Energy & Commodities

“With summer doldrums well and truly upon us markets have been drifting lower on low volume and trying to hold their May lows. Most metals and certainly gold have performed better and seem to have bottoms in place. As we note in the updates there are three companies on the HRA list that have been getting a lot more attention from traders and several others that are getting traction based on results to com.”.

“Major markets have not been cooperating thanks to debt issues that won’t go away soon. There are plenty

of headwinds still but commodity prices, though lower, are all at levels that makes them hard to pin the

blame on for weak markets.”

“Gold has defended its recent lows well, though not without a couple of scares along the way. Whatever the day to day comments of central bankers, few can see a way out of the current crises that doesn’t involve massive money printing. The US may have the lowest yields but it’s done the least about controlling expenditures so Washington will be printing right along with everyone else. Gold will benefit.”

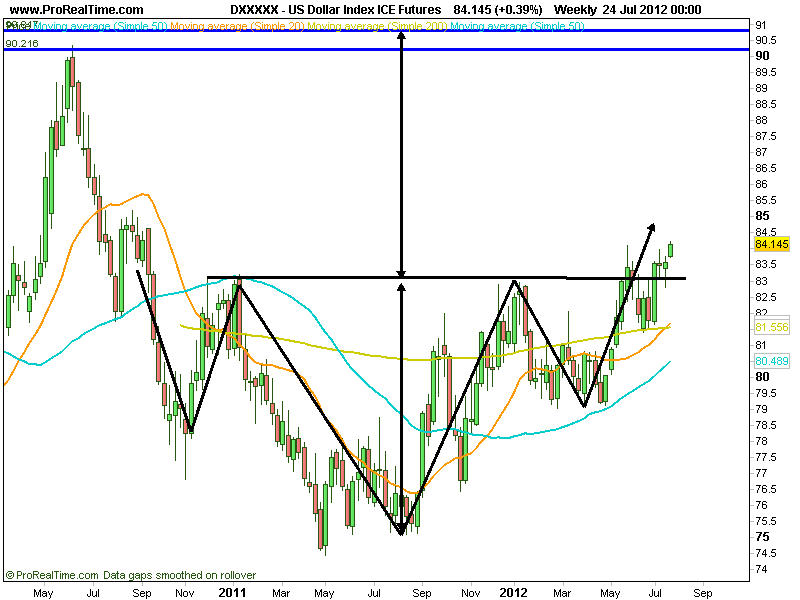

“The Dollar continues to be helped by its safe haven status. Every disappointment out of Europe has

generated upticks in the US Dollar Index which is now trading near a two year high”.

…. read the entire 5 page analysis HERE

US Dollar Chart

It was just about a year ago today when the S&P was sitting at fresh highs and everyone was enjoying a rather upbeat summer. It was a nice summer, the markets were calm, and there was a surreal sense of optimism. Then, in the matter of a few days, things got real ugly, real quickly.

Well, it doesn’t seem like too much has changed since then. We’ve had mixed earnings reports, ever-evolving worries in Europe, and the always looming fiscal mess in the US. Once again, are we in the calm before the storm?

It looks like things in Europe may start to heat up again. Riots turned violent again in Spain as protestors took to the street over austerity measures. With seemingly no resolution, a sinking tourism industry in the PIGS, and a typically hot summer August on its way, all signs point to further turmoil.

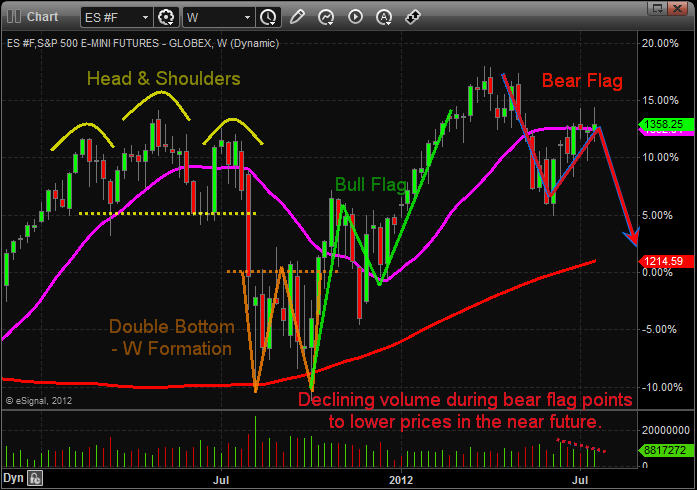

Technically, we’re currently seeing a number of bearish indicators setting up in the S&P and other markets. First, on the weekly chart of the S&P 500 Futures we can see what appears to be a bear flag formation developing. Note the recent rise in price since the beginning of June on decreasing volume.

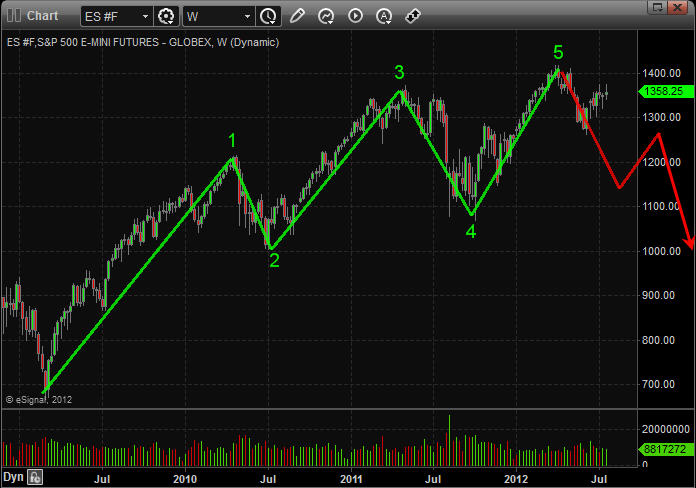

A second look at the S&P daily illustrates two intermediate time frames that are currently pointing down.

- Completion of two intermediate cycles within longer term five wave pattern

- Downwards wave one from April until beginning of June followed by wave two correction from June until present.

A look at the longer term view using the weekly chart again supports our argument for a major correction. We have just completed a five wave pattern since the 2009 lows, and it is looking more like a big pull back is due. Remember most major trends end after the fifth wave.

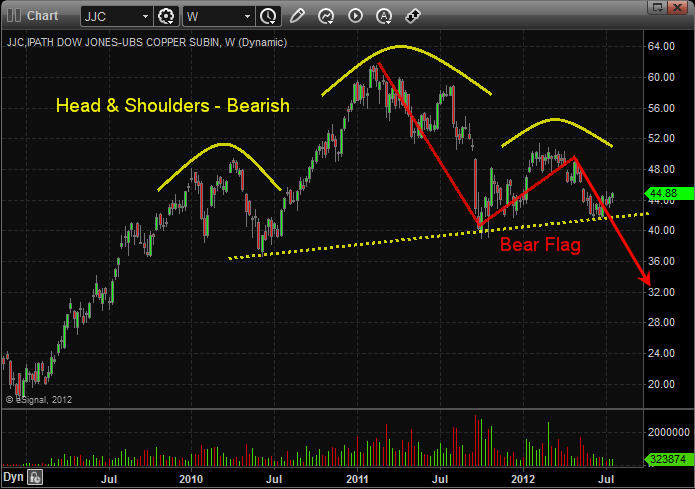

If we take a look at the copper ETF, “JJC”, we are provided with further justification. Copper is often referred to as “Dr.Copper” due to its industrial application and is known to be a leading indicator for equity markets. Copper has significantly underperformed equity markets and is likely leading the next move down. A look at the weekly chart which points to a rather dismal outlook. There is a major head and shoulder patterns developing.

Last summer turned into a bloodbath with nothing but red candlesticks taking stocks and commodities sharply lower. If you haven’t already, it’s time to lock in some profits. Short, intermediate, and long term cycles are pointing down, and the increasingly bearish technical developments cannot be ignored. We’ll be looking at entering multiple shorts potentially in the very near future once/if setups present themselves. Buckle up and stay tune for more…

Stay in the loop by joining my free weekly newsletter and weekly video to stay ahead of the crowd:www.TheGoldAndOilGuy.com

Pundits may have closed the book on the so-called nuclear renaissance, but the story is far from over. In this exclusive interview with The Energy Report, Gold Stock Trades Editor Jeb Handwerger names the “sleeping beauties” quietly proving their worth. A new generation of nuclear energy must be part of a diversified happy ending, Handwerger says, but by that time, merger and acquisition activity may have already rewarded the investors who believed in a brighter future.

OMPANIES MENTIONED: AREVA – ATHABASCA URANIUM INC. – BABCOCK & WILCOX CO. – BHP BILLITON LTD. – CAMECO CORP. – DENISON MINES CORP. – EUROPEAN URANIUM RESOURCES LTD. – EXELON CORP. – FISSION ENERGY CORP. – FLUOR CORP. – GENERAL ELECTRIC CO. – RIO TINTO PLC – THE SHAW GROUP INC. – U3O8 CORP. – UEX CORP. –UR-ENERGY INC. – URANERZ ENERGY CORP. –URANIUM ENERGY CORP. – URANIUM ONE INC.

The Energy Report: Jeb, at the turn of 2012 you were bullish on junior uranium mining stocks. It’s halfway through the year and a lot of these stocks have still underperformed. Is this the result of continued economic fallout after the Fukushima nuclear disaster, or perhaps a consequence of the availability of cheap natural gas?

Jeb Handwerger: We had a really difficult year for uranium equities in the aftermath of both Fukushima and the end of QE2. The whole resource sector went, and uranium was hit extra hard. Cameco Corp. (CCO:TSX; CCJ:NYSE) and Uranium One Inc. (UUU:TSX) declined more than 50%.

However, we are beginning to see a notable improvement in the supply-and-demand fundamentals with more institutional investor interest in uranium. Year-to-date, Cameco is up close to 21%, making a higher low than in late 2011 and holding the 200-day moving average. It seems that the bottom we predicted in uranium miners in late 2011 is still holding. Compare that to the gold miners’ ETF (GDX:NYSE), which is down 17% and to the rare earths ETF (REMX), which is down about 12%. The uranium ETF is down only 10%. That shows me that uranium miners are relatively strong in a weak, panic-driven natural resource market where investors are hoarding cash and treasuries.

TER: So what’s breathing life into the uranium sector now?

JH: In 2011, nuclear energy had a lot of competitors from alternative energy sources such as solar, wind and natural gas. Since then, the challenges for each of these sources have become more apparent and the entire energy sector has undergone an outright selloff. A lot of articles have talked about cheap natural gas taking the place of nuclear. What the pundits don’t say is that natural gas has plenty of its own issues, ranging from the environmental downsides of hydraulic fracturing to greenhouse gas emissions. Furthermore, service stations and natural gas liquefaction plants must be set up along the chain of supply from mine to consumer. Major costs are involved and there is no assurance that the price of natural gas will remain at these low levels. Plus, some parts of the world don’t have abundant natural gas. The cost of liquefying it and shipping it can be extravagant. Japan, for instance, tried importing natural gas, but eventually gave up and recently reactivated nuclear plants amid growing fears of power outages affecting industry.

The short position in nuclear miners has increased even as money is being directed toward construction of new nuclear power plants globally. The shorts use the stories of cheap natural gas to depress the uranium sector. This means uranium miners may even have additional upside because of the large short position that may soon have to run for cover in the event of a turnaround. We have seen short covering rallies before in the uranium miners. In the summer of 2010, after QE2 was announced, the sector experienced major gains. The same was true in 2007/2008 before the credit crisis. We saw a huge exponential move. These moves came out of nowhere and were very powerful, with miners moving up 10–20% a day.

We must not tar nuclear energy with the broad brush of the entire resource sector malaise. Construction of new nuclear plants proceeds steadily and the media is not emphasizing that. The U.S., for the first time in three decades, announced the approval of plans for nuclear reactors in Georgia and South Carolina. Even Japan is reactivating nuclear reactors. India and China are moving full speed ahead, and this alone will require an additional 40 million pounds (40 Mlb) of uranium annually by the end of this decade. We must remember that the underperformance right now in junior uranium miners is transient. Nuclear power is here to stay. All energy sources have their own sets of cost and environmental issues. No one source can fulfill everyone’s needs for the next 30 years. Nuclear will always be part of the long-term energy mix, and when the market turns, long-term uranium investors have the potential to experience exponential profits.

TER: Japan’s Fukushima Nuclear Accident Independent Investigation Commission published its report on the 2011 accident. It largely blamed the Tokyo Electric Power Co. operators for administration and operational failures. What did these findings mean for the future of nuclear power in Japan and around the world?

JH: Many countries are still stuck with the old, 40-year-old nuclear reactors, which is what Fukushima was. A renaissance has since occurred in nuclear engineering. The next generation of reactors has a fraction of the risks involved with the old reactors. That is what is being built in China, India and Russia. Even Saudi Arabia has 16 plants under serious consideration. Four are in the works in the United States.

TER: Given that more than 500 new reactors are in some phase of the building pipeline right now, how attractive are investments in the engineering and contracting firms that design and build reactors?

JH: Investors are looking into the companies that build the reactors. The Shaw Group Inc. (SHAW:NYSE) is building the South Carolina reactors. Babcock & Wilcox Co. (BWC:NYSE) used to build nuclear submarines, but has also moved into small modular nuclear reactors. Fluor Corp. (FLR:NYSE) and General Electric Co. (GE:NYSE) are other names with exposure to nuclear power. One can also look at utilities like Exelon Corp. (EXC:NYSE) who are major players in nuclear power generation in the United States.

TER: If this is where the increased demand for uranium will come from, what about the supply? The large producers will probably deliver, but will the explorers eventually benefit as they find the fuel for the future? From an investment point of view, what is the best way to capitalize on this coming trend? Is it through the big companies or the juniors?

JH: To answer that, I think we need to take a look at what happened in 2011. One of the biggest deals was that Hathor Exploration, which owned the Roughrider deposit up in the Athabasca Basin, was bought up for multiples by the giant Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK). Rio Tinto’s stock price did not move nearly as much as Hathor’s price. Hathor received over $11/lb uranium. If you are looking to leverage the sector, a good way to play it might be to find a suitable candidate for the major uranium miners, many of which are trading at one-tenth of that value right now. Cameco and Rio Tinto have expressed ongoing interest in further acquisitions of juniors. That is why we are specifically looking at areas that are in mining-friendly jurisdictions where the majors are going to be looking to develop economic resources. The undervaluation of quality uranium miners is creating a possible once-in-a-lifetime buying opportunity.

TER: Do you see other buying opportunities in the Athabasca Basin?

JH: Following the Hathor buyout, we expect even more consolidation in the Athabasca Basin. When a company that large sinks $650 million into an area, we don’t think that’s the end. It is just the beginning. Rio Tinto will want to build resources and consolidate its position. We also think Cameco and possibly BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) is going to try to build a larger position in the basin. Target candidates include Denison Mines Corp. (DML:TSX; DNN:NYSE.A). It has the Wheeler River deposit, which is one of the best undeveloped projects in the basin. UEX Corp. (UEX:TSX) has a large resource base in the basin and is already 22% owned by Cameco. Fission Energy Corp. (FIS:TSX.V; FSSIF:OTCQX) has the J Zone, which is pretty much a continuation of the Roughrider deposit.

Athabasca Uranium Inc. (UAX:TSX.V; ATURF:OTCQX) is an early-stage company in the area, but it has some great prospects at Keefe Lake. Athabasca has an interesting team with Dr. Zoltan Hajnal from the University of Saskatchewan, who is an expert at using seismic data for uranium exploration. He did this successfully for Hathor. He is a world-class seismic expert and he has joined Athabasca’s advisory board, along with Kim Goheen, who recently retired as CFO for Cameco. The company also came out with spring drilling program results that showed some very promising early-stage success using that seismic data. The second half of 2012/2013 may be interesting.

TER: Could Athabasca Uranium or any of these be standalone projects, or are they mainly acquisitions targets?

JH: In time, there won’t be many juniors in the Athabasca Basin. The high-quality ones will be a part of Rio Tinto or Cameco. The same thing will happen in the U.S., where we follow three juniors who are currently very active. Uranium Energy Corp. (UEC:NYSE.A), Ur-Energy Inc. (URE:TSX; URG:NYSE.A) and Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.A) are going to be U.S. producers who are part of the solution to the U.S. supply crisis. Just under 20% of U.S power comes from nuclear reactors, however more than 95% of the uranium is imported. The U.S. used to be one of the largest uranium exporters. Now it produces less than 4 Mlb of uranium.

As part of a plan to meet that demand, in the near term Uranerz, could be a takeover target for Cameco or Uranium One. It already has a processing agreement with Cameco and an off-take agreement with Exelon Corp. Uranerz has an incredible land package right between the two majors in the Powder River Basin, which has been producing uranium for five decades. The company employs in-situ mining, which also has many benefits over conventional mining when it comes to environmental issues and costs.

TER: How soon might a takeover happen? Is there some catalyst in the wings?

JH: You just never know when it’s going to happen, although I do know it will be sooner rather than later. I think as we get closer to 2013 there’s going to be more pressure. Over the next 6-18 months a huge amount of consolidation could come to the industry.

TER: Has the market already priced in these takeovers?

JH: No, no, no. Uranerz is trading near three-year lows. Investors have a chance to get into these companies on historic lows.

In South America, a company I like is U3O8 Corp. (UWE:TSX.V; OTCQX:UWEFF) in Colombia, Guyana and Argentina. The main project is Berlin in Colombia. The company has shown incredible resource growth during the past year. It has increased the Indicated and Inferred resource sevenfold, from 7.1 Mlb to 47.6 Mlb, and it has only documented the three southern kilometers (km) of a 10.5 km mineralized trend. The Berlin deposit is also home to phosphate and vanadium and has shown some very positive metallurgical recoveries. U3O8 is rapidly growing and derisking its resources in South American countries that are mining friendly. I understand the company will be completing a PEA in the second half of 2012. The company thinks it can potentially grow this asset in the near term to 40–50 Mlb uranium.

U308 already has a strong cash position with institutional support. What is really interesting is that the phosphate, vanadium and rare earths may pay the way with the uranium as pure profit. That is what we are looking for in the second half of the year from this company.

TER: U308 Corp is trading at $0.33 right now. How much could it go up from there?

JH: Right now, U3O8 is priced at about $0.77/lb uranium; Hathor was bought out for $11/lb and Mantra for $10/lb. That is almost a potential tenfold increase. As the project is derisked in the second half of the year, the stock should get to at least a comparable value to some of its current competitors, at over $1/lb.

TER: Are you looking at any uranium companies in Europe?

JH: Yes. We have one that we really like in Slovakia called European Uranium Resources Ltd. (EUU:TSX.V; TGP:FSE). First of all, it has a great management team. Plus, Europe is the largest user of nuclear power per capita. There is only one operating uranium mine in Slovakia at the moment and that is rapidly depleting. European Uranium Resources is really Europe’s next answer for uranium production. The deposit may be one of the lowest-cost uranium mines in the world. The prefeasibility study is very impressive from an environmental and economic perspective. The real momentous catalyst is if the company can sign an off-take agreement with the Slovakian government, with a surplus going to other EU nations.

AREVA (AREVA:EPA), the third-largest uranium producer in the world, already took a 10% position at approximately $0.35 a share and is on the European Uranium board giving technical expertise. The company is now trading at three-year lows of $0.22 per share. This may be a real undervalued situation in Europe.

Overall, Europe and the Americas are much better mining pictures than Africa and Australia right now. Rising resource nationalism in Africa and rising costs in Australia make these other stories much more attractive.

TER: So, is the overarching story mergers and acquisitions?

JH: I think so. There is going to be a dramatic change of landscape in the uranium sector. As the high-quality juniors come closer to production, they’ll be taken over by the majors. We saw the beginnings of that in 2011 and we will see it continue. One needs patience and fortitude and the ability to go against the consensus.

TER: Thank you for your time and your insights, Jeb.

JH: Thank you.

Gold Stock Trades Editor Jeb Handwerger is a stock analyst and best-selling writer who’s syndicated internationally and known throughout the financial industry for accurate, in depth and timely analysis of the general markets, particularly as they relate to the rare earths, precious metals and, nuclear sectors. He studied engineering and mathematics and received his undergraduate degree from University of Buffalo and a masters degree from Nova Southeastern the University in Fort Lauderdale. Teaching technical analysis to professionals in South Florida for some seven years, Handwerger began a daily newsletter that grew to become Gold Stock Trades: Mining for Winners in Any Market, with thousands of readers from more than 40 nations who are interested in the North American resource markets. Click here to subscribe to his free newsletter.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

One of the biggest stories in the media over the past week or so has been the tremendous drought affecting the nation’s Corn Belt. The spike in crop prices has been dramatic …

Corn has rallied more than 50 percent since mid-June as the condition and size of the crop is consistently downgraded.

Drought conditions are some of the worst in nearly twenty years. And it’s a sharp reversal from just two months ago when it was generally expected that the corn crop would be a “bumper crop.”

Just last week, the USDA reduced the expected corn production this summer by 1.8 billion bushels, and reduced the per acre crop yield to 146 bushels/acre this month, from 166 last month.

Trading corn in this market is a risky venture because at the first sight of rain the contract will fall hard, but there’s no telling how high it can go before that happens. Moreover, higher grain prices can impact other sectors in the market, too.

Normally, when grain prices are this high it’s bullish for agricultural equipment manufacturers like John Deere (DE). The general thinking is that farmers, with a lot more money in their pockets from the higher prices, will buy new tractors, plow new fields, and upgrade old equipment. But what we’re seeing now isn’t a typical price rise in the grains …

Prices are rising because the general thought is that the crop will be much smaller than anticipated. So while farmers who are lucky enough to have their corn survive will receive a better price, many more farmers will simply have no crop to sell. As a result, we have to be cautious about investing the same old way.

Taking the Contrarian Approach …

As I think about the potential effects of this drought and the investment opportunities, there is one sector in agriculture that will likely benefit — seeds.

Farmers are not simply going to let their crops fail without trying to get something out of the ground. Consequently, a lot of them will replant certain fields in soybeans or other crops where corn might have failed. In fact, I’ve read multiple reports of farmers already replanting soybeans where they had just planted corn, in an effort to have something to bring to market at harvest time.

The point is that we can expect increased demand for seeds as we enter the later parts of the summer, and to a lesser extent see an increased demand for fertilizer as well.

In particular, there should be a higher spot demand for drought resistant seeds made by companies like Monsanto (MON).

However, if you prefer the diversification of an exchange traded fund, you might consider the Market Vectors Agribusiness ETF (MOO). It holds some of the largest seed and fertilizer companies in the world, companies that should benefit from additional demand as unlucky farmers try to salvage what they can from a difficult growing season.

As contrarian investors we must always look at an event in the market from multiple angles, and look beyond the typical response. Higher grain prices due to a drought are not a blanket “good thing” for all agricultural companies. But savvy contrarian investors who look deeper can identify the sectors that do stand to profit.

Best,

Tom

Source:http://www.moneyandmarkets.com

About Money and Markets

For more information and archived issues, visit http://www.moneyandmarkets.com

Money and Markets is a free daily investment newsletter published by Weiss Research, Inc. This publication does not provide individual, customized investment or trading advice. All information is based upon data whose accuracy is deemed reliable, but not guaranteed. Performance returns cited are derived from our best estimates, but hypothetical as we do not track actual prices of customer purchases and sales. We cannot guarantee the accuracy of third party advertisements or sponsors, and these ads do not necessarily express the viewpoints of Money and Markets or its editors. For more information, see our //www.gliq.com/cgi-

Consider this chart of crude oil. It’s one of the ugliest charts I’ve seen in a while.

While oil is trying hard to hold the $80 level, it will soon fail to do so. Instead, a shocking decline lies ahead for oil, one that will see it plunge to below $60 a barrel.

Keep your eyes on the $77.33 level. Once that gives way, oil will spin a lot of heads as it tumbles hard. Only a weekly closing above $92.87 would turn the immediate trend around for oil.

As for U.S. stocks, don’t expect much upside there either. While the broader U.S. stock markets are in a new long-term bull market, they remain vulnerable to the downside in the short term.

There’s simply too much global uncertainty right now, and I see the Dow falling to at least 11,500 and possibly 10,500 — before any sustainable rally develops.

My view:

- Continue to keep most of your liquid funds in cash, ready to be deployed on a moment’s notice, but as safe as can be right now. The best way: A short-term Treasury-only fund in the U.S., or equivalent.

- Despite gold’s weakness, hold on to all long-term gold holdings. You do not want to let go of those. Long term, gold is heading to well over $5,000 an ounce. Short term, gold is heading lower. Consider inverse gold ETFs, such as the ProShares UltraShort Gold (GLL), to hedge your long-term holdings.

- Consider prudent speculative positions to grow your wealth. Like those I have recommended in myReal Wealth Report, which are doing great right now as silver falls, as the euro struggles, and more.

Most of all, don’t let the pundits on Wall Street kid you. The Fed will not prop up the markets for the elections … Europe will not be able to solve its sovereign-debt crisis … corporate earnings have seen their best for the current cycle … and there are more dangers to your wealth right now than there have been in the recent past, since at least 2008.

So stay cautious, but ready to pounce on new opportunities as they unfold.

Best wishes,

Larry

P.S. My Real Wealth Report subscribers have side-stepped the crash in gold and silver mining shares … have hedged up most of their gold holdings from much-higher levels … and they are also enjoying pretty nifty gains in their speculative positions, including inverse ETFs on silver and the euro.

Wouldn’t you like to join them? All you have to do is click here to start your risk-free Real Wealth Report trial today!

About Uncommon Wisdom

For more information and archived issues, visit http://www.uncommonwisdomdaily.com/

Uncommon Wisdom (UWD) is a free daily investment newsletter published by Weiss Research, Inc. This publication does not provide individual, customized investment or trading advice. All information is based upon data whose accuracy is deemed reliable, but not guaranteed. Performance returns cited are derived from our best estimates, but hypothetical as we do not track actual prices of customer purchases and sales. We cannot guarantee the accuracy of third party advertisements or sponsors, and these ads do not necessarily express the viewpoints of Uncommon Wisdom or its editors. For more information, see our Terms and Conditions. View our Privacy Policy. Would you like to unsubscribe from our mailing list? To make sure you don’t miss our urgent updates, just follow these simple steps to add Weiss Research to your address book.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair