Economic Outlook

Michael “Mish” Shedlock of Global Economic Trend Analysis, explains why Canada, the US’s largest trading partner, is now in recession and how the US is likely to follow as well. He talks about the recent string of poor economic numbers, why he’s been out of the market, and the next trigger for a possible market collapse.

Michael “Mish” Shedlock of Global Economic Trend Analysis, explains why Canada, the US’s largest trading partner, is now in recession and how the US is likely to follow as well. He talks about the recent string of poor economic numbers, why he’s been out of the market, and the next trigger for a possible market collapse.

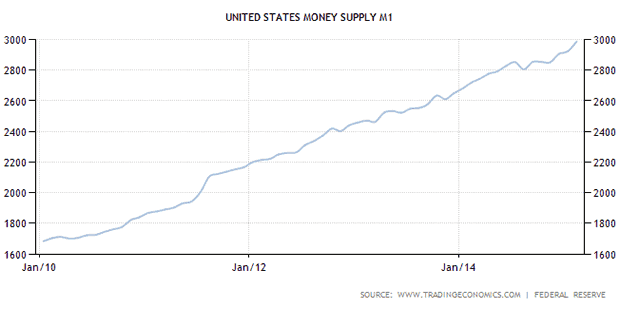

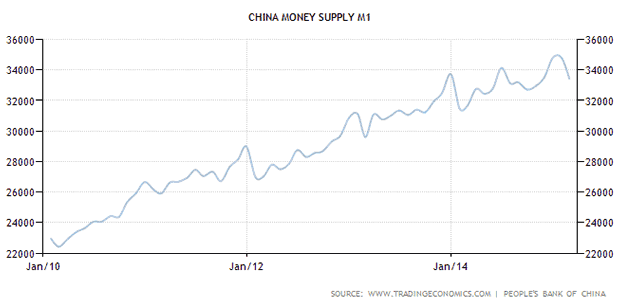

That stats just keep getting stranger and, if you’re a policymaker or an investor, scarier. According to a (now widely publicized) McKinsey & Co study, instead of deleveraging after the debt-induced crisis of 2008-2009, the world borrowed another $57 trillion. And most of the advanced economies ran their monetary printing presses flat-out. The next couple of charts show what the US and China, for instance, have been up to since 2010:

Now, conventional economic theory says that double-digit growth in debt and money creation should produce a boom, and that today our biggest problem should be too many people getting big raises at work. Yet that’s not the case at all:

Weak Japan business confidence highlights recovery doubts

(Daily Mail) — Doubts about a rebound in Japan’s economy are rippling through boardrooms across the country, a key central bank survey suggested Wednesday, as efforts to revive growth falter. The Bank of Japan’s closely watched Tankan report showed confidence among big manufacturers stood at plus 12 in March, flat from the previous survey and missing expectations that the level would come in at 14.

While sentiment among non-manufacturers was more upbeat, they pared profit expectations while Japan’s increasingly pessimistic corporate titans trim their spending plans.

The survey of more than 10,000 companies — which shows the difference between the percentage of firms that are optimistic and those that see conditions as unfavourable — is the most comprehensive indicator of how Japan Inc. is faring.

“A weak yen and lower oil prices has provided some support (to the economy) but the Tankan showed that firms, particularly manufacturers, are now acutely aware that overseas demand is softening,” SMBC Nikko Securities said in a report.

The tepid survey comes days after separate data showed output from Japanese factories shrank by a worse-than-expected 3.4 percent in February, while inflation stalled as a key measure of prices was flat for the first time in nearly two years. “Japanese companies aren’t convinced the economy is going to get stronger,” said Atsushi Takeda, an economist at Itochu Corp. “Without an improvement in business confidence, it’s hard to imagine Japan will achieve a full-fledged recovery.”

Chinese government admits that things aren’t going so well

(Business Insider) — A high-level Chinese official on Sunday made the government’s first admission that the country’s economic slowdown was not going as planned. China’s top banker, Zhou Xiaochuan, told a meeting of regional leaders that his country’s growth rate had tumbled “a bit too much.”

“China’s inflation is also declining, so we need to be vigilant to see if the disinflation trend will continue, and if deflation will happen or not,” said Zhou, governor of the People’s Bank of China. His remarks were made at the Boao Forum for Asia, an annual conference on the island of Hainan in southern China.

For many, the way he described China’s health was no surprise. The country’s economy has not been growing this slowly since the 1990s. Debt-laden corporations are seeing sickly profit margins. Banks are carrying loads of debt, too, and the housing market is slowing. China’s official 2015 GDP growth target is 7%, but that seems shaky.

U.S. job growth brakes sharply, clouds Fed rate hike timing

(Reuters) — U.S. employers added the fewest number of jobs in more than a year in March, the latest sign of weakness in the economy and one likely to further delay an anticipated interest rate increase by the Federal Reserve.

Nonfarm payrolls rose 126,000 last month, less than half February’s pace and the smallest gain since December 2013, the Labor Department said on Friday.

The weakness was concentrated in the goods-producing sector, which has been hurt by a strong dollar and lower crude oil prices. Leisure and hospitality also saw a sharp slowdown in jobs growth, suggesting harsh winter weather could have dragged on hiring.

While the jobless rate held at a more than 6-1/2-year low of 5.5 percent, the workforce shrank. The labor force participation rate returned to a more than 36-year low reached late last year.

“The report confirms the emerging narrative of slowing growth momentum seen in the other economic indicators. It will weaken the argument for a mid-year (rate) hike,” said Millan Mulraine, deputy chief economist at TD Securities in New York.

The tepid increase in payrolls ended 12 straight months of job gains above 200,000 – the longest streak since 1994. In addition, data for January and February were revised to show 69,000 fewer jobs created than previously reported, giving the report an even weaker tone.

After its robust stretch, the jobs figures now appear more in line with other signals from consumer spending to housing starts and manufacturing that have suggested the economy grew at a sub-1 percent annual rate in the first quarter. Economists had forecast that payrolls would rise 245,000 last month.

So is anybody out there doing okay? Well, yes, sort of. In relative terms at least, Europe is suddenly a bit of a success story:

Eurozone Q4 Growth Reflects Broad-Based Recovery

(RT) — The Eurozone economy expanded as initially estimated in the fourth quarter on broad-based support from spending, investment and exports.

Gross domestic product grew 0.3 percent sequentially, slightly faster than the third quarter’s 0.2 percent expansion, second estimates from Eurostat showed Friday. The statistical office confirmed the estimate released on February 13.

All components on the expenditure side of GDP expanded in the fourth quarter. While the growth in household spending moderated to 0.4 percent from 0.5 percent, government spending growth remained unchanged at 0.2 percent.

Investment increased by 0.4 percent, after staying flat a quarter ago. At the same time, growth in exports eased to 0.8 percent from 1.5 percent and that in imports to 0.4 percent from 1.7 percent.

Year-on-year, the economy expanded 0.9 percent as estimated, which was marginally above the 0.8 percent growth posted in the third quarter. Over the whole year of 2014, the 19-nation currency bloc expanded 0.9 percent versus a 0.5 percent contraction in 2013.

What lessons are we supposed to draw from this? One would be that if you borrow too much money it’s hard to generate growth by borrowing even more. Austrian economics, still the only branch of the discipline that pays attention to debt levels, holds that a boom has to be followed by a deleveraging in order to wipe the slate clean. You literally can’t have a boom without a bust.

Another lesson is that currency devaluation works, at least in the short run. Here’s the euro versus the dollar over the past year:

It’s down by nearly a third and by lesser but still considerable amounts versus the yen and yuan. And low and behold, the eurozone is doing better than its trading partners. This is what the currency war script says should happen, and leads to an obvious conclusion: If the other big economies are going to avoid dropping into a unique kind of recession — one in which interest rates start out at historically low levels — then they’ll have to fight back with devaluations of their own. Either Japan has to cheapen the yen some more (it has already devalued versus the dollar in the past year) and China has to break its link to the dollar and let the yuan fall, or the US has to stop talking about raising rates, get serious about growth and do something to bring down all the non-euro currencies simultaneously. Otherwise, today’s bad numbers will turn into tomorrow’s catastrophic ones.

But of course while all this is going on debt will keep rising and leverage will become even more extreme. The deleveraging, when it comes, will be epic.

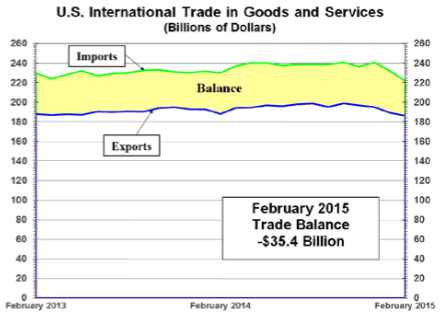

Trade Deficit Shrinks

Inquiring minds are investigating the Commerce Department report on International Trade in Goods and Services for February 2015, for clues about first quarter GDP.

Highlights

- Exports were $186.2 billion, down $3.0 billion from January.

- Imports were $221.7 billion, down $10.2 billion from January.

- Year-to-date, the goods and services deficit decreased $ 2.6 billion, or 3.2 percent, from the same period in 2014.

- Year-to-date exports decreased $5.3 billion or 1.4 percent.

- Year-to-date imports decreased $7.9 billion or 1.7 percent.

Balance of Trade

GDP Analysis

Recall that exports add to GDP and imports subtract from GDP. Thus my first reaction to the report was that

GDP estimates would go up. They did, but very slightly.

Atlanta Fed GDPNow Model

Yesterday, following an Unexpected Decline in Construction activity, the Atlanta Fed GDPNowforecast dipped to 0.0%.

Today following the shrinkage in the trade deficit, the forecast is back in positive territory at 0.1%.

“The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2015 was 0.1 percent on April 2, up from 0.0 percent on April 1. Following this morning’s international trade release from the U.S. Census Bureau, the nowcast for the change in real net exports in 2009 dollars increased from -40 billion to -33 billion. The nowcast for real equipment investment growth declined from 7.5 percent to 6.1 percent following the international trade report and the Census Bureau’s M3 manufacturing report.“

GDPNow Estimate for 1st Quarter

Another Sign of Slowing Global Economy

The declining trade deficit is a good thing. However, the shrinking trade deficit is not as positive as it may look at first glance.

It would have been far better had the trade deficit shrinkage been on rising exports. Instead, imports and exports are both down. That is yet another sign of the slowing global economy.

Back in January, I forecast declining exports on the strength of the US dollar. Here we are. If oil ticks back up for any reason, so will imports.

There is not a lot to cheer about in today’s reports (Also see Factory Orders Unexpectedly Rise Snapping String of 6 Straight Declines.)

Under the recent information deluge, we haven’t had the time to analyze a very interesting and disturbing trend. The U.S. business inventory to sales ratio has been rising for months. What does it mean for the American economy and the gold market?

According to the Monthly Wholesales Report, inventories were up 6.2 percent in January from a year ago and 0.3 percent from December. Coupled with weak sales data (sales fell by 3.1 percent from December 2014 and 1 percent from January 2014), the inventory to sales ratio increased to 1.35 in January from 1.33 in December 2014. It means that it would take 1.35 months for businesses to clear shelves, the highest inventory-to-sales ratio since July 2009.

Why is data on business inventories so important? The answer is that the changes in the inventory to sales ratio indicate any supply or demand imbalances in the economy. Inventories rise when supply is greater than demand. Inventories rising relative to sales mean that sales fail to meet demand projections. Thus, the inventory to sales ratio usually reaches its cyclical peak in the middle of the recession, when the economy is slowing down. Indeed, please note three things.

First, that inventories of durable goods jumped the most – by 7.7 percent from year ago, which is generally in line with weak data on news orders for durable goods. Second, contrary to the historical declining trend (due to improved inventory management), we are witnessing a gradual rise since 2013 and particularly since the summer of 2014. Actually, the inventory to sales ratio has reached the highest level since the Great Recession (see the chart below). Third, inventories are rising despite low prices. Thus, this indicates week global demand.

The consequences may be significant. The high levels of inventories could make entrepreneurs very

uncomfortable with adding more stocks. Thus, they will probably try to reduce their orders to get inventories in line. However, those orders are the suppliers’ sales. It means that reducing stocks and cutting orders may trigger a spiraling decline in sales and a recession. After Lehman, businesses reduced orders so aggressively that the supply chain seized, sales went down and inventories soared.

To sum up, inventories should not look only at the Fed’s actions and speeches, but also analyze fundamental data. The inventory to sales ratio is of utmost importance, since it shows the supply/demand imbalances. The rising ratio indicates that the U.S. economy is slowing down due to weak demand. The report on U.S. durable goods orders is good news for gold prices, because the possible recession could boost safe-haven demand for gold and change the Fed’s monetary policy stance to even more dovish.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor originally sent to subscribers on March 30, 2015, 7:00 AM.

ET Now: Do you think financial markets are very naive in the way they are reacting? The world is fighting for deflation, but despite a global growth scare, most of the major markets are sitting at a record high, be it DAX, the Nikkei or the NASDAQ.

Marc Faber : Yes. There is decoupling between economic activity and asset markets. If you look at the economies globally, we know that in Europe there is hardly any growth. Can Europe, relative to its poor performance of the last few years, grow this year by 1-1.5%? It is possible, but we understand GDP is not a very relevant measure of economic well-being. In the US, the latest statistics are rather disappointing and in China, we have meaningful slowdown as well as in all resource producers of the world.

Marc Faber : Yes. There is decoupling between economic activity and asset markets. If you look at the economies globally, we know that in Europe there is hardly any growth. Can Europe, relative to its poor performance of the last few years, grow this year by 1-1.5%? It is possible, but we understand GDP is not a very relevant measure of economic well-being. In the US, the latest statistics are rather disappointing and in China, we have meaningful slowdown as well as in all resource producers of the world.

John Anderson, my friend who is a very good economist and also has his own consulting firm, calculated that the GDP figures in India are actually overstating economic growth significantly. It does not mean that he is bearish about the Indian financial assets. I am also positive essentially about the Indian assets, but growth is not what the government is publishing.

– in Economic Times of India

….more from Marc Faber:

Marc Faber: Indian Stocks can correct by 20%

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair