI and Brent across the futures curve is evidence of that. Rapidly increasing output in the Midwest and Canada necessitates steady increases in transportation capacity. Declining demand across the United States makes the supply and demand balance even more lopsided.

To Read More CLICK HERE