Economic Outlook

It’s the same story every time: Imbalances build up during a recovery but most investors ignore them because good times have become the new normal and the uptrend seems bullet-proof. Then things fall apart and everyone wishes they’d paid attention to history.

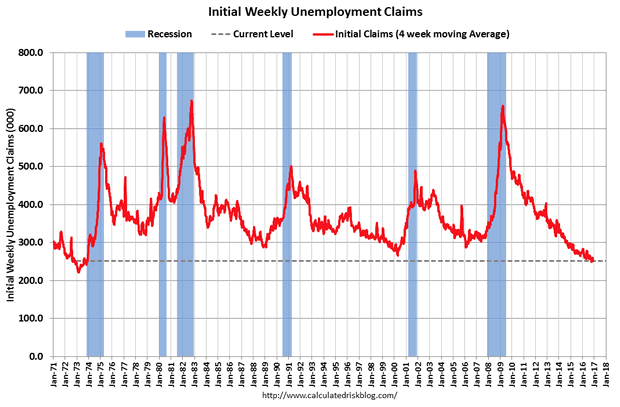

This series will cover a few of the more glaring examples of late-cycle myopia, beginning with jobless claims, i.e., the number of people joining the ranks of the unemployed.

In hard times when layoffs are widespread and new jobs scarce, this number spikes. In better times, when jobs are plentiful and employers are desperate to keep good people, the number falls.

But when it falls past a certain point wages start rising at a rate that leads (through market forces and/or Federal Reserve actions) to rising inflation and higher interest rates, which are destabilizing and generally cause a recession.

So let’s see what this stat says about our place in the current business cycle:

It certainly looks like we’re back in 1999 or 2007, with a tightening labor market at the tail end of a long recovery. If so, interest rates should be rising. And they are:

On the surface, at least, the US seems to be following the standard script: A few years of recovery, followed by a tightening labor market followed by rising interest rates. Followed by a recession that works off the imbalances built up during the expansion.

But the interesting part of the process is always the (many and seemingly quite reasonable) reasons why it’s different this time and the old rules no longer apply. The latest batch includes the following:

1) The terrible quality of the new jobs being created. Where in past recoveries people who were initially laid off tended to eventually regain their old jobs or something similar, in this recovery the new jobs are mostly in service industries (read bar-tending and waitressing) that are no one’s idea of career-track. So there’s room for a few more years of growth to get those people back into their old high-paying spots before wage inflation really gets going.

2) The incoming administration is proposing a big increase in government spending and tax cutting, paid for with borrowed money. This is stimulative and should turbocharge growth, which in turn should boost corporate profits, making stocks a lot more attractive.

3) The next stage of monetary policy experimentation seems to involve central banks buying equities more or less indiscriminately with newly created currency. The Bank of Japan, for instance, now owns about half of that country’s equity ETFs, thus providing a huge boost to the Japanese stock market. Let the Fed decide to join this party and it’s anyone’s guess how high blue chip stocks can climb.

When laid out this way, these do sound like compelling reasons for optimism. And maybe they are. But remember, every single expansion in the past century came with equally-strong arguments for ignoring traditional limits. And every one of them turned out to be illusory.

….also from Martin Armstrong: The Cycle of Assassination & War Bottomed in 2014

I’m afraid the Trump train is headed for a sharp economic curve that takes the US further away from free-market capitalism. The US already pulled out of the free-market station a long time ago, but Trumponomics moves deeply into a “mixed economy,” an economy in which government funding and private funding are married. The bankster-baron confederation in the Trump cabinet is where business and government consumate their marriage.

My pervious article about Trump’s cabinet lineup demonstrated a major economic shift forming in the presidential cabinet. This article explains what that shift means.

How Trumponomics may radically change the US economy

In Trumponomics, this is worked out by placing corporate giants in direct control over all the reins of government in order to make sure that government is compliant to corporate interests as an effective way of boosting the economy. Trump has stated that most of his infrastructure spending will come from private enterprise, and this confederation assures government funding and business funding align.

While this union empowers rapid economic growth, the downside to Trumponomics is that a mixed economy easily sidetracks from its stimulus intentions to becoming the ultimate form of crony capitalism because government and industry become such intimate partners in development that you cannot tell where one begins and the other really ends. That entices a flow of money from public to private interests. The state risks becoming the weaker partner in this arrangement — a mere servant of corporate needs and wants — because those running the state have their former institutions, lifelong friends and their pocket books at heart.

Purportedly, Trumponomics is for the economic betterment of the entire nation, which is accelerated by combining the strength of state and business as a team in a unified direction. (It worked well for Germany after World War I.) I believe the Donald intends it for the best; but another downside is that Government — instead of having purely regulatory roles (congress and the executive branch) and the judicial role — effectively subsidizes certain businesses in creating the projects that government wants to accomplish.

Trump is proposing that government may, for example, pay half the cost of building a bridge while a private contractor pays the other half in exchange for owning the right to collect a toll at the bridge forever. A bridge can support a toll that will be profitable up to a certain cost of construction. Above that cost, no one will pay the toll. So, the government kicks in the full cost above what industry sees as leaving room for an acceptable margin of profit. Government also helps clear the hurdles for construction. That gets a lot more things done quickly, but at what risks?

Trumponomics is a plan for petal-to-the-metal growth; but it leaves no one regulating businesses when business executives are placed in charge of all the regulatory agencies. Another pitfall is that government, instead of simply assuring a level playing field for all businesses, can slip into favoritism toward businesses that are highly regarded by the corporate executives who assume the government reins of power.

Granted, the US hasn’t had a truly free market for decades. The Fed, which is corporately owned, already rigs the economy constantly by enticing banks to soak up government debt at practically no interest with its promises of buying the debt back from its member banks and by creating money that it gives freely to banks to invest in stocks.

Trump, however, is moving the country further in the direction of a mixed economy. Instead of state ownership of the economy (communism), it is corporate ownership of the state by corporate control of state offices, potentially directing them to the opposite end from what those offices were originally created for as regulatory bodies.

I’m not saying corporate leaders should never hold cabinet positions, but when the cabinet is stacked almost entirely in the direction of Trump placing his corporate cronies in power, it looks very problematic, whether they are truly cronies (as in friends) or just a clutch of high-power corporate colleagues.

The early surprise effects of Trumponomics

Trump is already boosting the economy, and he hasn’t even assumed office. His Wall-Street cabinet lineup and his enormous corporate tax gifts (See “Trump: Titan of Corporate Tax Cuts” and “Trump Tax Plan Turns the Donald into Trickle-Down King.”) coupled to his promise that the government will take out huge sums of debt to buy projects from corporate tycoons have all certainly goosed stock-market expectations. Investors now run long with hopes that Trump’s plans will further inflate the stock market bubble to all-time weather-balloon heights.

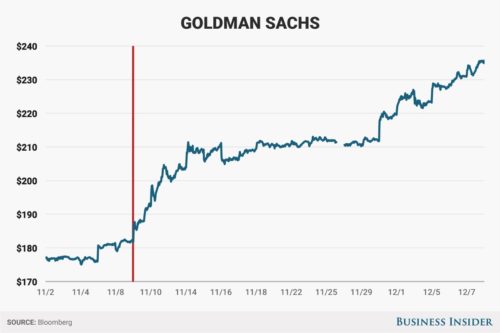

Given how Trump railed against Wall Street in his campaign, it is ironic that Trumponomics has proven most outstanding for Wall Street where bank stocks have risen more than any other sector. Leading the leaders of the pack, Goldman Sachs has absolutely skyrocketed, up a massive 33% since Trump won the election earlier this month:

The financial sector has taken off since the election, on the assumption that a Republican administration will foster a much more lenient regulatory environment than has been in place since the financial crisis…. In particular, Goldman Sachs — a previous employer of several key Trump advisers — has been on a tear…. Indeed, according to legendary trader Art Cashin, about one-third of the postelection increase in the Dow Jones Industrial Average came directly from Goldman Sachs’ performance. (Business Insider)

Three of Trump’s key team members are former Goldman Sachs executives. Several others come from or own other major banks. To be sure, the Trump cabinet looks like a cabal of the world’s biggest bankers, such as you might find meeting in a darkly paneled room at the Hotel de Bilderberg or in Davos, Switzerland.

This all builds a massive amount of steam to power economic growth (and, for that reason, it may be hard for Democrats to totally resist when confirmation time arrives, though they have manifold other reasons to object); but where does the Trump train end up?

To what extent will the corporate interests that now saturate the Trump cabinet come to own government and use its potent economic fuel to power their own engines? Such massive economic changes certainly have the power to change my predicted 2016 schedule for the Epocalypse, made before anyone knew Trump would be the engineer of the nation’s new economic train — vastly different from Obama’s sputtering economy.

That would be good, except I think the Trumponomics train arrives at the same station only with much more momentum as we power headlong into much greater government debt, crewed by a cabinet rife with conflicts of interest and enticements toward self-serving corporate corruption. We are either counting on the sterling reputation of the nation’s biggest bankers and oil barons to resist temptation or on Trump’s mighty ability to keep this rambunctious train on the rails and out of the swamps of corruption while running the locomotive at a head pressure greater than the engine’s normal operating capacity.

Will we say at the end, “How the mighty have fallen?”

Trumponomics ends in a train wreck if it doesn’t end before it even begins.

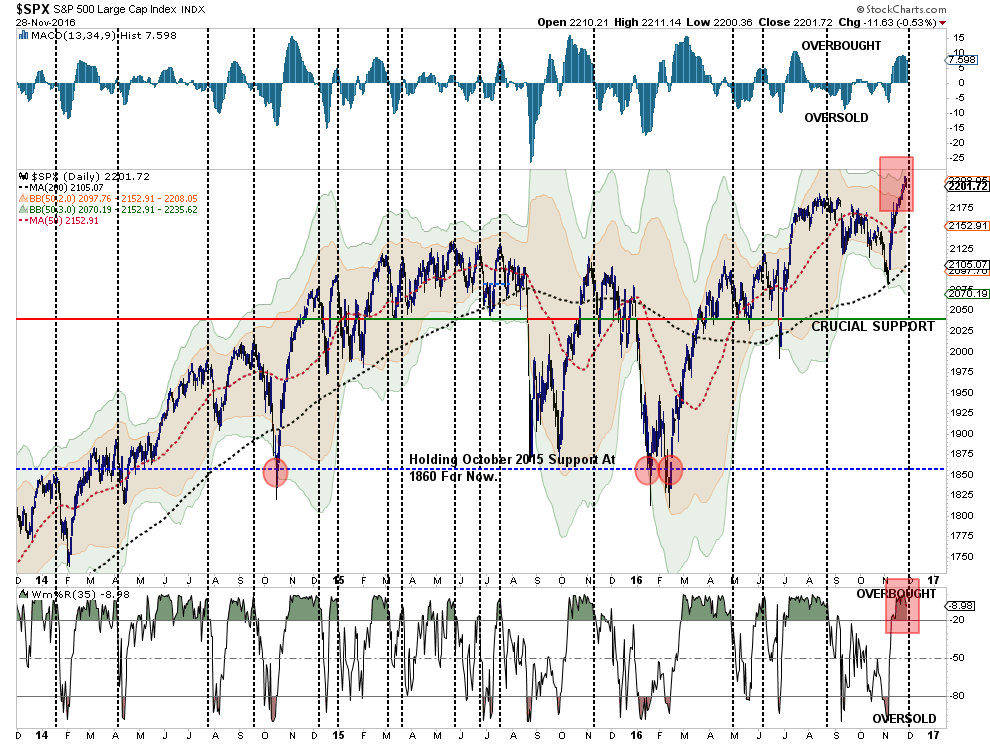

Following the election, the market has surged around the theme of “Trumponomics” as a “New Hope” as tax cuts and infrastructure spending (read massive deficit increase) will fuel earnings growth for companies, stronger economic growth, and higher asset prices. It is a tall order given the already lengthy economic recovery at hand, but like I said, it is “hope” fueling the markets currently.

“First, the market has moved from extremely oversold conditions to extremely overbought in a very short period. This is the first time, within the last three years, the markets have pushed a 3-standard deviation move from the 50-day moving average. Such a move is not sustainable and a correction to resolve this extreme deviation will occur before a further advance can be mounted.Currently, a pullback to the 50-day moving average, if not the 200-dma, would be most likely.”

“Secondly, as discussed above, the advance to ‘all-time highs’ has been narrowly defined to only a few sectors. As shown the number of stocks participating, while improved from the pre-election lows, remains relatively weak and does not suggest a healthy advance.”

….continue to see all the charts and analysis HERE

On Friday, November 25, Fidel Castro died at age 90. The former revolutionary and hardline dictator of Cuba was among the 20th century’s longest-serving leaders, third only to Elizabeth II and Bhumibol Adulyadej, the King of Thailand, who passed away in October.

Castro’s death comes at a pivotal moment in U.S.-Cuban relations. With trade between the two countries on the path to normalization, and with U.S. airlines making scheduled flights to Havana for the first time in more than 50 years, President-elect Donald J. Trump has pledged to reinstate many of the Cold War embargos that were lifted by President Barack Obama.

“If Cuba is unwilling to make a better deal for the Cuban people, the Cuban/American people and the U.S. as a whole, I will terminate deal,” Trump tweeted on November 28.

In light of Castro’s passing, we are rerunning this Frank Talk from March 2015, in which Frank compares and analyzes the widely divergent economies of Cuba and Singapore under their now-deceased leaders, Castro and Lee Kuan Yew.

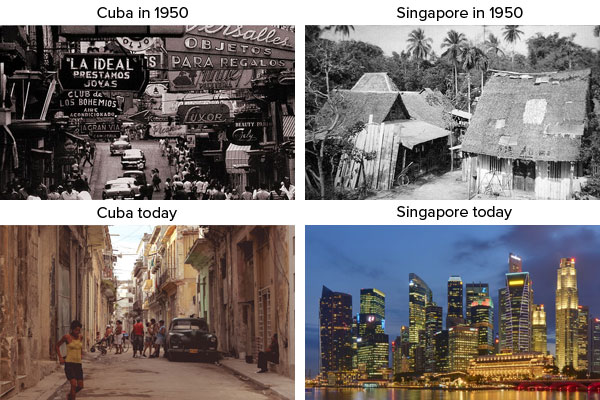

It would be nearly impossible to find two world leaders in living memory whose influence is more inextricably linked to the countries they presided over than Cuba’s Fidel Castro and Singapore’s Lee Kuan Yew, who passed away this Monday at the age of 91.

You might find this hard to believe now, but in 1959—the year both leaders assumed power—Cuba was a much wealthier nation than Singapore. Whereas Singapore was little more than a sleepy former colonial trading and naval outpost with very few natural resources, Cuba enjoyed a thriving tourism industry and was rich in tobacco, sugar and coffee.

Fast forward about 55 years, and things couldn’t have reversed more dramatically, as you can see in the images below.

The ever-widening divergence between the two nations serves as a textbook case study of a) the economic atrophy that’s indicative of Soviet-style communism, and b) the sky-is-the-limit prosperity that comes with the sort of American-style free market capitalism Lee introduced to Singapore.

Sound fiscal policy, a strong emphasis on free trade and competitive tax rates have transformed the Southeast Asian city-state from an impoverished third world country into a bustling metropolis and global financial hub that today rivals New York City, London and Switzerland. Between 1965 and 1990—the year he stepped down as prime minister—Lee grew Singapore’s per capita GDP a massive 2,800 percent, from $500 to $14,500.

Since then, its per capita GDP based on purchasing power parity (PPP) has caught up with and zoomed past America’s.

Under Castro and his brother Raúl’s control, Cuba’s once-promising economy has deteriorated, private enterprise has all but been abolished and the poverty rate stands at 26 percent. According to the CIA’s World Factbook, “the average Cuban’s standard of living remains at a lower level than before the collapse of the Soviet Union.” Its government is currently facing bankruptcy. And among 11.3 million of Cuba’s inhabitants, only 5 million—less than 45 percent of the population—participate in the labor force.

Compare that to Singapore: Even though the island is home to a mere 5.4 million people, its labor force hovers above 3.4 million.

|

Because of the free-market policies that Lee implemented, Singapore is ranked first in the world on the World Bank Group’s Ease of Doing Business list and, for the fourth consecutive year, ranked second on the World Economic Forum’s Global Competitiveness Report. The Heritage Foundation ranks the nation second on its 2015 Index of Economic Freedom, writing:

Sustained efforts to build a world-class financial center and further open its market to global commerce have led to advances in… economic freedoms, including financial freedom and investment freedom.

Cuba, meanwhile, comes in at number 177 on the Heritage Foundation’s listand is the “least free of 29 countries in the South and Central America/Caribbean region.” The Caribbean island-state doesn’t rank at all on the World Bank Group’s list, which includes 189 world economies.

Many successful international businesses have emerged and thrived in the Singapore that Lee created, the most notable being Singapore Airlines. Founded in 1947, the carrier has ascended to become one of the most profitable companies in the world. It’s been recognized as the world’s best airline countless times by dozens of groups and publications. Recently it appeared on Fortune’s Most Admired Companies list.

We at U.S. Global Investors honor the legacy of Lee Kuan Yew, founder of modern-day Singapore. He showed the world that when a country chooses to open its markets and foster a friendly business environment, strength and prosperity follow. Even on the other side of the globe, the American Dream lives on.

The Global Competitiveness Index, developed for the World Economic Forum, is used to assess competitiveness of nations. The Index is made up of over 113 variables, organized into 12 pillars, with each pillar representing an area considered as an important determinant of competitiveness: institutions, infrastructure, macroeconomic stability, health and primary education, higher education and training, goods market efficiency, labor market efficiency, financial market sophistication, technological readiness, market size, business sophistication and innovation.

The Ease of Doing Business Index is an index created by the World Bank Group. Higher rankings (a low numerical value) indicate better, usually simpler, regulations for businesses and stronger protections of property rights.

The Index of Economic Freedom is an annual index and ranking created by The Heritage Foundation and The Wall Street Journal in 1995 to measure the degree of economic freedom in the world’s nations.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. None of the securities mentioned in the article were held by any accounts managed by U.S. Global Investors as of 9/30/2016.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

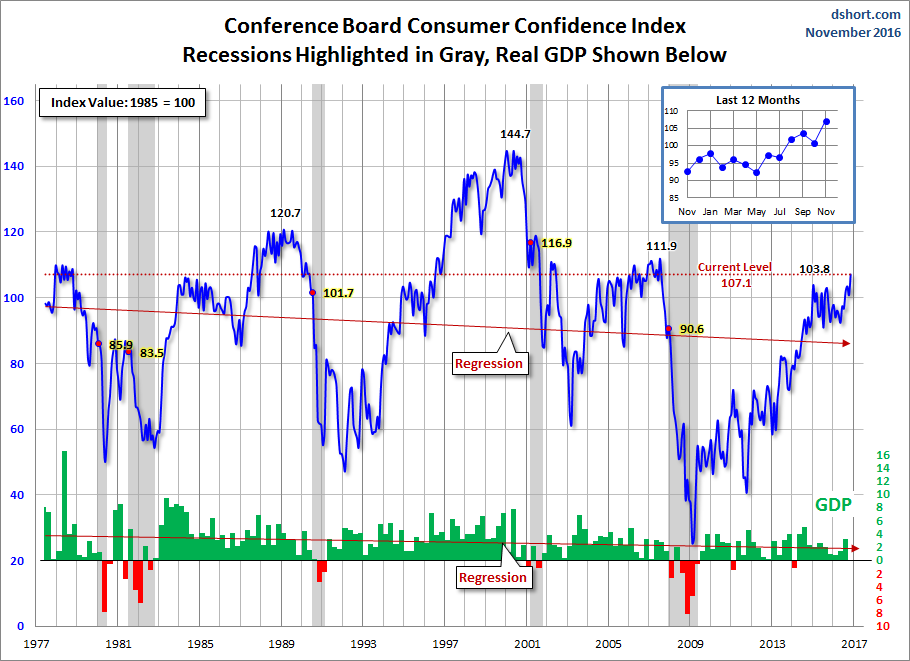

The latest Conference Board Consumer Confidence Index was released this morning based on data collected through November 15. The headline number of 107.1 was an increase from the final reading of 100.8 for October, an upward revision from 98.6. Today’s number was above the Investing.com consensus of 101.2.

The latest Conference Board Consumer Confidence Index was released this morning based on data collected through November 15. The headline number of 107.1 was an increase from the final reading of 100.8 for October, an upward revision from 98.6. Today’s number was above the Investing.com consensus of 101.2.

Here is an excerpt from the Conference Board press release.

“Consumer confidence improved in November after a moderate decline in October, and is once again at pre-recession levels,” said Lynn Franco, Director of Economic Indicators at The Conference Board. (The Index stood at 111.9 in July 2007.) “A more favorable assessment of current conditions coupled with a more optimistic short-term outlook helped boost confidence. And while the majority of consumers were surveyed before the presidential election, it appears from the small sample of post-election responses that consumers’ optimism was not impacted by the outcome. With the holiday season upon us, a more confident consumer should be welcome news for retailers.” Click for larger charts

Putting the Latest Number in Context

….also:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair